The Sicilian Expedition Ancient Philosophy The Sicilian Expedition

- Slides: 55

The Sicilian Expedition Ancient Philosophy

The Sicilian Expedition • 18. 26 With this Nicias concluded, thinking that he should either disgust the Athenians by the magnitude of the undertaking, or, if obliged to sail on the expedition, would thus do so in the safest way possible.

The Sicilian Expedition • The Athenians, however, far from having their taste for the voyage taken away by the burdensomeness of the preparations, became more eager for it than ever; and just the contrary took place of what Nicias had thought, as it was held that he had given good advice, and that the expedition would be the safest in the world.

The Sicilian Expedition • All alike fell in love with the enterprise. The older men thought that they would either subdue the places against which they were to sail, or at all events, with so large a force, meet with no disaster; those in the prime of life felt a longing foreign sights and spectacles, and had no doubt that they should come safe home again; while the idea of the common people and the soldiery was to earn wages at the moment, and make conquests that would supply a neverending fund of pay for the future.

Sicilian Expedition • With this enthusiasm of the majority, the few that liked it not, feared to appear unpatriotic by holding up their hands against it, and so kept quiet.

The Icarus Paradox • The 'Icarus Paradox' was coined by Danny Miller who observed that great success often precedes severe decline. • The Greek word for this was hubris, or pride.

The Icarus Paradox • Icarus attached wings made of wax and feathers to his shoulders and flew up into the sky. He flew higher and higher, until he came close to the sun, which melted the wax and Icarus fell to his death in the Aegean sea. What made him soar was the very reason for his decline.

The Icarus Paradox • The same happens to organizations. Successful organizations tend to give more funding, support and status to the people they perceive as the basis of their success (for instance, a technology department).

The Icarus Paradox • People with other ideas, from other departments, lose funding and status and decrease in number, making the organization more homogenous, 'simple', and inert.

The Icarus Paradox • The organization loses its sense of urgency and becomes blind to opportunities and threats from a changing environment.

The Icarus Paradox • Eventually, performance declines, at which time the alerted organization begins watching the environment again only to find out that it is too late and dramatic restructuring is needed to get back on track.

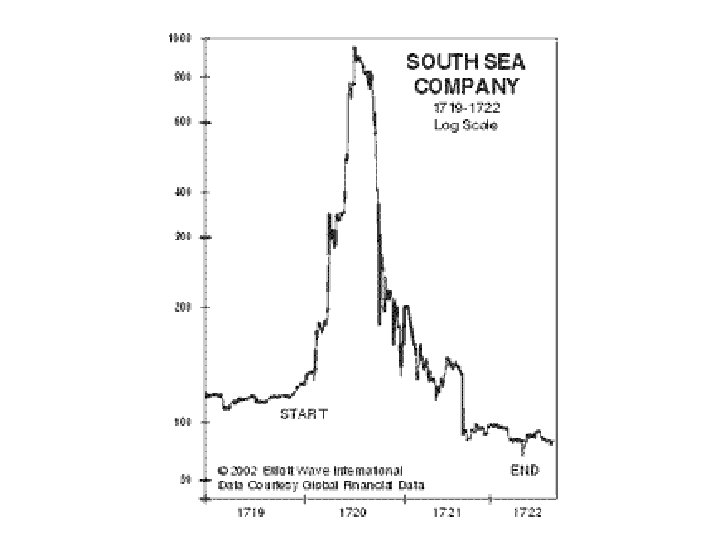

Secular bear market underway The history of stock markets is one of long bull markets and long bear markets. We believe that U. S. stocks are in a secular bear market - one that could last years, rather than months.

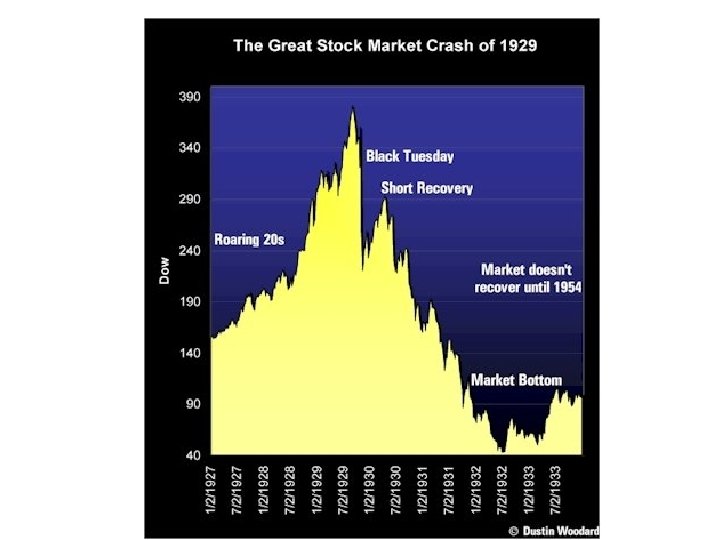

Bull and bear market cycles Here’s a quick overview of the last 100 years: • 1909 - 1921: Stocks entered the 1900 s trending higher, and rose 35% in less than three years. But stocks swung wildly, peaking in 1909. By August 1921, the broad market was 40% lower. • 1921 -1929: In the famous bull market of the Roaring ‘ 20 s, stocks returned more than 400%. • 1929 - 1948: Stocks plunged, recovered significantly by 1937, but by 1948, stocks were down more than 50% from the ’ 29 peak.

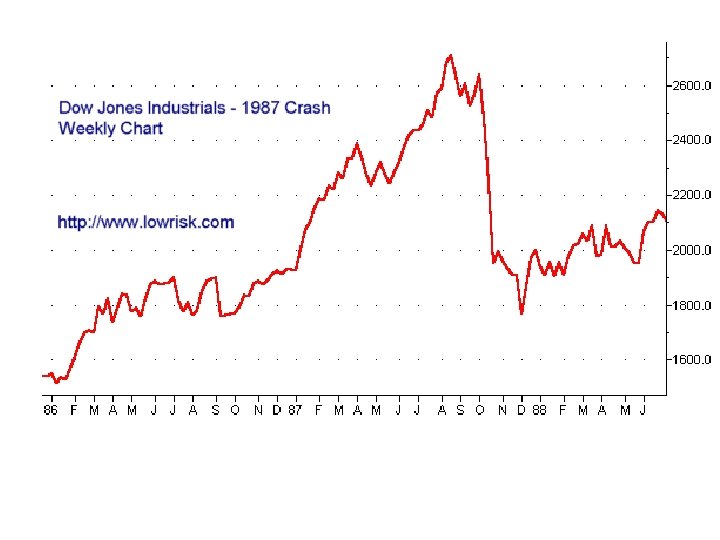

Bull and bear market cycles… • 1948 - 1973: Stocks prices produced a six-fold increase, culminating in the Nifty-Fifty market of 1972. • 1973 - 1982: The S&P 500 was lower in August 1982 than in January 1973. Adjusted for inflation, the results were far worse. • 1982 - 1999: The S&P 500 index rose by a factor of 12. The NASDAQ ended the 90 s at 21 times its 1982 level.

Most stock returns come from secular bull markets Annual price change for 1900 - 1999 5. 6% Long term compound annual 13. 8% price change from Secular Bull periods only (last century) Excludes: 190020, 1929 -48, 1966 -81 Compound annual price change, no Secular Bulls 1. 1% (Simple ave. +2. 1%) Excludes: 192128, 1949 -66, 1982 -99 Based on S&P Composite 1900 -1999, dividends not

Periods following secular bull markets can produce dismal returns 1929: 1966: The next decade saw the 2 most severe bear markets* in the first half of this century: 1929 peak – 1932 trough: -86% The next decade saw the most severe bear markets* in the last half of this century: 1969 -70: -34% 1937 peak – 1938 trough: -54% 1973 -74: -47% (Between December 1968 and December 1974, the ’ 29 peak to ’ 38 trough: -73% unweighted Value Line Index of 1700 stocks lost *Based on S&P Composite, dividends excluded more than 74%)

Secular Bear Markets can devastate investors $1, 000 Year Initial # of Invested at Investment Years to Peak of Recovered Recover 1929 1966 1953 1993 24 27 Inflation adjusted recovery period, excluding dividends

We can conclude: Secular Bear Markets usually parallel the Secular Bull markets that precede them

Bear follows bull - another view:

Credit excesses fuel speculative asset bubbles. In fact, all great speculative manias have been associated with rapid credit growth. The greater the credit excesses the wilder the speculation.

The following table from “Crunch Time for Credit? An inquiry into the state of the credit system in the United States and Great Britain” by Edward Chancellor highlights the source of credit fueling famous speculative manias. Date Mania Source of Credit

Date Mania Source of Credit Source: Crunch Time for Credit? An inquiry into the state of the credit system in the United States and Great Britain

According to financial historian Edward Chancellor, there are several indicators that a credit boom is underway and placing an economy at risk: Rapid credit growth Speculative buying (inflows) by foreigners Investment and/or consumption boom Decline in credit quality Financial liberalization Influx of new credit providers and increasing competition among them Zeal for lending against assets (rather than income) Concentration of risk Tendency by lenders/investors to underestimate risk Was the late ’ 90 s stock market a credit-fueled ma

The ‘ 90 s stock market certainly resembled other stock manias of the 20 th century

Here’s another sign of a mania. . . 105% more equity funds in 5 years! Source: Investment Company Institute

Sound familiar? In his book, “A Short History of Financial Euphoria, ” Economist John Kenneth Galbraith outlines common features of a market mania. See if any of these sound familiar: Brevity of financial memory, disaster is quickly forgotten (S&L debacle, junk bonds, Japanese bubble, Mexico collapse, Orange County, Asian collapse, LTCM) Association of money with intelligence (Derision of those who question New Era market, elevation in status of CEOs, financial commentators, money managers) Arrival, development of something new (Internet, telecom and myth of increased productivity) Claims of financial innovation (Increased use of derivatives,

Credit fueled our recent mania

The credit surge, another view

And another view

Credit fueled our recent mania Credit flooded the corporate sector in the late ’ 90 s, supplying financing to too many marginal companies and credit excess capacity, particularly in telecom. When credit growth slowed in these sectors, the Federal Reserve tried to buoy the economy by easing monetary and credit conditions further. The result was a middling economy and a bubble in the home mortgage sector. For the first time in memory, rather than retrenching, consumers took on more debt during the recession.

Telecom helped business borrowings explode in the late ’ 90 s

When business borrowing collapsed, the mortgage sector more than made up for it

Cash-out refis were key to the surprising strength in consumer spending

When the refi boom faded…

… home equity lending surged

…enabling the mortgage finance bubble to keep going

The physical evidence of the bubble is obvious Bubble!

For another view of the mortgage bubble, consider the dollars involved

Meanwhile, the mortgage bubble squeezes consumer income

And balance sheets bear the burden of excess

Despite credit-induced ‘wealth creation’ consumers are more leveraged to housing than ever

From the previous pages it’s clear that the credit bubble is ongoing. The Fed’s aggressive posture simply shifted the stock bubble to new sectors. Asset price inflation, which is dependent on credit, continued and has crept back into the stock market as well. What happens when the credit bubble bursts?

What will drive the economy once the desire to save returns?

Greenspan once had it right about how credit booms can distort an economy: “The excess credit which the Fed pumped into the economy spilled over into the stock market triggering a fantastic speculative boom. Belatedly, Federal Reserve officials attempted to sop up the excess reserves and finally succeeded in braking the boom. But it was too late: by 1929 the speculative imbalances had become so overwhelming that the attempt precipitated a sharp retrenching and a constant demoralizing of business confidence. ” Alan Greenspan, Gold and Economic Freedom, 1966

Have we had our bear market? Valuations never reached “bear market” levels The following charts reveal that stocks remain expensive by a number of measures.

Dividend yields unattractive

Stocks look pricey relative to gold

S&P Industrials price to book value We are here! This chart combines price-to-book with dividend yield Source: Elliott Wave International Bond yield/stock yield

Even over long periods, high PEs result in sub-par returns Poorest return decile burdened by periods with high starting P-Es S&P 500 PE = 20 as of Mar. 2005 Source: Crestmont Research

Still no capitulation that typically follows a Super Bull Net Cash Flows into U. S. domestic equity mutual funds: 1995 – 2001: 2002: 2003: 2004: +$1, 256 billion -$28 billion +$152 billion +$177 billion Source: Investment Company Institute

History has taught us: Long bear markets are a natural outgrowth of long bull markets Stocks remain expensive. Even if earnings grow at historic rates, stocks could provide poor returns over the next 5 -10 years. Credit is the driver of speculative manias. Historically, once credit becomes less available, asset prices suffer.

The Bubble Trouble Remains “Since early 2000, the US has gone through a mild recession and the most anemic recovery on record. Over that same period, America’s net national saving rate has plunged to a record low, the household sector debt ratio has risen to an alltime high, and the US current account has gone deeper into deficit than ever. All this smacks of a US economy that is living far beyond its means, as those means are delineated by domestic income generation. Far from purging the excesses of the late 1990 s, the United States has upped the ante on structural imbalances as never before. ” Stephen Roach, Morgan Stanley 9/2/03