1 Fixed Income Securities Analysis Copyrights 2004 9

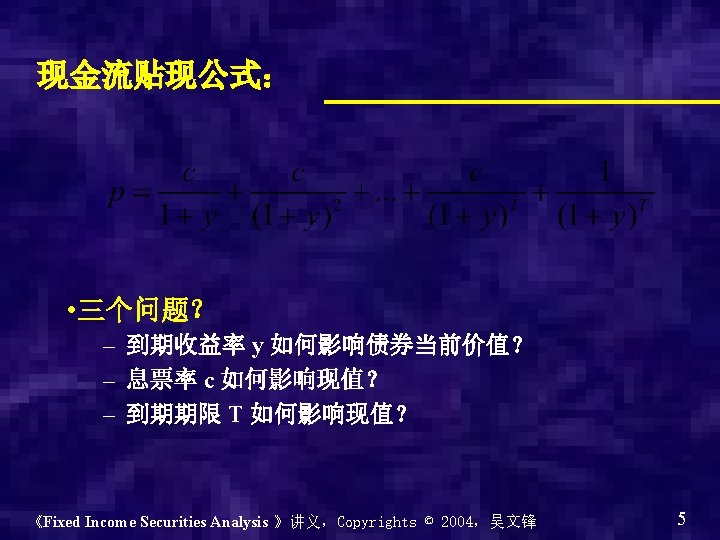

债券价值是c/y和1的加权平均。推论: 票面利率,到期收益率,与价格 YTM = coupon rate: par value bond coupon rate > YTM")

")

• 注意事项: –")

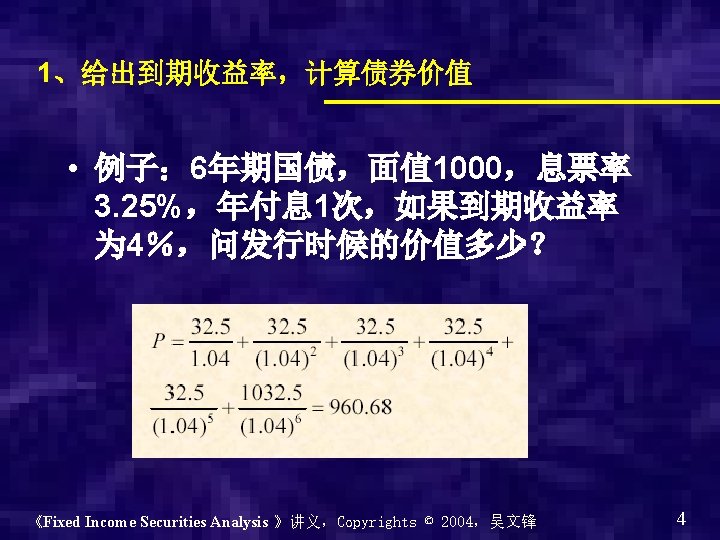

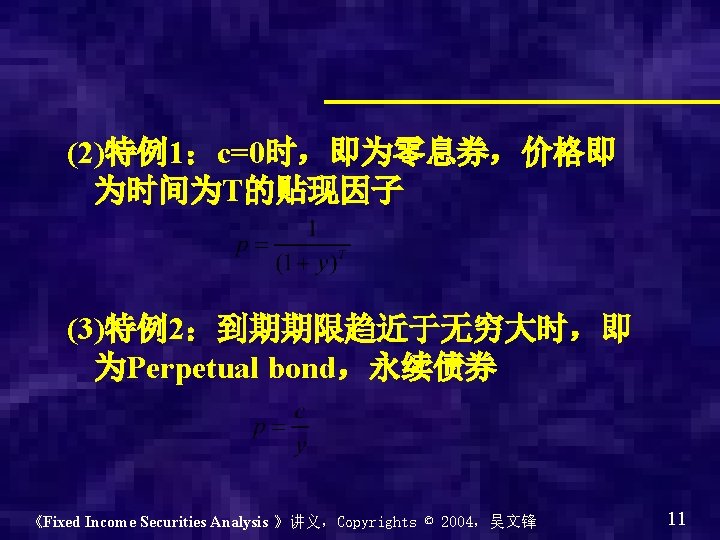

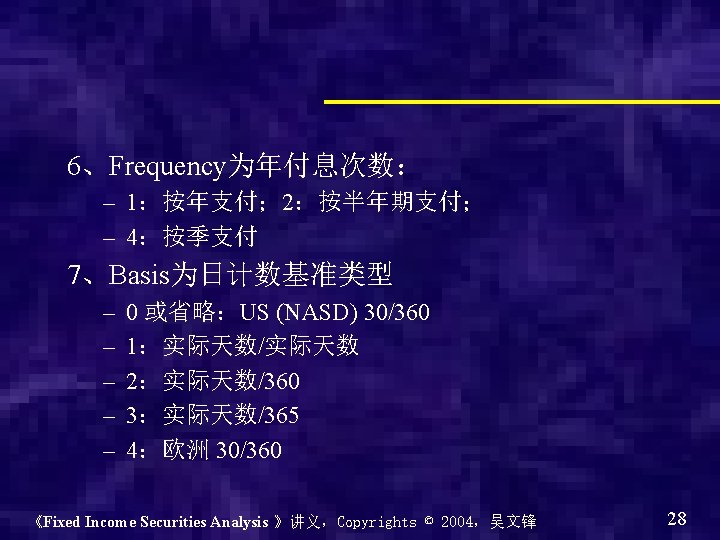

5、Redemption为面值 $100 的有价证券的 清偿价值 《Fixed Income Securities Analysis")

=32. 5+ x • Fisher方程: B 0(1+i) = c +")

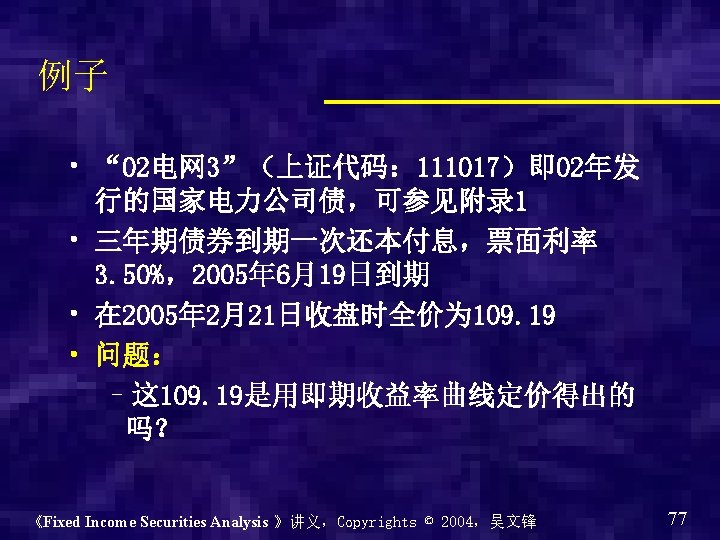

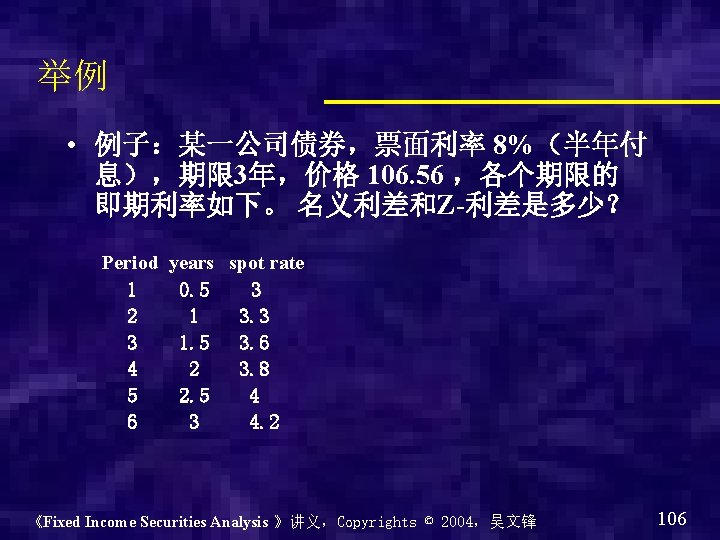

• 上市日期: 2001 -8 -20 • 息票率为: 4. 26%,年支付")

– – – 国债 政府机构债券、市政债券 公司债券 MBS")

, bp issuer Rating 2 -year 5 -year Merrill Lynch Aa")

– 不同信用评级的两种债券之间的到期收益 率差,但其他方面都一样,包括期限,息 票率等 • 信用利差与经济周期")

Sector AAA AA A Industrials 90 97 128 Utility 88 94")

• OAS ? P 0 3. 00%+r.")

- Slides: 161

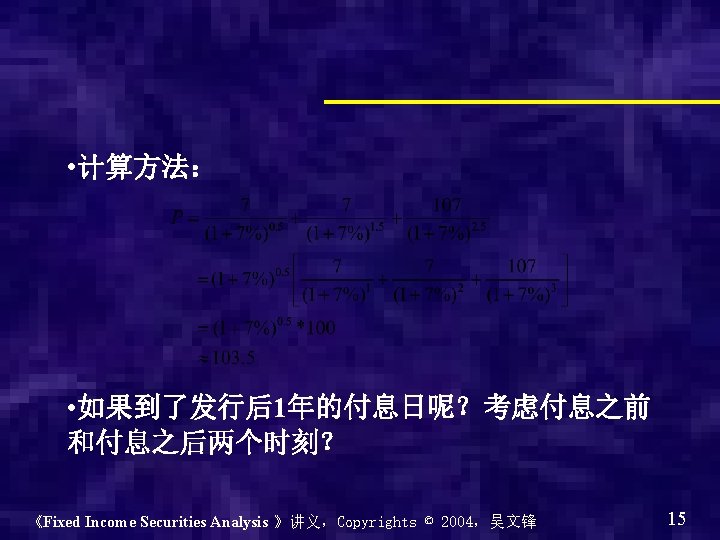

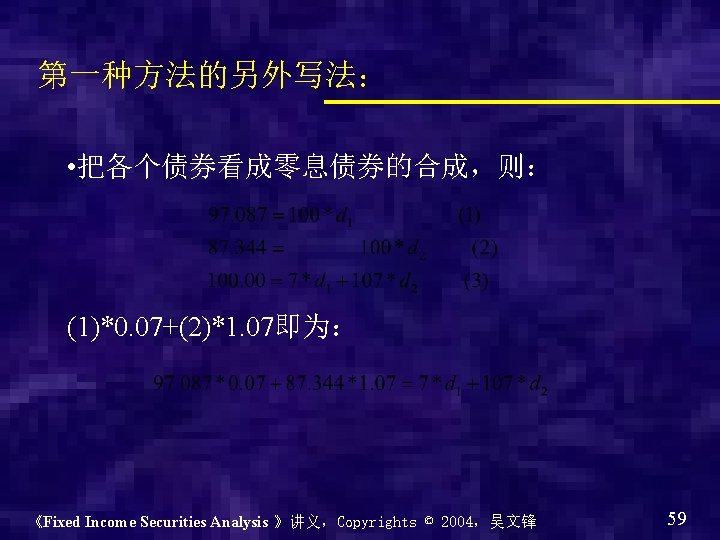

假设面值为 1,定价公式作个变换: 《Fixed Income Securities Analysis 》讲义,Copyrights © 2004,吴文锋 9

经济含义: (1)债券价值是c/y和1的加权平均。推论: 票面利率,到期收益率,与价格 YTM = coupon rate: par value bond coupon rate > YTM : premium bond coupon rate < YTM : discount bond 《Fixed Income Securities Analysis 》讲义,Copyrights © 2004,吴文锋 10

• 付息之前: • 付息之后: 《Fixed Income Securities Analysis 》讲义,Copyrights © 2004,吴文锋 16

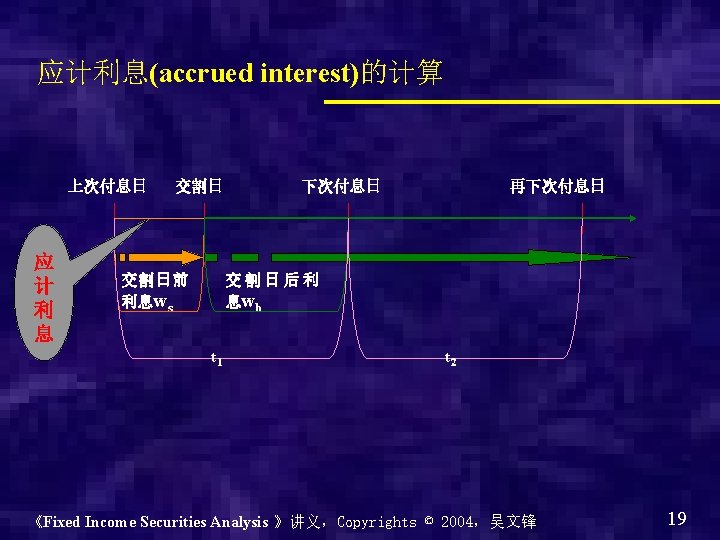

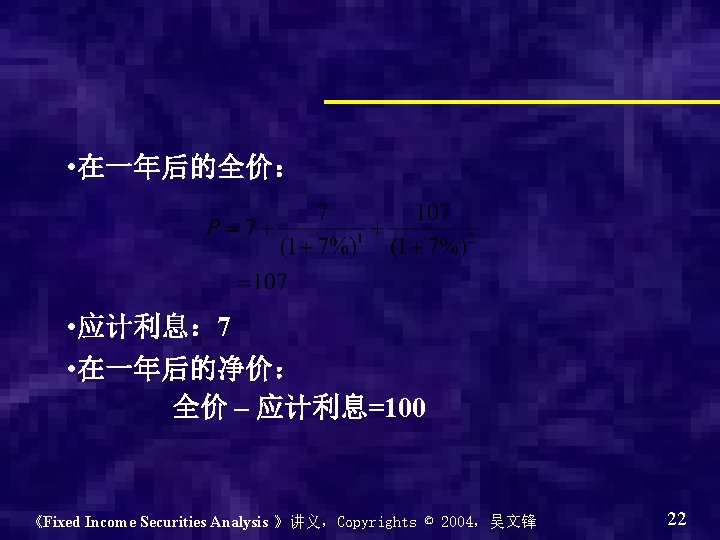

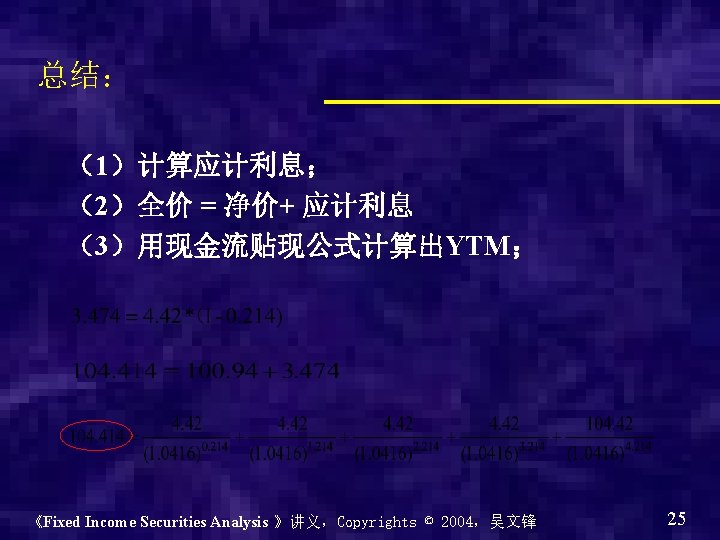

• 全价 • 应计利息: 7*0. 5=3. 5 • 净价: 全价 – 应计利息=103. 5 -3. 5=100 《Fixed Income Securities Analysis 》讲义,Copyrights © 2004,吴文锋 21

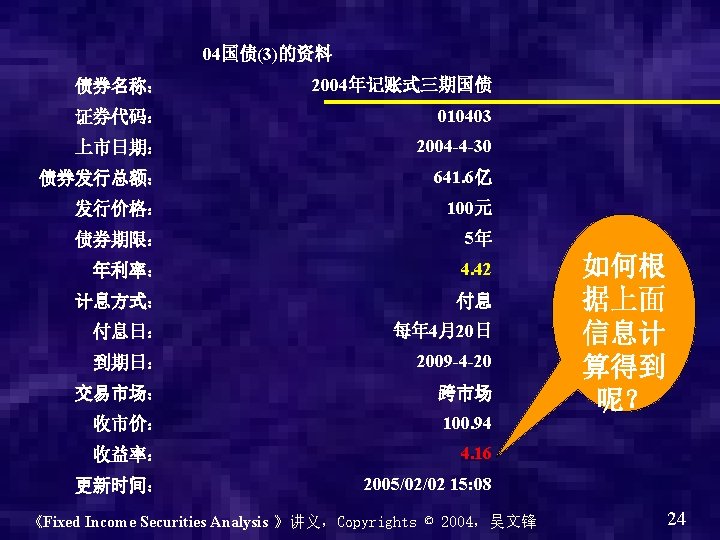

Exercise: • 进入中国国债投资网 http: //www. gz 998. com/ • 国债收益率: 名称 代码 收益率 03国债(8) 010308 4. 73 03国债(11) 010311 4. 46 04国债(1) 010401 2. 2 04国债(3) 010403 4. 16 04国债(4) 010404 4. 49 04国债(5) 010405 2. 66 04国债(7) 010407 4. 48 《Fixed Income Securities Analysis 》讲义,Copyrights © 2004,吴文锋 23

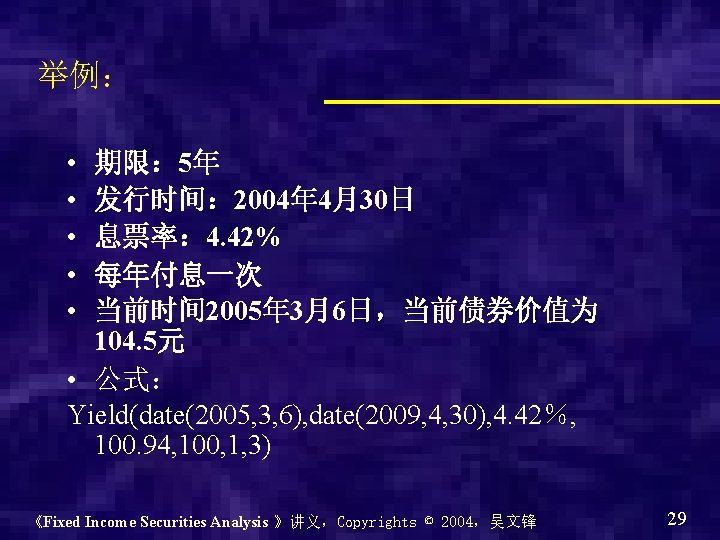

Excel 2003中的Yield函数 • YIELD(settlement, maturity, rate, pr, redemption, frequ ency, basis) • 注意事项: – 使用函数 DATE(2008, 5, 23) 表示 2008 年 5 月 23 日 • 相关函数 – YIELDDISC(settlement, maturity, pr, redemption, basis):不付息 的债券的yield – YIELDMAT(settlement, maturity, issue, rate, pr, basi s):到期日付息的债券的yield 《Fixed Income Securities Analysis 》讲义,Copyrights © 2004,吴文锋 26

1、Settlement是成交日 2、Maturity为到期日 3、Rate为年息票利率。 4、Pr为面值 $100 的价格(净价) 5、Redemption为面值 $100 的有价证券的 清偿价值 《Fixed Income Securities Analysis 》讲义,Copyrights © 2004,吴文锋 27

《Fixed Income Securities Analysis 》讲义,Copyrights © 2004,吴文锋 31

Price-Yield-Time Relationship • Price of premium bond converges to par value at maturity (premium is getting lower) • Price of discount bond converges to par value at maturity (discount is getting higher) 《Fixed Income Securities Analysis 》讲义,Copyrights © 2004,吴文锋 32

《Fixed Income Securities Analysis 》讲义,Copyrights © 2004,吴文锋 34

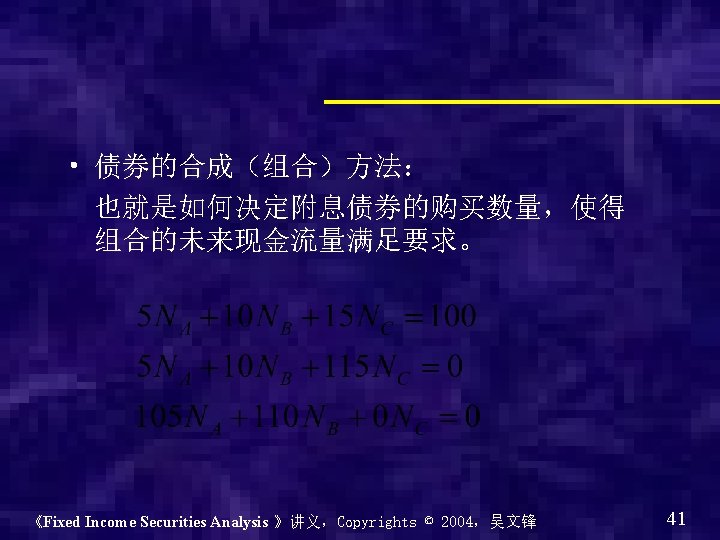

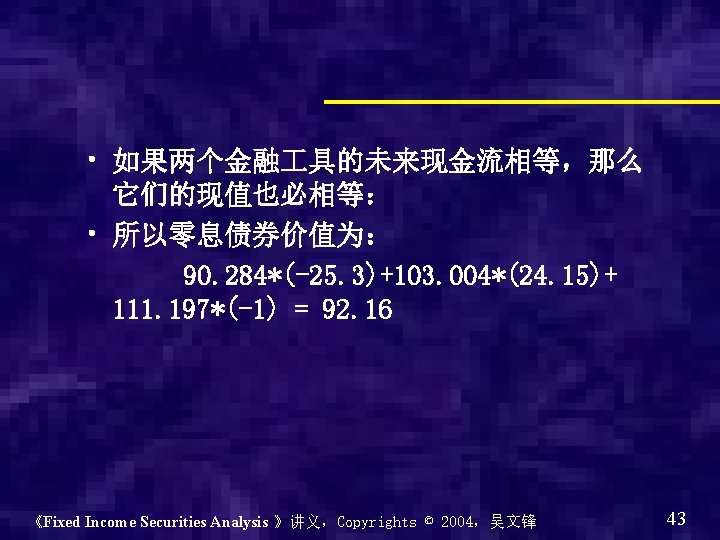

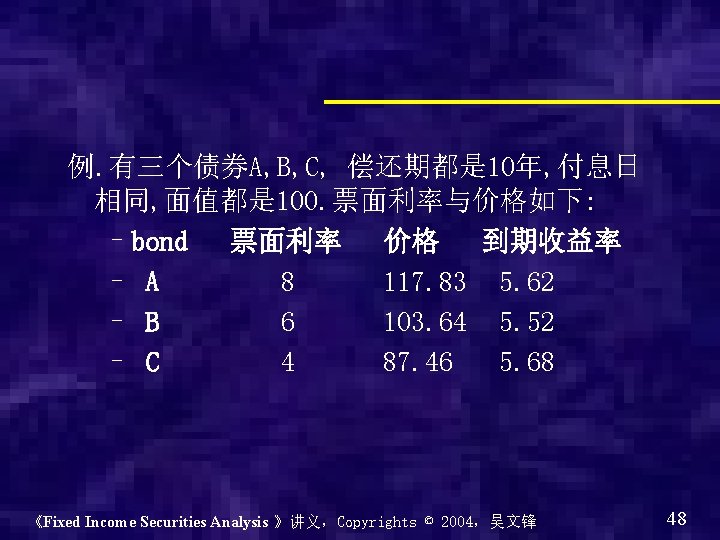

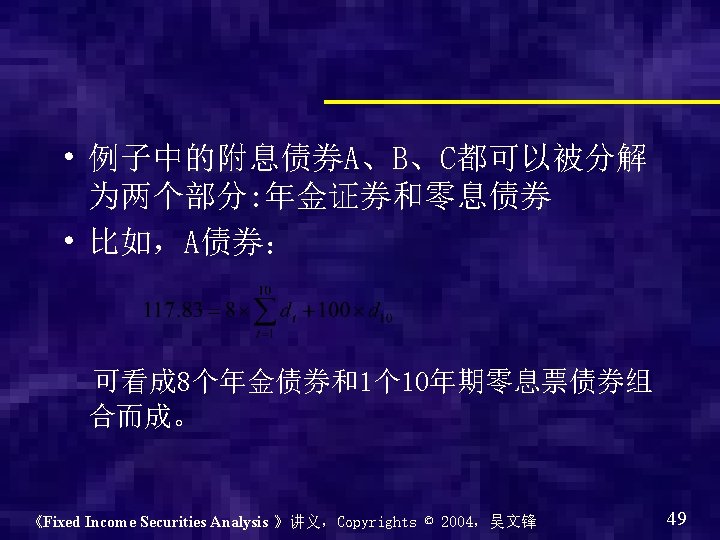

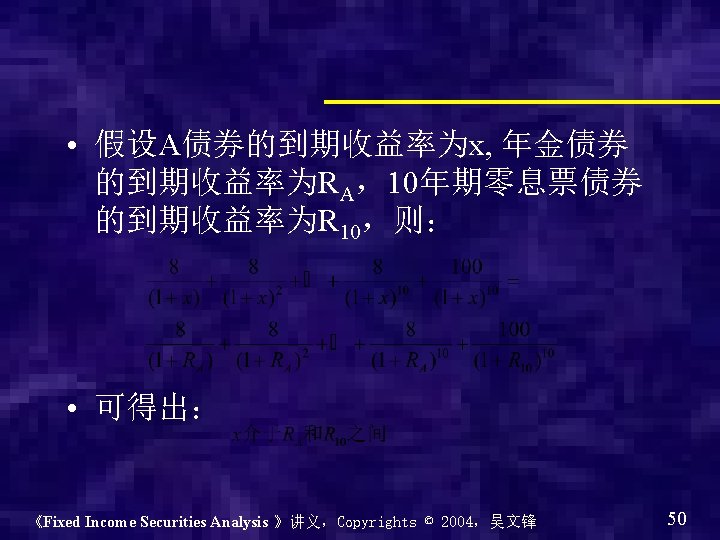

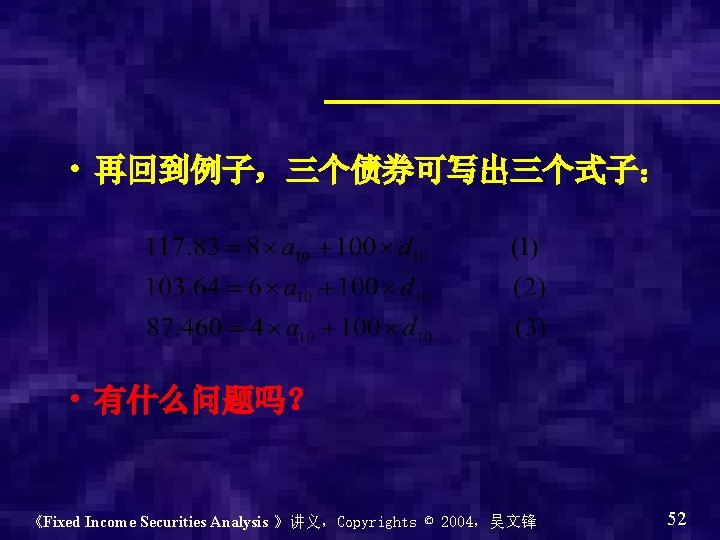

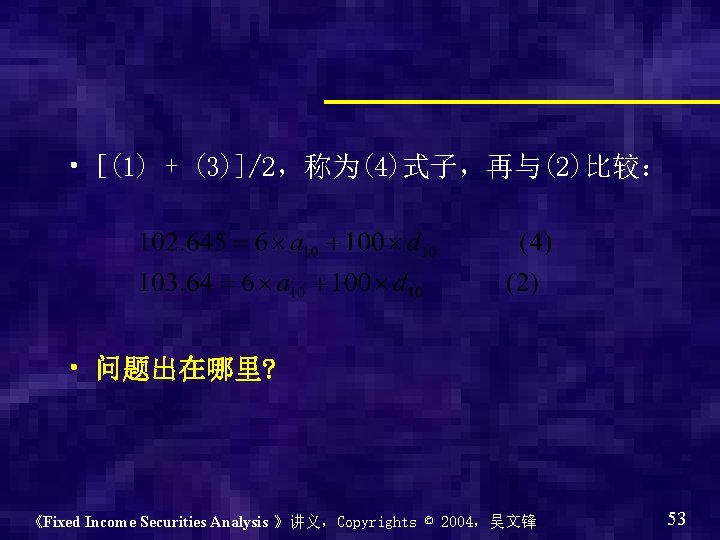

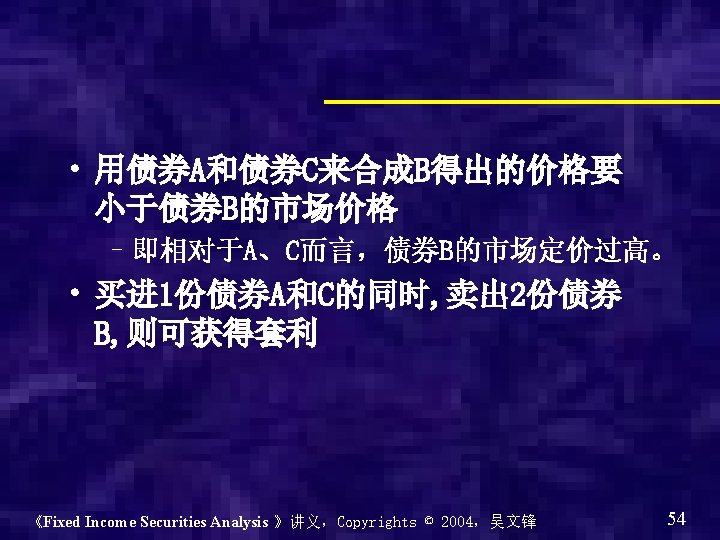

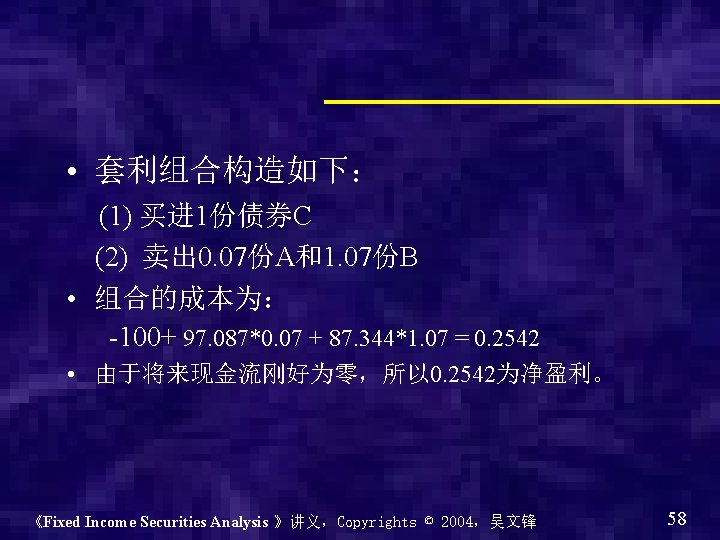

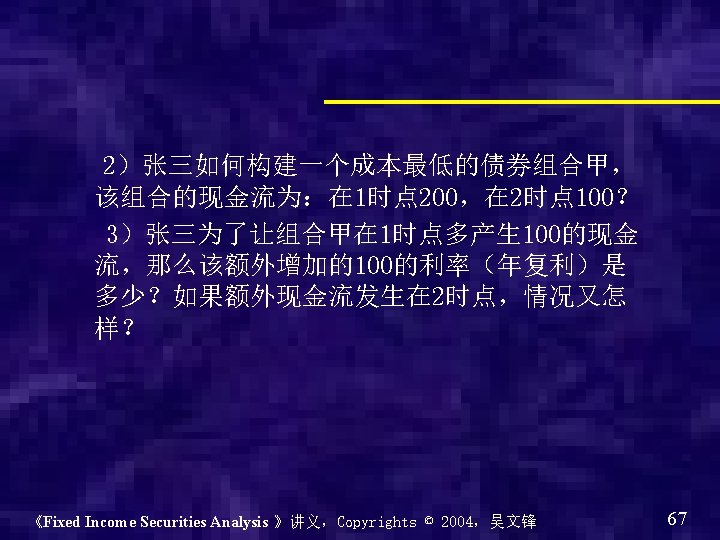

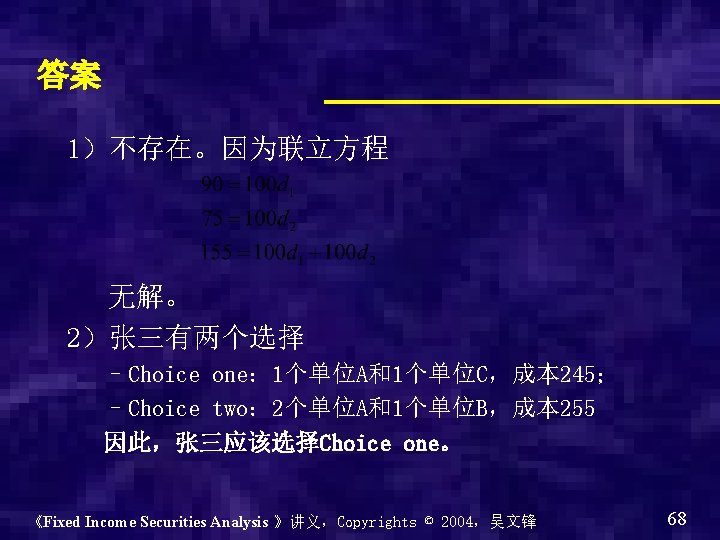

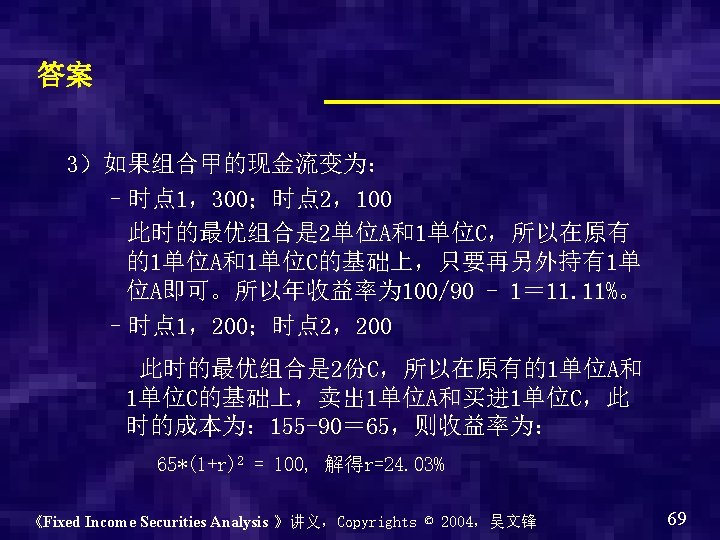

• 例: 有三个附息债券 Time 0 1 2 3 A -90. 284 5 5 105 B -103. 004 10 10 110 C -111. 197 15 115 0 • 问题:如何通过A、B、C来构建一个 1年期的 零息债券,面值 100? 《Fixed Income Securities Analysis 》讲义,Copyrights © 2004,吴文锋 40

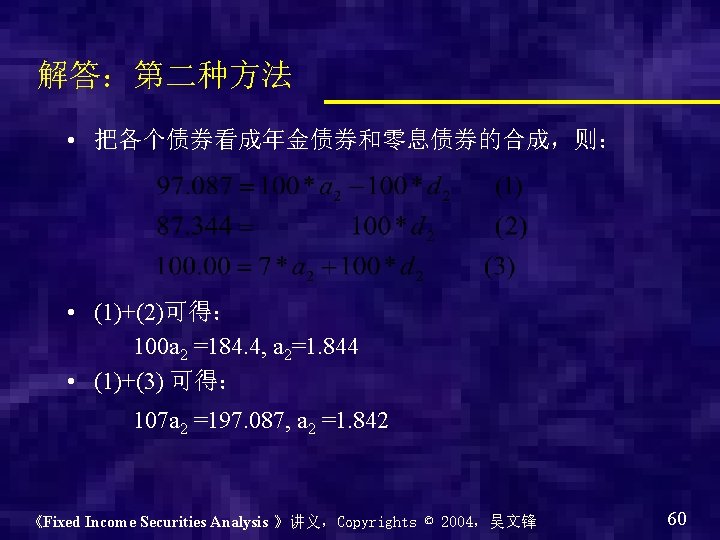

• 求解方程 《Fixed Income Securities Analysis 》讲义,Copyrights © 2004,吴文锋 42

合成债券的一般方法 《Fixed Income Securities Analysis 》讲义,Copyrights © 2004,吴文锋 44

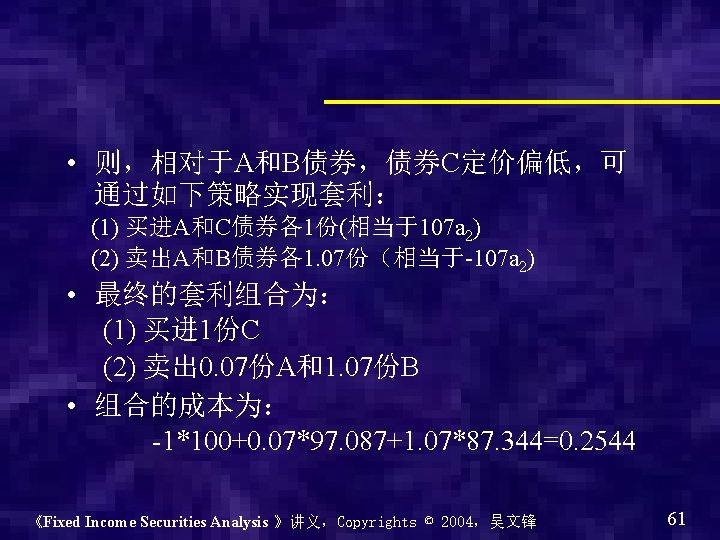

• 上面的例子说明: – 有时候息票剥离,或者说把付息债券的利 息和本金分开来卖,则可赚取套利 – It is possible to strip coupons from U. S. Treasuries and resell them, and aggregates tripped coupons and reconstitute them into U. S. Treasury coupon bonds 《Fixed Income Securities Analysis 》讲义,Copyrights © 2004,吴文锋 62

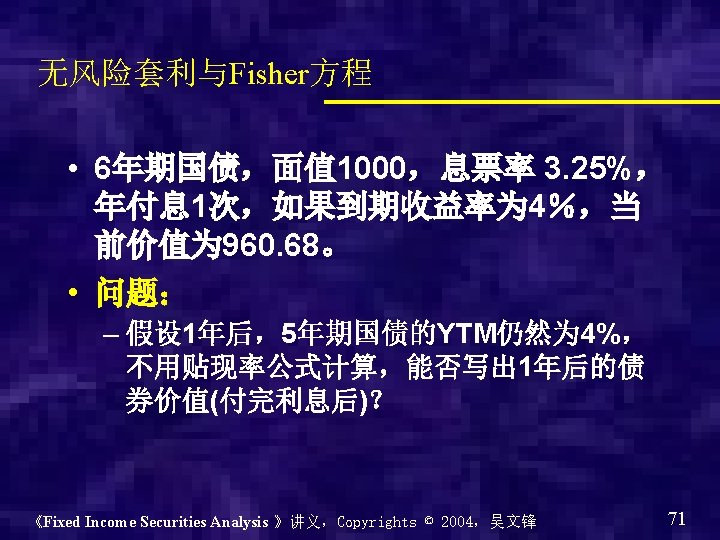

• 债券的1年投资回报率应该等于无风险利率 960. 68*(1+4%)=32. 5+ x • Fisher方程: B 0(1+i) = c + B 1 i=c/B 0+ΔB/ B 0, 即y=current yield+ΔB/ B 0 • 葡萄园租金与名� 利率 《Fixed Income Securities Analysis 》讲义,Copyrights © 2004,吴文锋 72

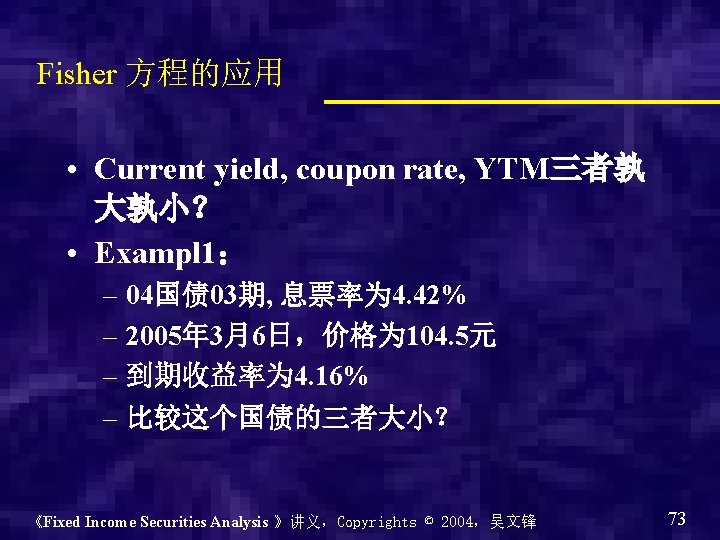

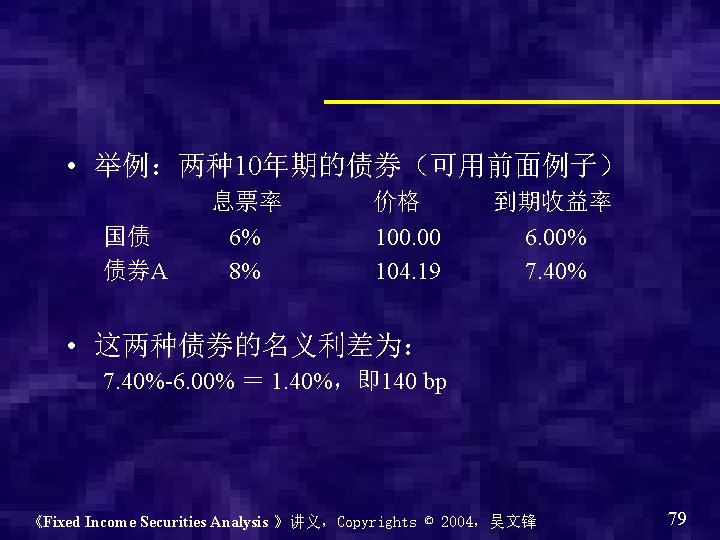

Example 2: • 2001记帐 7期(20年) • 上市日期: 2001 -8 -20 • 息票率为: 4. 26%,年支付 1次 • 到期日: 2021 -8 -20 • 当前时间: 2005 -3 -6,价格: 93. 85 • 问题: Current yield, coupon rate, YTM三者孰 大孰小? 《Fixed Income Securities Analysis 》讲义,Copyrights © 2004,吴文锋 74

利差的度量方法 • Absolute spread yield A - yield B • Relative spread (yield A - yield B)/ yield B • Yield ratio yield A / yield B 《Fixed Income Securities Analysis 》讲义,Copyrights © 2004,吴文锋 80

Example: • Two bonds, A and B have yields of 4. 75% and 5. 5%, respectively. Using bond A as a reference bond, we get three yield spreads. Absolute = 5. 5 – 4. 75 = 75 bp Relative = 0. 75 / 4. 75 = 0. 158 Yield ratio = 5. 5 / 4. 75 = 1. 158 《Fixed Income Securities Analysis 》讲义,Copyrights © 2004,吴文锋 81

Yield Spread Measures • Absolute yield spread is the most commonly used. – May stay at the same level if interest rates are rising or falling • The relative yield spread and yield ratio are better measures 《Fixed Income Securities Analysis 》讲义,Copyrights © 2004,吴文锋 82

Yield Spread Measures Embedded options affect yield spreads – Higher yield to offset risk – Overstatement and understatement of the true yield 《Fixed Income Securities Analysis 》讲义,Copyrights © 2004,吴文锋 83

板块间利差与板块内利差 • 板块间利差 ( Intermarket yield spread) – – – 国债 政府机构债券、市政债券 公司债券 MBS ABS 外国债券 • 板块内利差 ( Intramarket yield spread) – on-the-run and off-the-run – AAA and BBB, etc. 《Fixed Income Securities Analysis 》讲义,Copyrights © 2004,吴文锋 84

举例 • 相对于美国国债的利差 (7/23/99), bp issuer Rating 2 -year 5 -year Merrill Lynch Aa 3 90 115 Citicorp Aa 2 84 118 Bank America Aa 3 86 120 Time Warner Baa 3 87 111 Philip Morris A 2 97 120 Sprint Baa 1 85 105 MCI/World com A 3 74 95 7 -year 125 123 128 120 135 116 10 -year 148 135 138 155 140 119 30 -year 167 160 162 158 175 158 136 问题:为什么不同公司债券利差不同? 《Fixed Income Securities Analysis 》讲义,Copyrights © 2004,吴文锋 85

极� � 投 � 良 � � 尚可 S&P’s Fitch Moody’s AAA AA+ Aaa Aa 1 AA AA Aa 2 AA- Aa 3 A+ A+ A 1 A A A 2 A- A- A 3 BBB+ Baa 1 BBB Baa 2 BBB- Baa 3 《Fixed Income Securities Analysis 》讲义,Copyrights © 2004,吴文锋 86

S&P’ Moody’ Fitch s s 投机性 BB+ Ba 1 BB BB Ba 2 BB- Ba 3 B+ B+ B 1 B B B 2 B- B- B 3 投 机 � 高� � � 《Fixed Income Securities Analysis 》讲义,Copyrights © 2004,吴文锋 87

投 机 � � � 以存活 即将倒� S&P’s Fitch Moody’s CCC+ Caa 1 CCC Caa 2 CCC- Caa 3 CC CC Ca C C C SD DDD D 《Fixed Income Securities Analysis 》讲义,Copyrights © 2004,吴文锋 88

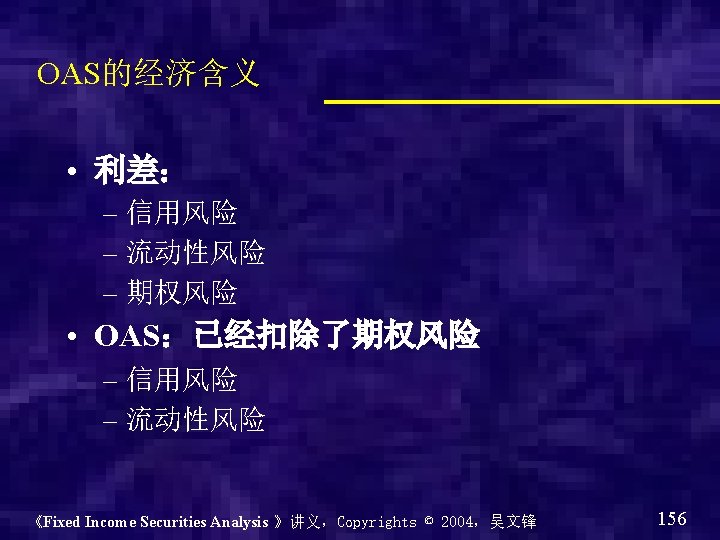

信用利差 • 信用利差 ( Credit Yield Spread ) – 不同信用评级的两种债券之间的到期收益 率差,但其他方面都一样,包括期限,息 票率等 • 信用利差与经济周期 – During an expanding economy, credit spreads decline – “Flight to quality” in weak markets/economy 《Fixed Income Securities Analysis 》讲义,Copyrights © 2004,吴文锋 90

信用利差 • 不同行业的利差(7/23/99) Sector AAA AA A Industrials 90 97 128 Utility 88 94 110 Finance 94 120 134 Banks 120 130 《Fixed Income Securities Analysis 》讲义,Copyrights © 2004,吴文锋 BBB 152 137 158 145 91

流动性 • 流动性越好,利差越小 – Greater liquidity = lower spread • 影响流动性的因素 – on-the-run and off-the-run – 规模 – 投资需求 – 其他风险 《Fixed Income Securities Analysis 》讲义,Copyrights © 2004,吴文锋 92

• 根据即期收益率曲线,可得国债的价格 为: discount present Period 1 2 3 4 5 6 years 0. 5 1 1. 5 2 2. 5 3 spot rate cash flow factor value 3 3. 6 3. 8 4 4. 2 4 4 4 104 0. 99 0. 97 0. 95 0. 93 0. 91 0. 88 price 3. 94 3. 87 3. 79 3. 71 3. 63 91. 92 110. 87 《Fixed Income Securities Analysis 》讲义,Copyrights © 2004,吴文锋 108

• 通过EXCEL过程,算出 – 国债的YTM=4. 14 – 公司债券的YTM=5. 66 • 名义利差: – 5. 66 – 4. 14 = 1. 52,即 152个bp 《Fixed Income Securities Analysis 》讲义,Copyrights © 2004,吴文锋 109

计算 Z-利差 Peri od spot rate treasury 1 3 3. 94 3. 92 3. 90 3. 91 2 3. 3 3. 87 3. 84 3. 80 3. 82 3 3. 6 3. 79 3. 74 3. 69 3. 71 4 3. 8 3. 71 3. 64 3. 57 3. 61 5 4 3. 63 3. 54 3. 46 3. 50 6 4. 2 91. 92 89. 33 86. 83 88. 07 price 110. 87 108. 01 105. 25 106. 61 Zs-100 Zs-200 《Fixed Income Securities Analysis 》讲义,Copyrights © 2004,吴文锋 Zs-150 111

• 在EXCEL中的计算可得: – Z利差为: 150 bp 《Fixed Income Securities Analysis 》讲义,Copyrights © 2004,吴文锋 112

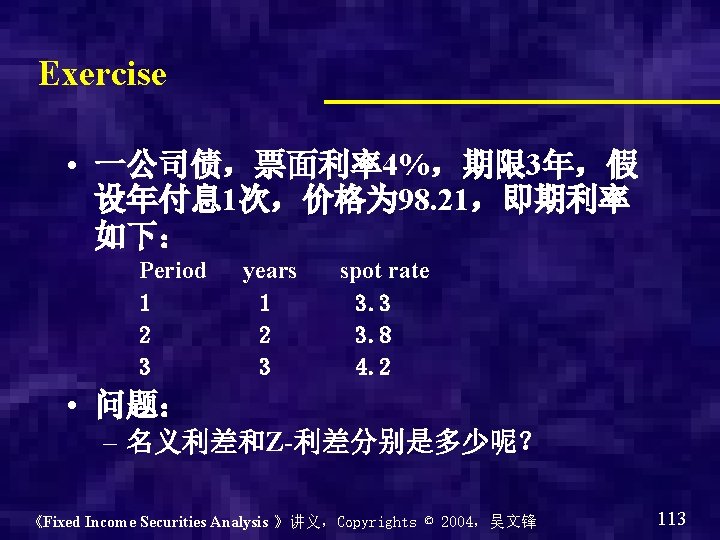

Period years spot rate cash discount present factor value 1 2 3 3. 8 4. 2 4 4 104 0. 9681 0. 9281 0. 8839 price 3. 8722 3. 7125 91. 9243 99. 51 《Fixed Income Securities Analysis 》讲义,Copyrights © 2004,吴文锋 114

• 答案: – 国债的YTM: 4. 176% – 公司债的YTM: 4. 653% – 名义利差: 4. 653% - 4. 176% = 47. 7 bp – Z-利差: 47. 5 bp 《Fixed Income Securities Analysis 》讲义,Copyrights © 2004,吴文锋 115

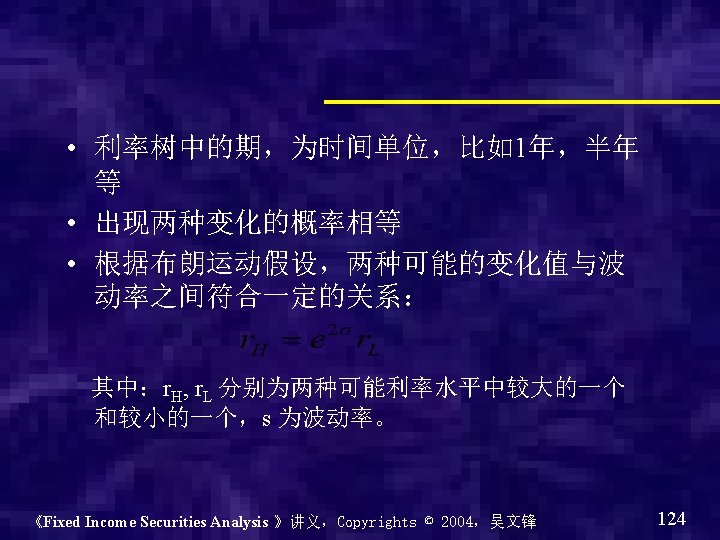

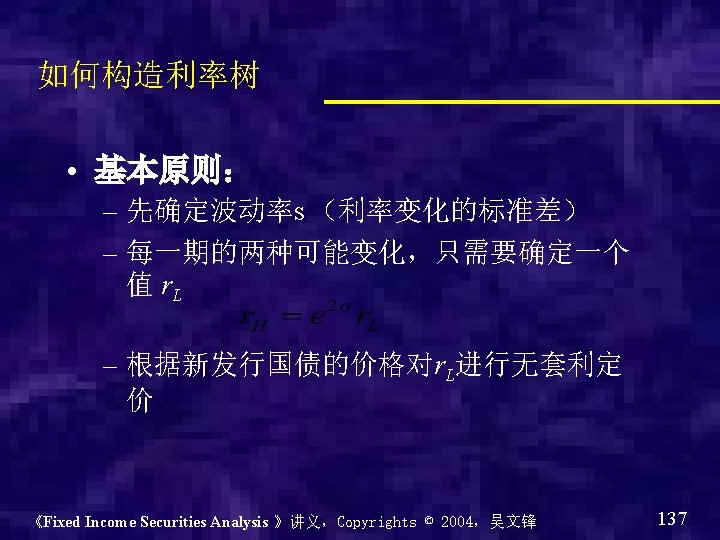

两期的利率树 6. 9146% 4. 4225% 5. 6612% 3. 00% 3. 6208% 4. 6350% 《Fixed Income Securities Analysis 》讲义,Copyrights © 2004,吴文锋 123

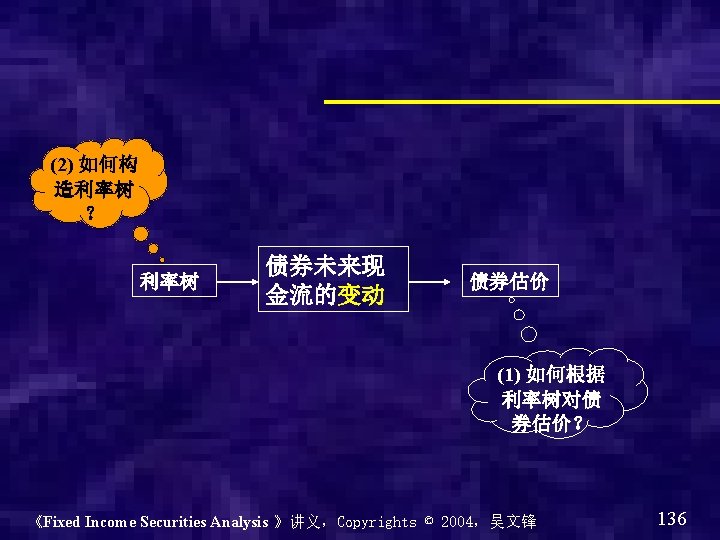

利率树和未来现金流树 100 4 4 4. 4225% ? 3. 00% 3. 6208% 4 100 4 利率树 未来现金流树 《Fixed Income Securities Analysis 》讲义,Copyrights © 2004,吴文锋 127

利率树和现金流树合并 ? P 1. H 100 4 4 4. 4225% ? P 0 3. 00% ? P 1. L 4 3. 6208% 100 4 《Fixed Income Securities Analysis 》讲义,Copyrights © 2004,吴文锋 128

根据利率树贴现 《Fixed Income Securities Analysis 》讲义,Copyrights © 2004,吴文锋 129

100 4 100. 9521 3. 00% 99. 5954 4 4. 4225% 100. 3659 4 3. 6208% 100 4 《Fixed Income Securities Analysis 》讲义,Copyrights © 2004,吴文锋 130

100 4 ? 3. 00% 根据可赎回条 件,发行人会 以 100赎回 99. 5954 4 4. 4225% 100. 3659 4 3. 6208% 100 4 《Fixed Income Securities Analysis 》讲义,Copyrights © 2004,吴文锋 132

? P 0 3. 00% 99. 5954 4 4. 4225% 100 4 3. 6208% 100 4 《Fixed Income Securities Analysis 》讲义,Copyrights © 2004,吴文锋 133

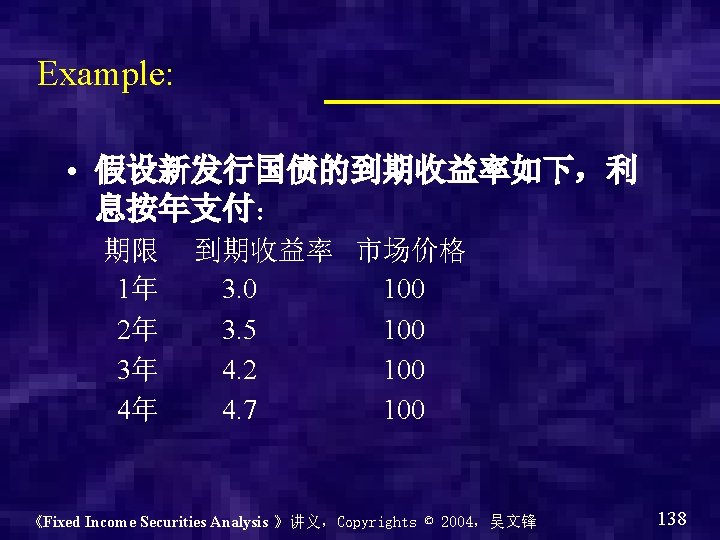

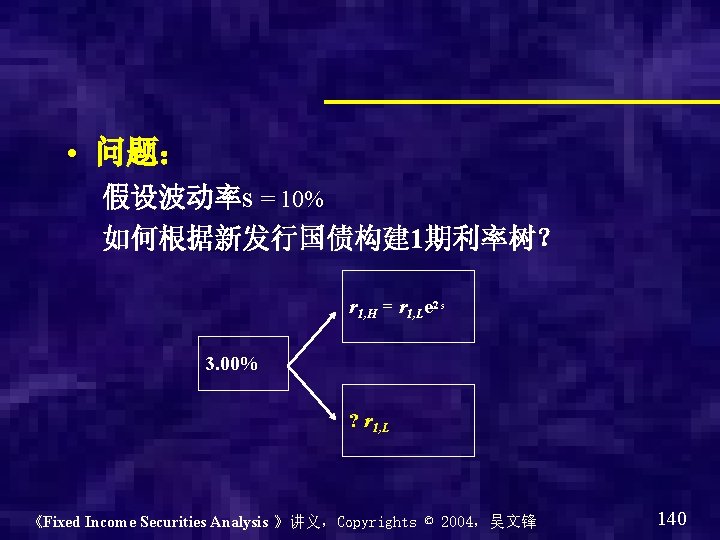

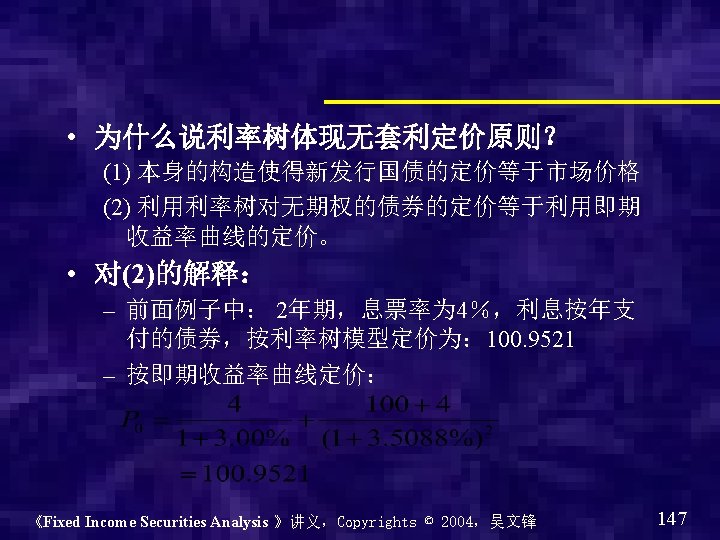

题外话:回顾Bootstrapping • 运用Bootstrapping技术可求得即期利率: 期限 1年 2年 3年 4年 到期收益率 市场价格 3. 0 100 3. 5 100 4. 2 100 4. 7 100 即期利率 3. 00 3. 5088 4. 2373 4. 7689 《Fixed Income Securities Analysis 》讲义,Copyrights © 2004,吴文锋 139

• 当 r 1, L = 4. 0% 99. 6108 3. 00% 100. 00 3. 50 98. 6789 3. 50 4. 8856% 99. 5192 3. 50 4. 00% 100. 00 3. 50 《Fixed Income Securities Analysis 》讲义,Copyrights © 2004,吴文锋 142

• 减少r 1, L ,变为 3. 50% 100. 1247 3. 00% 100. 00 3. 50 99. 2569 3. 50 4. 2749% 100. 00 3. 50% 100. 00 3. 50 《Fixed Income Securities Analysis 》讲义,Copyrights © 2004,吴文锋 143

• 最后,得到无套利定价的利率树 100. 00 3. 50 100. 0000 3. 00% 99. 1166 3. 50 4. 4225% 99. 8834 3. 50 3. 6208% 100. 00 3. 50 《Fixed Income Securities Analysis 》讲义,Copyrights © 2004,吴文锋 144

Exercise: • 如何构造两期的利率树 4. 4225% 100. 0000 3. 00% 3. 6208% ?r 2, LL 《Fixed Income Securities Analysis 》讲义,Copyrights © 2004,吴文锋 145

答案: 100. 00 4. 20 100. 0000 3. 00% 97. 9090 4. 20 4. 4225% 99. 6911 4. 20 3. 6208% 97. 4610 4. 20 6. 9146% 98. 6171 4. 20 5. 6612% 99. 5843 4. 20 4. 6350% 100. 00 4. 20 《Fixed Income Securities Analysis 》讲义,Copyrights © 2004,吴文锋 146

• Z – Spread (static spread) • OAS ? P 0 3. 00%+r. OAS 99. 5954 4 4. 4225% +r. OAS 100 4 3. 6208% +r. OAS 100 4 《Fixed Income Securities Analysis 》讲义,Copyrights © 2004,吴文锋 154

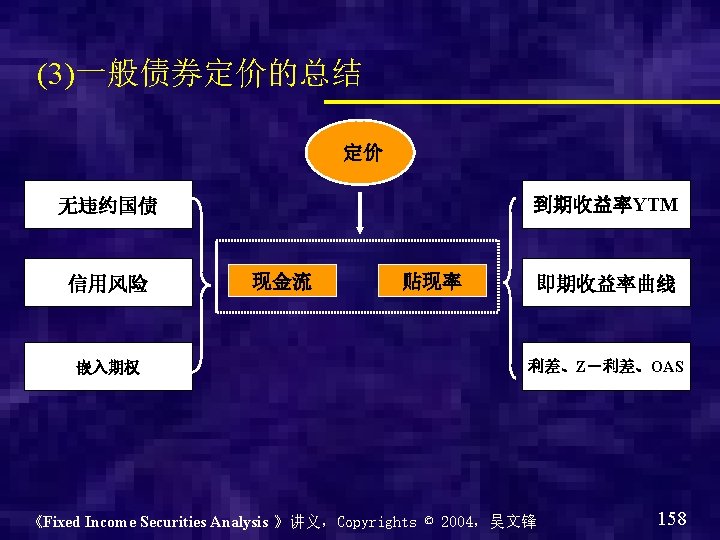

定价过程 • Estimate the cash flows • Determine the appropriate discount rate—riskfree rate + a risk premium • Calculate the sum of present values of the estimated cash flows • The value of a bond is a function of the present value of future cash flow from coupons and the principal 《Fixed Income Securities Analysis 》讲义,Copyrights © 2004,吴文锋 159

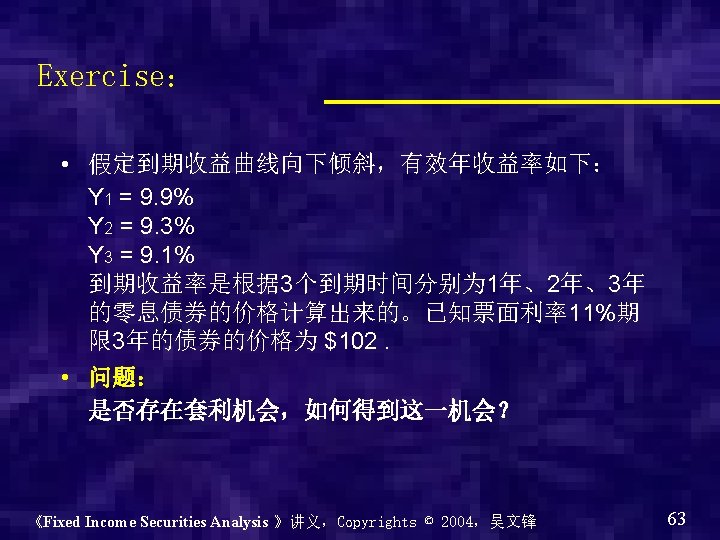

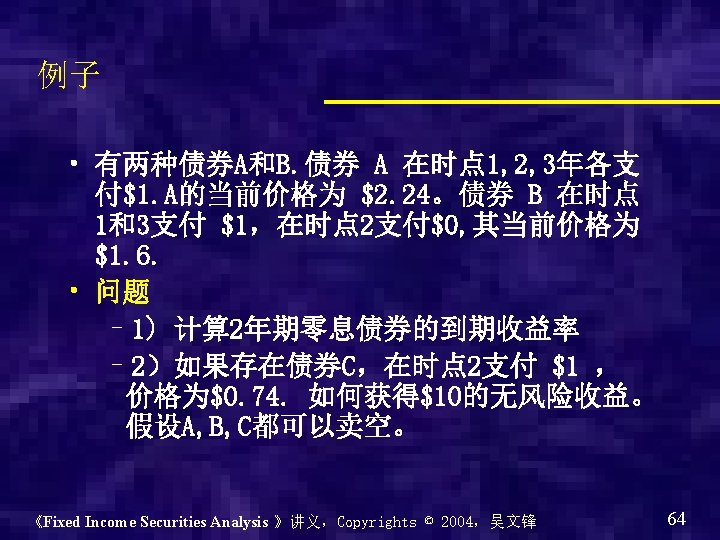

Difficulties in valuing bonds • • Credit problems Embedded options—e. g. call features Variable rate coupons Conversion privileges 《Fixed Income Securities Analysis 》讲义,Copyrights © 2004,吴文锋 161