Principles of Accounting II Asst Prof Dr Panchat

. . . AC. Date")

. . . AC. Date")

• Sales Return Journal")

Cr. Sale")

xx")

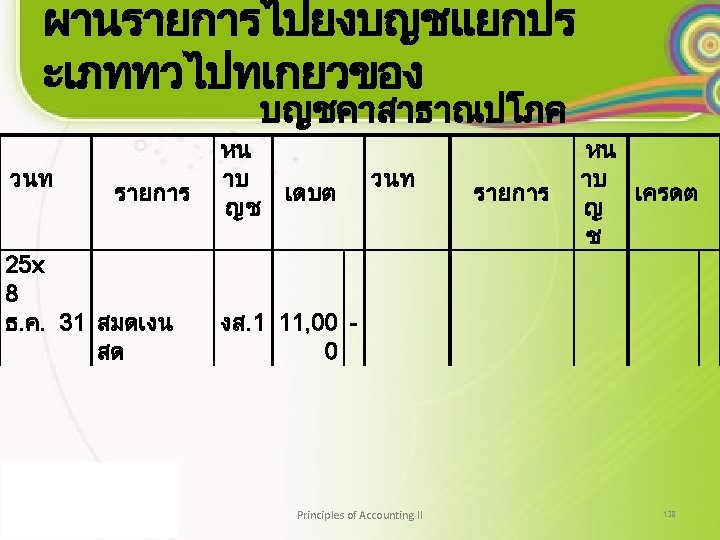

1( Date (3) Page) 2( Dr. Cr. Voucher Accounts Credit Ac.")

")

xx Cash in")

1 Date Ac Voucher name NO. Cr. Dr. Discretion Cash")

Vat of")

1( Date Invoice No. Name Accounts Payable (3) (4) (5) Page)")

")

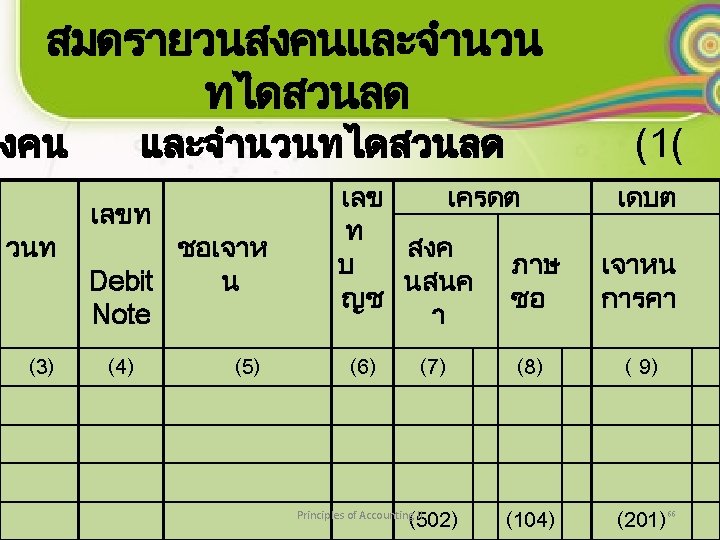

1( Date (3) Debit Note No (4)")

1 Date (3) Voucher No. (4) Account Name Description Dr.")

- Slides: 139

Principles of Accounting II Asst. Prof. Dr. Panchat Akarak p. thipnew 1@hotmail. com School of Accounting Chiang Rai Rajabhat University Principles of Accounting II 1

Accounting Systems and Special Journals Outline 1. Control Accounts and Subsidiary Ledgers 2. Special Journals 3. Alternative Methods of Processing data Principles of Accounting II 2

Accounting Systems and Special Journals Learning Objectives 1. Describe the relationship between subsidiary accounts in subsidiary ledgers and control accounts in the general ledger. 2. Describe the relationship between special journals and the general journal. 3. Describe computer applications in business. Principles of Accounting II 3

1. The Processing of Data Manual System 1. An accounting system can be defined as a set of records such as; -Journals, (สมดรายวน ) -Ledgers, (บญชแยกประเภท ) -Trial balances (งบทดลอง) -Work sheets, and (กระดาษทำการ ) -Financial reports, (รายงานทางการเงน /งบการเงน ) plus the procedures and equipment regularly used to process business transactions Principles of Accounting II 4

1. The Processing of Data Manual System 2. For accounting systems to be effective, they should: a. Provide for the efficient processing of data at the least cost, The cost of the system should be equal to or less than the benefits received. b. Ensure a high degree of accuracy. c. Provide for internal control to prevent theft or fraud. d. Provide for the growth of a business. Principles of Accounting II 5

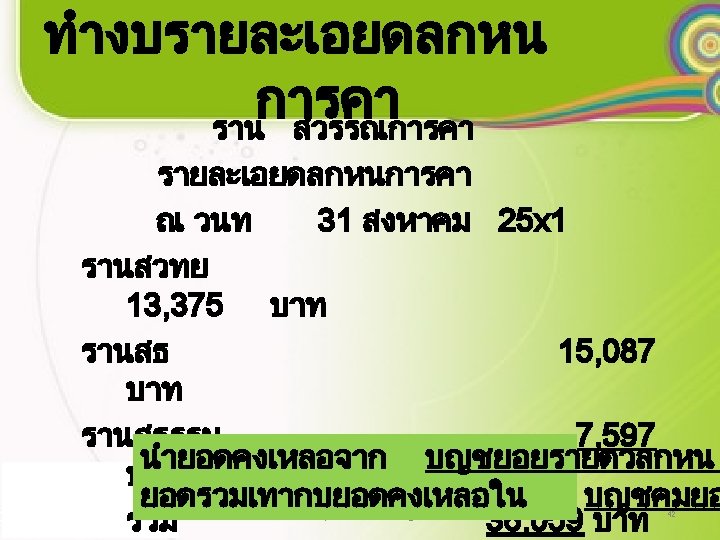

2. Control Accounts and Subsidiary Ledgers • The method of initially recording and summarizing transaction data is influenced by the nature of the transactions, the materiality of the amounts, the means available for processing the data, and the reports desired. a. Sometimes a company need general information and at other times it needs specific information b. In order to provide for both types of information, control accounts are maintained to provide balance sheet data and subsidiary accounts are maintained to provide specific information relating to customers and creditors. Principles of Accounting II 6

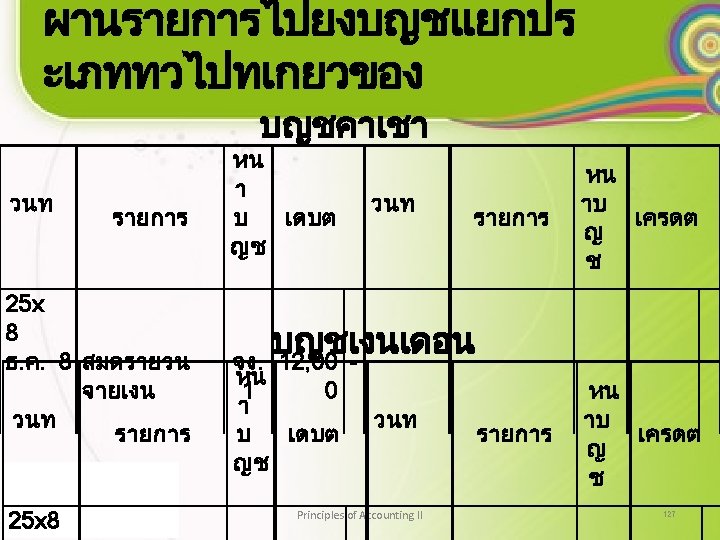

3. Control Accounts • A Control account is an account in the general ledger that shows the total balance of all the subsidiary accounts related to it. general ledger…. No…. Date Description Page No. Dr. Date Description amount Principles of Accounting II Page No. Cr. amount 7

4. Subsidiary Ledger Accounts • Subsidiary ledger accounts show the details supporting the related general ledger control account balance. Principles of Accounting II 8

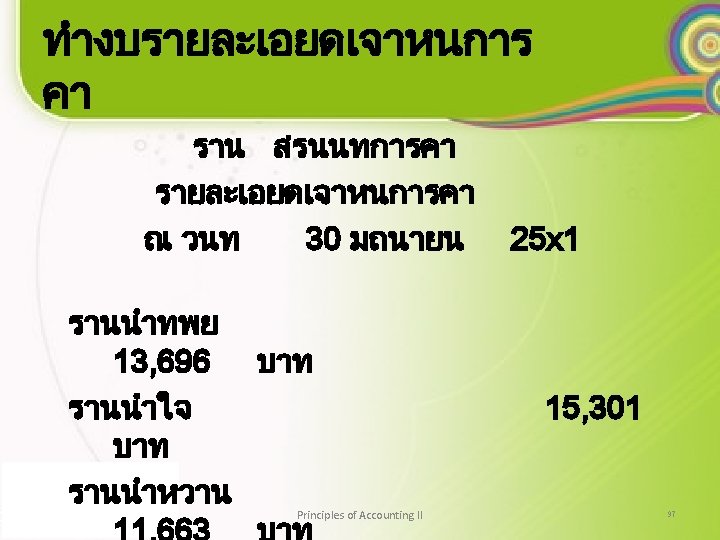

5. Subsidiary Ledger • A subsidiary ledger is a group of related accounts showing the details of the balance of the general ledger control account. a. A subsidiary ledger relives the general ledger of a mass of detail and shortens the general ledger trial balance. b. A subsidiary ledger promotes a division of labor. Principles of Accounting II 9

5. Subsidiary Ledger Accounts Receivable name. . . . (1). . . AC. Date Description Dr. Page (2) (3) (4) (5) Principles of Accounting II Page). . . 2. . . ( Cr. (6) Balance (7) 10

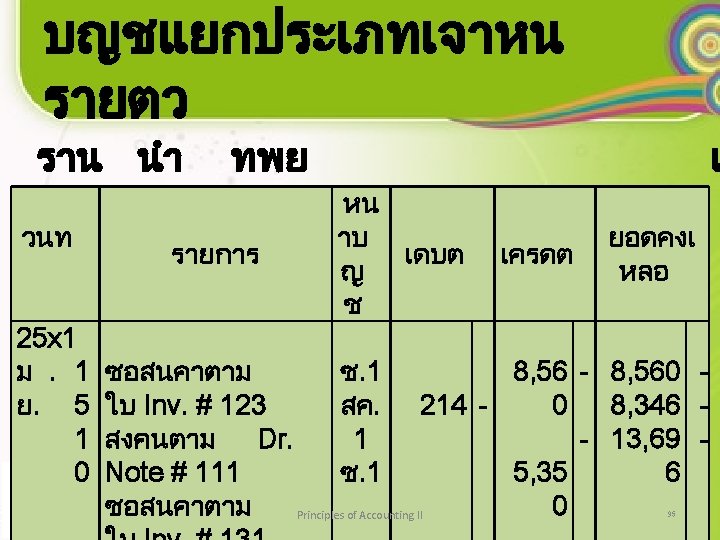

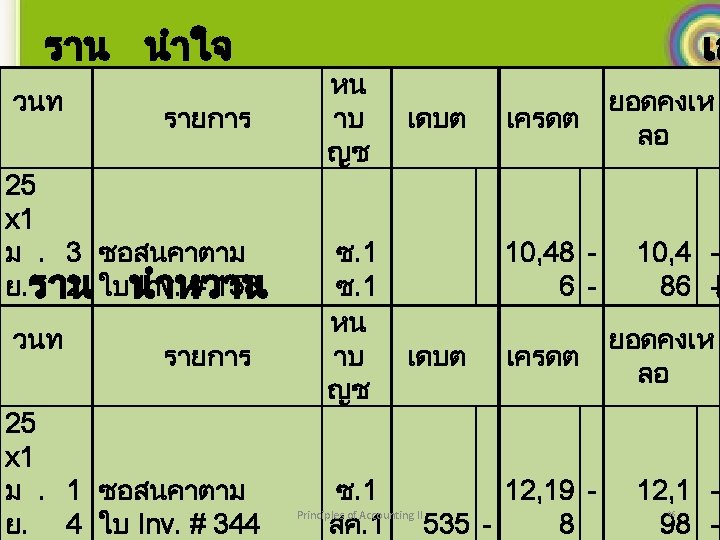

5. Subsidiary Ledger Accounts Payable name. . . . (1). . . AC. Date Description Dr. Page (2) (3) (4) (5) Principles of Accounting II Page). . . 2. . . ( Cr. (6) Balance (7) 11

6. Special Journals • Special Journals have been designed to systematize the original recording of major recurring transactions. a. The general journal is used for all transactions that cannot be entered readily in one of the special journals. b. Each of the special journals is a record of original entry which contains the data which will be posted to ledger accounts. Principles of Accounting II 12

7. Advantages of Special Journals • Several advantages are obtained from the use of special journals. a. Time is saved in journalizing. b. Time is saved in posting. c. Detail is eliminated from the general journal. d. Division of labor is promoted. e. Management analysis is aided. Principles of Accounting II 13

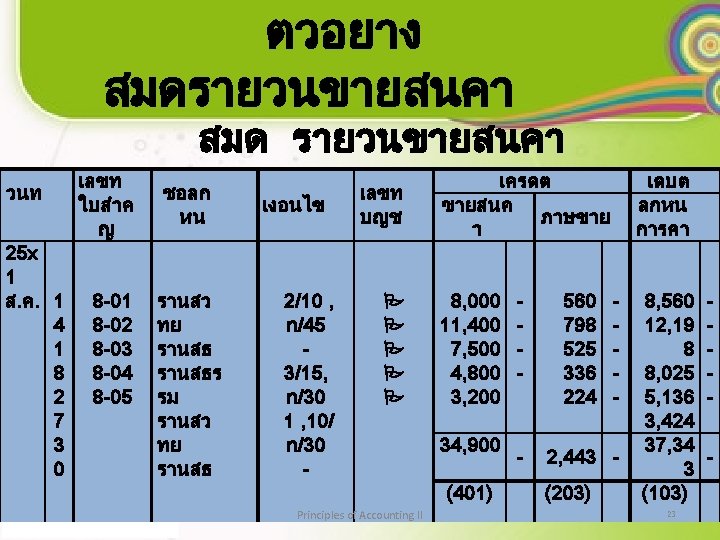

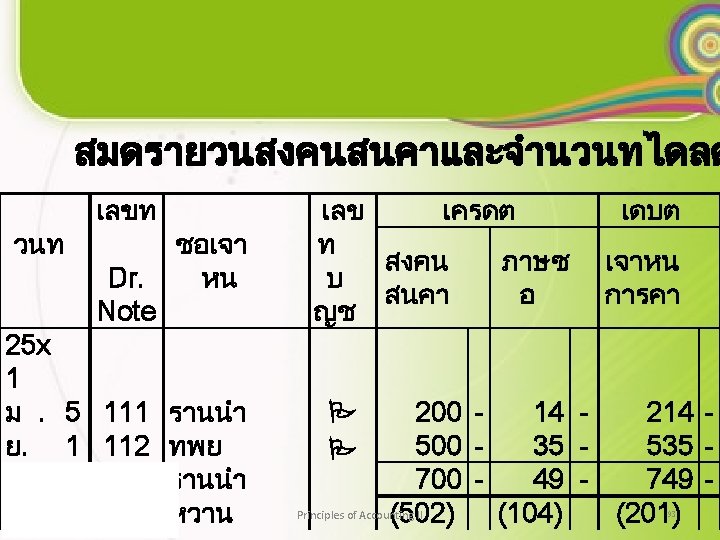

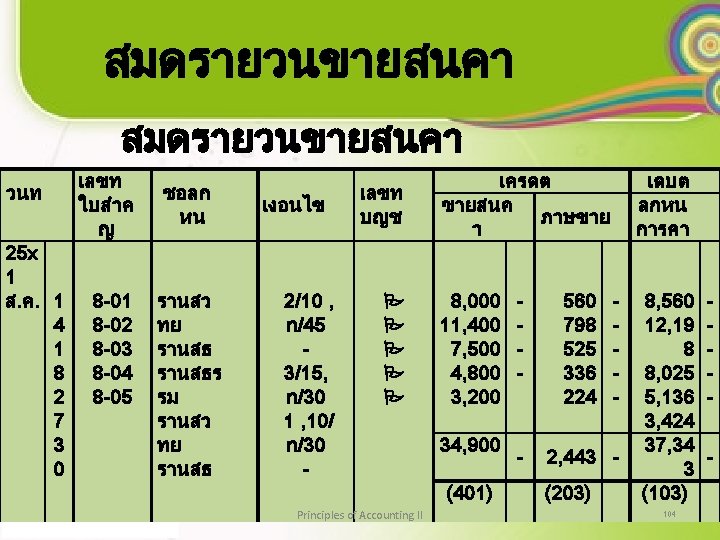

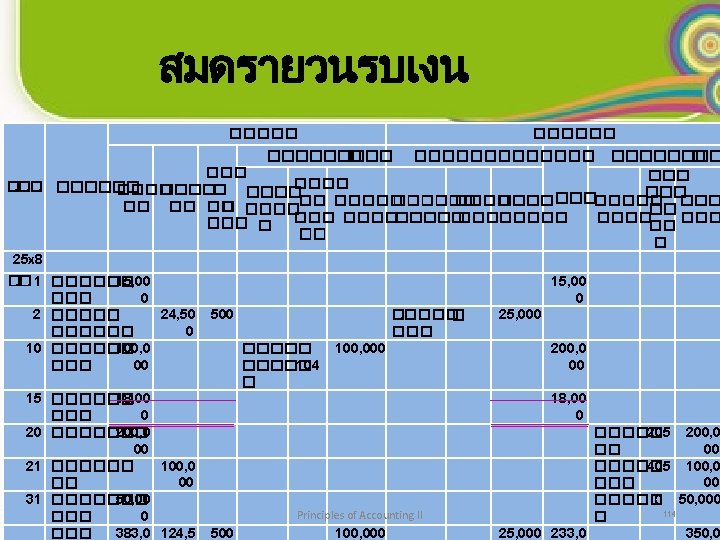

8. Type of Special Journals • Sales Journal (สมดรายวนขาย ) • Sales Return Journal (สมดรายวนรบคน ) • Cash Receipt Journal (สมดรายวนรบเงน ) • Purchases Journal (สมดรายวนซอ • Purchases Return Journal (สมดรายวนสงคน ) Principles of Accounting II ) 14

8. Type of Special Journals • • Sales Journal -Sale on account Sales Return Journal -S/R on account Cash Receipt Journal - Cash Receipt Purchases Journal -Purchases on account Purchases Return Journal -P/R on account Cash Disbursements Journal -Cash paid General Journal -general recorded Principles of Accounting II 15

9. Sales Journal Recognition entry; Sale on account Dr. Accounts Receivable (103) Cr. Sale (401) Vat of Sale (203) Principles of Accounting II xx xx xx 16

9. Sales Journal Recognition entry; Sale on account การบนทกบญช ขายสนคาเปนเงนเชอ Dr. ลกหนการคา (103) xx Cr. ขายสนคา (401) xx Principles of Accounting II 17

9. Sales Journal) 1( Date (3) Page) 2( Dr. Cr. Voucher Accounts Credit Ac. Receivable term No Revenues No. (4) (5) (6) (7) Principles of Accounting II (8) VAT (9) Accounts Receivable (10) 18

9. Sales Journal • The sales journal should be used to record all sales of merchandise on account. a. The simplest form has only one money column entitled Accounts Receivable Dr. and Sales Cr. b. Columns are included for the date, name of the customer, and invoice number. c. A Sales Cr. Column can be provided for each department, if needed. Principles of Accounting II 20

9. Sales Journal d. The posting of sales involves entering the total of the Sales Cr. Column as a credit to the general ledger Sales account. e. The total of the Accounts Receivable Dr. column is posted as a debit to the Accounts Receivable account in the general ledger. Principles of Accounting II 21

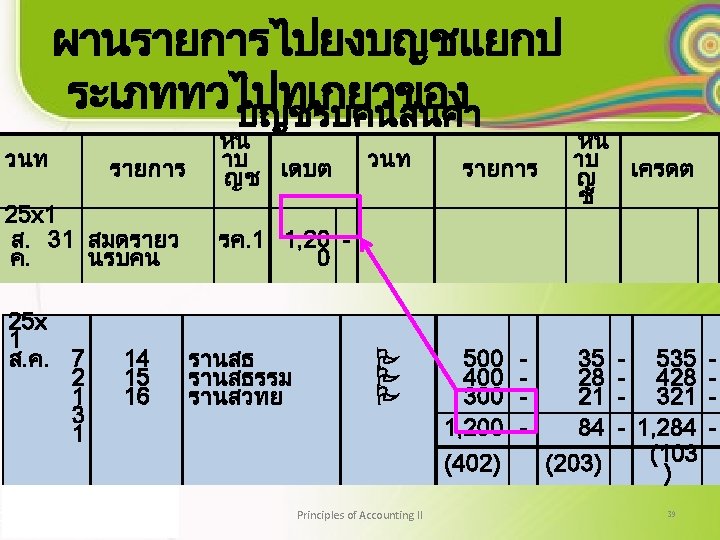

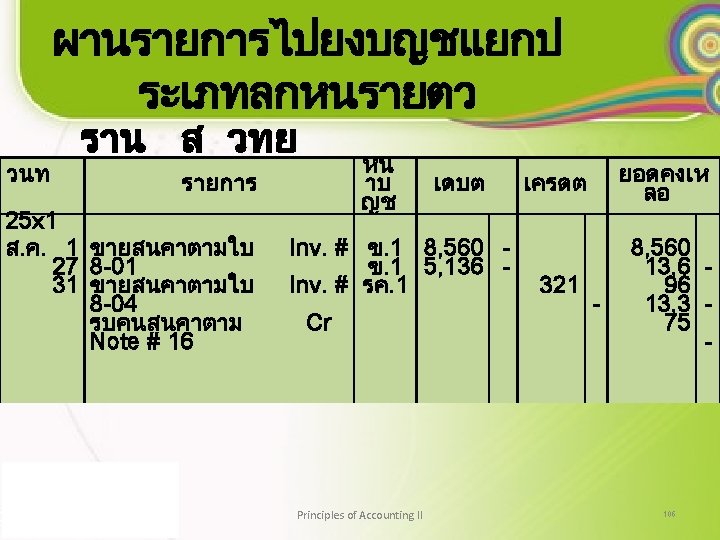

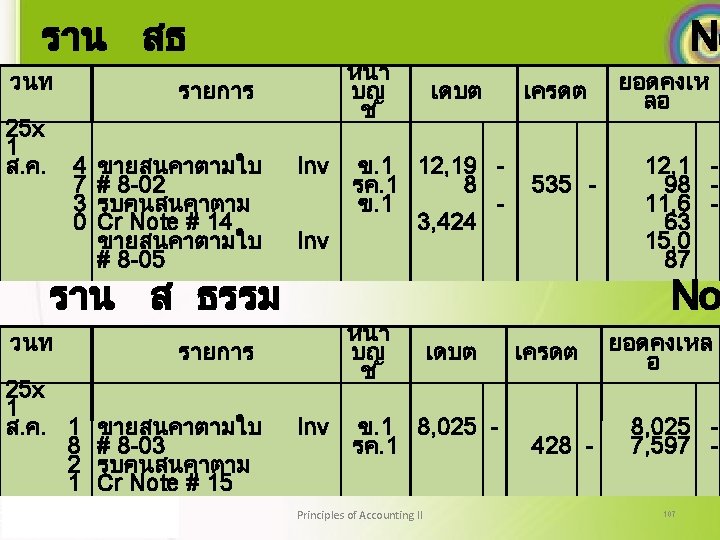

9. Sales Journal f. The individual amounts in the Accounts Receivable Dr. column are posted to each individual customer’s account in the subsidiary ledger. g. Some companies use sales invoices as their sales journal by entering the amount of each sales invoice directly in the subsidiary ledger account of the customer. At the end of the month the total of the sales invoices is debited to Accounts Receivable and credited to Sales in the general journal. Principles of Accounting II 22

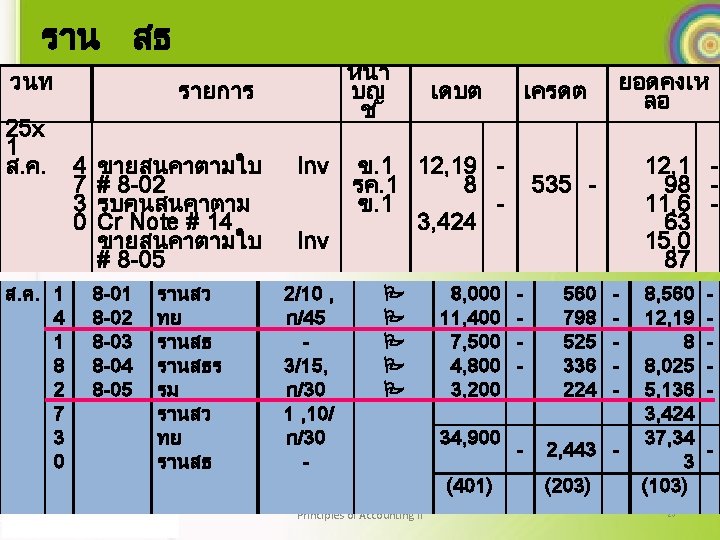

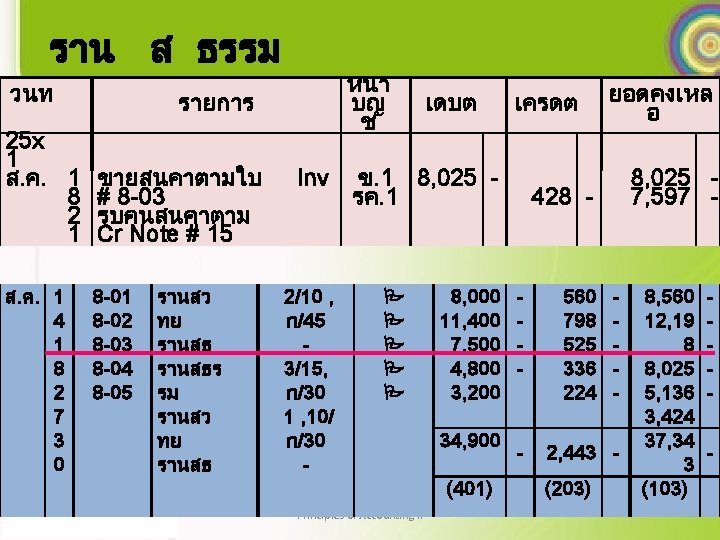

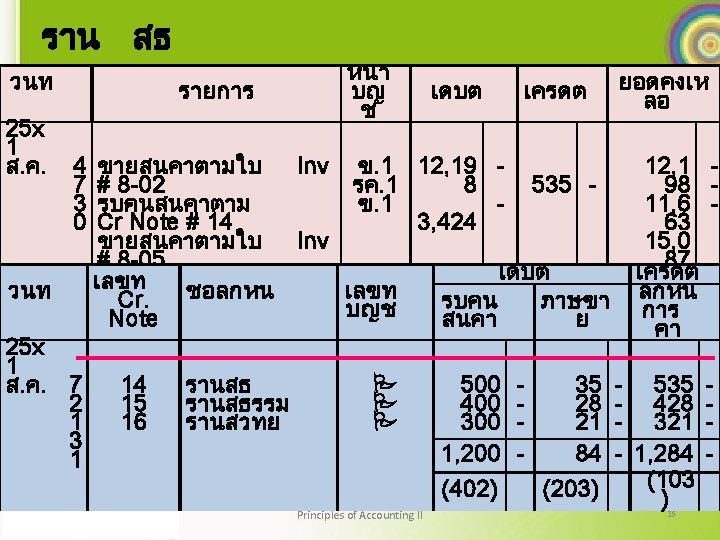

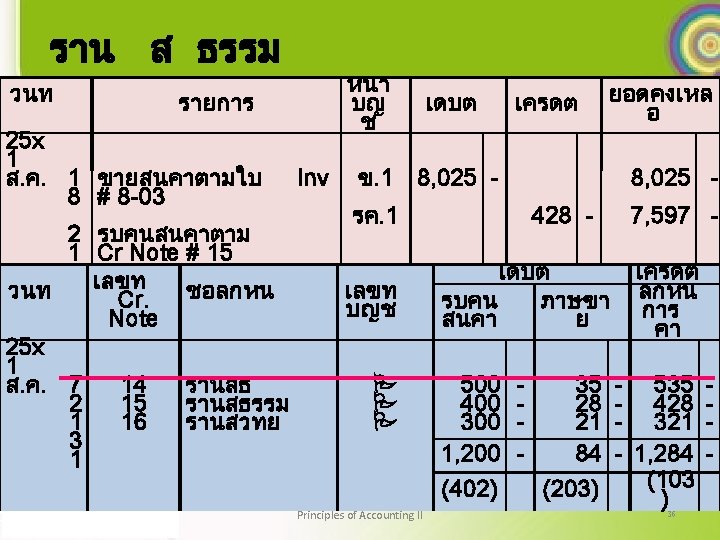

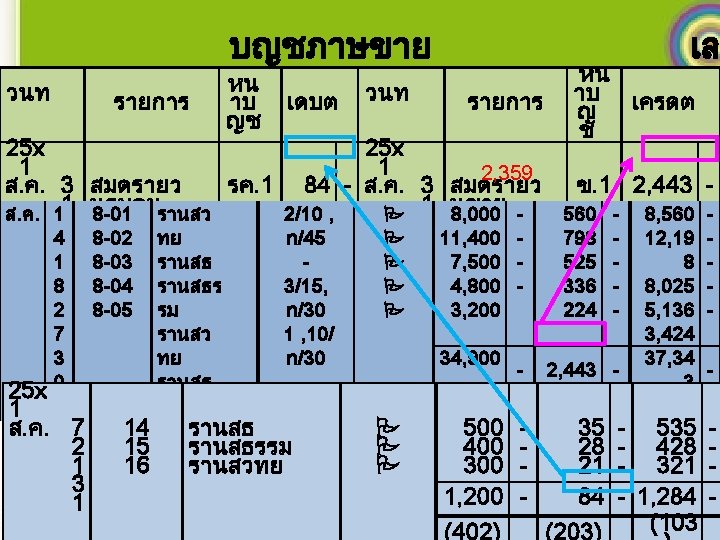

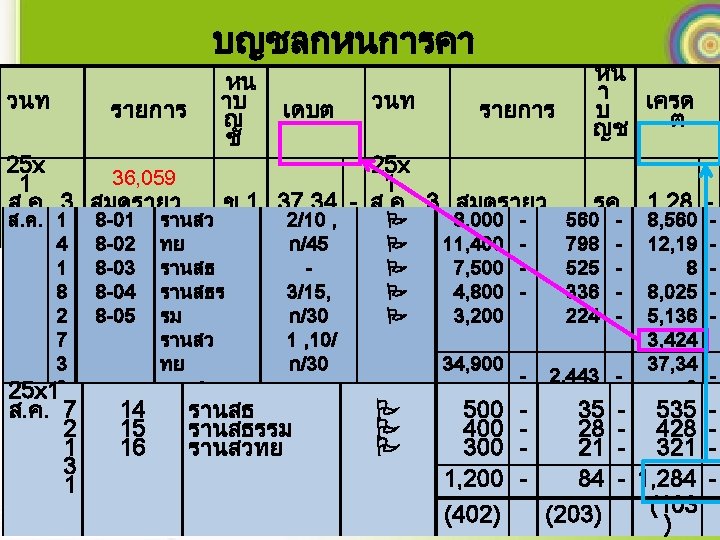

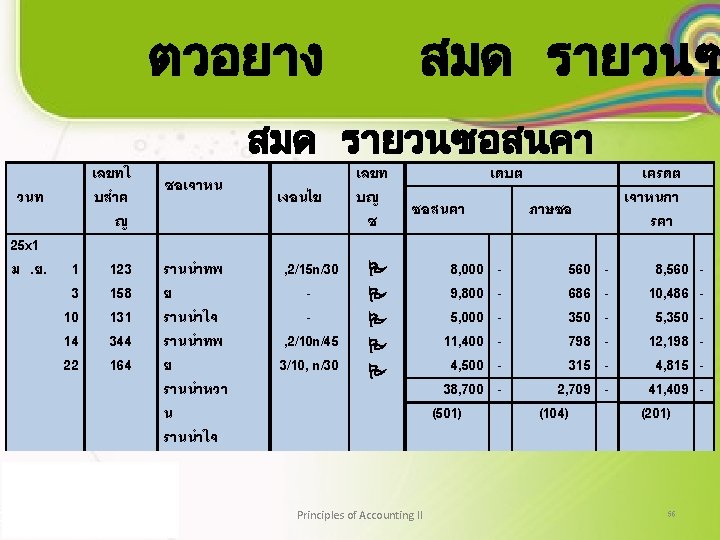

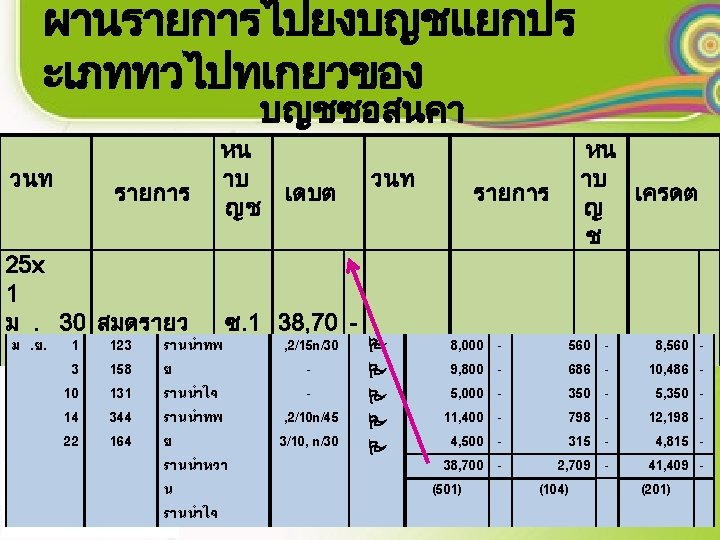

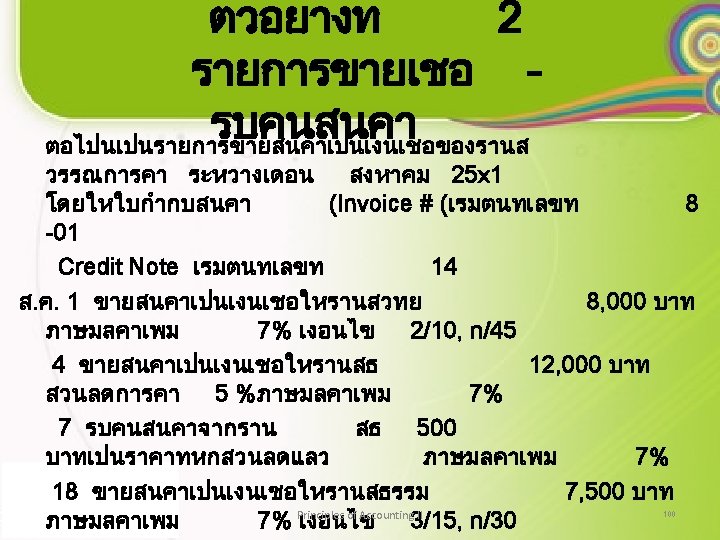

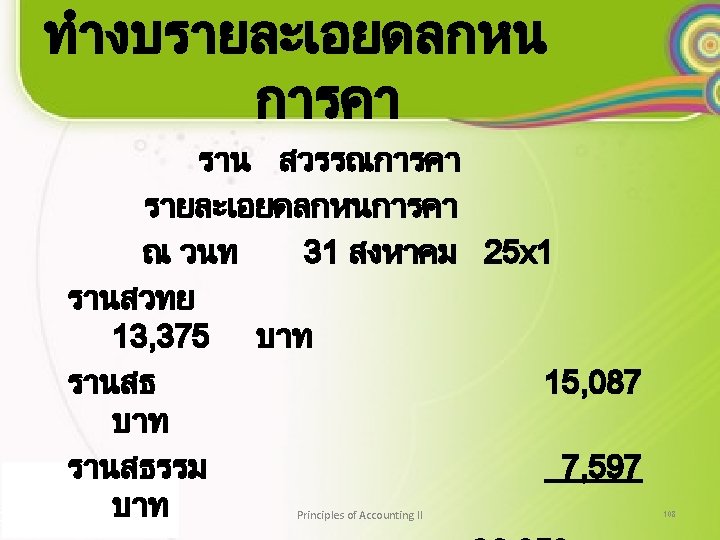

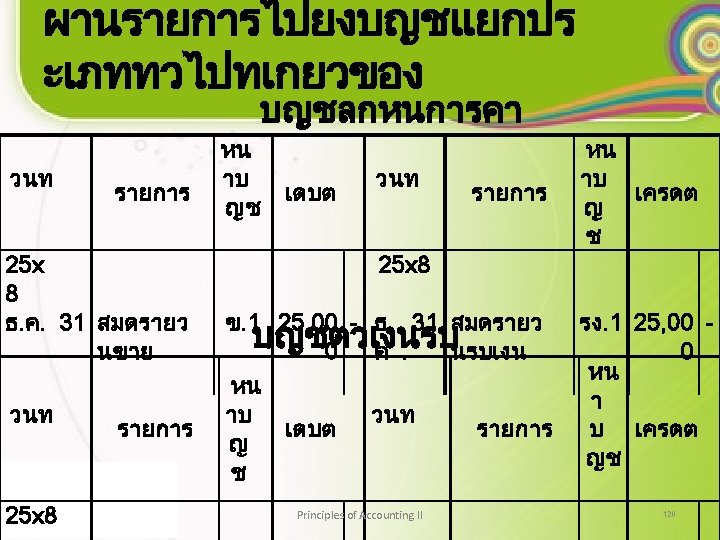

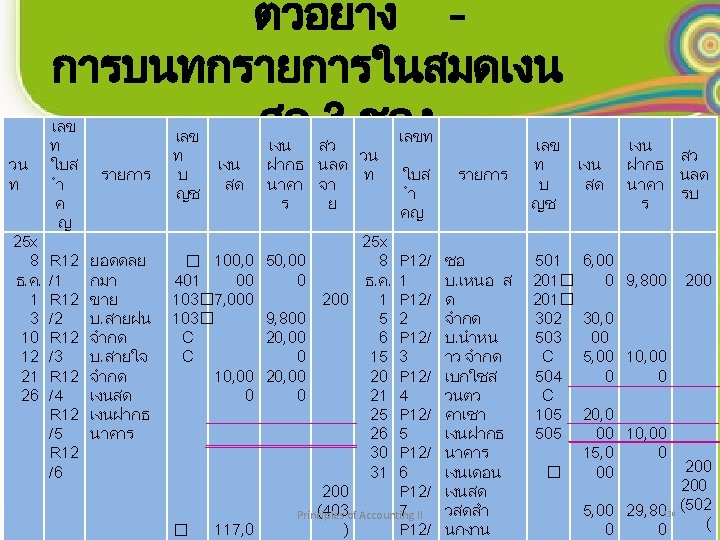

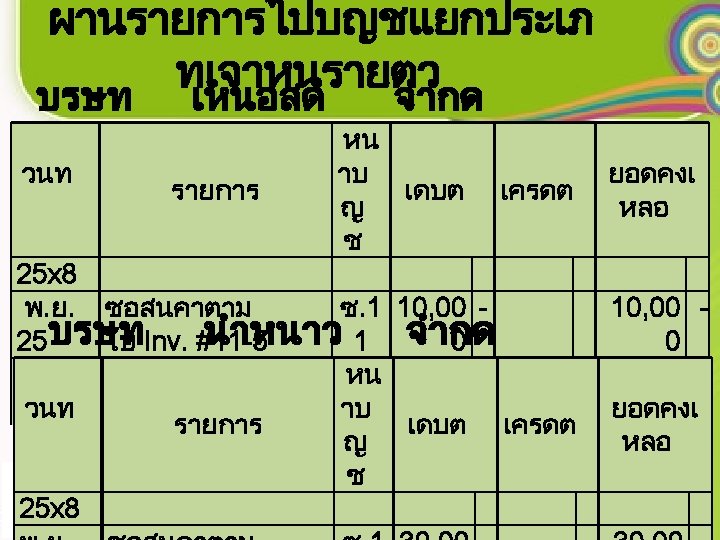

ผานรายการไปบญชแยกปร ะเภททวไป ขายสนคา Date Description Page No. Dr. Date Description amount 25 x 1 ส. ค. 31 สมดรายวน ขาย ส. ค. 1 4 1 8 2 7 3 8 -01 8 -02 8 -03 8 -04 8 -05 รานสว ทย รานสธร รม รานสว ทย 2/10 , 8, 000 n/45 11, 400 7, 500 3/15, 4, 800 n/30 3, 200 1 , 10/ n/30 Principles of Accounting II 34, 900 - Page No. Cr. amount ข. 1 34, 900 - 560 798 525 336 224 - 2, 443 - 8, 560 12, 19 8 8, 025 5, 136 3, 424 27 37, 34 -

ผานรายการไปบญชแยกปร ะเภททวไป ภาษขาย Date Description Page No. Dr. Date Description amount 25 x 1 ส. ค. 31 สมดรายวน ขาย ส. ค. 1 4 1 8 2 7 3 0 8 -01 8 -02 8 -03 8 -04 8 -05 รานสว ทย รานสธร รม รานสว ทย รานสธ 2/10 , 8, 000 n/45 11, 400 7, 500 3/15, 4, 800 n/30 3, 200 1 , 10/ n/30 34, 900 Principles of Accounting II - Page No. Cr. amount ข. 1 2, 443 - 560 798 525 336 224 - 2, 443 - 8, 560 12, 19 8 8, 025 5, 136 3, 424 37, 34 28 3 - N

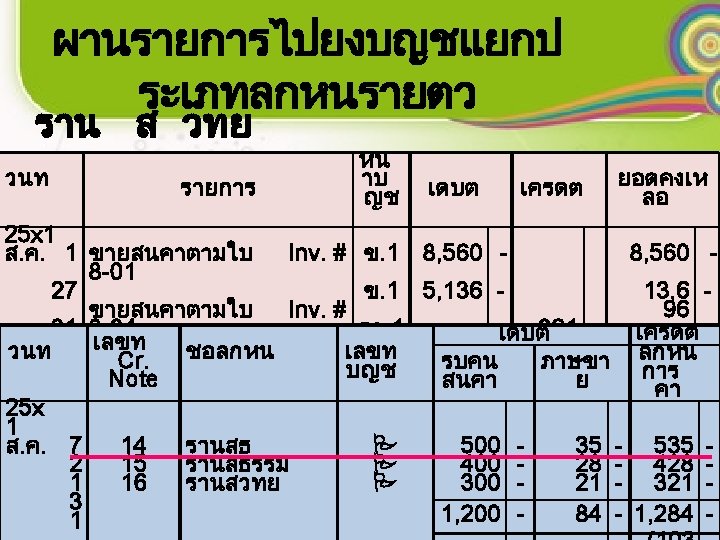

ผานรายการไปบญชแยกปร ะเภททวไป ลกหนการคา Date Description 25 x 1 ส. ค. 31 สมดรายวนข าย ส. ค. 1 4 1 8 2 7 3 0 8 -01 8 -02 8 -03 8 -04 8 -05 รานสว ทย รานสธร รม รานสว ทย รานสธ Page No. Dr. Date Description amount ข. 1 37, 343 - 2/10 , 8, 000 n/45 11, 400 7, 500 3/15, 4, 800 n/30 3, 200 1 , 10/ n/30 34, 900 Principles of Accounting II - Page No. 560 798 525 336 224 - 2, 443 - Cr. amount 8, 560 12, 19 8 8, 025 5, 136 3, 424 37, 34 29 3 -

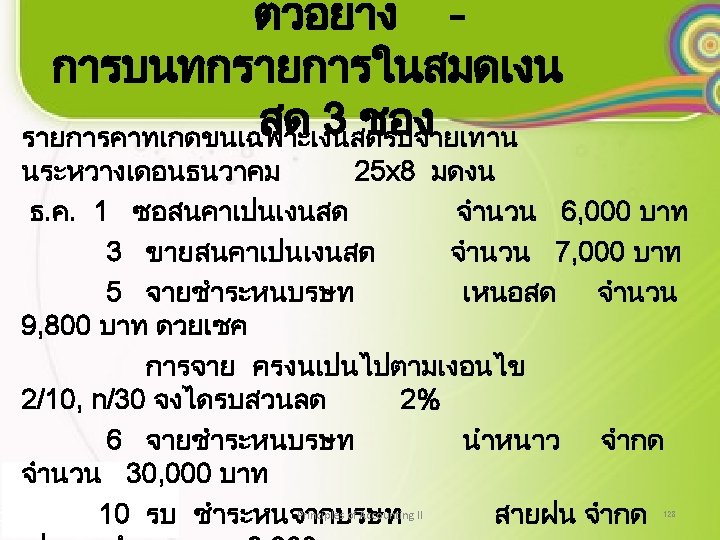

10. Sales Return Journal • When, Sales Returns on account Dr. Sales Returns (402) xx Vat of Sale (203) xx Cr. Accounts Receivable (103) xx Principles of Accounting II 30

10. Sales Return Journal • When, Sales Returns on account • การบนทกบญช รบคนสนคาจากการขายเช อ Dr. รบคนสนคา (402) xx Principles of Accounting II 31

10. Sales Return Journal Page 1 Date No. Cr. Note Accounts Receivable AC. No. (1) (2) (3) (4) Principles of Accounting II Dr. Sale Returns VAT (5) (6) Cr. Accounts Receivable (7) 32

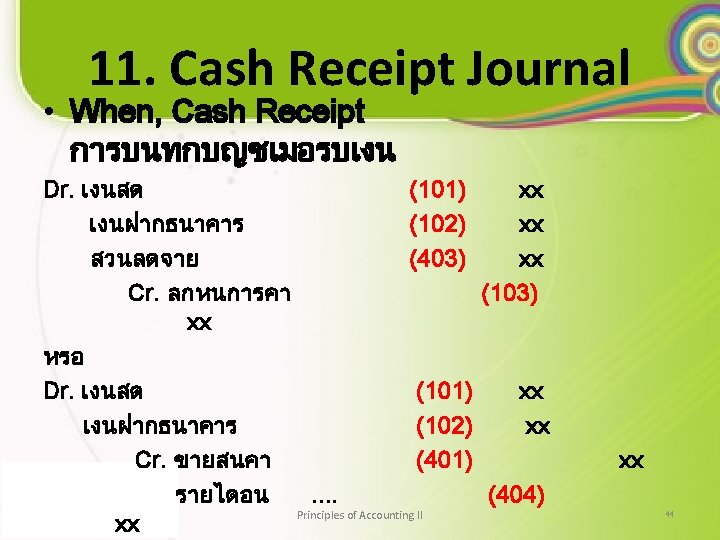

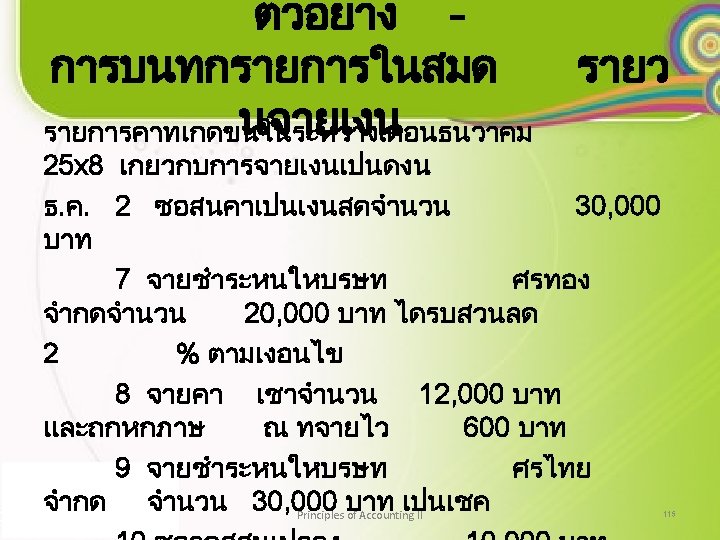

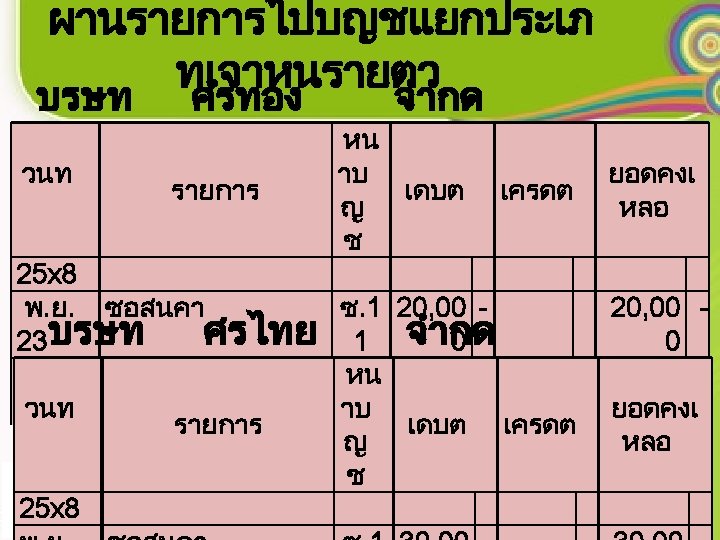

11. Cash Receipt Journal • When, Cash Receipt Dr. Cash (101) xx Cash in Bank (102) xx Sale Discounts (403) xx Cr. Accounts Receivable (103) or Dr. Cash (101) xx Cash in Bank (102) xx Cr. Sale (401) Other Revenues (404) Loan (204) Investment (105) Principles of Accounting II xx xx xx 43

11. Cash Receipts Journal) 1 Date Ac Voucher name NO. Cr. Dr. Discretion Cash bank Accounts Receivable Sale Discounts (4) (5) (6) (7) (8) (9) (10 1) (10 2) (403 ) Cr. Other Account Sale VAT (10) (11) (12) (13) (10 3) (40 1) (203 ) (3) (Page (2) Principles of Accounting II Amount Ac. no amount (14) (15) 45

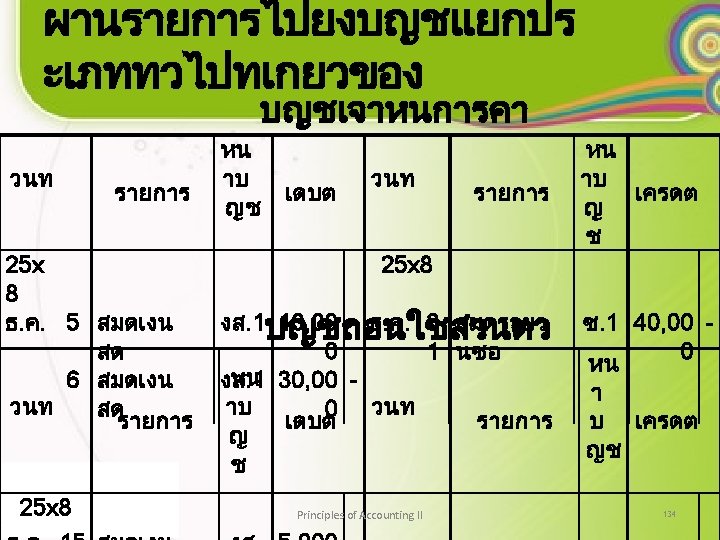

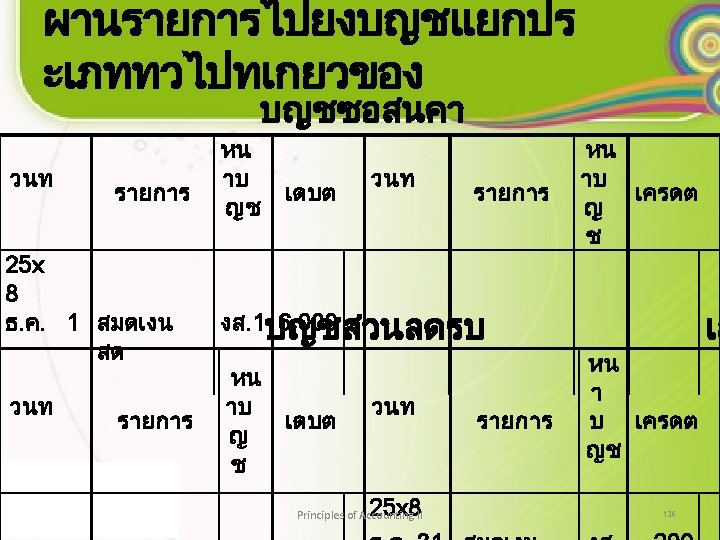

11. Cash Receipt Journal • The cash receipts journal is used to record all receipts of cash, including cash sales. a. Typically, the following columns, will be provided: Cash Dr. , Sales Discounts Dr. , Date, Description, Sales Cr. , Accounts Receivable Cr. , Other Accounts Cr. b. The Cash Dr. , Sales Discounts Dr. , Sales Cr. , and Accounts Receivable Cr. Column totals are posted to those accounts in the general ledger. Principles of Accounting II 47

11. Cash Receipt Journal c. The individual amounts in the Accounts Receivable Cr. Column are posted to each individual customer’s account in the subsidiary ledger. d. The amounts appearing in the Other Accounts Cr. Column are posted in the general ledger to the accounts indicated; the column total is not posted. Principles of Accounting II 48

12. Combined Sales and Cash Receipts Journal • It is possible to combine the sales and cash receipts journals. A. Total sales can then be posted as one amount rather than two. B. But the number of persons who can work with the data is restricted. Principles of Accounting II 49

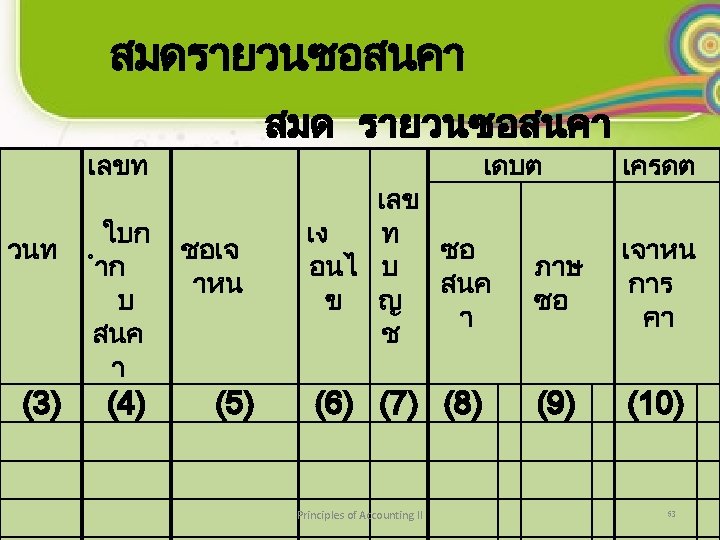

13. Purchases Journal • Recognition entry; Purchases on account Dr. Purchases (501) Vat of Purchases (104) Cr. Accounts Payable (201) Principles of Accounting II xx xx xx 50

13. Purchases Journal • Recognition entry; Purchases on account การบนทกบญช : ซอสนคาเปนเงนเชอ Dr. ซอสนคา (501) xx ภาษซอ (104) xx Cr. เจาหนการคา (201) xx Principles of Accounting II 51

13. Purchases Journal )1( Date Invoice No. Name Accounts Payable (3) (4) (5) Page) 2( Dr. Credit Ac. term No. Purchase (6) (7) Principles of Accounting II Cr. VAT (8) (9) (501) (104) Accounts Payable (10) (201) 52

13. Purchases Journal • The purchases journal is used to record all purchases made on account. a. The simplest form has only one money column entitled Purchases Dr. , Accounts Payable Cr. b. Columns are included for the date, terms of sale, invoice number, and name of creditor. c. A purchases Dr. column can be provided for each department, if needed. Principles of Accounting II 54

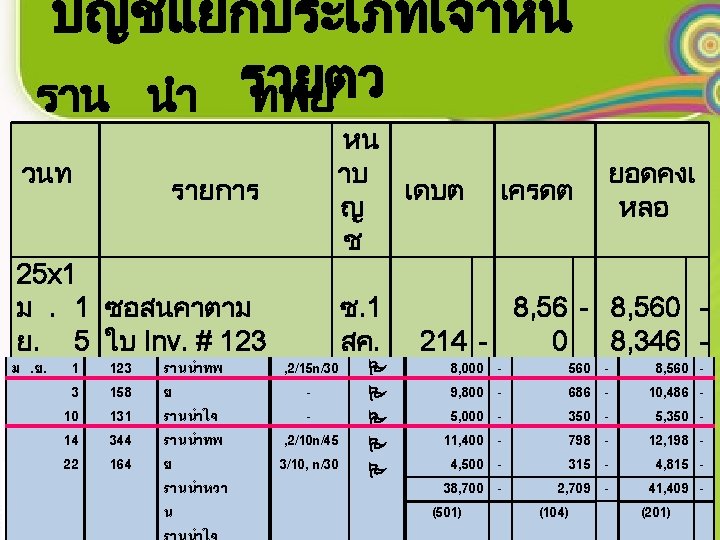

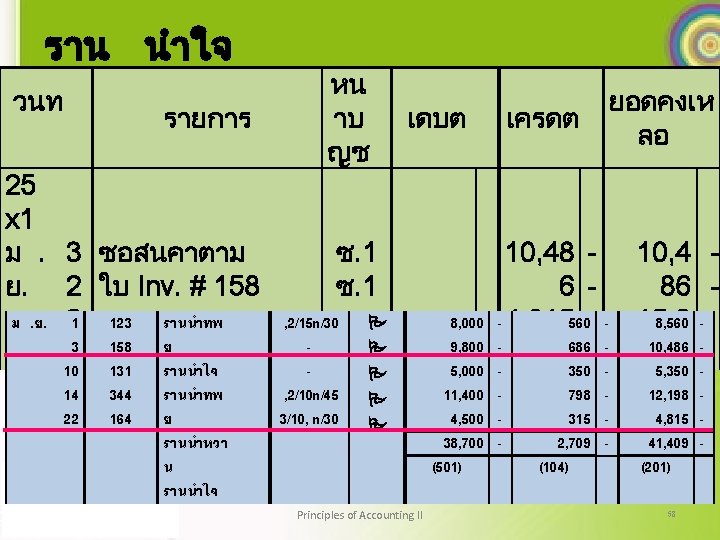

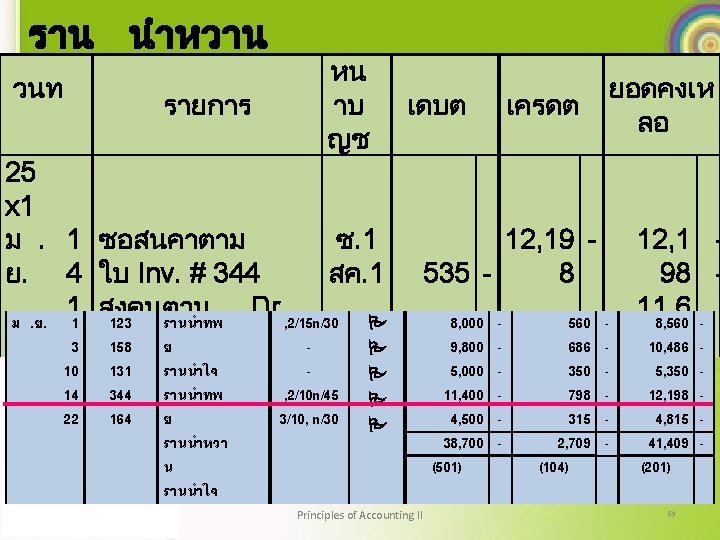

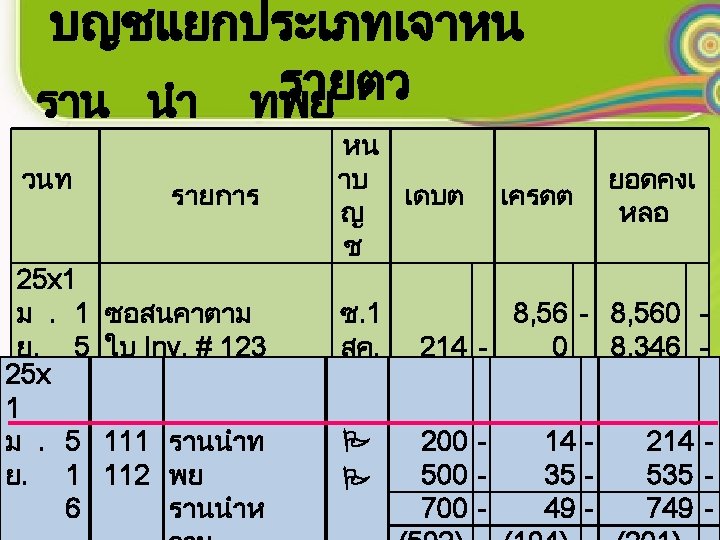

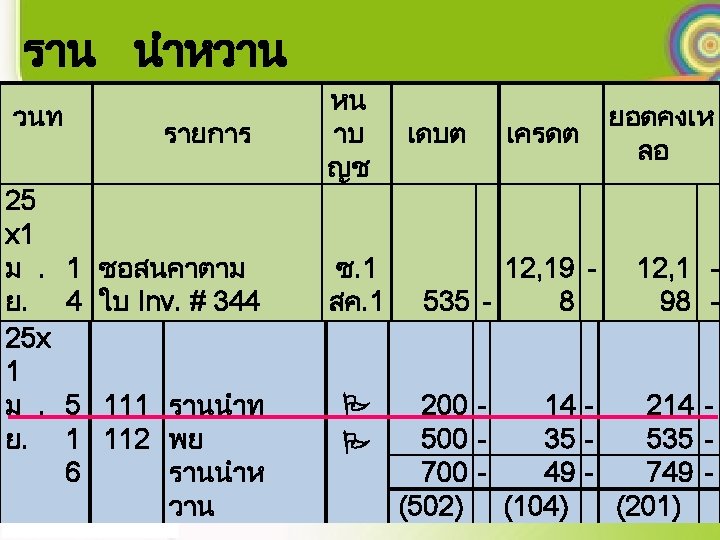

13. Purchases Journal d. The total of the Purchases Dr. column is posted as a debit to the general ledger Purchases account. e. The total of the Accounts Payable Cr. Column is posted as a credit to the general ledger Accounts Payable account. f. The individual amounts in the Accounts Payable Cr. Column are posted to each individual creditor’s account in the subsidiary ledger. Principles of Accounting II 55

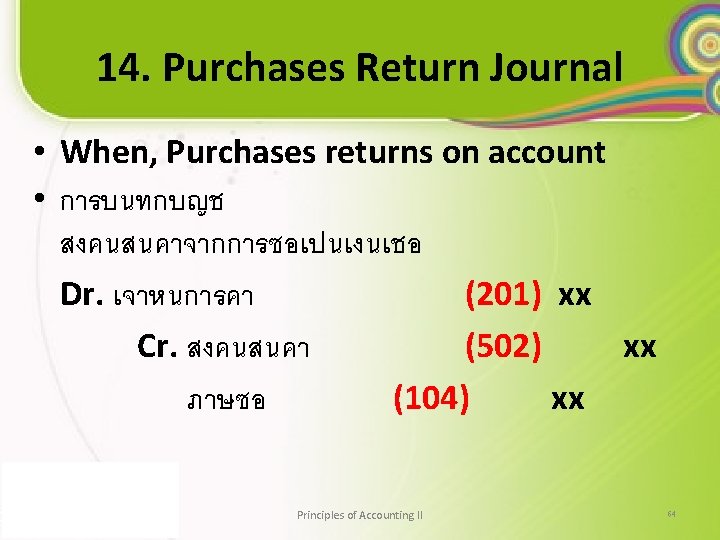

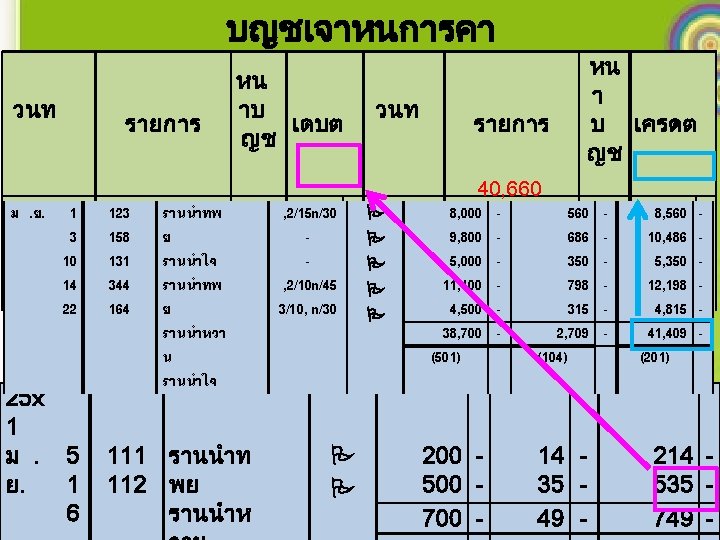

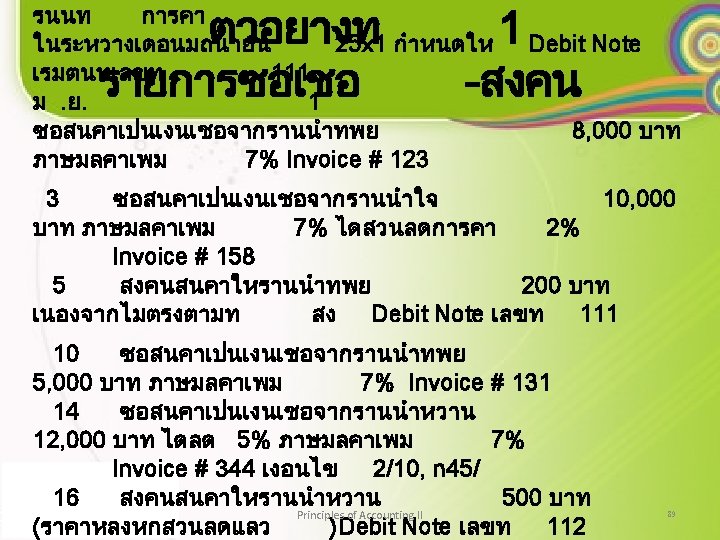

14. Purchases Return Journal • When, Purchases returns on account Dr. Accounts Payable (201) xx Cr. Purchases Returns (502) xx Vat of Purchases (104) xx Principles of Accounting II 63

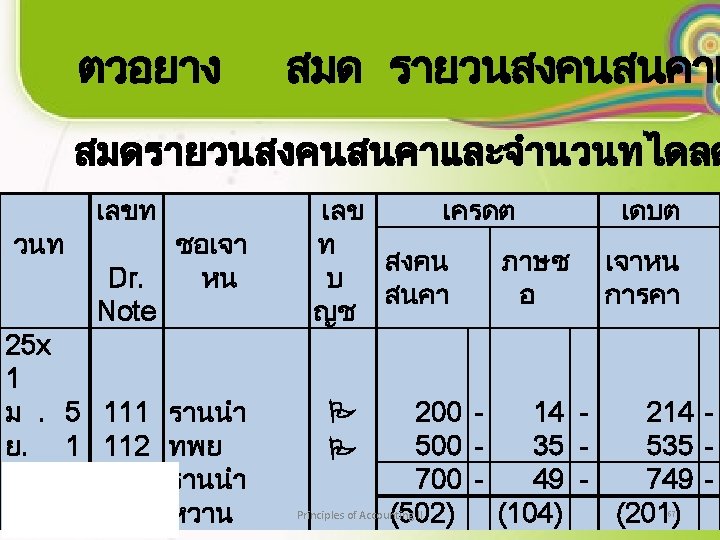

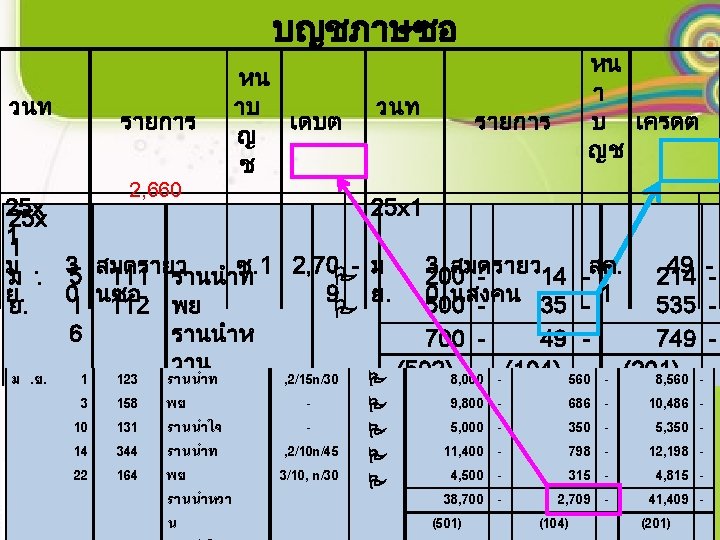

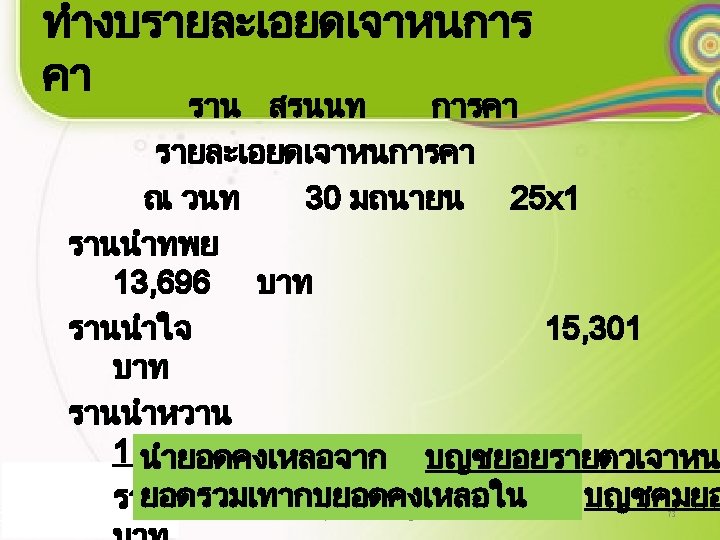

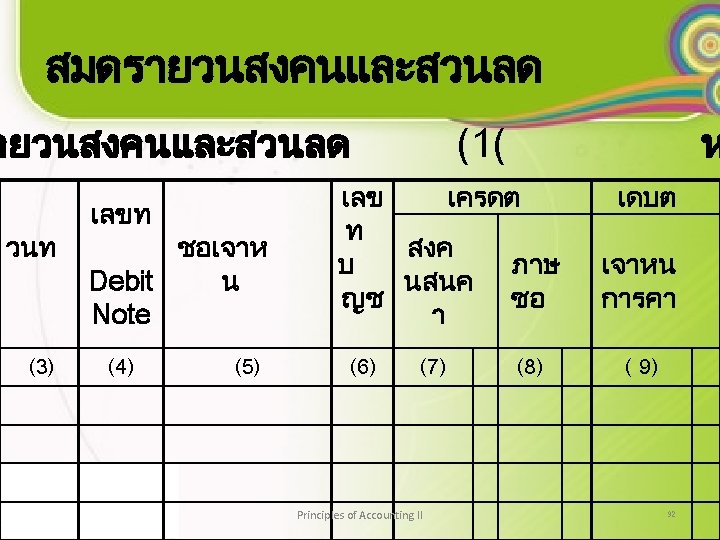

14. Purchases Return Journal Purchases Return Journal) 1( Date (3) Debit Note No (4) Name Accounts Payable (5) Page )2. . . ( Cr. Dr. AC. No. Purchases Returns VAT Accounts Payable (6) (7) (8) ( 9) (502) (104) (201) Principles of Accounting II 65

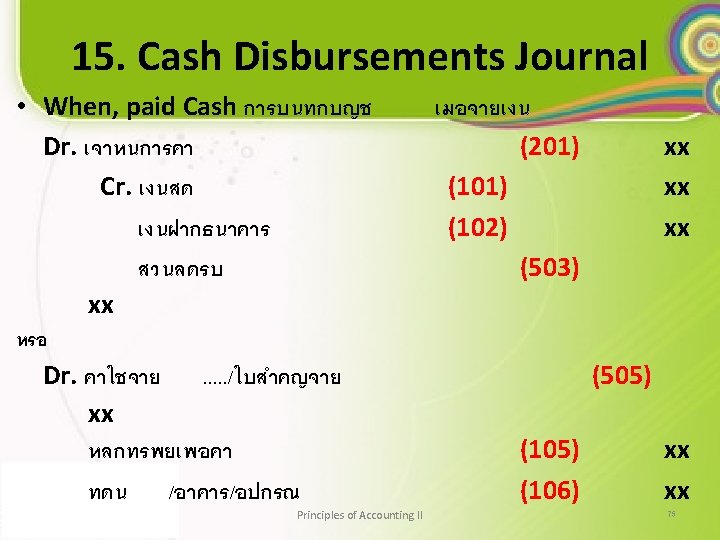

15. Cash Disbursements Journal • When, paid Cash Dr. Accounts Payable Cr. Cash in Bank Purchases Discounts (201) (101) (102) (503) xx (505) (106) (101) (102) xx xx xx Or Dr. Expense/Voucher Investment Fixed Assets Cr. Cash in Bank Principles of Accounting II xx xx 74

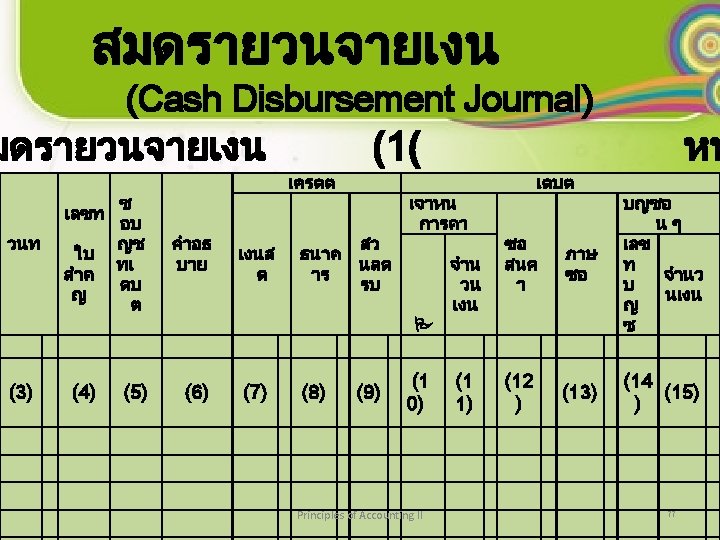

15. Cash Disbursement Journal )1 Date (3) Voucher No. (4) Account Name Description Dr. (5) (6) Cr. Cash Bank Accounts Payable Purchases Discount (7) (8) (9) (101) (102) (503) amount Page (2) ( Dr. Purchases VAT (10) (11) (12) (13) (201) (501) (104) Principles of Accounting II Other Accounts AC. No. amount (14) (15) 76

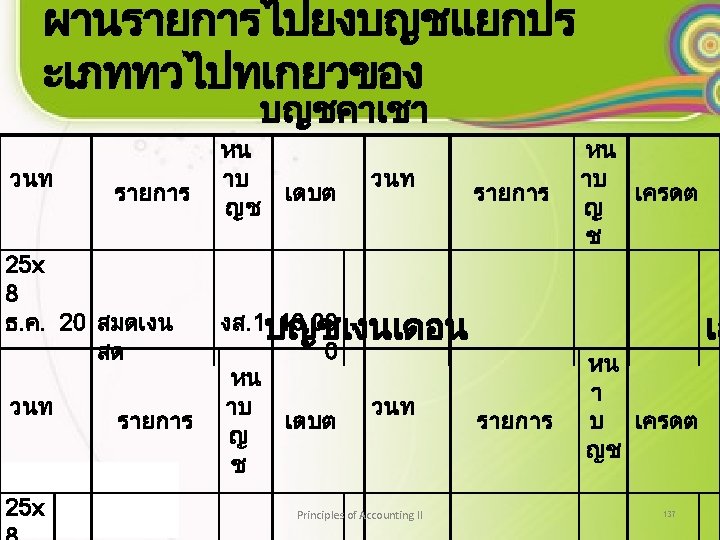

15. Cash Disbursements Journal • The cash disbursements journal is used to record all disbursements of cash. a. Typically, the following columns will be provided: Accounts Payable Dr. , Supplies Expense Dr. , Other Accounts Dr. , Date, Description, Check Number, Cash Cr. , Purchases Discounts Cr. b. The Accounts Payable Dr. , Supplies Expense Dr. , Purchase Discounts Cr. , and Cash Cr. Column totals are posted to those accounts in the general ledger. Principles of Accounting II 78

15. Cash Disbursements Journal c. The individual accounts in the Accounts Payable Dr. column are posted to each individual creditor’s accounts in the subsidiary ledger. d. The amounts appearing in the other Accounts Dr. column are posted in the general ledger to the accounts indicated; the column total is not posted. Principles of Accounting II 79

16. Combined Purchases and Cash Disbursements Journal • The purchases and the cash disbursements journal can be combined; however, this limits the number of people who can work with the journals at any one time. Principles of Accounting II 80

General Journal • Transactions that do not belong in a special journal are entered in the general journal. Principles of Accounting II 81

Alternative Methods of Processing Data • Accountants have a wide range of equipment that can be used in accounting systems to process data, including the following: a. Manual systems b. Bookkeeping machine system c. Microcomputers and Minicomputers d. Service bureaus e. Time-sharing terminal. f. Mainframe In-House Computer Principles of Accounting II 82

Manual System • Small businesses often use a handposted system in which the accounting function is handled by the accountant and possible one or two clerks. Principles of Accounting II 83

Bookkeeping Machine System • A bookkeeping machine system is usually set up so that recurring transactions are recorded on the bookkeeping machines. Principles of Accounting II 84

Minicomputers and Microcomputers • With the lowering of computer prices, may small and medium-sized businesses are replacing their manual systems with microcomputers and minicomputers. a. Microcomputers are smaller than minicomputers. b. Cost is often the distinction between a microcomputer and a minicomputer. Principles of Accounting II 85

Time-Sharing Terminal. • Time sharing occurs when several users Utilize the same host computer to process data. Principles of Accounting II 86

Mainframe in-house Computer • The purchase of an in-house computer is often justified if the volume of transaction is very large. Principles of Accounting II 87

Accounting Software • Express Accounting 28% • • • SAP* • • ACCPAC • • ORACLE* • • EASY- ACC. • • FORMULA SUPER GL Clip Accounting My Account Auto Flight Pattani Freeware Imoneys Account ERP Impress Professional • QUICK BOOKs • BUSINESS • SCALA *เปนโปรแกรมเหมาะกบกจการขนา Principles of Accounting II 88

The End Thank you for your Attention Q&A Principles of Accounting II 139