Participation Questions Chapter 9 The capital structure of

– unlimited attempts")

bond and how are they issued? Bond – formal debt")

Face Value")

")

What is the BIG Idea? - Present value")

Present value depends on: ¡ ¡ ¡ Amount")

32 Rate Maturity Bid Ask/yld 7¾ Feb.")

")

$3,")

Interest expense $3, 728 Carrying value")

")

- Slides: 70

Participation Questions – Chapter 9 ¡ ¡ ¡ The capital structure of an organization is the mixture of debt funding and equity funding. T/F Ford Automotive uses a higher level of equity funding in comparison to debt funding. T/F “Coupon Rate” is the same as which of the following on a bond: l Market interest rate l Stated interest rate l The Dow Jones interest rate l LIBOR interest rate How much did the Hersey bar cost from the 1950’s as shown in the Seinfeld episode? The cash amount of interest paid to a bond holder is based on which of the following under the effective interest rate method? l Face Value l Carrying Value

Announcements ¡ Assignments – Due 4/10/16 l Chapter 9 Homework (Connect) – unlimited attempts l Participation questions for Chapter 9 (Webcourses) – 1 attempt l Syllabus Quiz #2 (Webcourses) – 2 attempts ¡ Assignments – Due 4/17/16 l Chapter 10 Homework (Connect) – unlimited attempts l Participation questions for Chapter 10 (Webcourses) – 1 attempt l Definitions Quiz (Webcourses) – 2 attempts Short tutorials in Class Materials

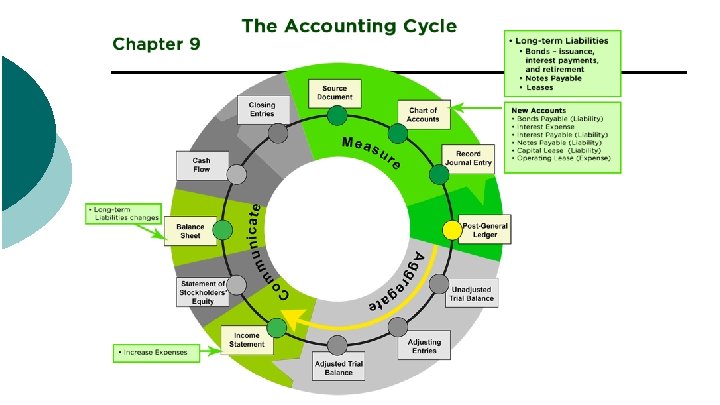

Questions to be Answered Overall - How has society shaped today’s financial reporting? Chapter 9 – How do companies use the different types of long-term financing (bonds, notes, and leases) and what are the impacts to the income statement and balance sheet?

Part A Overview of Long Term Debt 9 -5

Accounting Equation

LO 1 Explain financing alternatives o o Financing Options o Debt Financing - borrowing money (liabilities) o Bonds – most common form of Lg. Corp debt o Notes Payable (typically bank financing) o Leases o Equity Financing - obtaining additional investment from stockholders (stockholders’ equity) Capital Structure - the careful balance between equity and debt that a business uses to finance its assets, day-to-day operations, and future growth. o The capital structure influences everything from the firm’s risk profile, how easy it is to get funding, how expensive that funding is, the return its investors and lenders expect, and its degree of insulation from both microeconomic business decisions and macroeconomic downturns. 9 -7

Starbucks 2014

Ford Automotive

What is a (Bail) bond and how are they issued? Bond – formal debt instrument that obligates the borrower to repay a stated amount at a specified maturity date. Company (Borrower) – receives cash in exchange for issuing bond contract to investor Investor (Lender) – Lends company $ to receive periodic interest payments over time and a return of original principal at bond maturity.

FYI - Why Bonds versus Bank Borrowing? In the world of corporate finance, many chief financial officers (CFOs) view banks as lenders of last resort because of the restrictive debt covenants that banks place on direct corporate loans. Covenants - rules placed on debt that are designed to stabilize corporate performance and reduce the risk to which a bank is exposed. ¡ ¡ ¡ Cannot issue any more debt until loan is paid off Cannot participate in any share offerings until loan is paid off Cannot acquire any companies until loan is paid off, and so on. Debt to Equity cannot exceed 3 to 1. Current assets to current liabilities must exceed a ratio of 1. 5. Some of the more restrictive covenants may state that the interest rate on the debt increases substantially should the (CEO) quit, or should earnings per share drop in a given time period.

Bonds Definition - Formal debt instrument that obligates the borrower to repay a stated amount, referred to as the principal or face amount, at a specified maturity date. Important topics for our class today on bonds: 1. Bonds terms and characteristics 2. Bond Issuances (how we account for them) 1. 2. 3. 4. Pricing Interpretation - Pricing calculations will not be covered, but you will need to be able to interpret the price. Record bond issuance Record interest payments Record repayment of bonds

Item #1 - Bond Terms and Characteristics 13

Terms ¡ Bond certificate states: l l l 14 Company name (Borrower) Face Value (Principal amount) – Usually $1, 000 Maturity date (Term) Interest rate (stated or coupon rate) Interest payment dates (usually twice a year)

Bond listing in Financial Statement Notes ¡

Characteristics of Bonds Issued 1. 2. 3. Collateral? Principal and Interest Payments Additional Features 1. 2. Callable Convertible

Bond Characteristics o Collateral o o Secured Bonds - supported by specific assets the issuer (borrower) has pledged as collateral. Unsecured bonds - referred to as debentures, are not backed by a specific asset. 9 -18

Bond Characteristics o Principal and Interest 1. Serial bonds - require payments in instalments over a series of years. ¡ Interest typically paid annually or semi-annually 2. Term bonds - require payment of the full principal amount of the bond at a single maturity date. ¡ Interest typically paid annually or semi-annually Bond Issue Secured Serial Unsecured Term Serial Term 9 -19

Bond Characteristics – Cont. o Callable - Allows the borrower to repay the bonds before their scheduled maturity date at a specified call price. o Call price is stated in the bond o Convertible bonds - allow the lender to convert each bond into a specified number of shares of common stock. 9 -20

Summary of Bond Characteristics 9 -21

1. BOND ISSUANCE PRICING (Interpretation Only)

Bond Interest Rates ¡ Two separate interest rates set bond issuance price l Stated Rate – (rate on the face of the bond) ¡ The rate ‘stated’ in the bond contract ¡ The rate used to calculate the cash interest payments. ¡ Market Rate – (also known as the effective interest rate) ¡ True interest rate used by investors to value bond issue. ¡ What investors are seeking as a return.

Time Value of Money – (FYI) What is the BIG Idea? - Present value (PV) is the current worth of a future sum of money or stream of cash flows given a specified rate of return. 1. ) Value of $1, 000 in terms of todays money 2. ) Dollar invested earns income 24 http: //www. youtube. com/watch? v=7 QM-Vqkx. IEQ

Time Value of Money (Cont. ) Present value depends on: ¡ ¡ ¡ Amount of future payment (aka principal) Length of time Interest rate

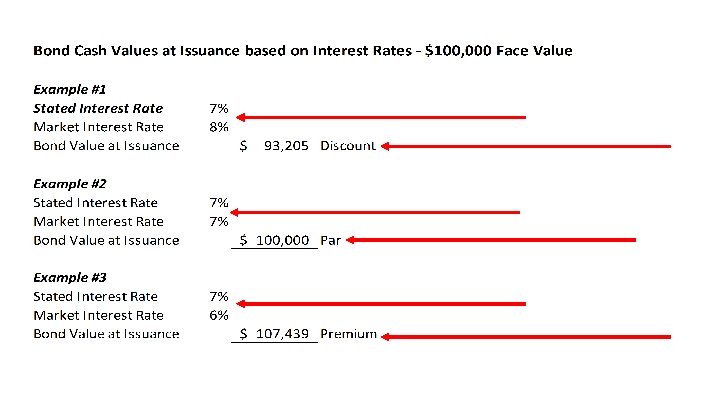

Cash Value of Bonds at Issuance Bond value at issuance is always based on Market Rate & Present Value. Based on the comparison of stated rate and market rate, the following three terms describe the issuance: 1. Par - stated interest rate equals the market interest rate. The bond is issued for face value of bonds. 2. Premium – stated interest rate exceeds the market interest rate. The bond is issued for more than the face value of bonds. 3. Discount – stated interest rate is below the market interest rate. The bond is issued for less than the face value of bonds.

¡ ¡ ¡ On January 1, 2012, 10 year bonds were issued at Par $100, 000 Face Value 7% stated interest rate 7% market interest rate Interest paid semi-annually (Face value * Annual interest rate * Time) $100, 000

However, stated rate almost always differs from market rate

In-Class Short Exercise 8 -7 30

Interpreting Bond Quotes In the financial press, bond prices are always quoted in relation to 100 to signify if they are sold at a premium, discount, or at par. The price quote is related to the face value, but is not the face value – it is really the % percentage of face value. Par = Premium = Discount = 31 Price Quote 100 (100% of face value) 105 (105% of face value) 95 (95% of face value)

Bond Pricing from Financial Mkt. (Cont. ) 32 Rate Maturity Bid Ask/yld 7¾ Feb. 2021 105. 12 5. 50 5 3/8 Feb. 2019 99. 26 5. 44

Total Value of Bond Issuance ($ received by issuing company)

34 Copyright © 2010 Pearson Education Inc. Publishing as Prentice Hall.

Check-ins 1. The most common bond characteristics are a serial or term bond that is secured or unsecured? (Circle the two correct answers in bold) 2. A bond issued at a discount will have a market rate that is higher or lower than the stated rate on the bond. (Circle the one correct answers in bold). 3. If a bond issuance with a face value of $1, 000 has an issue price of 98, how much cash will the organization receive at the time of issuance?

1. BOND ISSUANCE 2. INTEREST PAYMENTS 3. REPAYMENT

Bonds issued at Par - Steps Par - stated interest rate equals the market interest rate. The bond is issued for face value of bonds. Therefore, the amount of cash the organization receives from lenders (investors) will equal the face value of the bonds. Steps for original issuance: 1. Debit Cash for amount received 2. Credit Bonds Payable for amount of cash received. Steps for semi-annual interest payments: 1. Calculate ‘cash’ interest expense/payments using stated rate and our typical formula. 2. Debit Interest Expense 3. Credit Cash Steps for final repayment of bond at maturity to lenders (investors): 1. Debit Bonds Payable for face value of bond 2. Credit cash for amount of repayment.

Bond issued at Par - Example 10 year $100, 000 term bonds with stated rate of interest of 7% issued at par on 1/1/12. Interest is payable semiannually. Original transaction, 1 st interest payment, and maturity of bond in 10 years.

Issuance of a bond at a Discount/Premium Discount – stated interest rate is below the market interest rate. The bond is issued for less than the face value of bonds. Therefore, the amount of cash the organization receives from lenders (investors) will be less than the face value of the bonds. Steps for original issuance: 1. Debit Cash for amount received 2. Credit Bonds Payable for amount of cash received. Steps for semi-annual interest payments: 1. Use the ‘Effective Interest Rate Method” Steps for final repayment of bond at maturity to lenders (investors): 1. Debit Bonds Payable for face value of bond 2. Credit cash for amount of repayment.

Carrying Value The balance in the bonds payable account is the carrying value. ¡ We initially record the bonds payable account at $93, 205. The carrying value will increase from the amount originally borrowed ($93, 205) to the amount due at maturity ($100, 000) over the 10 -year life of the bonds using the effective interest rate method.

Effective Interest Method The effective interest method for bonds provides an ‘amortization’ of the discount (or premium) over the term of the bond so that the bond payable account equals face value at maturity. Very important – ‘CASH’ interest payments to investors are a different amount than the ‘INTEREST EXPENSE’ we record semi-annually. Steps: 1. Calculate ‘Cash Interest Payment’ (Credit to Cash account) Formula - Face Value * Stated Interest * Time Period 41 2. Calculate amount recorded as ‘Interest Expense’ (Debit the expense account) Formula - Carrying Value * Market Interest * Time Period 3. Difference between Interest Payment and Interest Expense is either Credited (discount) or Debited (premium) to Bonds Payable. 4. Calculate new carrying value after discount or premium is amortized.

Issuance - Recording Bonds Issued at a Discount o o In the preceding example we assumed the stated interest rate (7%) and the market interest rate (7%) were the same. If the market interest rate is 8%, the bonds will issue at only $93, 205. This is less than $100, 000. The bonds are paying only 7%, while investors can purchase bonds of similar risk paying 8%. The entry RC Enterprises makes to record the bond issue at a discount is: 9 -42

Effective Interest Method Step 1: Interest Payment – Credit Cash Interest payment (CASH) $3, 500 Face value $100, 000 Stated (coupon) interest rate 7% 1/2

Effective Interest Method Step 2: Interest Expense (Debit) Interest expense $3, 728 Carrying value $93, 205 Market (effective) interest rate 8% 1/2

Recording Bonds Issued at a Discount Step 1: Cash paid for interest is equal to the face amount times the stated rate (3. 5% semi-annually or 7% annually, in our example). Cash paid for Interest = Face amount of bond X Stated interest rate period $3, 500 = $100, 000 7% x ½ Step 2: We calculate interest expense as the carrying value (the amount actually owed during that period) times the market rate. Interest expense = Carrying value of bond X Market interest rate period $3, 728 = $93, 205 8% x ½ Step 3: On June 30, 2012, RC Enterprises the interest payment and expense. June 30, 2012 Debit Credit Interest Expense ($93, 205 x 8% x ½) 3, 728 Bonds Payable (difference) 228 Cash ($100, 000 x 7% x ½) 3, 500 (Record semiannual interest payment) 9 -45

Amortization Schedule for Bonds Issued at a Discount o o An amortization schedule provides a nice summary of the cash interest payments, interest expense, and changes in carrying value for each semiannual interest period. The amounts for the June 30, 2012 and the December 31, 2012 semiannual interest payment entries can be taken directly from the amortization schedule. (1) Date 1/1/2012 (2) Cash Paid for interest (3) Interest Expense (4) Increase in Carrying Value (5) Carrying Value Face Amount x Stated Rate Carrying Value x Market Rate (3) – (2) Prior Carrying Value + (4) $93, 205 6/30/2012 $3, 500 $3, 728 $228 93, 433 12/31/2012 3, 500 3, 737 237 93, 670 * * * * 99, 057 6/30/2021 3, 500 3, 962 462 99, 519 12/31/2021 3, 500 3, 981 481 $100, 000 9 -46

Recording Bonds Issued at a Premium o o o RC Enterprises issues $100, 000 of 7% bonds when other bonds of similar risk are paying only 6%. The bonds will issue at $107, 439. Investors will pay more than $100, 000 for these 7% bonds because bonds of similar risk are paying only 6% interest. The entry to record the bond issue at a premium is: January 1, 2012 Cash Debit Credit 107, 439 Bonds Payable 107, 439 (Bonds issued at a premium) On June 30, 2012, RC Enterprises records interest expense. June 30, 2012 Debit Credit Interest Expense ($107, 439 x 6% x ½) 3, 223 277 3, 500 Bonds Payable (difference) Cash ($100, 000 x 7% x ½) (Semi-annual interest payment) 9 -47

Amortization Schedule for Bonds Issued at a Premium o o An amortization schedule provides a nice summary of the cash interest payments, interest expense, and changes in carrying value for each semi-annual interest period. The amounts for the June 30, 2012 and the December 31, 2012 semi-annual interest payment entries can be taken directly from the amortization schedule. (1) Date 1/1/2012 (2) Cash Paid for interest (3) Interest Expense (4) Decrease in Carrying Value (5) Carrying Value Face Amount x Stated Rate Carrying Value x Market Rate (2) – (3) Prior Carrying Value + (4) $107, 439 6/30/2012 $3, 500 $3, 223 $277 107, 162 12/31/2012 3, 500 3, 215 285 106, 877 * * * 100, 956 6/30/2021 3, 500 3, 029 471 100, 485 12/31/2021 3, 500 3, 015 485 $100, 000 9 -48

Changes in Carrying Value Over Time 9 -49

Examples 1 -1 -12: $200, 000 of bonds issued with a stated interest rate of 9%. Interest due semi-annually. Due in 10 years 1. Market Rate = 9%. Record the bond issue on 1 -1 -12 and the first 2 interest payments on 6/30/12 and 12/31/12. Market Rate = 10%. Record the bond issue in the amount of $187, 538 on 1/1/12 and the first 2 interest payments on 6/30/12 and 12/31/12. 3. Market Rate = 8%. Record the bond issue in the amount of $213, 590 on 1/1/12 and the first 2 interest payments on 6/30/12 and 12/31/12. 9 -50

Example 1 – Bonds issued at ______

Example 2 – Bonds issued at ______

Bond Issued at Discount – Amortization Schedule Cash Increase Interest in Carrying Date 1/1/2012 6/30/2012 12/31/2012 6/30/2013 12/31/2013 6/30/2014 12/31/2014 6/30/2015 12/31/2015 6/30/2012 Paid 9, 000 9, 000 Expense 9, 377 9, 396 9, 416 9, 436 9, 458 9, 481 9, 505 9, 530 Interest Payment = 200, 000 x. 09 x 1/2 = 9, 000 Interest Expense = 187, 538 x. 10 x 1/2 = 9, 377 Value 377 396 416 436 458 481 505 530 Value 187, 538 187, 915 188, 311 188, 726 189, 163 189, 621 190, 102 190, 607 191, 137

Example 3 – Bonds issued at ______

Bond Issued at Premium – Amortization Schedule Cash Decrease Interest in Carrying Date Paid Expense Value 1/1/2012 213, 590 6/30/2012 9, 000 8, 544 (456) 213, 134 12/31/2012 9, 000 8, 525 (475) 212, 659 6/30/2013 9, 000 8, 506 (494) 212, 165 12/31/2013 9, 000 8, 487 (513) 211, 652 6/30/2014 9, 000 8, 466 (534) 211, 118 12/31/2014 9, 000 8, 445 (555) 210, 563 6/30/2015 9, 000 8, 423 (577) 209, 985 12/31/2015 9, 000 8, 399 (601) 209, 385 6/30/2012 Interest Payment = 200, 000 x. 09 x 1/2 = 9, 000 Interest Expense = 213, 590 x. 08 x 1/2 = 8, 544

Changes in Carrying Value Over Time $213, 590 $200, 000 $187, 538 9 -56

2. BOND ISSUANCE INTEREST PAYMENTS 3. REPAYMENT 1.

Payment of Bond Principal at Maturity Date 12/31/2021 Account Bonds Payable Cash Payment of Bond @ maturity Debit 200, 000 Credit 200, 000

Part D Other Long-Term Liabilities

Installment Notes Each installment payment includes both interest and principal: o Calculate the amount that represents interest expense. o o Calculate the amount that represents a reduction of the outstanding loan balance. o o Step 1 - Calculated as Carrying Value * annual interest rate * time (x/12) Step 2 - Subtract the monthly interest from the total payment and the remainder is a principal reduction. RC Enterprises obtains a $25, 000, 6%, four-year loan for a truck on January 1, 2012. Payments of $587. 13 (principal and interest) are required at the end of each month for 48 months. We record the note and the first two monthly payments as: 9 -60

Installment Notes Each installment payment includes both: o An amount that represents interest. o An amount that represents a reduction of the outstanding loan balance. o RC Enterprises obtains a $25, 000, 6%, four-year loan for a truck on January 1, 2012. o Payments of $587. 13 are required at the end of each month for 48 months. o We record the note and the first two monthly payments as: January 1, 2012 Cash Notes Payable (Issue a note payable) January 31, 2012 Interest Expense ($25, 000 x 6% x 1/12) Notes Payable (difference) Cash (monthly payment) (Record first monthly payment) February 28, 2012 Interest Expense ($24, 537. 87 x 6% x 1/12) Notes Payable (difference) Cash (monthly payment) (Record second monthly payment) Debit 25, 000 Credit 25, 000 125. 00 462. 13 587. 13 122. 69 464. 44 587. 13 9 -61

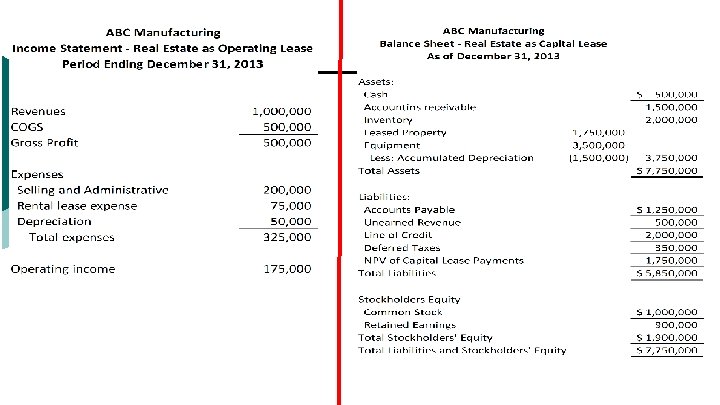

Leases o o A lease is a contractual agreement by which the lessor (owner) provides the lessee (user) the right to use an asset for a specific period of time. For accounting purposes, we have two basic types of leases: o Operating Leases: This type of a lease is similar to a rental. Example: Car rentals and short-term apartment leases. o Payments are expenses on income statement. Is not recorded on the balance sheet. o Capital Leases: Occurs when a lessee buys an asset and borrows the money through a lease to pay for the asset. Example: A borrower signs a four-year lease for a car that automatically transfers ownership at the end of the lease term. o Recorded on the balance sheet. 9 -62

J C Penney Operating Lease Obligations – Notes to the Financial Statements 163

Exercise 9 -8 Pretzelmania, Inc. , issues 8%, 10 -year bonds with a face amount of $90, 000 for $90, 000 on January 1, 2012. The market interest rate for bonds of similar risk and maturity is 8%. Interest is paid annually on December 31. Record initial transaction and first interest payment.

Exercise 9 -9 Pretzelmania, Inc. , issues 5%, 10 -year bonds with a face amount of $70, 000 for $55, 909 on January 1, 2012. The market interest rate for bonds of similar risk and maturity is 8%. Interest is paid annually on December 31. Show bond issue and first two interest payment based on amortization table. Record journal entries.

Exercise 9 -10 Pretzelmania, Inc. , issues 5%, 10 -year bonds with a face amount of $80, 000 for $101, 558 on January 1, 2012. The market interest rate for bonds of similar risk and maturity is 2%. Interest is paid annually on December 31. Show bond issue and first two interest payment based on amortization table. Record journal entries.

Operating Lease versus Capital Lease Chunky Cheese Pizza has $60 million in bonds payable. The bond indenture states that the debt to equity ratio cannot exceed 4. Chunky’s total assets are $350 million, and its liabilities other than the bonds payable are $220 million. The company is considering some additional financing through leasing. What does the stockholders’ equity total? Debt to equity? The company enters a lease agreement requiring lease payments with a present value of $6 million. Will this lease agreement affect the debt to equity ratio differently if the lease is recorded as an operating lease versus a capital lease? Yes. The debt to equity ratio will not be affected under an operating lease. However, under a capital lease, assets and liabilities will both increase $6 million while stockholders’ equity will remain unchanged. The increase in liabilities will increase the debt to equity ratio.

Long-term Notes Payable On December 1, 2012, Stoops Entertainment purchases a building for $450, 000, paying $100, 000 down and borrowing the remaining $350, 000, signing a 9%, 15 -year mortgage. How much interest is accrued at the end of the month for the preparation of the financial statements.

Participation Questions – Chapter 9 ¡ ¡ ¡ The capital structure of an organization is the mixture of debt funding and equity funding. T/F Ford Automotive uses a higher level of equity funding in comparison to debt funding. T/F “Coupon Rate” is the same as which of the following on a bond: l Market interest rate l Stated interest rate l The Dow Jones interest rate l LIBOR interest rate How much did the Hersey bar cost from the 1950’s as shown in the Seinfeld episode? The cash amount of interest paid to a bond holder is based on which of the following? l Face Value l Carrying Value