Accounting Principles From Accounting Principles 7 th Edition

- Slides: 29

Accounting Principles From: Accounting Principles, 7 th Edition Weygandt • Kieso • Kimmel Prepared by Naomi Karolinski Monroe Community College and Marianne Bradford Bryant College John Wiley & Sons, Inc. © 2005

CHAPTER 1 ACCOUNTING IN ACTION WHAT IS ACCOUNTING? • • Accounting is an information system that identifies, records, and communicates the economic events of an organization to interested users. Akuntansi merupakan sistem informasi tentang identifikasi, pencatatan dan komunikasi tentang kejadian ekonomi dalam organisasi untuk kepentingan pengguna. •

THE ACCOUNTING PROCESS

Users of Accounting Information – Investors / investor – Creditors / kreditor – Suppliers / pemasok barang – Customers / pelanggan – Owners / pemilik perusahaan – Management / manajemen (direktur dan manajer) – Employees / karyawan – Others / Masyarakat

QUESTIONS ASKED BY INTERNAL USERS

QUESTIONS ASKED BY EXTERNAL USERS

BUSINESS ENTERPRISES • Proprietorship / perseorangan Owned by one person. • Partnership / firma atau CV Owned by two or more persons. • Corporation / PT Organized as a separate legal entity under state corporation law and having ownership divided into transferable shares of stock.

PERHATIAN DALAM AKUNTANSI • • Ethics / etika Standards by which actions are judged as right or wrong, honest or dishonest. Generally Accepted Accounting Principles (GAAP) Established by the F. A. S. B and the S. E. C. Pernyataan Standar Akuntansi Keuangan (PSAK) Penerbit Dewan Standar Akuntansi (DSAK/IAI) Assumptions /Asusmi – Monetary Unit Only data that can be expressed in terms of money is included in the accounting records. – Economic Entity Includes any organization or unit in society. - Going Concern - assumes organization will continue into foreseeable future

Prinsip Dasar Akuntansi • • • Fiscal Period Principle Historical Period Principle Accrual Basic Principle Revenue Realization Principle Cost Income Matching Principle Full Disclosure Principle Materiality Principle Consistency Principle Objectivity Principle Conservatism Principle

Persamaan Dasar Akuntansi Assets = Liabilities( + Owner’s Equity

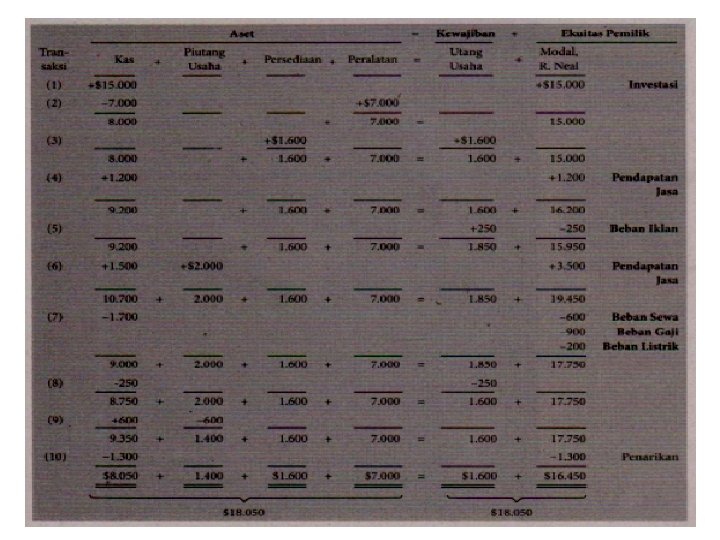

Contoh Soal • • • Tuan Ray Neal memutuskan untuk mendirikan perusahaan jasa pemrograman computer dengan nama “SOFTBYTE”. Pada tgl 1 september 2005 Tuan Ray Neal menginvestasikan uang tuani sebesar $15. 000 kedalam bisnis tersebut “SOFTBYTE” membeli peralatan berupa computer secara tunai sebesar $7. 000 “SOFTBYTE” membeli perlengkapan berupa ATK secara kredit sebesar $1. 600 “SOFTBYTE” menerima jasa pemrograman dari pelanggan secara tunai $1. 200 “SOFTBYTE” memasang iklan di sebuah surat kabar, pada saat di tagih “SOFTBYTE” menjanjikan akan di bayar minggu depan sebesar $250 “SOFTBYTE” menyerahkan jasa pemrograman seharga $3. 500 kepada pelanggan, namun pelanggan tersebut membayar sejumlah $1. 500 dan sisanya akan dibayar bulan depan “SOFTBYTE” membayar secara tunai sewa took sebesar $600, gaji karyawan $900 dan rekening listrik $200 “SOFTBYTE” membayar tagihan iklan sebesar $250 Diterima secara tunai tagihan dari pelanggan sejumlah$600 Tuan Ray Neal mengambil uang dari perusahaan sejumlah $1. 300 untuk keperluan pribadinya

Kelompok Aktiva/Harta • Assets are resources owned by a business. They are used in carrying out such activities as production, consumption and exchange. • Assets : Current Asset and Fixes Assets 1. Current Assets : Cash, Account receivable, Note Receivable, Inventory, Prepaid expenses, Accrued Revenues 2. Fixes Assets : Fixed tangible Assets and Fixed intangible Assets a. Fixed tangible Assets : land, Building, Furniture, Equipment Machine, Cars b. Fixed intangible Assets : Goodwill, Patent, Trade Mark

Kelompok Hutang/Kewajiban Liabilities = Assets - Owner’s Equity • Liabilities are creditor claims against assets or existing debts and obligations to creditors • Current Liabilities : Short Term Loan, Account Payable, Notes Payable, Accrued Expense • Long Term Liabilities : Bonds, Hipotek

Kelompok Modal Owner’s Equity = Assets - Liabilities • Owner’s Equity represents the ownership claim to total assets. Subdivisions of Owner’s Equity: 1 Capital or Investments by Owner (+) 2 Drawing (-) 3 Revenues (+) 4 Expenses (-). •

Kelompok Investasi • Investments • are the assets the owner puts in the business • increase owner’s equity

Kelompok Prive • Drawings • are withdrawals of cash or other assets by the owner for personal use • decrease owner’s equity

Kelompok Pendapatan/Penjualan • Revenues • gross increases in owner’s equity from business activities entered into for the purpose of earning income • may result from sale of merchandise, services, rental of property, or lending money • usually result in an increase in an asset

Kelompok Biaya/Beban • Expenses • decreases in owner’s equity that result from operating the business • cost of assets consumed or services used in the process of earning revenue • examples: utility expense, rent expense, supplies expense, and tax expense

Menaikan atau menurunkan modal pemilik Decreases Investments Withdrawals Owner’s Equity Revenues Expenses

Proses Identifikasi Transaksi

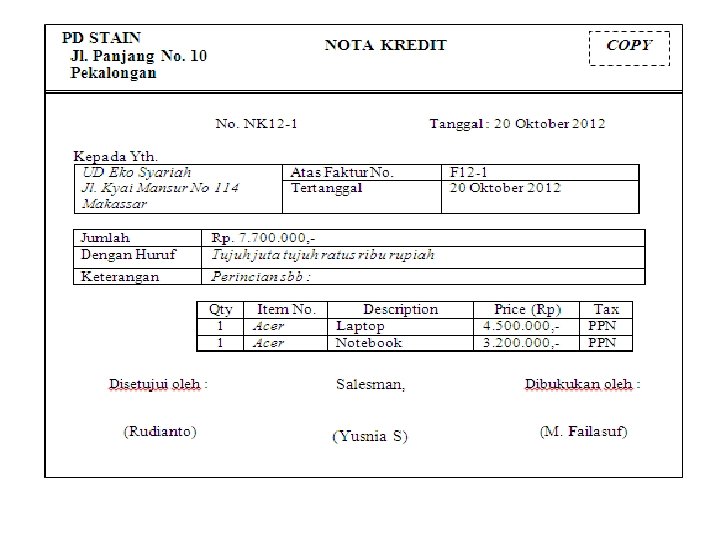

ANALISIS BUKTI TRANSAKSI Lima puluh enam juta dua ratus ribu rupiah

Laporan Keuangan • Four financial statements are prepared from the summarized accounting data: • Income Statement/ Laporan laba rugi revenues and expenses and resulting net income or net loss for a specific period of time • Owner’s Equity Statement/ Laporan perubahan equitas (modal) changes in owner’s equity for a specific period of time • Balance Sheet / Neraca assets, liabilities, and owner’s equity at a specific date • Statement of Cash Flows / Laporan arus kas cash inflows (receipts) and outflows (payments) for a specific of time period

FINANCIAL STATEMENTS AND THEIR INTERRELATIONSHIPS SOFTBYTE, INC. Income Statement For the Month Ended September 30, 2005 Revenues Service revenue Expenses Salaries expense Rent expense Advertising expense Utilities expense Total expenses Net income $ 4, 700 $ 900 600 250 200 1, 950 • $ 2, 750 Net income of $2, 750 shown on the income statement is added to the beginning balance of owner’s capital in the owner’s equity statement.

FINANCIAL STATEMENTS AND THEIR INTERRELATIONSHIPS SOFTBYTE, INC. Owner’s Equity Statement For the Month Ended September 30, 2005 Retained earnings, September 1, 2005 Add: Investments Net income Less: Drawings Retained earnings, September 30, 2005 $ 15, 000 2, 750 $ -017, 750 1, 300 • $16, 450 Net income of $2, 750 carried forward from the income statement to the owner’s equity statement. The owner’s capital of $16, 450 at the end of the reporting period is shown as the final total of the owner’s equity column of the Summary of Transactions (Illustration 1 -8).

FINANCIAL STATEMENTS AND THEIR INTERRELATIONSHIPS SOFTBYTE, INC. Balance Sheet September 30, 2005 Cash Accounts receivable Supplies Equipment Total assets Liabilities Accounts payable Owner’s equity Assets $ 8, 050 1, 400 1, 600 7, 000 $ 18, 050 Liabilities and Owner’s Equity R. Neal, capital Total liabilities and owner’s equity $ 1, 600 • 16, 450 $ 18, 050 Owner’s capital of $16, 450 at the end of the reporting period shown in the owner’s equity statement is shown on the balance sheet.

FINANCIAL STATEMENTS AND THEIR INTERRELATIONSHIPS SOFTBYTE, INC. Balance Sheet September 30, 2005 Assets Cash Accounts receivable Supplies Equipment Total assets • $ 8, 050 1, 400 1, 600 7, 000 $ 18, 050 Liabilities and Owner’s Equity Liabilities Accounts payable Owner’s equity R. Neal, capital Total liabilities and owner’s equity $ 1, 600 16, 450 $ 18, 050 Cash of $8, 050 on the balance sheet is reported on the statement of cash flows.

FINANCIAL STATEMENTS AND THEIR INTERRELATIONSHIPS SOFTBYTE, INC. Statement of Cash Flows For the Month Ended September 30, 2005 Cash flows from operating activities Cash receipts from revenues Cash payments for expenses Net cash provided by operating activities Cash flows from investing activities Purchase of equipment Cash flows from financing activities Sale of common stock Payment of cash dividends Net cash provided by financing activities Net increase in cash Cash at the beginning of the period Cash at the end of the period $ 3, 300 (1, 950) 1, 350 (7, 000) $ 15, 000 (1, 300) 13, 700 8, 050 – 0– • $ 8, 050 Cash of $8, 050 on the balance sheet and statement of cash flows is shown as the final total of the cash column of the Summary of Transactions (Illustration 1 -8).