Chapter 3 Audit Reports What are the parts

. Also called")

Auditor Has Knowledge (Limitation of Scope) Auditor Lacks Knowledge")

- Slides: 51

Chapter 3 Audit Reports

What are the parts of the standard unqualified audit report ? 1. Report title 2. Audit report address 3. Introductory paragraph 4. Scope paragraph 5. Opinion paragraph 6. Name of CPA firm 7. Audit report date

1. Report title The report should be titled. Include the word independent. Examples : independent auditor’s report. What is the need for such title ? ? to convey to users that the audit was unbiased.

2. Audit report address The report is usually addressed to the company, its stockholders or the board of directors. It has become customary to address the report to the Board OF Directors.

3. Introductory paragraph The first paragraph does three things : 1. Makes simple statement that the CPA firm has done the Audit. 2. Lists the financial statements that where audited. (including balance sheet dates and accounting periods for income statement and cash flow statement). 3. States that the statements are the responsibility of management and Auditor’s responsibility is to express an opinion on the statements.

4. Scope paragraph What the auditor did in the audit. States the chosen criteria. Auditing standards used. States that the Audit is designed to obtain Reasonable Assurance that the statements are free of material misstatements. Test Basis.

5. Opinion paragraph Auditor’s conclusions based on the results of the Audit. Stated as an opinion rather than as a statement of absolute fact or guarantee. Bases on professional judgment. Opinion on the financial statements taken as a whole.

6. Name of CPA firm Identifies the CPA firm who performed the Audit.

7. Audit report date The appropriate date is the on which the auditor completed the auditing procedures in the filed.

Conditions required to issue the standard unqualified audit report 1. All financial statements are included. 2. The three general standards have been followed in all respects on the engagement. 3. Sufficient evidence has been accumulated to conclude that the three standards of field work have been met. 4. The financial statements are presented in accordance with generally accepted accounting principles. 5. There are no circumstances requiring the addition of an explanatory paragraph or modification of the wording of the report

Four Categories of Audit Reports 1. Standard unqualified. 2. Unqualified with explanatory paragraph or modified wording. 3. Qualified 4. Adverse or disclaimer

Standard unqualified • The five conditions. Unqualified with Explanatory paragraph or Modified wording • Complete audit took place with satisfactory results and financial statements are fairly presented. • The auditor believes it is important or required to provide additional information. Qualified • The overall financial statements are fairly presented but : • The scope of the audit has been materially restricted. • Or GAAP were not followed • Adverse or Disclaimer • The financial statements are not fairly presented(adverse). The auditor is unable to form an opinion to whether the financial statements are fairly presented or not (Disclaimer)

Report on internal control over Financial reporting Sarbanes-Oxley Act: This Act requires the auditor of a public company to attest to management’s report on the effectiveness of internal control over financial reporting. The Auditor may choose to issue : 1. Separate reports. (separate report on internal control over financial reporting ). 2. Combined report on financial statements and internal control over financial reporting.

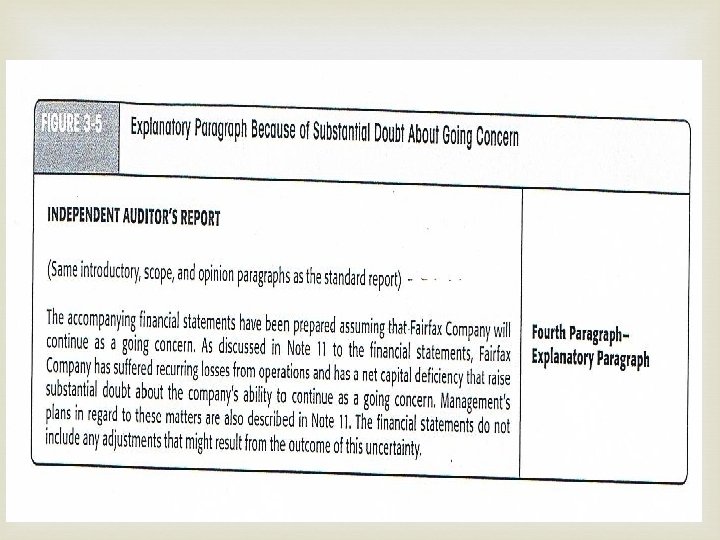

Unqualified with Explanatory paragraph or Modified wording Describe the five circumstances when an unqualified report with an explanatory paragraph or modified wording is appropriate. 1. Lack of consistent application of generally accepted accounting principles 2. Substantial doubt about going concern 3. Auditor agrees with a departure from promulgated accounting principles 4. Emphasis of a matter 5. Reports involving other auditors

The first four reports all require an explanatory paragraph, following the opinion paragraph. Only reports involving other auditors use a modified wording report. (this report contains three paragraphs and all three paragraphs are modified).

1. Lack of consistent application of generally accepted accounting principles Accounting principles change is observed in the current period compared the previous period. When a material change occurs the auditor modifies the report by adding explanatory paragraph. The materiality of a change is evaluated based on the current year effect of the change. Those changes could affect 1 - Consistency 2 - Comparability.

Changes that affect consistency and require an explanatory paragraph Change in accounting principles (FIFO to LIFO ) consistency Changes in reporting entities(inclusion of an additional company in combined financial statements) Corrections of errors involving principles.

Changes that affect consistency and require an disclosure in footnotes. Changes in an estimate. Error correction not involving principles(mathematical error in previous year) comparability Variations in format and presentation of financial statements. Changes because of substantially different transactions or events (sale of a subsidiary)

Substantial Doubt About Going Concern 1. Significant recurring operating losses or working capital deficiencies. 2. Inability of the company to pay its obligations as they come due. 3. Loss of major customers, the occurrence of uninsured catastrophes. 4. Legal proceedings, legislation that might jeopardize the entity’s ability to operate.

Auditor Agrees with a Departure from a Promulgated Principle The auditor must be satisfied and must state and explain, in a separate paragraph or paragraphs in the audit report, that adhering to the principle would have produced a misleading result in that situation.

Emphasis of a Matter Under certain circumstances, the CPA may want to emphasize specific matters regarding the financial statements, even though the CPA intends to express an unqualified opinion. A. The existence of significant related party transactions. B. Important events occurring subsequent to the balance sheet date. C. A description of accounting matters affecting the comparability of the financial statements with those of previous years. D. Material uncertainties disclosed in the footnotes.

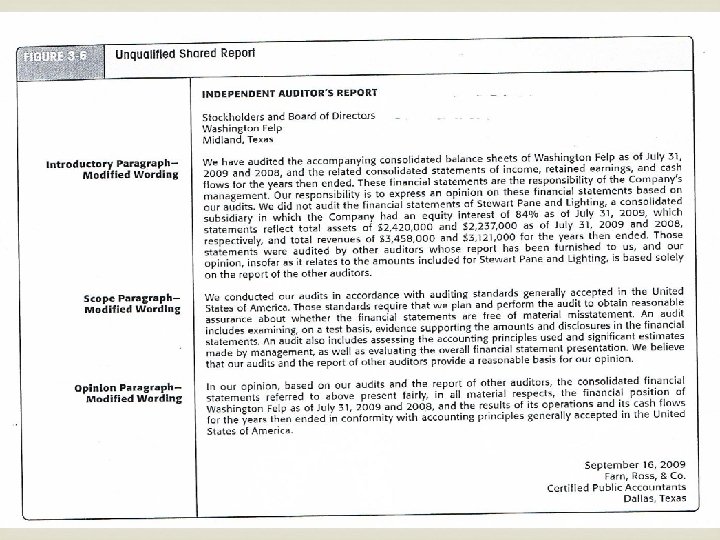

Reports Involving Other Auditors 1. Make no reference in the audit report A. The auditor audited an immaterial portion of the statements. B. The other auditor is well known or closely supervised by the principal auditor. C. The principal auditor has thoroughly reviewed the other auditor’s work.

Reports Involving Other Auditors 2. Make reference in the report(modified wording report). Also called shared opinion. A. When it is impractical to review the work of the other auditor. B. The portion of financial statements audited by the other CPA is material. Introductory paragraph discusses the shared responsibility. And the other auditor is referred to in the scope and opinion paragraphs.

Reports Involving Other Auditors 3. Qualify the opinion Qualified or disclaimer (depending on materiality ) if the auditor is not willing to assume any responsibility for the work of the other auditor.

Causes of Modified Wording or Explanatory Paragraph Consistency Exception Substantial Doubt About Going Concern Auditor Agrees with a Departure from GAAP Emphasis of a Matter Reports Involving Other Auditors Example Change from LIFO to FIFO inventory Significant recurring losses Type of Report Unqualified with explanatory paragraph Federal legislation requires the use of a new method of accounting for the automotive industry A merger with a large Unqualified with explanatory company occurred after the paragraph balance sheet date A chartered accounting firm Unqualified with modified audited a sub sidiary operating wording in Canada

Departures from An Unqualified Opinion 1. Scope limitation: The auditor has not accumulated sufficient appropriate evidence. Restrictions could be caused by the client or caused by circumstances. 2. GAAP departure Using replacement cost for assets rather than historical cost. 3. Auditor is not independent

Materiality Level (GAAP Departure) Auditor Has Knowledge (Limitation of Scope) Auditor Lacks Knowledge Immaterial Material Unqualified Qualified (opinion only) Qualified (scope and opinion) Highly Material Adverse Disclaimer

Qualified Opinion A qualified opinion report can result from a limitation on the scope of the audit or failure to follow generally accepted accounting principles. Can be used only when the auditor concludes that the overall financial statements are fairly stated. The term “except for “ must be used in the opinion paragraph. Types : Qualification of both the scope and opinion OR the opinion alone.

1. Qualification of both the scope and opinion: The auditor has been unable to accumulate all of the evidence required GAAS. Used when the scope has been restricted. 2. Qualification of the opinion alone. Financial statements are not stated in accordance with GAAP.

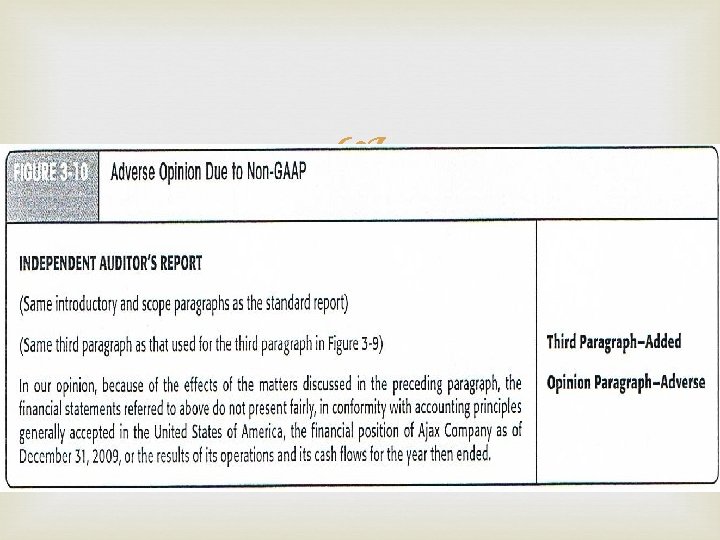

Adverse Opinion It is used only when the auditor believes that the overall financial statements are so materially misstated or misleading that they do not present fairly the financial position or results of operations and cash flows in conformity with GAAP. Rarely used.

Disclaimer of Opinion It is issued when the auditor is unable to be satisfied that the overall financial statements are fairly presented. Caused by : 1. severe limitations on the scope of the audit. 2. Nonindependent relationship.

Materiality A misstatement in the financial statements can be considered material if knowledge of the misstatement would affect a decision of a reasonable user of the statements.

1 -Amounts are immaterial. Is unlikely to affect the decision of a reasonable user. Unqualified. 2 -Amounts are material but do not overshadow the financial statements as a whole. The misstatement in the financial statement would affect users decision, BUT the overall statements are fairly stated. Qualified opinion ‘except for’.

3 -Amounts are so material or so pervasive that overall fairness of the statements is in question. Users are likely to make incorrect decisions if they rely on the overall financial statements. Adverse or disclaimer.

Materiality Level Significance in Terms of Reasonable Users’ Decisions Type of Opinion Immaterial Users’ decisions are unlikely Unqualified to be affected. Material Users’ decisions are likely to be affected. Qualified Highly material Users’ decisions are likely to be significantly affected. Disclaimer or adverse

Materiality Decisions Failure to follow GAAP Report type Unqualified Qualified Opinion only Adverse

Materiality Decisions 1. Dollar amount compared with a base. Common bases : net income/total assets/ current assets/working capital. 2. Measurability. Acquisition of a new company after balance sheet date. 3. Nature of the item. Illegal or fraudulent transactions.

Scope limitation Report type Unqualified Qualified scope and opinion Disclaimer

Conditions Scope Restricted: By Client Scope Restricted: By Conditions Failure to Follow GAAP Example Client refuses to allow CPA to examine minutes Engagement begins after year end Client uses replacement cost for inventory Types of Opinions • Unqualified • Qualified (scope and opinion) • Disclaimer • Unqualified • Qualified (opinion only) • Adverse Auditor Lacks Independence Ownership of stock in client • Disclaimer by partner

Auditor’s scope has Been Restricted The auditor may issue : Unqualified report, Qualification of both scope and opinion or a disclaimer of opinion, depending on materiality. If the auditor can be satisfied with alternative procedures that the information being verified is fairly stated, an unqualified report is appropriate. If those procedures cannot be performed ? ? ?

Qualified Scope and Opinion Due to Scope Restriction

Qualifying paragraph preceding the opinion to describe the restriction.

Disclaimer of Opinion Due to Scope Restriction

“We were engaged” in the introductory paragraph. Second paragraph added. Scope paragraph is deleted. The opinion paragraph is changed to disclaimer.

Statements Are Not in Conformity with GAAP The auditor knows that the statements may be misleading because they were not prepared in conformity with GAAP. The client is unable or unwilling to correct the misstatement. Qualified or adverse opinion depending on materiality.

Qualified Due to Non-GAAP

Disclaimer

Lack of statement of cash flow The client is unwilling to include the statement of cash flow. A third paragraph stating the omission and an “except for” opinion qualification.