SECONDARY MARKET MEANING The market for longterm securities

2. National Stock Exchange")

, Coimbatore")

• The Stock Exchange, Bombay, which was established in 1875")

• The National Stock Exchange of India was set up")

& Global Depository Receipts (GDRs) • Indian companies are permitted")

is a certificate issued by a depository")

• A foreign company can access Indian securities market for")

is a convertible bond")

")

• Traditional brokers are full")

• Discount brokers offer low brokerage, high speed and")

margin • As mandated by SEBI, the Value")

margin- • Marked to Market (MTM) is a margin that is")

The first thing")

done on a")

")

with the help of clearing")

- Slides: 128

SECONDARY MARKET

MEANING • The market for long-term securities like bonds, equity stocks and preferred stocks is divided into primary market and secondary market. • The primary market deals with the new issues of securities. • Outstanding securities are traded in the secondary market, which is commonly known as stock market that predominantly deals in the equity shares. • Debt instruments like bonds and debentures are also traded in the stock market. • Well regulated and active stock market promotes capital formation. Growth of the primary market depends on the secondary market. • The health of the economy is reflected by the growth of the stock market.

Relationship between the Primary and Secondary Markets • The new issue market cannot function without the secondary market. The secondary market or the stock market provides liquidity for the issued securities are traded in the secondary market offering liquidity to the stocks at a fair price. • The stock exchanges through their listing requirements, exercise control over the primary market. The company seeking for listing on the respective stock exchange has to comply with all the rules and regulations given by the stock exchange. • The primary market provides a direct link between the prospective investors and the company. By providing liquidity and safety, the stock markets encourage the public to subscribe to the new issues. • The market ability and the capital appreciation provided in the stock market are the major factors that attract the investing public towards the stock market. Thus, it provides an indirect link between the savers and the company.

• Even though they are complementary to each other, their functions and the organizational set up are different from each other. The health of the primary market depends on the secondary market and vice-versa.

Stock Exchanges • Stock Exchange means any body or individuals whether incorporated or not, constituted for the purpose of assisting, regulating or controlling the business of buying, selling or dealing in securities. • It is an association of member brokers for the purpose of self-regulation and protecting the interests of its members. With the stock exchanges becoming corporate bodies with demutualisation the control and ownership will be in different hands. • The Securities Contracts (Regulation) Act is the basis for operations of the stock exchanges in India. • No exchange can operate legally without the government permission or recognition. • Recognition can be granted to a stock exchange provided certain conditions are satisfied and the necessary information is supplied to the government. Recognition can also be withdrawn, if necessary.

History • The origin of the secondary market i. e. , stock exchanges in India can be traced back to the later half of 19 th century. After the American Civil War (1860 -61) due to the share mania of the public, the number of brokers dealing in shares increased. • The brokers organized an informal association in Mumbai named "The Native Stock and Share Brokers Association" in 1875. • Increased activity in trade and commerce during the First World War and Second War resulted in an increase in the stock trading. Stock exchanges were established in different centers like Chennai, Delhi, Nagpur, Kanpur, Hyderabad and Bangalore. • The growth of stock exchanges suffered a set back after the end of World War. Worldwide depression affected them. Most of the stock exchanges in the early stages had a speculative nature of working without technical strength. • Securities and Contract Regulation Act (SCRA) 1956 gave powers to the central government to regulate the stock exchanges.

• The SCR Act recognized the stock exchanges in Mumbai, Kolkata, Chennai, Ahmedabad, Delhi, Hyderabad and Indore. The Bangalore stock exchange was recognized only in 1963. • At present we have 6 active stock exchanges and 2 commodity exchanges in India. • Till recent past, floor trading took place in all the stock exchanges. In the floor trading system, the trade takes place through open outcry system during the official trading hours. • Trading posts are assigned for different securities where buy and sell activities of securities took place. This system needs a face-to-face contact among the traders and restricts the trading volume. The speed of the new information reflected on the prices was rather slow. The deals were also not transparent and the system favored the brokers rather than the investors. • The setting up of NSE and OTCEI with the screen based trading facility resulted in more and more stock exchanges turning towards the computer based trading.

• Bombay stock exchange introduced the screen based trading system in 1995, which is known as BOLT (Bombay On-line Trading System). Madras stock exchange introduced Automated Network Trading System (MANTRA) on Oct 7 th 1996. Apart from Bombay stock exchange, Vadodara, Delhi, Pune, Bangalore, Calcutta and Ahmadabad stock exchanges have introduced screen based trading. Other exchanges are also planning to shift to the screen based trading.

Stock Exchanges • • • 1. Bombay Stock Exchange (BSE) 2. National Stock Exchange 3. Calcutta Stock Exchange (CSE) 4. Metropolitan Stock Exchange (MSE) 5. India International Exchange (India INX) 6. NSE IFSC Ltd

General info • The Hyderabad Securities and Enterprises Ltd (erstwhile Hyderabad Stock Exchange), Coimbatore Stock Exchange Ltd, Saurashtra Kutch Stock Exchange Ltd , Mangalore Stock Exchange, Inter-Connected Stock Exchange of India Ltd, Cochin Stock Exchange Ltd, Bangalore Stock Exchange Ltd , Ludhiana Stock exchange Ltd, Gauhati Stock Exchange Ltd, Bhubaneswar Stock Exchange Ltd, Jaipur Stock Exchange Ltd, OTC Exchange of India , Pune Stock Exchange Ltd, Madras Stock Exchange Ltd, U. P. Stock Exchange Ltd, Madhya Pradesh Stock Exchange Ltd, Vadodara Stock Exchange Ltd, Delhi Stock Exchange Ltd and Ahmedabad Stock Exchange Ltd have been granted exit by SEBI vide orders dated January 25, 2013, April 3, 2013, April 5, 2013, March 3, 2014, December 08, 2014, December 23, 2014, December 26, 2014, December 30, 2014, January 27, 2015, February 09, 2015, March 23, 2015, March 31, 2015 , April 13, 2015, May 14, 2015, June 09, 2015, November 09, 2015, January 23, 2017 and April 02, 2018 respectively.

Functions of Stock Exchange • Maintains Active Trading: Shares are traded on the stock exchanges, enabling the investors to buy and sell securities. The prices may vary from transaction to transaction. A continuous trading increases the liquidity or marketability of the shares traded on the stock exchanges. • Fixation of Prices: Price is determined by the transactions that flow from investors‘ demand supplier's preferences. Usually the traded prices are made known to the public. This helps the investors to make better decisions. • Ensures Safe and Fair Dealing: The rules, regulations and by-laws of the stock exchanges‘ provide a measure of safety to the investors. Transactions are conducted under competitive conditions enabling the investors to get a fair deal. • Aids in Financing the Industry: A continuous market for shares provides a favorable climate for raising capital. The negotiability and transferability of the securities helps the companies to raise long-term funds. When it is easy to trade the securities, investors are willing to subscribe to the initial public offerings. This stimulates the capital formation.

• Dissemination of Information: Stock exchanges provide information through their various publications. They publish the share prices traded on daily basis along with the volume traded. Directory of Corporate information is useful for the investors' assessment regarding the corporate. Handouts, handbooks and pamphlets provide information regarding the functioning of the stock exchanges. • Performance Induced: The prices of stock reflect the performance of the traded companies. This makes the corporate more concerned with its public image and tries to maintain good performance. • Self-regulating Organization: The stock exchanges monitor the integrity of the members, brokers, listed companies and clients. Continuous internal audit safeguards the investors against unfair trade practices. It settles the disputes between member brokers, investors and sub-brokers.

Demutualisation of Stock Exchanges • Demutualisation is the process by which a customer-owned mutual organization (mutual) or cooperative changes legal structure to form a joint stock company. • Historically stock exchanges started as a mutually governed, self-regulated structures where profit was not a very strong motive. • The stock exchanges were authorized to circulate by-laws to govern their functioning. They were physical locations with trading floors. • The stock exchanges had a mutually dependent, co-operative structure. However with technological innovation came electronic trading system. • The concept of floor trading no longer held ground, hence the physical presence of the trader was no longer important, which in turn meant that the cost of inducting additional member fell drastically, reducing the overall trading cost.

• The basic objective of demutualisation of stock exchanges was to do away with the involvement of brokers in the management of the exchanges and to convert the exchanges into business entities so that they are professionally managed. • The membership fee did not have much of significance. This in turn reduced the importance of mutual dependence and cooperation. The outcome of this was demutualization. • In India OTCEI set up in 1992 and NSE in 1994 made the first attempt at Demutualisation.

Advantages of Demutualization • Firstly, the interests of public and investors can be taken care of better by the vesting of control and regulation in a separate agency other than the trading members. • Secondly, professionalism in Management is possible when non-trading public owns it. • Thirdly, the derivative markets can be controlled and regulated better by professionals and experts. • Fourthly, the larger funds needed by the stock exchanges for infrastructure development and electronic trading can be better accessed from the Capital Market and the public. • Demutualization results in more flexible governance structure fostering decisive action in response to changes in the business environment.

• It leads to greater investor participation in the governance of the exchange. • It yields an improved platform in response to potential competitors in the form of alternative trading systems. • Further, demutualization allows greater flexibility and access to global markets. • It also facilitates faster and more complete consolidation of stock exchanges to enhance available synergies. • And finally, it ensures increased access to resources for capital investment raised by way of equity offerings or private investment

Bombay Stock Exchange (BSE) • The Stock Exchange, Bombay, which was established in 1875 as ‘The Native Share and Stockbrokers' Association, is the oldest Stock Exchange in Asia, even older than the Tokyo Stock Exchange, which was founded in 1878. • The Bombay Stock Exchange is the premier stock exchange in India. • It is the first in the country to be granted permanent recognition under the Securities Contract Regulation Act, 1956 and has an interesting rise to prominence over the past 137 years. • While BSE Ltd is now synonymous with Dalal Street, it was not always so. The first venue of the earliest stock broker meetings in the 1850 s was in rather natural environs - under banyan trees - in front of the Town Hall, where Horniman Circle is now situated. • A decade later, the brokers moved their venue to another set of foliage, this time under banyan trees at the junction of Meadows Street and what is now called Mahatma Gandhi Road. As the number of brokers increased, they had to shift from place to place, but they always overflowed to the streets.

• At last, in 1874, the brokers found a permanent place, and one that they could, quite literally, call their own. The new place was, aptly, called Dalal Street (Brokers' Street). • The journey of BSE Ltd. is as eventful and interesting as the history of India's securities market. In fact, as India's biggest bourse in terms of listed companies and market capitalisation, almost every leading corporate in India has sourced BSE Ltd. services in raising capital and is listed with BSE Ltd. • Even in terms of an orderly growth, much before the actual legislations were enacted, BSE Ltd. had formulated a comprehensive set of Rules and Regulations for the securities market. • It had also laid down best practices which were adopted subsequently by 23 stock exchanges which were set up after India gained its independence. • BSE Ltd. , as a institutional brand, has been and is synonymous with the capital market in India. Its SENSEX is the benchmark equity index that reflects the health of the Indian economy. • It is the 10 th largest stock exchanges in the world by market capitalization.

• BSE is a corporatized and demutualised entity, with a broad shareholderbase which includes two leading global exchanges, Deutsche Bourse and Singapore Exchange as strategic partners. BSE provides an efficient and transparent market for trading in equity, debt instruments, derivatives, mutual funds. • BSE is Asia's first & the Fastest Stock Exchange in world with the speed of 6 micro seconds and one of India's leading exchange groups. • It also has a platform for trading in equities of small-and-medium enterprises (SME). Around 5000 companies are listed on BSE making it world's No. 1 exchange in terms of listed members. • The companies listed on BSE Ltd commanded a total market capitalization of $2. 2 trillion on as of April 2018. • BSE established India INX on 30 December 2016. India INX is the first international exchange of India.

Trading System at BSE • Till Now, buyers and sellers used to negotiate face-to-face on the trading floor over a security until agreement was reached and a deal was struck in the open outcry system of trading, that used to take place in the trading ring. • The transaction details of the account period (called settlement period) were submitted for settlement by members after each trading session. • The computerized settlement system initiated the netting and clearing process by providing on a daily basis statements for each member, showing matched and unmatched transactions. • Settlement processing involves computation of each member's net position in each security, after taking into account all transactions for the member during the settlement period, which was different for different groups of securities. • Now members and their authorized assistants do the trading from their Trader Work Stations (TWS) in their offices, through the BSE On-Line Trading (BOLT) system. • BOLT system has replaced the open out cry system of trading.

National Stock Exchange (NSE) • The National Stock Exchange of India was set up by Government of India on the recommendation of Pherwani Committee in 1991. • Promoted by leading financial institutions essentially led by IDBI at the behest of the Government of India, it was incorporated in November 1992 as a tax-paying company. In April 1993, it was recognized as a stock exchange under the Securities Contracts (Regulation) Act, 1956. • The National Stock Exchange is stock exchange located at Mumbai, India. It is the 11 th largest stock exchanges in the world by market capitalization and largest in India by daily turnover and number of trades, for both equities and derivative trading. • National Stock Exchange has a total market capitalization of more than US$2. 27 trillion, and over 1, 652 listings as of April 2018. • Though a number of other exchanges exist, NSE and the Bombay Stock Exchange are the two most significant stock exchanges in India, and between them are responsible for the vast majority of share transactions.

• The NSE's key index is the S&P CNX Nifty, known as the NSE NIFTY (National Stock Exchange Fifty), an index of fifty major stocks weighted by market capitalisation. • NSE is mutually owned by a set of leading financial institutions, banks, insurance companies and other financial intermediaries in India but its ownership and management operate as separate entities. • NSE commenced operations in the Wholesale Debt Market (WDM) segment in June 1994. The Capital market (Equities) segment of the NSE commenced operations in November 1994, while operations in the Derivatives segment commenced in June 2000. • The stocks trading at the BSE and NSE account for only around 4% of the Indian economy, which derives most of its income related activity from the so-called unorganized sector and households. • Economic Times estimated that as of April 2018, 60 million (6 crore) retail investors had invested their savings in stocks in India, either through direct purchases of equities or through mutual funds.

• NSE is the first exchange in the world to use satellite communication technology for trading. Its trading system, called National Exchange for Automated Trading (NEAT), is a state of-the-art client server based application. At the server end all trading information is stored in an inmemory database to achieve minimum response time and maximum system availability for users. • For all trades entered into NEAT system, there is uniform response time of less than one second.

Euro issue • Firms raise capital by either getting debt or by raising equity. Equity can be raised in the home country or in other international markets. When a firm trades simultaneously in different international market, it is termed as Euro-issues. • Euro issue is a name given to sources of finance or capital available to raise money outside the home country in foreign currency. • The most commonly used sources of funds that fall under Euro issues are American Depository Receipts (ADR), Global Depository Receipts (GDR), and Foreign Currency Convertible Bonds (FCCB) among others. • Rules and regulations for Indian Companies : 1. These issues will be done through depository receipt mechanism. 2. Every Indian company has to get approval from ministry of finance if it has to get money through euro issue. 3. Company must also get approval from RBI under FERA/FEMA laws.

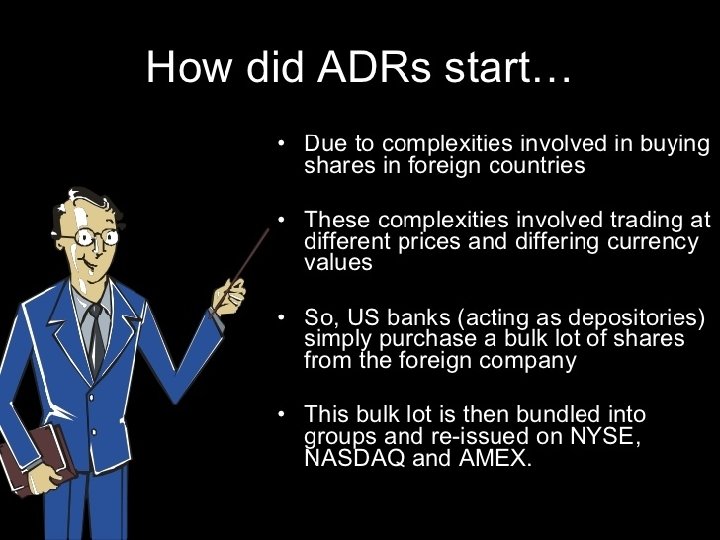

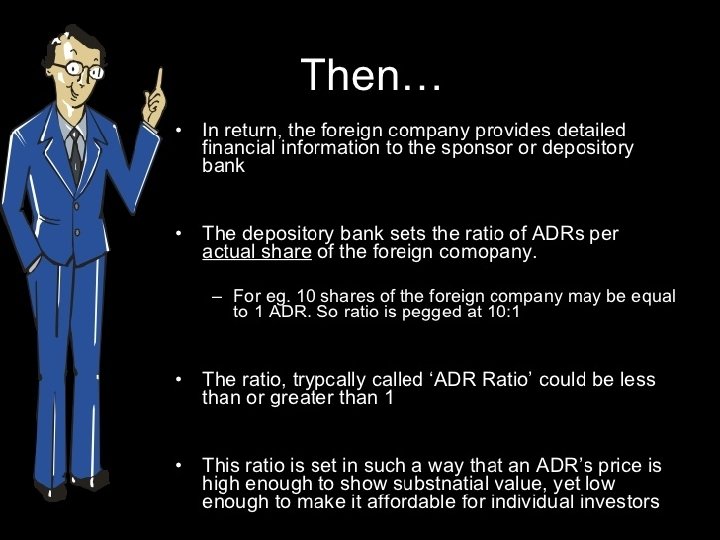

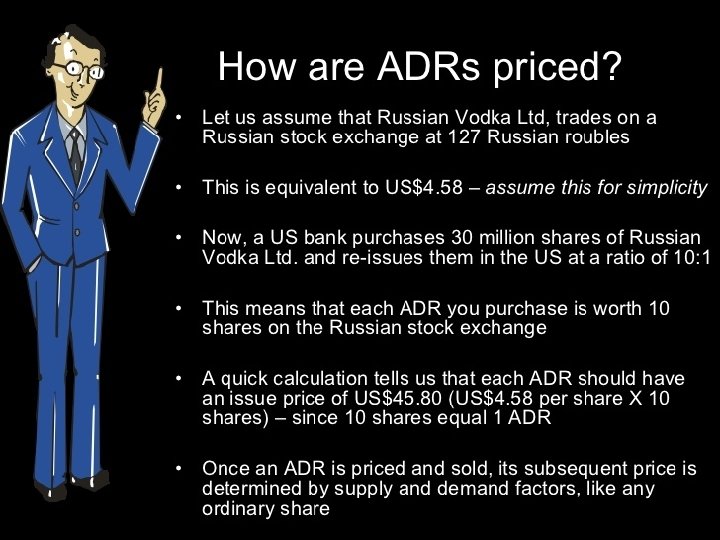

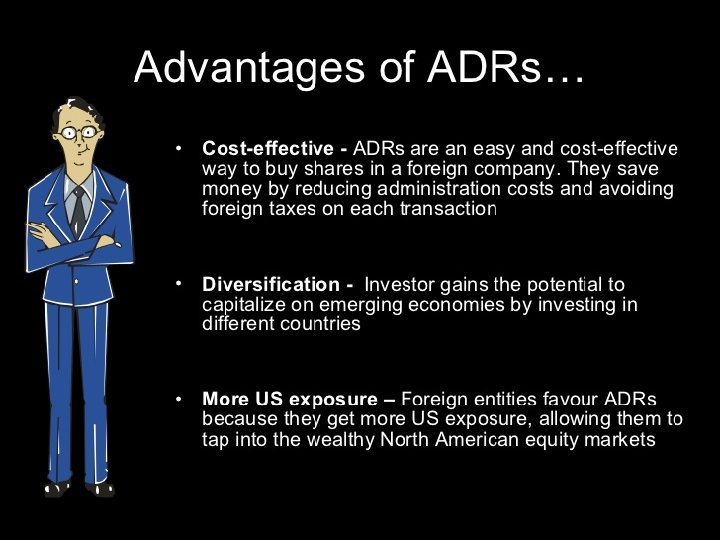

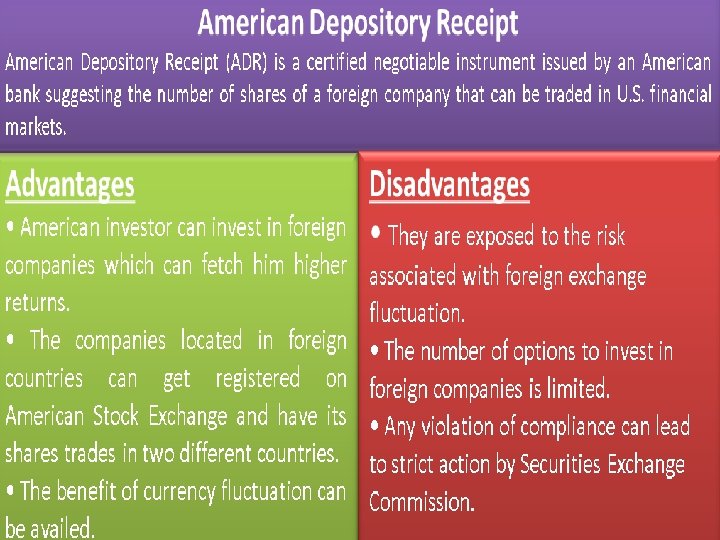

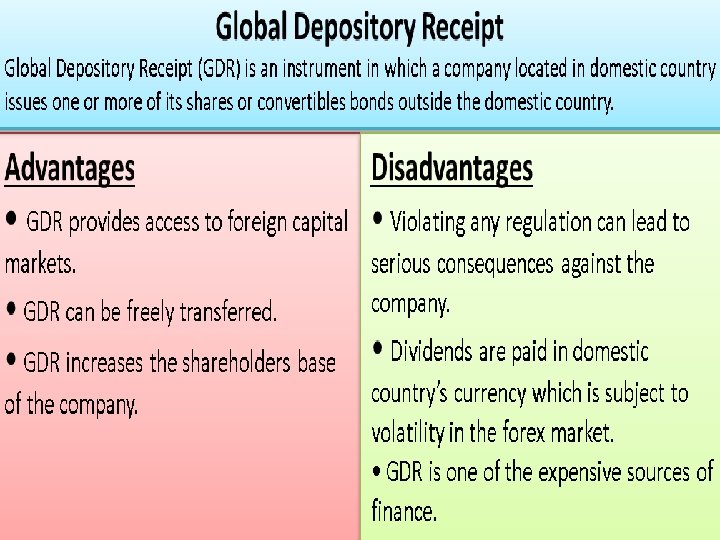

American Depository Receipts (ADRs) & Global Depository Receipts (GDRs) • Indian companies are permitted to raise foreign currency resources through two main sources: 1. Issue of Foreign Currency Convertible Bonds (FCCBs) 2. Issue of Ordinary equity shares through depository receipts, namely, Global Depository Receipts/ American Depository Receipts to foreign investor's i. e. institutional investors or investors residing abroad. • An American depositary receipt (ADR) is a negotiable certificate issued by a U. S. bank representing a specified number of shares (or one share) in a foreign stock traded on a U. S. exchange. • The certificate is issued by an overseas depository bank against certain underlying stocks/shares. • The shares are deposited by the issuing company with the depository bank. The depository bank in turn tenders DRs to the investors.

• This is a financial instrument used by the companies to raise capital in either dollars or Euros. GDRs are also called European Depositary Receipt. • These are mainly traded in European countries and particularly in London. • However, ADRs and GDRs make it easier for individuals to invest in foreign companies, due to the widespread availability of price information, lower transaction costs, and timely dividend distributions.

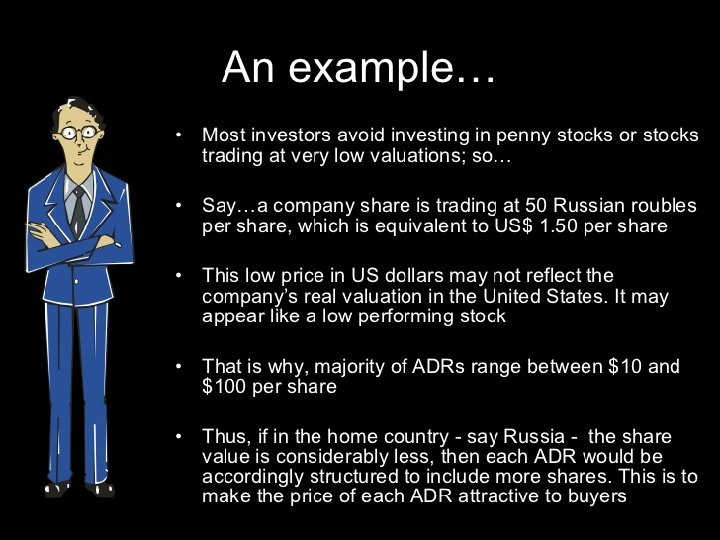

Why do Companies go for ADRs or GDRs? • Indian companies need capital from time to expand their business. If any foreign investor wants to invest in any Indian company, they follow two main strategies. • Either the foreign investors can buy the shares in Indian equity markets or the Indian firms can list their shares abroad in order to make these shares available to foreigners. • But the foreign investors often find it very difficult to invest in India due to poor market design of the equity market. Here, they have to pay hefty transaction costs. • This is an obvious motivation for Indian firms to bypass the incompetent Indian equity market mechanisms and go for the well-functioning overseas equity markets. • When they issue shares in forms of ADRs or GDRs, their shares command a higher price over their prices on the Indian bourses.

• A Depository Receipt represents a particular bunch of shares on which the receipt holder has the right to receive dividend, other payments and benefits which company announces from time to time for the shareholders. • However, it is non-voting equity holding. DRs facilitate cross border trading and settlement, minimize transaction cost and broaden the potential base, especially among institutional investors. • More and more Indian companies are raising money through ADRs and GDRs these days. • ADR holders do not have to transact in foreign currencies, because ADRs trade in U. S. dollars and clear through U. S. settlement systems. • The U. S. banks require that the foreign companies provide them with detailed financial information, making it easier for investors to assess the company's financial health compared to a foreign company that only transacts on international exchanges.

Source- Slideshare

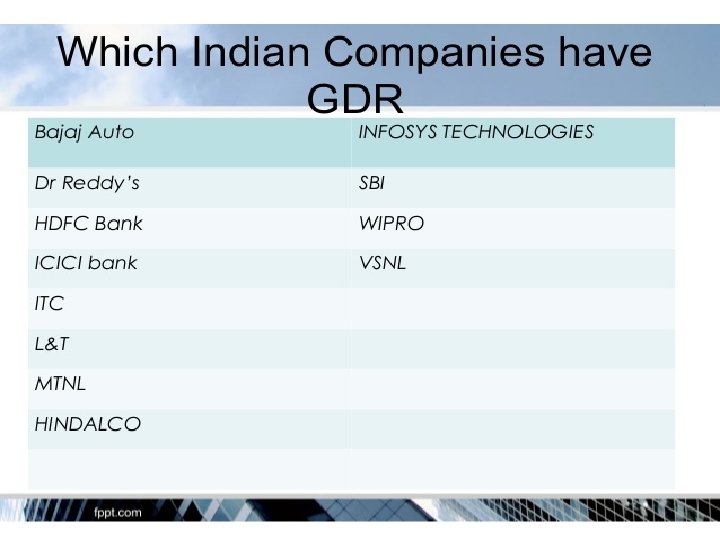

Indian Companies Listed Abroad? • Infosys Technologies was the first Indian company to be listed on NASDAQ in 1999. • However, the first Indian firm to issue sponsored GDR or ADR was Reliance industries Limited. • Beside, these two companies there are several other Indian firms are also listed in the overseas bourses. • These are Wipro, Vedanta, Makemytrip, State Bank of India, Tata Motors, Dr Reddy's Lab, Ranbaxy, Larsen & Toubro, ITC, ICICI Bank, Hindalco, HDFC Bank and Bajaj Auto.

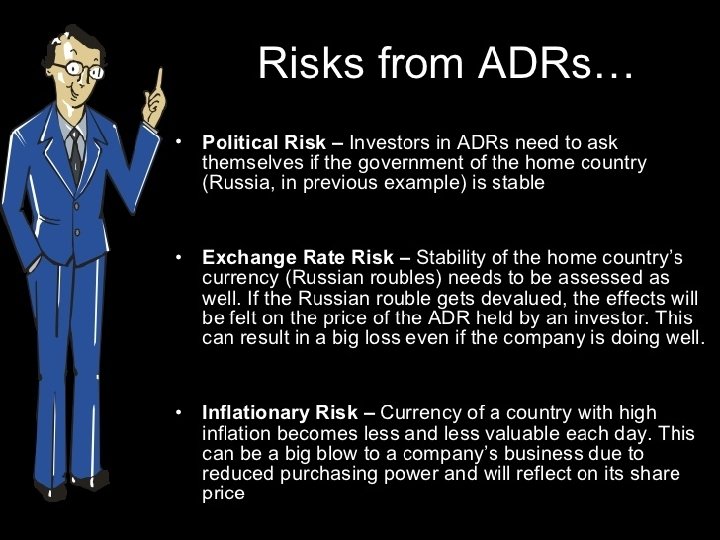

Dividend Payment • ADRs are issued and pay dividends in U. S. dollars, making them a good way for domestic investors to own shares of a foreign company without the complications of currency conversion. • However, this does not mean ADRs are without currency risk. • Rather, the company pays dividends in its native currency and the issuing bank distributes those dividends in dollars -- net of conversion costs and foreign taxes -- to ADR shareholders.

Example • When the exchange rate changes, the value of the dividend changes. or example, let's assume the ADRs of XYZ Company, a French company, pay an annual cash dividend of 3 euros per share. • Let's also assume that the exchange rate between the two currencies is even -- meaning one Euro has an equivalent value to one dollar. XYZ Company's dividend payment would therefore equal $3 from the perspective of a U. S. investor. • However, if the euro were to suddenly decline in value to an exchange rate of one euro per $0. 75, then the dividend payment for ADR investors would effectively fall to $2. 25. • The reverse is also true. If the euro were to strengthen to $1. 50, then XYZ Company's annual dividend payment would be worth $4.

GDR • A global depository receipt (GDR) is a certificate issued by a depository bank, which purchases shares of foreign companies and deposits it on the account. • They are the global equivalent of the original American depository receipts (ADR) on which they are based. • A global depositary receipt (GDR) is similar to an ADR, but is a depositary receipt sold outside the United States and outside the home country of the issuing company. • GDRs represent ownership of an underlying number of shares of a foreign company and are commonly used to invest in companies from developing or emerging markets by investors in developed markets. • Each GDR represents a particular number of shares in a specific company. A single GDR can represent anywhere from a fraction of a share to multiple shares, depending on its design.

Summarized Working

BASIS FOR COMPARISON ADR GDR Acronym American Depository Receipt Global Depository Receipt Meaning ADR is a negotiable instrument issued by a US bank, representing non-US company stock, trading in the US stock exchange. GDR is a negotiable instrument issued by the international depository bank, representing foreign company's stock trading globally. Relevance Foreign companies can trade in US Foreign companies can trade in any stock market. country's stock market other than the US stock market. Issued in United States domestic capital market. European capital market. Listed in American Stock Exchange such as NYSE or NASDAQ Non-US Stock Exchange such as London Stock Exchange or Luxemberg Stock Exchange. Negotiation In America only. All over the world.

Indian Depository Receipts (IDRs) • A foreign company can access Indian securities market for raising funds through issue of Indian Depository Receipts (IDRs). • An IDR is an instrument denominated in Indian Rupees in the form of a depository receipt created by a Domestic Depository (custodian of securities registered with the Securities and Exchange Board of India) against the underlying equity of issuing company to enable foreign companies to raise funds from the Indian securities Markets. • DR are issued by a domestic depository in India and denominated in Rupees. It represents an ownership interest in a fixed number of underlying equity shares of the Issuing Company. These shares are called Deposited Shares. • Standard Chartered Bank created history in the Indian Capital Market by becoming the first foreign company to come up with an IDR issue.

• According to Sebi guidelines, the minimum bid amount in an IDR issue is Rs 20, 000 per applicant. • Like in any public issue in India, resident Indian retail (individual) investors can apply up to an amount of INR 2, 000 and non-institutional investors (also called high-net-worth individuals) can apply above INR 1, 000 but up to applicable limits.

Foreign Currency Convertible Bond FCCB • A bond is a debt instrument that provides income to investors in the form of regular scheduled interest payments called coupons. • At the maturity date of the bond, the investors are repaid the full face value of the bond. Some corporate entities issue a type of bond known as convertible bonds. • A foreign currency convertible bond (FCCB) is a type of convertible bond issued in a currency different than the issuer's domestic currency. • A bondholder with a convertible bond has the option of converting the bond into a specified number of shares of the issuing company. • Convertible bonds have a conversion rate at which the bonds will be converted to equity. • In other words, the money being raised by the issuing company is in the form of a foreign currency. • A convertible bond is a mix between a debt and equity instrument. It acts like a bond by making regular coupon and principal payments, but these bonds also give the bondholder the option to convert the bond into stock.

• • • A foreign currency convertible bond (FCCB) is a convertible bond that is issued in a foreign currency, which means the principal repayment and periodic coupon payments will be made in a foreign currency. For example, an American listed company that issues a bond in India in rupees has, in effect, issued an FCCB. Foreign currency convertible bonds are typically issued by multinational companies operating in a global space and looking to raise capital in foreign currencies. A company may decide to raise money outside its home country to gain access into new markets for new or expansionary projects. FCCBs are generally issued by companies in the currency of those countries where interest rates are usually lower than the home country or the foreign country economy is more stable than the home country economy. An FCCB investor can purchase these bonds at a stock exchange, and has the option to convert the bond into equity or a depositary receipt after a certain period of time. Investors can participate in any price appreciation of the issuer’s stock by converting the bond to equity.

Depositories • The Indian Capital Markets were notorious for their outdated ways of doing business. • It was a major relief when NSE and BSE had introduced on line trading that transformed the trading from scream based to screen based. • But the clumsy procedures of handling share certificates and the recurring problem of bad deliveries made life horrendous not for just an amateur investor but even for a professional broker. With the paper work nightmare looming large, securities business was never a pleasant job. • That's till; the new method of holding stocks in the electronic form was introduced in 1996. • The new system called a depository was put in place to hold stocks of all companies in electronic form on behalf of the investors and maintain a record of all "buy" and "sell“ transactions.

• The organization responsible for holding and handling securities on behalf of investors is known as a Depository. • It caters to both large and small investors through a network of intermediaries called Depository Participants or DPs for short. • Depository is a technology driven electronic storage system. It completely does away with cumbersome paper work relating to share certificates, transfer forms etc. , involved in securities business. • It caters to investor's transactions with greater speed, efficiency and ease as it deals with all stocks in just a book entry mode and not in their physical form. • In India, National Securities Depository Limited (NSDL) as a joint venture between IDBI, UTI and the National Stock Exchange has set up the first depository. • The second depository has been set up by Central Depository Services Limited (CDSL), which was promoted by the Bombay Stock Exchange and Bank of India. • Both the depositories have a network of Depository Participants (DPs) who are electronically connected to the depository and serve as contact points with the investors.

Depositories - Glossary • Depository: A depository like a bank, safe keeps your securities in electronic form. Besides holding securities, it provides various services related to transactions in securities • Dematerialization: Dematerialization or Demat for short, is a process where securities held by you in physical form are cancelled and credited to your DP account in the form of electronic balances. • Depository Participant (DP): A depository participant is an intermediary between the investor and the Depository who is authorized to maintain your accounts of dematerialized shares. Presently only financial institutions, banks, custodians, clearing corporations, stockbrokers and non-banking finance companies are permitted to become DPs. You can choose any of them as your DP. You can also have accounts with more than one DP like you may have accounts with more than one bank.

Advantages of holding shares in Demat form 1. 2. 3. 4. 5. 6. First and foremost, you don't have to chase errant brokers to rectify cases of bad deliveries, company objections or fake, forged or stolen shares. No tedious correspondence with the Registrars for transfer of shares in your name. The depository itself would do all transfers instantly. Your cost of transactions would be less, as you don't have to pay for the stamp duty on transfer of shares. Even the brokerage you pay is less if you are buying or selling shares in demat form. You will be rid of the hassles in handling and safekeeping volumes of paper. No nightmares like loss, theft, mutilation or forgery of share certificates.

Stock Price Indices • An index is a number that measures the change in a set of values over a period of time. • A stock index is a way of measuring the performance of a group of stocks as a single number. • A stock index represents the change in value of a set of stocks, which constitute the index. • A good stock market index is one, which captures the behavior of the overall equity market. • It should represent the market, it should be well diversified and yet highly liquid. • A good market index should have three attributes: 1. It should capture the behavior of a large variety of different portfolios in the market. 2. The stocks included in the index should be highly liquid. 3. It should be professionally maintained.

Types of Indices • Most of the commonly followed stock market indexes are of the following two types- market capitalization weighted index or price weighted index. 1. Price Weighted Index: this method, an index value is calculated on the basis of the company’s stock price, and not market capitalization. Stocks with higher prices have greater weightage in the index than stocks with lower prices. • Company Share price at time 0 at time 1 (Rs. ) • Grasim Inds 351. 55 340. 50 • Telco 329. 10 350. 30 • SBI 274. 60 280. 40 • Wipro 1335. 25 1428. 75 • Bajaj 539. 25 570. 25 • Total 2829. 75 2970. 20

• In the present example the base index = 1000 • Index = (2970. 20/2829. 75) x 1000 = 1049. 56

Market capitalisation based index • Market capitalisation is an important parameter which many investors consider while putting money in a company. • Market capitalisation is the outstanding number of shares of a company multiplied by its current market price. • For example, if a company has 1 lakh outstanding shares and the stock price is Rs 20, then the market capitalization of the company is Rs 20 lakh. • Capitalization-weighted index, also called a market-value-weighted index, is a stock market idex whose components are weighted according to the total market value of their outstanding shares. • Every day an individual stock's price changes and thereby changing a stock index's value. The impact that individual stock's price change has on the index is proportional to the company's overall market value (the share price multiplied by the number of outstanding shares), in a capitalizationweighted index. •

• Example: Suppose an index contains two stocks, A and B. A has a market capitalization of Rs. 1000 crore and B has a market capitalization of Rs. 3000 crore. Then we attach a weight of 1/4 to movements in A and 3/4 to movements in B. • There are two types of market capitalization that you could have. One is the total market capitalization, which is simply called market capitalization and the other is the free float market capitalization.

2. Market Capitalization Weighted Index: Market capitalization is the total market value of a company’s stock. This is calculated by multiplying the share price of a stock with the total number of stocks floated by the company. It thus takes into consideration both the size and the price of the stock. • In an index using market-cap weightage, stocks are given weightage on the basis of their market capitalization in comparison with the total market-capitalization of the index. The point to remember is that market capitalization changes every day as the stock price fluctuates. For this reason, a stock’s weightage too changes every day. • Index = (Current market capitalization/ Base market capitalization) x Base value Company Current Market capitalization Base Market capitalization Grasim Inds 1, 668, 791. 10 1, 654, 247. 50 Telco 872, 686. 30 860, 018. 25 SBI 1, 452, 587. 65 1, 465, 218. 80 Wipro 2, 675, 613. 30 2, 669, 339. 55 Bajaj 660, 887. 85 662, 559. 30 Total 7, 330, 566. 20 7, 311, 383. 40

What is "free-float market capitalization"? • Free-float Methodology refers to an index construction methodology that takes into consideration only the free-float market capitalization of a company for the purpose of index calculation and assigning weight to stocks in the Index. • Many different types of investors hold the shares of a company. The Govt. may hold some of the shares. Some of the shares may be held by the “founders” or “directors” of the company. Some of the shares may be held by the FDI’s etc! • Now, only the “open market” shares that are free for trading by anyone, are called the “free-float” shares. When we are calculating the Sensex, we are interested in these “free-float” shares. • A simple way to understand the “free-float market cap” would be, the total cost of buying all the shares in the open market.

• ü ü • Free float market capital would exclude the following: 1) Shares that are locked in. 2) Shares that are held by the promoters. 3) Shares that have been acquired through Foreign Direct Investment route. 4) Shares that are held by the government. Free-float market capitalization takes into consideration only those shares issued by the company that are readily available for trading in the market. It generally excludes promoters' holding, government holding, strategic holding and other locked-in shares that will not come to the market for trading in the normal course. . • A Free-float based index is regarded as a better benchmark in comparison to a full market capitalization weighted index. It not only reflects the market trends in a more rational manner, but also aids both active and passive investing styles.

• In the present example, the base index = 1000 and the index value works out to be 1002. 60 • Index = (7330566. 20/7311383. 40) x 1000 = 1002. 62

Major Advantages of Free-float Methodology 1. 2. 3. 4. A Free-float index reflects the market trends more rationally as it takes into consideration only those shares that are available for trading in the market. Free-float Methodology makes the index more broad-based by reducing the concentration of top few companies in Index. A Free-float index aids both active and passive investing styles. It aids active managers by enabling them to benchmark their fund returns vis-àvis an investible index. Being a perfectly replicable portfolio of stocks, a Free-float adjusted index is best suited for the passive managers as it enables them to track the index with the least tracking error. Free-float Methodology improves index flexibility in terms of including any stock from the universe of listed stocks. This improves market coverage and sector coverage of the index. For example, under a fullmarket capitalization methodology, companies with large market capitalization and low free-float cannot generally be included in the Index because they tend to distort the index by having an undue influence on the index movement.

5. Globally, the free-float Methodology of index construction is considered to be an industry best practice. ü Both NSE and the BSE use the free float market capitalisation method to calculate their benchmark indices Nifty and Sensex respectively and assigning weight to stocks in the index. So a company with a higher free float has a higher weightage on the indices.

Full float-market capitalization • Total/Full float market capitalization based index is calculated by multiplying the number of shares outstanding by their current price. • Market capitalization equals a company's share price times the number of shares it has outstanding. • Market cap is the value that the investment community places on a company. Here is a simple example of a three-stock index weighted by market capitalization.

Basis of Inclusion in the Index • Every six months, the constituents of the Nifty and Sensex are reviewed, leading to replacement of some stocks. Criterion for inclusion in index is as follows: 1. Market Capitalization : The Security should figure in the Top 100 companies listed by full market capitalization. In case of Sensex, the weight of each S&P BSE SENSEX Security based on free-float should be at least 0. 5% of the Index. (Market Capitalization would be averaged for last six months) 2. Trading Frequency : The Security should have been traded on each and every trading day for the last one year. Exception can be made for extreme reasons like Security suspension etc. 3. Average Daily Trades : In case of Sensex, the Security should be among the Top 150 companies listed by average number of trades per day for the last one year.

4. 5. 6. 7. Average Daily Turnover : The Security should be among the Top 150 companies listed by average value of shares traded per day for the last one year. Listed History : In case of Sensex, the Security should have a listing history of at least one year on BSE. Securities from all major sectors of economy should be included in the index. When a stock is replaced by another stock in the index, the index divisor is adjusted so the change in index market value that results from the inclusion and exclusion does not change the index level.

How corporate actions impact stock price ? 1. BONUS SHARES These are additional shares gifted by a company to its shareholders. A 1: 1 bonus issue implies that shareholders get one additional share for each share that they already hold. Generally, when a company faces liquidity issues or is not in a position to distribute the dividends, it issues bonus shares out of its profits or reserves. But there are no free lunches. In case of a bonus issue, the share price of the company falls in the same proportion. 2. RIGHTS ISSUE In a rights issue, fresh shares are issued by a company to its existing shareholders. But unlike bonus shares, they come at a price— usually a discounted price. To illustrate, a 1: 5 rights issue implies that you are entitled to buy one additional share for every five shares you hold. “Cashstrapped companies generally turn to a rights issue to raise money”.

• Impact : The share price falls in the same proportion as the rights issue. 3. STOCK SPLIT It refers to a split in the stock into two or more equal portions. Stock splits are generally announced by companies to make their shares affordable to small retail investors and thus make them more liquid. • The stock is split keeping in mind its face value—not market value. For instance, if the stock’s face value is Rs 10, and there is a 1: 1 split, its face value will change to Rs 5. • Impact : The share prices gets slashed in the accordance with the stock split ratio. • IMP- A value weighted index like S&P needs no adjustment for stock split. On the other hand price based index like DJIA needs adjustment as it considers only the prices. The adjustment is made by changing the divisor so that the position before stock split and immediately after stock split is not altered.

Bulls and Bears

Basics 1. What are Bear? • Bear : An operator who expects the share price to fall • Bear Market : A weak and falling market where buyers are absent 2. What are Bulls? • Bull : An operator who expects the share price to rise and takes position in the market to sell at a later date. • Bull Market : A rising market where buyers far outnumber the sellers • A bull market is one where prices are rising, whereas a bear market is one where prices are falling. The two terms are also used to describe types of investors. • A common story is that the terms ‘Bull market’ and ‘Bear market’ are derived from the way those animals attack. Bulls are supposed to be aggressive and attacking while bears would wait for the prey to come down.

1. BULL MARKETS • When can you say it’s a bull market? When the prices of stocks moves up rapidly cracking previous highs , you may assume that it’s a bull market. • If there are many bullish days in a row you can consider that as a ‘bull market run’. Technically a bull market is a rise in value of the market by at least 20%. 2. BEAR MARKETS • A bear market is the opposite of a bull market. When the prices of stocks moves crashes rapidly cracking previous lows , you may assume that it’s a bear market. • Generally markets must fall by more than 20% to confirm that it’ a bear market.

What Drives Bear and Bull Markets? 1. 2. 3. 4. The stock market is affected by many economic factors. High employment levels, strong economy, and stable social and economic conditions generally build investor confidence and encourage investors to put their money in the stock market. Often, this can bolster bull markets. Also, new technologies and companies that encourage investors to put their money in stocks can create bull markets. For example, in the 1990 s, the dot com craze encouraged many investors to put their money in stocks that they felt would keep increasing. In some cases, a bullish market is simply self-perpetuating. Since the market is doing well, it only encourages investors to invest more money or to start investing. On the other hand, discouraging economic or social political changes in a society can push the market down.

5. 6. Sudden instability or unemployment -- or even fears of unemployment caused by wars and other problems -- can start to make investors more conservative and therefore lead to bear markets. Of course, again this becomes a self-perpetuating trend. As the economy slows down, companies begin downsizing. Increased unemployment makes people far less willing to gamble on the stock market. Sometimes, a panic caused by dire predictions about the market can also create bearish conditions.

How To Predict Bear and Bull Markets? 1. 2. 3. 4. The easiest way to predict both types of markets is to realize that what goes up must come down. That is, if the market is rising, then you know that at some point it will start to fall again. Similarly, if the market is currently falling, you can be certain that eventually it will pick up again. There are no precise ways to predict either bull or bear markets, although general social economic situations can help you to determine what will happen. A country which wages a war will experience bullish market conditions as government contracts create more jobs and boost investor confidence if their expectation is to win. Sudden international crises push the market downward and create bearish conditions. News is very often a good indicator of where investors are headed. The reports will inform about loss of investor confidence as well as sudden economic downturns that may affect the market.

5. If one notices from stock market research that several indices have changed by 15% to 20%, you can be sure that market direction is changing. When you notice such changes, it is time to sit up and take notice. You may be headed for a bullish or bearish market.

Factors influencing the movement of stock markets • Movements in the stock market can be quite volatile and sometimes movements in share prices can seem divorced from economic factors. However, there are certain underlying factors which have a strong influence on the movement of share prices and the stock market in general. 1. 2. Economic growth. Higher economic growth or better prospects for growth will help firms be more profitable because there will be more demand for goods and services. This will help boost company dividends and therefore share prices. Interest rates. Lower interest rates can make shares more attractive for two reasons. Lower interest rates help boost economic growth making firms more profitable. Also, lower interest rates make shares relatively more attractive than saving money in a bank or holding bonds. If bond yields fall, it may encourage investors to switch into shares which give a relatively better dividend.

4. Stability. Stock markets dislike shocks that could threaten economic stability and future growth. Therefore, they will tend to fall on news of terrorist attacks or spikes in the price of oil. They will also dislike political instability which may make it difficult to pursue strong economic policies. 4. Confidence and expectations. A key factor is the mood of investors. If they receive economic news that gives optimism then they are more likely to buy shares. If they receive bad news they will sell. This is why in the depth of a recession, stock markets can start to rise. Investors are always trying to predict the future. Therefore if they feel the worst is over – the stock market can rally – even when economic fundamentals remain poor. 4. Bandwagon effect. At times the stock market seems to over-react to certain events. Even today it remains a little mystery why the stock market fell so much – there was no economic problem. In fact, the stock market soon recovered it’s lost ground. Part of the issue is that people follow the mood. When prices fall, people may feel the need to follow suit and get out of the market.

7. Related markets. Often investors have choices. For example, rather than investing in stock market, they could buy government bonds or commodities. If investors feel government bonds are overpriced and likely to fall, then the stock market can benefit as people move into shares. 8. Price to earnings ratios. Some investors and economists, feel the best guide to the long-term performance of shares is their price to earnings ratios. If share prices rise significantly above historical averages, then this is a sign that shares are becoming overvalued and are due a correction at some point in the future. 9. Inflation- Inflation means higher consumer prices. This often slows sales and reduces profits. Higher prices will also often lead to higher interest rates. For example, the RBI may raise interest rates to slow down inflation. These changes will tend to bring down stock prices. 10. Deflation- Falling prices tend to mean lower profits for companies and decreased economic activity. Stock prices may go down, and investors may start selling their shares and move to fixed-income investments like bonds. Interest rates may be lowered to encourage people to borrow more. The goal is increased spending and economic activity. 11. Appreciation or Depreciation of currency

Role of a Stock Broker 1. 2. 3. 4. 5. 6. A stockbroker is a person or a company that acts as an intermediary between buyers and sellers of stocks. A stock broker is an agent who represents clients to buy or sell stocks and other securities. When the Stockbroker acts as agent for the buyers and sellers of securities, a commission is charged for this service. As an agent the stock broker is merely performing a service for the investor. This means that the broker will buy for the buyer and sell for the seller, each time making sure that the best price is obtained for the client. The term is applied to both companies that deal in securities and their employees, who technically are registered representatives working for the brokerage. To most investors, however, the broker is the person they call when they want to invest in or trade stocks. Most individual brokers work in offices far removed from the stock trading floors.

7. An investor should regard the stockbroker as one who provides valuable service and information to assist in making the correct investment decision. 8. They are adequately qualified to provide answers to a number of questions that the investor might need answers to and to assist in participating in the regional market. 9. Stock brokers are governed by SEBI Act, 1992, Securities Contracts (Regulation) Act, 1956, Securities and Exchange Board of India [SEBI (Stock brokers and Sub brokers) Rules and Regulations, 1992], Rules, Regulations and Bye laws of stock exchange of which he is a member as well as various directives of SEBI and stock exchange issued from time to time. 10. Every stock broker is required to be a member of a stock exchange as well as registered with SEBI. 11. Every broker displays registration details on their website and on all the official documents. 12. “Sub-broker” means any person not being a member of a Stock Exchange who acts on behalf of a member-broker as an agent or otherwise for assisting the investors in buying, selling or dealing in securities through such member-brokers.

Types of Brokers 1. Full Service Brokers (Traditional Brokers) • Traditional brokers are full service brokers offering trading (stocks, commodities and currency), research and advisory, investment banking, sales and asset management under one umbrella. • They also allow investing in Forex, Mutual Funds, IPOs, FDs, Bonds and Insurance. In some cases full-service brokers also have in-house banking and demat account services. • India has over 10, 000 traditional retail brokers. They are 'advisors' for the client and at the same time salesmen for the financial products. ICICIDirect, Kotak Security, HDFC Sec, Sharekhan, Motilal. Oswal, India Infoline are some of the full-service brokers.

2. Discount Brokers (Budget Brokers) • Discount brokers offer low brokerage, high speed and the state-of-the-art execution platform for trading in stocks, commodities and currency derivatives. • Discount "Online-Service" brokers usually allow clients to trade of their own with little or no interaction with a live broker. Discount brokers could be a better choice for the fee-conscious investor who prefers to go it alone. • They are also known as online brokers who offer savings of 80 -90% on brokerage. • India has around 15 discount brokers including Pro. Stocks, Zerodha, RKSV etc.

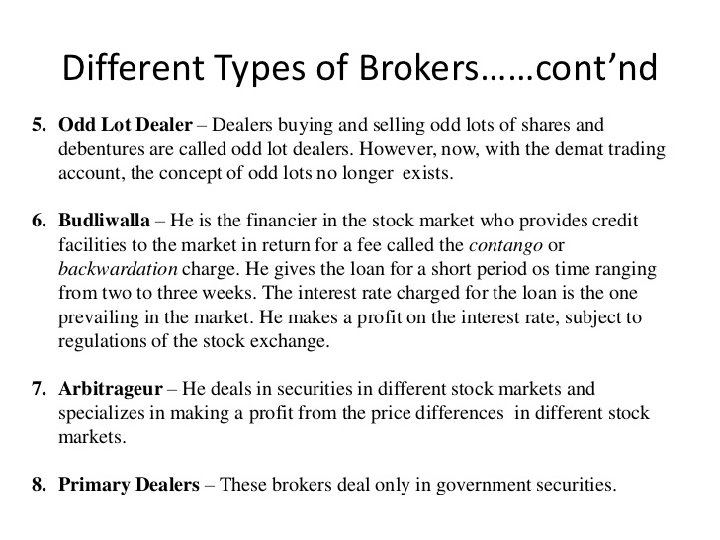

Sub Types 1. Floor brokers • They execute orders for other brokers and receive a share in the brokerage commission that a commission broker charges to his client. 2. Commission brokers • They execute orders of their customers by buying and selling securities on the exchange. They charge a specified commission on the purchase or sale value. They are registered members of stock exchange. A commission broker does not buy or sell securities in his own name. They deal with many clients and consequently with many securities. 3. Jobbers • They are professional independent brokers/ speculators engaged in buying and selling of specified securities in their own name. Jobbers cannot deal on behalf of public and are barred from taking commission. They deal or resell to brokers who in turn transact on behalf of the public. A jobber deals in a limited number of securities which he tracks regularly.

Types of Brokers contd • Jobbers generally quote two prices, one at which he is prepared to purchase and the other at which he is prepared to sell a security. This two way price is known as ‘double-barrelled price’. 4. Tarawaniwalas • Most of the Big brokers who deal on their own account on the stock exchange are termed as Tarawaniwallas. They are the High Net Worth Brokers who can make or break a market price

Selection of a Broker • A stock broker is a registered professional who buys and sells stocks or shares in the secondary market on behalf of their clients or investors. • An individual or company who wants to buy or sell stock must go through a broker since only they are authorized to perform these transactions. • A stock broker needs to be a financial expert who is aware of the market and market conditions that control the stock price. • Brokers should also have excellent judgment and foresight to offer the right advice to clients based on their financial needs and their ability to bear risk. • In return for their services, brokers are paid a commission called brokerage that is based on each transaction or the total trade value. • The National Stock Exchange (NSE) and the Bombay Stock Exchange (BSE), among other institutes, offer certified courses in stock brokering. These courses are related to capital markets, investment, financial planning, equity research, securities and portfolio analysis and other certificate courses.

• One of the criteria for becoming a stock broker in India is to have a minimum of two years’ work experience at a stock brokering firm or in a field related to securities or financial services. • One of the criteria the Securities Exchange Board of India (SEBI) considers while evaluating applications for a stock broker is whether the candidate has the required office space, equipment and manpower to work effectively as a stock broker. • If one intends to become an online stock broker, he/she must provide a reliable online stock trading platform that offers access to stock exchanges and depositories and functions without technical glitches. • Stock brokers in India are governed by the SEBI Act of 1992, which requires stock brokers to first register with SEBI, who will evaluate their application to see if they are eligible to become a stock broker before issuing them a registration certificate.

• Besides registering with the SEBI, stock brokers must become members of one or more stock exchanges such as the NSE and the BSE. The application forms are closely evaluated by the exchanges before granting membership. Most major exchanges require stock brokers to pay a security deposit and a membership fee, which usually involve a considerable expense.

Requirement of Base Minimum Capital for Stock Broker • The Capital Adequacy requirements shall consist of the following two components: 1. 2. 3. The Base Minimum Capital (BMC) is the deposit maintained by the member of a stock exchange against which no exposure for trades is allowed. It is meant for meeting contingencies in any segment of the exchange and commensurate with the risks that the broker may bring to the system. The BMC deposit requirement prescribed for the different profiles ranges has been increased from Rs. 10 Lacs to Rs. 50 lakhs for members of stock exchanges having nation-wide trading terminals. Minimum 50 per cent of the deposit shall be in the form of cash and cash equivalents.

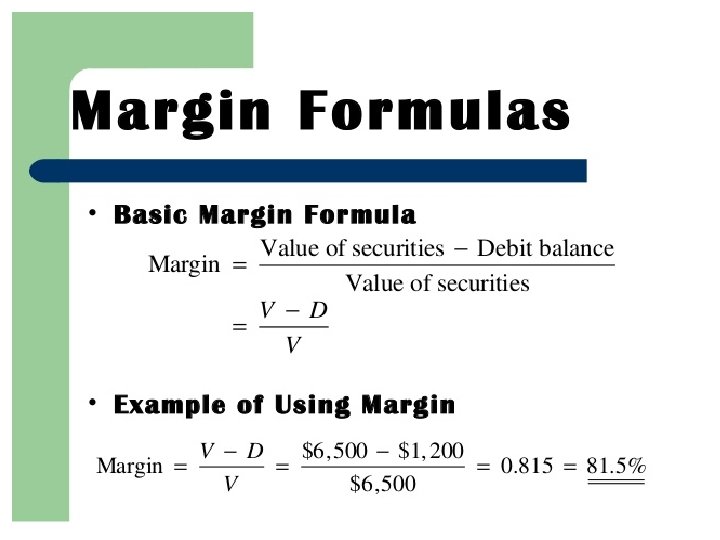

Margin Requirement • Just as we are faced with day to day uncertainties pertaining to weather, health, traffic etc and take steps to minimize the uncertainties, so also in the stock markets, there is uncertainty in the movement of share prices. This uncertainty leading to risk is sought to be addressed by margining systems by stock markets. • In order to contain the risk arising out of transactions entered into by the members in various securities either on their own account or on behalf of their clients, stock exchanges have a well designed risk-management system which inter-alia, includes collection of margins from the Members. • They accordingly impose various kinds of margins on the Members based on their outstanding positions in the market. • A Margin Requirement is the percentage of marginable securities that an investor must pay for with his/her own cash.

• Suppose an investor, purchases 1000 shares of ‘xyz’ company at Rs. 100/on January 1, 2008. Investor has to give the purchase amount of Rs. 1, 000/- (1000 x 100) to his broker on or before January 2, 2008. • Broker, in turn, has to give this money to stock exchange on January 3, 2008. There is always a small chance that the investor may not be able to bring the required money by required date. • As an advance for buying the shares, investor is required to pay a portion of the total amount of Rs. 1, 000/- to the broker at the time of placing the buy order. • Stock exchange in turn collects similar amount from the broker upon execution of the order. This initial token payment is called margin. Remember, for every buyer there is a seller and if the buyer does not bring the money, seller may not get his / her money. • Margin is levied on the seller also to ensure that he / she gives the 100 shares sold to the broker who in turn gives it to the stock exchange. • Margin payments ensure that each investor is serious about buying or selling shares

• In the above example, assume that margin was 15%. That is investor has to give Rs. 15, 000/-(15% of Rs. 1, 000/) to the broker before buying. Now suppose that investor bought the shares at 11 am on January 1, 2008. Assume that by the end of the day price of the share falls by Rs. 25/-. That is total value of the shares has come down to Rs. 75, 000/-. • That is buyer has suffered a notional loss of Rs. 25, 000/-. In our example buyer has paid Rs. 15, 000/- as margin but the notional loss, because of fall in price, is Rs. 25, 000/-. • That is notional loss is more than the margin given. In such a situation, the buyer may not want to pay Rs. 1, 000/ - for the shares whose value has come down to Rs. 75, 000/-. S • Similarly, if the price has gone up by Rs. 25/-, the seller may not want to give the shares at Rs. 1, 000/-. • To ensure that both buyers and sellers fulfill their obligations irrespective of prices movements, notional losses also need to be collected. • Prices of shares may keep on moving every day. Margins ensure that buyers bring money and sellers bring shares to complete their obligations even though the prices have moved down or up.

• volatility essentially refers to uncertainty arising out of price changes of shares

Types of margins 1. Initial Margin • Initial Margin is the capital sum which an investor needs to park with his broker as a down payment in its account to initiate trades. This acts as a collateral. An investor can offer cash and securities or other collateral like open ended Mutual fund as collateral to enter into a trade. • In most cases, especially for equity securities, the initial margin requirement is 30 % or exchange defined margin whichever is higher, but this may vary. And yes, both buyers and sellers must put up a payment to enter into a trade. 2. Maintenance Margin • After purchasing the stocks, a minimum balance called as maintenance margin needs to be parked with the broker. In case the margin drops below the limit, your broker will make a margin call and can also liquidate the position if you do not make up for the requirement amount

3. Value at Risk (Va. R) margin • As mandated by SEBI, the Value at Risk (Va. R) margining system, which is internationally accepted as the best margining system, is applicable on the outstanding positions of the members in all scrips. • Va. R is a technique used to estimate the probability of loss of value of an asset or group of assets (for example a share or a portfolio of a few shares), based on the statistical analysis of historical price trends and volatilities. • In the stock exchange scenario, a Va. R Margin is a margin intended to cover the largest loss (in %) that may be faced by an investor for his / her shares (both purchases and sales) on a single day with a 99% confidence level. The Va. R margin is collected on an upfront basis (at the time of trade). • Va. R Margin is at the heart of margining system for the cash market segment. Va. R margin is collected on upfront basis.

Example • Let us assume that an investor bought shares of a company. Its market value today is Rs. 50 lakhs. Obviously, we do not know what would be the market value of these shares next day. An investor holding these shares may, based on Va. R methodology, say that 1 -day Va. R is Rs. 4 lakhs at the 99% confidence level. This implies that under normal trading conditions the investor can, with 99% confidence, say that the value of the shares would not go down by more than Rs. 4 lakhs within next 1 -day.

4. Mark-to-Market (MTM) margin- • Marked to Market (MTM) is a margin that is collected from a stockbroker over and above the regular initial margin if a trader wishes to carry a position to the next day under the circumstances that the closing price is not in favor of the trader. • This margin is specific to Derivative Segment of both equity and commodities market and particularly for Futures Trading. • MTM is calculated at the end of the day on all open positions by comparing transaction price with the closing price of the share for the day. • Example- A buyer purchased 1000 shares @ Rs. 100/- at 11 am on January 1, 2008. If close price of the shares on that day happens to be Rs. 75/-, then the buyer faces a notional loss of Rs. 25, 000/ - on his buy position. In technical terms this loss is called as MTM loss and is payable by January 2, 2008 (that is next day of the trade). • In case price of the share falls further by the end of January 2, 2008 to Rs. 70/-, then buy position would show a further loss of Rs. 5, 000/-. This MTM loss is payable.

• In case, on a given day, buy and sell quantity in a share equal, that is net quantity position is zero, but there could still be a notional loss / gain (due to difference between the buy and sell values), such notional loss also is considered for calculating the MTM payable. • MTM Profit/Loss = [(Total Buy Qty X Close price) - Total Buy Value] [Total Sale Value - (Total Sale Qty X Close price)]

Example • Assume on 1 st Dec 2014 at around 11: 30 AM, you decide to buy Hindalco Futures at Rs. 165/-. The Lot size is 2000. 4 days later on 4 th Dec 2014 you decide to square off the position at 2: 15 PM at Rs. 170. 10/-. Clearly as the calculation below shows, this is a profitable trade – • • • Buy Price = Rs. 165 Sell Price = Rs. 170. 1 Profit per share = (170. 1 – 165) = Rs. 5. 1/Total Profit = 2000 * 5. 1 = Rs. 10, 200/However, the trade was held for 4 working days. Each day the futures contract is held, the profits or loss is marked to market. While marking to market, the previous day closing price is taken as the reference rate to calculate the profit or losses.

Day Closing Price 1 st Dec 2014 168. 3 2 nd Dec 2014 172. 4 3 rd Dec 2014 171. 6 4 th Dec 2014 169. 9 • On Day 1 at 11: 30 AM the futures contract was purchased at Rs. 165/-, clearly after the contract was purchased the price has gone up further to close at Rs. 168. 3/-. Hence profit for the day is 168. 3 minus 165 = Rs. 3. 3/per share. Since the lot size is 2000, the net profit for the day is 3. 3*2000 = Rs. 6600/-. • Hence the exchange ensures (via the broker) that Rs. 6600/- is credited to your trading account at the end of the day. • But where is this money coming from? – Obviously it is coming from the counterparty. Which means the exchange is also ensuring that the counterparty is paying up Rs. 6600/towards his loss

• On day 2, the futures closed at Rs. 172. 4/-, clearly another day of profit. The profit earned for the day would be Rs. 172. 4/ – minus Rs. 168. 3/- i. e. Rs. 4. 1/- per share or Rs. 8, 200/- net profit. The profits that you are entitled to receive is credited to your trading account and the buy price is reset to the day’s closing price i. e. 172. 4/-. • On day 3, the futures closed at Rs. 171. 6/- which means with respect to the previous day’s close price there is a loss to the extent of Rs. 1600 /- (172. 4 – 171. 6 * 2000 ). The loss amount will be automatically debited from your trading account. Also, the buy price is now reset to Rs. 171. 6/-. • On day 4, the trader did not continue to hold the position through the day, but rather decided to square off the position mid day 2: 15 PM at Rs. 170. 10/ -. Hence with respect to the previous day’s close he again made a loss. That would be a loss of Rs. 171. 6/- minus Rs. 170. 1/- = Rs. 1. 5/- per share and Rs. 3000/- (1. 5 * 2000) net loss. Needless to say after the square off, it does not matter where the futures price goes as the trader has squared off his position. Also, Rs. 3000/- is debited from the trading account by end of the day.

Day 1 st Dec 2014 2 nd Dec 2014 3 rd Dec 2014 4 th Dec 2014 Ref Price for M 2 M 165 168. 3 172. 4 171. 6 & 170. 1 Total Closing Price 168. 3 172. 4 171. 6 169. 9 Daily M 2 M + Rs. 6, 600/+Rs. 8, 200/-Rs. 1, 600/– Rs. 3, 000/+Rs. 10, 200/- So, the mark to market is just a daily accounting adjustment where – Money is either credited or debited (also called daily obligation) based on how the futures price behaves The previous day close price is taken into consideration to calculate the present day M 2 M v M 2 M is a daily cash adjustment by means of which the exchange drastically reduces the counterparty default risk. As long a trader holds the contract, the exchange by virtue of the M 2 M ensures both the parties are fair and square on a daily basis.

HOW TO TRADE IN INDIAN SHARE MARKET 1. 2. 3. a) The first thing one needs to be able to invest in shares in India is a PAN card. We cannot directly go the stock exchange and buy or sell stocks/shares like we would buy or sell any other thing. People are authorized to buy and sell on the markets and they are called brokers. Brokers can be individuals or companies and even online agencies that are registered and licensed by SEBI or Securities and Exchanges Board of India, who regulates the share markets. Once you have a broker, whether in form of a person, company or online, you will now need a Demat and Trading account. Demat account will hold the stocks or shares in your name and the same will reflect in your stock portfolio. You cannot hold shares in physical form or store them physically. They have to in Dematerialized state or Demat state.

• A Demat account does that for you. It will store the shares you buy from the markets through your brokers in your account in your name. The selling will also be from here and it will reflect in your Demat statements that you receive from time to time. You will never have a physical share certificate in your hands; it will be reflected in your Demat Account Statement. b) The buying and selling of shares you wish to have or want to sell will however require a Trading account will be like an intermediary who facilitates the buying and selling. Usually your broker takes care of all this. • Whether you approach an individual broker, a broking firm or online agencies, the Demat and Trading accounts will be opened simultaneously as it is one without the other is useless for investing in shares in India. 4. There is also a Depositary Participant that you need to be aware of. There are two depositories in India: NSDL and CDSL which stands for National Securities Depository Limited and Central Depository Services Limited. These two have their agents in the form of Depository Participants who will provide an account to store the shares you hold.

• It is not the same as Demat and Trading account as in Demat it shows the number shares you hold and the Trading reflects the buying and selling that has taken place in your account. Depository Participants will hold those shares you bought and release the shares you sold. • However, it is usually taken care of by the broker who will also guide you through the Demat, Trading account opening process as well as register with a Depository. 5. A broker usually buys or sells shares on an individual’s behalf. For example, if you want to buy the shares of Microsoft and you want to buy it at Rs. 450, you let your broker know exactly how many shares you want to buy and the price you’re willing to pay for it. • You must also let the broker know on which exchange you want to buy the shares. So, if you want 10 shares of Microsoft at Rs. 450 each, your broker will buy them when the shares reach that price.

Margin Trading 1. 2. 3. 4. 5. When an investor borrows money from his broker to buy stocks, the process is called margin trading. Margin is a way of increasing your purchasing power for investments. Buying on margin means that you take a loan from your broker to increase the amount of funds you have at your disposal to invest. The loan comes with its own costs in the form of interest and there are limitations on how you use the loaned funds. If you wish to go for trade in margin then you need to have a margin account. Once your margin account gets activated, then you can borrow up to 50% of the purchase price of the stock. For Example : You have Rs 5000 to invest and are interested in the shares of Sport Sun Shoes, selling at Rs 50 per share. If you use only your own funds to make the investment, you can buy 100 shares of the company. But you decide to get your broker to lend you another Rs 5000. You can now buy 200 shares with an initial investment of just Rs 5000 from your side.

6. Let’s say the price of the Sports Sun shares goes up to Rs 100. If you had invested only your own Rs 5000, your investment would now be worth 100 shares x Rs 100 = Rs 10, 000. Your return on investment in this case will be 100%. 7. But as you had bought the shares on margin, adding the broker’s Rs 5000 to your own funds, your investment is now worth 200 shares x Rs 100 = Rs 20, 000. You have doubled your investment’s value with an outlay of the same Rs 5000 from your side. 8. Of course, you will still have to pay back the Rs 5000 plus interest and other applicable charges on the margin, but even after deducting that amount, you will be left with much more profit than you would have if you had not used margin. Your return on investment in this case will be 200%. 9. This example shows how using margin at the right time and with the right investments can multiply the gains you stand to get with your investment. 10. However, the most important thing to understand about margin trading is that it not only amplifies your gains, but also your losses. In the same example, if the stock price had fallen, you would lose much more when you use margin trading. This is the reason why margin trading is considered quite risky

11. In order to trade with a margin account, you are first required to place a request with your broker to open a margin account. This requires you to pay a certain amount of money upfront to the broker in cash, which is called the minimum margin. This would help the broker recover some money by squaring off, should the trader lose the bet and fail to recuperate the money. 12. Once the account is open, you are required to pay an initial margin (IM), which is a certain percentage of the total traded value pre-determined by the broker.

• Below are certain terms that would make the concept more clear. i. Initial margin: The proportion of total purchase price an investor is supposed to deposit for opening a margin account is referred as its initial margin and is generally 50% of the total value. ii. Maintenance margin: In order to keep the margin account open for doing margin trading, it is necessary to maintain minimum cash or marginable securities which is called the maintenance margin. This is just to prevent an investor from incurring a level of debt that he would not be able to repay. iii. Margin call: If your account falls below the maintenance margin, your broker will make a margin call to ask you to deposit more cash or securities into your account. If case you fail to meet the margin call, your broker will sell your securities so to make up for the stipulated maintenance requirement. • Margin calls are triggered when a fall in the value of the stocks reduces the net value of the portfolio (value of stocks less borrowed funds) and makes it necessary to bring in additional funds or securities to meet the maintenance margin specified. The lender retains the right to liquidate the position if the requirements are not met.

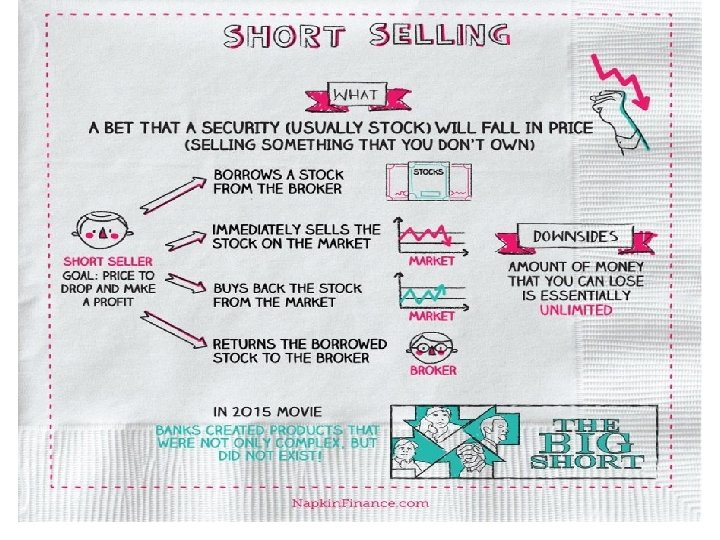

Short Selling • “Buy low and sell high” is a popular phrase used in investing. Shorting is the opposite. It’s the sale of a security with the expectation that its value will fall in the future. If the price falls, the seller can then buy it back at a lower price and make a profit. • A short is therefore a bet that a security will decrease in value. • Short-selling, in the context of the stock market, is the practice where an investor sells shares that he does not own at the time of selling them. • He sells them in the hope that the price of those shares will decline, and he will profit by buying back those shares at a lower price. • In India, there is no prohibition on short-selling by retail investors. • Institutional investors —domestic mutual funds and foreign institutional investors registered with the Securities and Exchange Board of India, banks and insurance companies — are prohibited from short-selling and are mandatorily required to settle on the basis of deliveries of securities owned and held by them.

How it works 1. 2. 3. 4. 5. 6. The short seller borrows the stock from someone else so that they can sell it. The short seller agrees to return the borrowed stock on a specific date in the future. The short seller then sells the stock on the market. When the specific date comes up, the short seller must return the stock that was borrowed. The short seller then buys that stock on the market at its new price. The goal for the short seller is for the price to drop and make a profit. If the price goes up for the stock, the short seller must pay the difference. For example- if a trader thinks that Apple’s stock, which is trading at $50, will decline in price, he can borrow 100 shares and then sell them. Since the trader sold something that he did not have in the first place, he is “short” 100 shares of Apple. A few weeks later, however, when Apple’s stock falls to $30, the trader can buy 100 shares of it and gain a profit of $2, 000.

Return on margin to a shortseller • Return on margin= Value of security on sale- Value of security on purchase. Dividend Amount Invested

Margin Adjustment • Since the price of the security bought or sold by the investor for a margin varies in the market from time to time, there is an adjustment requires in the margin to be kept by the investor with the broker. • This adjustment is called ‘marking to market’ i. e. margin is adjusted in such a manner so as to align with the prevailing price of the security in the market. • This is done because the brokers too have to maintain a margin with the stock exchange for all deals done by them. • Since these maintenance margins change with variation in prices of the securities, the brokers too follow the same concept with the investors who want to transact at a margin. • Example from Rakesh Shahni

Contract Note • A Contract note is a confirmation of trade(s) done on a particular day for and on behalf of a client. • A contract note issued in the format and manner prescribed by NSE establishes a legally enforceable relationship between the trading member and client in respect of settlement of trades executed on the exchange as stated in the contract note. • Contract notes are made in duplicate, and the member and client keep a copy each. The said contract notes should be signed by a trading member or by an authorised signatory of the trading member. • After verifying the details contained therein, the second copy of the contract note should be returned to the trading member, duly acknowledged by the investor. • The important usage of contract notes is mentioned below: 1. Computation of total capital gains/ losses for the purpose of return filing 2. Computation of the total brokerage charged by the trading member 3. In a case of failure in the delivery of stock, contract note is a legal proof for an arbitration or dispute resolution.