1 Introduction to Accounting WHAT IS ACCOUNTING Accounting

Introduction to Accounting")

results in an")

- Slides: 43

(1) Introduction to Accounting

WHAT IS ACCOUNTING? Accounting is an information system that provides reports to stakeholders about the economic activities and condition of a business

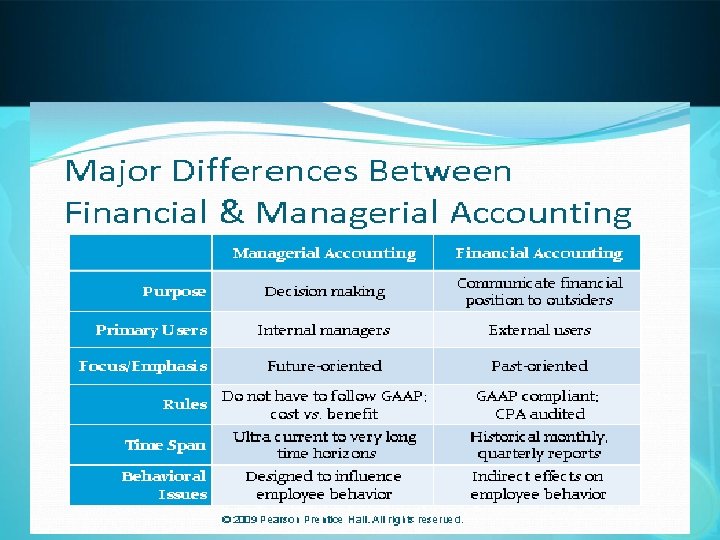

Users of Accounting Information External Users Internal Users Financial accounting provides external users with financial statements. Managerial accounting provides information needs for internal decision makers.

QUESTIONS ASKED BY INTERNAL USERS

QUESTIONS ASKED BY EXTERNAL USERS

Accounting Equation Assets = Liabilities + Equity The accounting equation must remain in balance after each transaction. Assets Liabilities & Equity

Accounting Equation – Cont’d Asset= Liabilities + Equity Resources Managed by Managers Sources of Financing Creditors Shareholders Separation between ownership and control Information

Definitions Assets : Are resources owned by a business and are excepted to generate future benefits Liabilities : Are creditor claims against asset They are existing debts and obligations Capital [Equity] Resources invested by the owner Equity = Assets – Liabilities = Net Assets

Assets Cash Accounts Receivable Vehicles Store Supplies Resources owned or controlled by a company Notes Receivable Land Buildings Equipment

A receivable is something you are going to “Receive” in the future [Collect cash in the future]; it is an ASSET

Liabilities Accounts Payable Bank Loans Notes Payable Liability Accounts Accrued Liabilities Unearned Revenue

A payable is something you are going to “Pay” in the future [Pay cash in the future]; it is a LIABILITY

Prepaid Accounts Prepaid Expenses are items that we pay for today to be used in the future (Provide Future Benefits). Assets Example: Prepaid Rent, Prepaid Insurance Unearned Revenues are amounts that we collect toady (Advance payments), but would be earned in the future after we sell the product or provide the service. Liabilities Example: Unearned Fees

If the transaction involves “Signing” a document then use Notes receivable or Notes payable. Ex: “The company sells a product for 100 and the buyer signs a note Agreeing to pay the amount at a future date” • The company will receive the cash in the future Receivable • A note is signed : Note Receivable Ex: “The company buys a product for 200 and signs a note Agreeing to pay the amount at a future date” • The company will pay the cash in the future : payable • A note is signed : Note Payable

If the transaction mentions “On credit” or “On account” use accounts receivable or accounts payable. Ex: “The company sells a product for 100 on credit (on account) and sends the bill to the buyer who will pay the cash at a future date ” • The company will receive the cash in the future: Receivable • The sale is on account : Accounts Receivable Ex: “The company buys a product for 200 on credit (on account) and gets the bill now, but will pay the cash at a future date • The company will pay the cash in the future: Payable The purchase is on account : Accounts Payable

Borrow Buy Pay. Land Cash and for from pay loan. Bank cash Cash Building Cash Equipment Cash Bank Loan Land Bank Loan Balance Sheet Assets= Liabilities + Owners’ Equity

Equity Contributed Capital “Common Stock”/Capital Stock Retained Earnings Owners’ claims to Assets “Net Assets” Equity = Assets - Liabilities

Definitions Common Stock / Capital Stock : The Corporation’s basic ownership share Revenues: Increases in equity resulting from a company’s business activities (e. g. Sales of a product, fees for rendering a service) Expenses: Decreases in equity resulting from a company’s business activities that are incurred to generate revenues. (e. g. Salaries Expense) Net Income = Revenues – Expenses Dividends: Distributions of assets generated by past earnings to stockholders Retained Earnings: Net income not distributed to stockholders

Invest Cash Receive for revenues Earned Paycash forexpenses dividends Revenues Dividends Expenses Cash Land Cash Equipment Cash Building Common Stock Liabilities Common Stock Balance Sheet Assets= Liabilities + Owners’ Equity Re Ea tain rn ed ing s Cash Retained Earnings

Equity Contributed Capital Common Stock Dividends Ret Ear ained nin gs Undistributed Net Income “Retained Earnings” Net Income = Revenues - Expenses 1. Distribute to Stockholders (Dividends) 2. Retain in company (Retained Earnings)

Three Types of Transactions That Affect Retained Earnings

Owners’ Investments 1. Invested $50, 000 in Shannon Realty, Inc. , in exchange for 5, 000 shares of $10 par value common stock 1. Common Stock $50, 000 Cash $50, 000 A = $50, 000 L + SE = $50, 000 Notice that the accounting equation Assets = Liabilities + Stockholders’ Equity or A = L + SE is always in balance

Purchase of Assets with Cash 2. Purchased a land for $10, 000 and a small building on the land for $25, 000 Cash 1. $50, 000 2. − 35, 000 Land Building $10, 000 $25, 000 A = $50, 000 Common Stock $50, 000 L + SE = $50, 000 This transaction only affects one side of the accounting equation – Assets Whenever a transaction affects only one side of the accounting equation, the total on each side of the equal sign remains unchanged

Purchase of Assets by Incurring a Liability 3. Purchased office supplies for $500 on credit Cash 1. $50, 000 2. − 35, 000 3. $15, 000 Supplies Land Building $10, 000 $25, 000 $500 A/P Common Stock $50, 000 $500 $10, 000 A = $50, 500 $25, 000 $50, 000 L + SE = $50, 500

Payment of a Liability 4. . Paid $200 of the $500 owed for supplies Cash 1. $50, 000 2. − 35, 000 3. 4. − 200 $14, 800 Supplies Land Building $10, 000 $25, 000 $500 $10, 000 A = $50, 300 $25, 000 A/P $500 − 200 $300 Common Stock $50, 000 L + SE = $50, 300

Revenues 5. Earned and received a commission of $1, 500 in cash Cash 1. $50, 000 2. − 35, 000 3. 4. − 200 5. 1, 500 $16, 300 Supplies Land Building $10, 000 $25, 000 $500 A/P Common Retained Stock Earnings $50, 000 $500 − 200 $10, 000 A = $51, 800 $25, 000 $300 $50, 000 $1, 500 L + SE = $51, 800

Revenues 6. Earned a commission of $2, 000 to be received at a later date Cash 1. $50, 000 2. − 35, 000 3. 4. − 200 5. 1, 500 6. $2, 000 $16, 300 $2, 000 Supplies A/R Land Building $10, 000 $25, 000 $500 A/P Common Retained Stock Earnings $50, 000 $500 − 200 $1, 500 2, 000 $500 $10, 000 A = $53, 800 $25, 000 $300 $50, 000 $3, 500 L + SE = $53, 800 Accrued Revenue not collected in cash

Collection of Accounts Receivable 7. Received $1, 000 from client for commission earned earlier in the month Cash 1. $50, 000 2. − 35, 000 3. 4. − 200 5. 1, 500 6. 7. 1, 000 $17, 300 Supplies A/R Land Building $10, 000 $25, 000 $500 $2, 000 − 1, 000 $1, 000 A/P Common Retained Stock Earnings $50, 000 $500 − 200 $1, 500 2, 000 $500 $10, 000 A = $53, 800 $25, 000 $300 $50, 000 $3, 500 L + SE = $53, 800

Expenses 8. Paid $1, 000 to rent equipment for office Cash 1. $50, 000 2. − 35, 000 3. 4. − 200 5. 1, 500 6. 7. 1, 000 8. − 1, 000 $16, 300 Supplies A/R Land Building $10, 000 $25, 000 $500 A/P Common Retained Stock Earnings $50, 000 $500 − 200 $1, 500 2, 000 $2, 000 − 1, 000 $500 $10, 000 A = $52, 800 $25, 000 $300 $50, 000 − 1, 000 $2, 500 L + SE = $52, 800

Expenses 9. Paid $400 in wages to part-time helper Cash 1. $50, 000 2. − 35, 000 3. 4. − 200 5. 1, 500 6. 7. 1, 000 8. − 1, 000 9. − 400 $15, 900 Supplies A/R Land Building $10, 000 $25, 000 $500 A/P Common Retained Stock Earnings $50, 000 $500 − 200 $1, 500 2, 000 $2, 000 − 1, 000 $500 $10, 000 A = $52, 400 $25, 000 $300 $50, 000 − 1, 000 − 400 $2, 100 L + SE = $52, 400

Expenses 10. Recorded utilities expense of $300 incurred in December but not yet paid Cash 1. $50, 000 2. − 35, 000 3. 4. − 200 5. 1, 500 6. 7. 1, 000 8. − 1, 000 9. − 400 10. $15, 900 Supplies A/R Land Building $10, 000 $25, 000 $500 A/P Common Retained Stock Earnings $50, 000 $500 − 200 $1, 500 2, 000 $2, 000 − 1, 000 $500 $10, 000 A = $52, 400 $25, 000 300 $600 $50, 000 − 1, 000 − 400 − 300 $1, 800 L + SE = $52, 400 Accrued Expense not paid immediately

Dividends 11. Declared and paid a $600 dividend Cash 1. $50, 000 2. − 35, 000 3. 4. − 200 5. 1, 500 6. 7. 1, 000 8. − 1, 000 9. − 400 10. 11. − 600 $15, 300 Supplies A/R Land Building $10, 000 $25, 000 $500 A/P Common Retained Stock Earnings $50, 000 $500 − 200 $1, 500 2, 000 $2, 000 − 1, 000 300 $1, 000 $500 $10, 000 A = $51, 800 $25, 000 $600 $50, 000 − 1, 000 − 400 − 300 − 600 $1, 200 L + SE = $51, 800

Financial Statements 1. Income Statement 2. Statement of Retained Earnings 3. Balance Sheet 4. Statement of Cash Flows

Income Statement Net Income=Revenues-Expenses Date reflects revenues and expenses incurred over a period of time Net income figure used to prepare statement of retained earnings

Non-Cash Expenses Depreciation • Using a fixed asset (e. g. machine) results in an expense called depreciation expense EX: A company buys a machine for $100, 000 and estimates that it has a useful life of 10 years. Each year the company would transfer $10, 000 (100, 000÷ 10) from the balance sheet to the income statement. The value of the machine after the first year is $90, 000. • Note: Although the depreciation expense reduces Net Income it has no effect of cash

Non-Cash Expenses Bad Debt Expense • Realistically not all of Accounts Receivable will be collected. • The company must estimate the amount of A/R that is expected to be uncollectible. This amount is called Bad Debt Expense EX: Assume the ABC has $10, 000 of A/R and it estimates that 2% will not be collected. Thus the $200 (0. 02 x 10, 000) will be reduced from the A/R on the balance sheet and $200 expense will appear on the Income Statement. Note: Although the bad debt expense reduces Net Income it has no effect of cash

Statement of Retained Earnings End RE=Beg RE+NI-DIV Ending retained earnings figure used to prepare the balance sheet Date reflects changes in retained earnings over a period of time Net income figure from income statement

Balance Sheet Assets=Liabilities + Equity Balance in Cash account used in statement of cash flows Date reflects account balances as of a certain date Retained earnings figure from the statement of retained earnings

Components of the Balance Sheet Assets Current assets Cash and other assets reasonably expected to be converted to cash, consumed, or sold within one year or its normal operating cycle, whichever is longer • Cash & Cash Equivalents : (T-Bills, highly liquid) maturing within 90 -days • Marketable Securities : Stocks and Bonds traded within current year • Receivables: Accounts (trade receivables) [NRV] • Inventories : Finished Goods, Raw Materials. Work in progress [LCM] • Prepayments: Prepaid Expenses

Components of the Balance Sheet Assets Property, plant, & equipment/ Noncurrent assets Long-term investments Long-term tangible assets like land buildings used in continuing operations. Resources which can be realized in cash Their conversion into cash is not expected within one year or the operating cycle, whichever is longer. Ex: Long-term loans to other companies, LT holdings of stock and bonds of other companies. • Building, Equipment : Depreciated [Net Book Value , Net Carrying amount] • Land : Not Depreciated [No Useful life]. Intangible Assets do not have physical substance Ex: patents copyrights, trademarks, Goodwill

Components of the Balance Sheet Liabilities Current liabilities Obligations due to be paid or performed within one year or within the normal operating cycle, whichever is longer Examples: Notes payable, accounts payable, Accrued Expenses (salaries and wages payable) , customer advances (Deferred Income), current portion of long-term debt Long-term liabilities Debts of a business that fall due more than one year in the future or beyond the normal operating cycle, which will be paid out of noncurrent assets Examples: Mortgages payable, long-term notes, bonds payable, employee pension obligations, long-term lease liabilities

Relationship Between Income Statement and Balance Sheet Income Statement Balance Sheet Revenues -Expenses= Net Income Assets= Liabilities+ Equity Net Income = Revenues - Expenses Retained Earnings