FIXED ASSETS AO OCT 2008 INSTRUCTOR CLASS SCHEDULE

l Subsystem Documents l FMS Tables")

")

")

l Supports the accounting & management of real and personal")

l Contains Capitalized Real and Personal Property. l Real Property")

l Allows asset depreciation to be computed manually or automatically")

l See the Fixed Asset Manual pages 2 -4 through")

l")

l Fixed Asset")

l Daily Report of items")

(F 876) (SGL 1720) • Transfer")

(F 762) (SGL 1832) • Transfer")

OA&MM")

Document to change the")

document for excess equipment. 4.")

.")

7 -12")

by FY, BFY, and FUND")

= General Ledger Trial Balance")

, AEMS/MERS, FAP")

•")

and")

RGLLIAV Form F 832.")

- Slides: 104

FIXED ASSETS A/O OCT 2008

INSTRUCTOR: CLASS SCHEDULE: Class begins at 8: 30 am Class ends at 4: 00 p. m.

OBJECTIVE: The objective of this course is to provide an overview of the Financial Management System (FMS) Fixed Asset Subsystem (FAP) including policy, reports and general ledger issues. Instructor illustrates fixed asset transactions and associated FMS table updates.

After completion of this course the student will be able to: l l l l l Describe Fixed Asset policy to include capitalization of assets Identify the Fixed Asset Subsystem (FAP) Identify Subsystem Documents Review FMS tables for research Describe Subsystem transactions and their effect on the general ledger Describe what to do with excess equipment Review RSD reports available for research Reconcile the Fixed Asset Subsystem to the Standard General Ledger Federal Entity Transfers and Station Integration

FIXED ASSETS OVERVIEW l Policy l Subsystem (FAP) l Subsystem Documents l FMS Tables

FIXED ASSETS OVERVIEW l General Ledger Transactions l Excess Equipment l RSD Reports l Reconciliation

WEB SITES l http: //www. va. gov/publ/direc/finance. htm VA Directives, Handbooks, Bulletins l http: //www. fsc. va. gov/fsc. index. htm FSC homepage l http: //vaww 1. fsc. va. gov/fmshome Under FMS User Guide, FMS guides can be accessed l http: //vaww. fscdirect. fsc. va. gov FMS GL and Proforma and Training l http: //vaww. fscdirect. fsc. va. gov/newsflash News Flash location l http: //vaww. frs. austin. aac. va. gov/logon. asp FRS l http: //vaww. aac. va. gov/ssw Snap. Web Access l http: //vaww. snapwebfms. aac. va. gov/ FMS Snap. Shot. Web l http: //vaww. austin. aac. va. gov/ EOS API for RSD reports

FIXED ASSETS PROPERTY, PLANT & EQUIPMENT POLICY 1 -1

Property, Plant and Equipment Policy l What is a Fixed Asset? –Property, Plant, and Equipment are called Fixed Assets.

l Property, Plant and Equipment Policy Real Property • 1711 • 1712 • 1730 • 1740 • 1812 • 1820 Land Improvements to Land Buildings Other Structures Buildings under Capital Leasehold Improvements

l Property, Plant and Equipment Policy Personal Property • 1750 Non-Expendable Equipment • 1751 ADP Non-Expendable Equipment • 1811 Equipment under Capital Lease • 1830 Information Technology Software • 1832 Software Development

Property, Plant and Equipment Policy l Capital Leases – Transfer of ownership by end of lease term – Bargain purchase option – Lease term is equal to or greater than 75% of economic life of the property – Present value or rental is equal to or greater than 90% of the fair value of the property l Operating Leases – Leases that do not satisfy one of the above criteria. These are expensed.

Property, Plant and Equipment Policy General Definitions l Capitalize: To set up expenditures as business assets in the books of account instead of treating as an expense l Expense: Outflows or the using up of assets as a result of the major or central operations of a business; also, the incurrence of liabilities may result as an alternative to outflows of assets.

Property, Plant and Equipment Policy Expense Policy l Real Property/Personal Property – cost is less than $100, 000 – useful life is less than 2 years – costs that do not satisfy the Department’s capitalization criteria l Exception – Projects that restore damaged properties to original state will be expensed – Asbestos removal costs will always be expensed

Property, Plant and Equipment Policy Capitalization l Real Property/Personal Property – – – cost is greater than $100, 000 for all obligations using BOC Series 32(Real Property) for all obligations using BOC Series 31(Personal Property) useful life is greater than 2 years Accountability for assets remains at $5, 000 l Exception: Land will be capitalized regardless of cost

Property, Plant and Equipment Policy Contact In Outlook VHA Accounting Policy (173 A)

Property, Plant and Equipment Policy l See the Fixed Asset Manual pages 1 -6 through 1 -15

Estimated Useful Lives of Land Improvements, Buildings, and Fixed Equipment Item Year 1. Architectural Automatic Door 10 ICU-CC counters 15 Interior finish 15 20 Lockers, built-in 20 Cabinet, biological safety 15 Mailboxes built-in 20 Canopies 15 Millwork 20 Carpentry work 20 Nurses’ counter 20 Ceiling finishes 12 Overhead door 10 Ceramic tile 20 Painting, new construction 10 Cubicle track 20 Partitions, interior 20 Designation signs 10 Pass-through boxes 20 Drapery track 10 Patient’s wardrobes and Drilled piers 40 Floor finishes 10 Sink and drain board 20 Folding partitions 10 Storefront construction 20 Hood, fume 18 Toilet partitions 20 Bench, bin, cabinet Counter, shelving built-in Vanities 20

Estimated Useful Lives of Land Improvements, Buildings, and Fixed Equipment Item Year 2. Electrical Clock System, central 15 Passenger, other 20 Conveying system 15 Emergency light system 15 Doctors in/out register 20 Escalator 20 Fire alarm system 20 Electric lighting and power Conduit and wiring 20 Door closing devices 15 Feed wiring 20 Generator set 20 Fixtures 10 Intercom system 15 Switch gear 20 Magnetic door holders 10 Transformer 20 Nurse call system 15 Paging system 15 Elevator Dumbwaiter 20 Telephone system 10 Freight 20 Television antenna system 10 Yard lighting 15 Passenger, high-speed automatic 20

Estimated Useful Lives of Land Improvements, Buildings, and Fixed Equipment Item Year 3. Heating and Air Conditioning Boiler smokestack, metal 15 Cooling tower, Clean air equipment 15 metal/wood 15 Duck work 20 large over 20 tons 15 Fan, air handling & vent 15 medium 5 -15 tons 10 Furnace, domestic type 15 small, under 5 tons 05 Heating, ventilating & air conditioning system 20 Heat & air conditioning system, all equipment & units Incinerator, indoor 10 Oil storage tank 20 Boiler 20 Piping 25 Compressor, air 15 Precipitator 15 Condense tank 10 Pump 15 Condenser 15 Radiator, cast iron 18 Controls 15 Radiator, finned tube 18 Cooler/humidifier 10 Solar heat equipment 10 Unit heater 10

Estimated Useful Lives of Land Improvements, Buildings, and Fixed Equipment Item Year 4. Plumbing Fire protection in hoods 10 Smoke & heat detectors 15 Laboratory plumbing, piping 20 Sprinkler system 25 Oxygen, gas, air, piping 20 Tank and tower 25 Oxygen storage tanks 20 Sterilize, built-in 20 Plumbing-fixture 20 Sump pump & sewage Plumbing-piping 25 Piping 20 Plumbing-pump 15 Ejector 10 Pneumatic tube system 15 Vacuum cleaning system 15 Sewerage, composite 25 Water heater, commercial 15 Water storage tank 20 Water wells 25 Sprinkler & fire: Fire pump 20 Protection system 25

Estimated Useful Lives of Land Improvements, Buildings, and Fixed Equipment Item Year 5. Site work Bumpers 05 Paving (including roadways, Culverts 18 walks and parking) Fencing-brick or stone 25 Asphalt 12 Fencing-chain link 15 Concrete 15 Fencing-wire 05 Gravel 05 Fencing-wood 08 Retaining wall 20 Flagpole 20 Shrubs, lawns, trees 10 Heated pavement 15 Sign 12 Lawn sprinkler system 15 Snow melting system 10 Parking lot gate 05 Turf, artificial 05 Parking lot, open walls 20 Underground sewer and water lines 25

Estimated Useful Lives of Land Improvements, Buildings, and Fixed Equipment Item Year 6. Structural Bridges 30 Computer flooring 15 Roof covering 10 Loading docks 15 Sewage treatment plant 20 Structure, masonry or wood 25 Water treatment plant 30 Masonry Reinforced concrete frame 40 Steel frame, fireproofed 40 Steel frame not fireproofed 30 Reinforced concrete, commercial design This list is not all-inclusive and the estimated useful life for items, which are not specifically listed, should be determined with assistance from Engineering Service. 40

FIXED ASSETS SUBSYSTEM (FAP)

FIXED ASSETS SUBSYSTEM (FAP) l Supports the accounting & management of real and personal property items. l Maintains original & subsequent value of assets and works with other FMS Subsystems to support fiscal & risk management as well as standard reporting.

FIXED ASSETS SUBSYSTEM (FAP) l Contains Capitalized Real and Personal Property. l Real Property entered directly by Fiscal. l Capitalized Personal Property entered via the AEMS/MERS Fixed Assets Interface.

FIXED ASSETS SUBSYSTEM (FAP) l Allows asset depreciation to be computed manually or automatically via an off-line program. l VA uses the straight line method. l Passes accumulated depreciation monthly to the FMS general ledger.

FIXED ASSETS SUBSYSTEM (FAP) l See the Fixed Asset Manual pages 2 -4 through 2 -6

FIXED ASSETS SUBSYSTEM TABLES

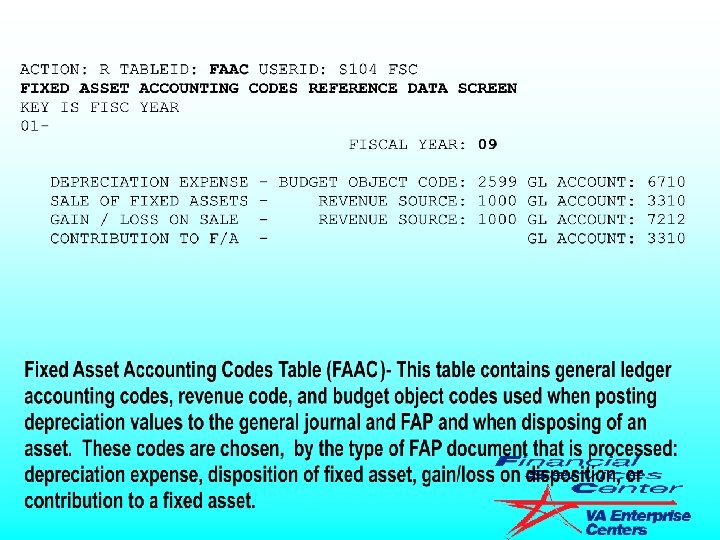

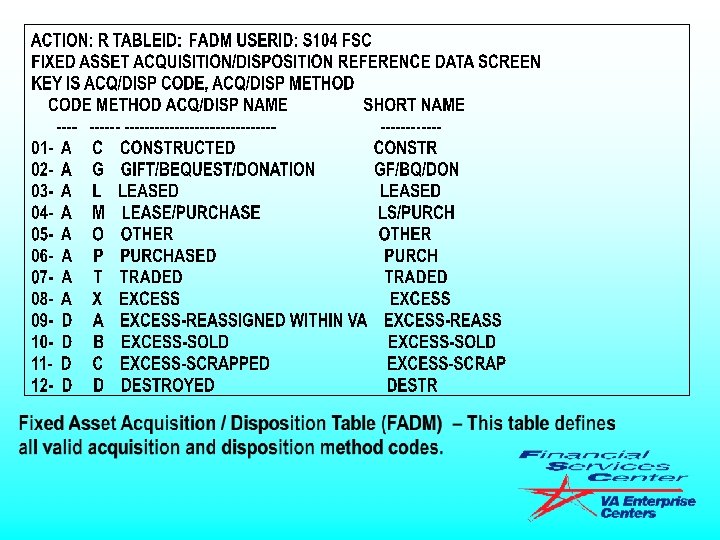

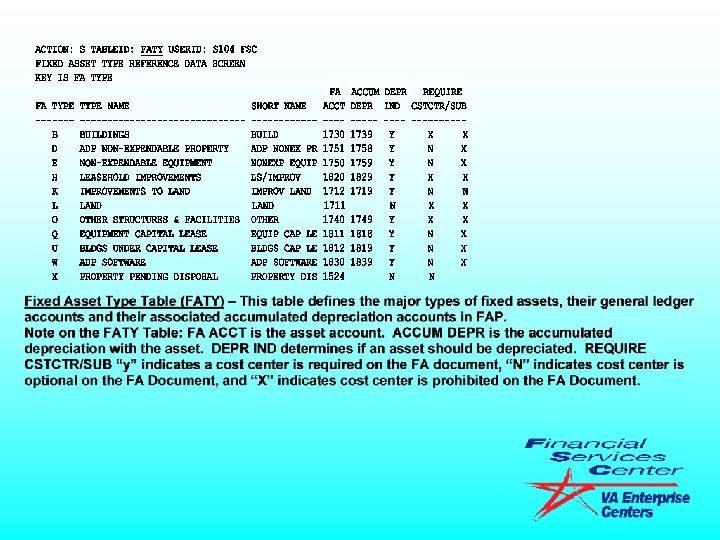

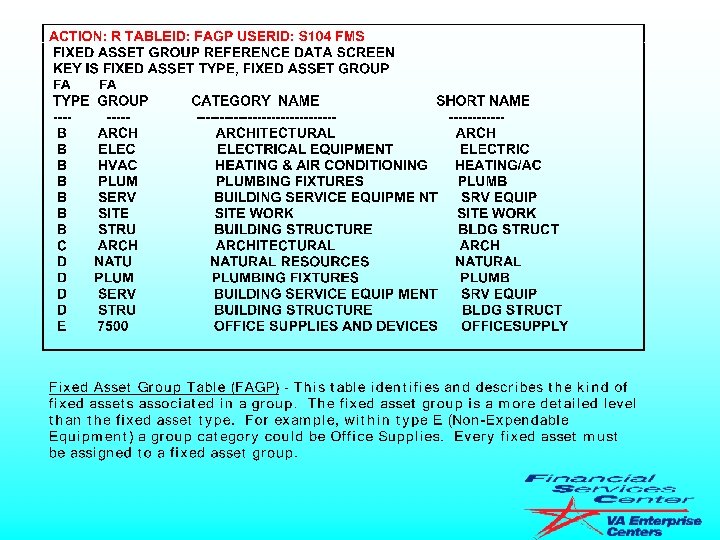

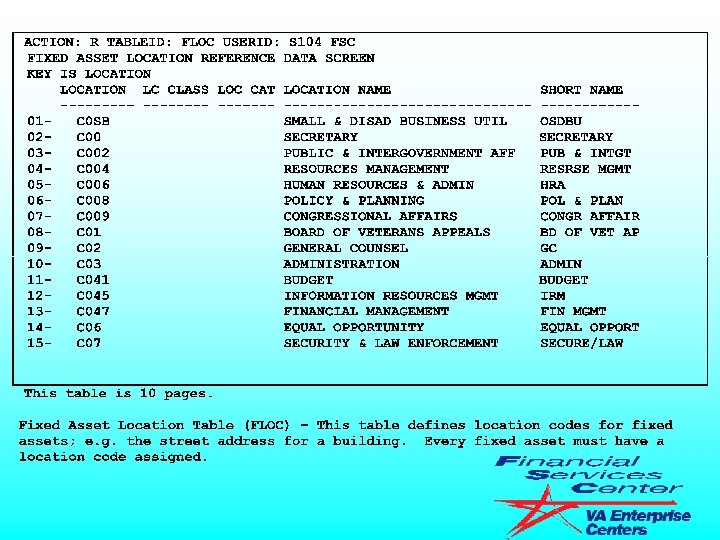

FIXED ASSETS SUBSYSTEM TABLES Reference Tables l Fixed Asset Accounting Codes Table (FAAC) l Fixed Asset Acquisition/Disposition Table (FADM) l Fixed Asset Type Table (FATY) l Fixed Asset Group Table (FAGP) l Fixed Asset Location Table (FLOC)

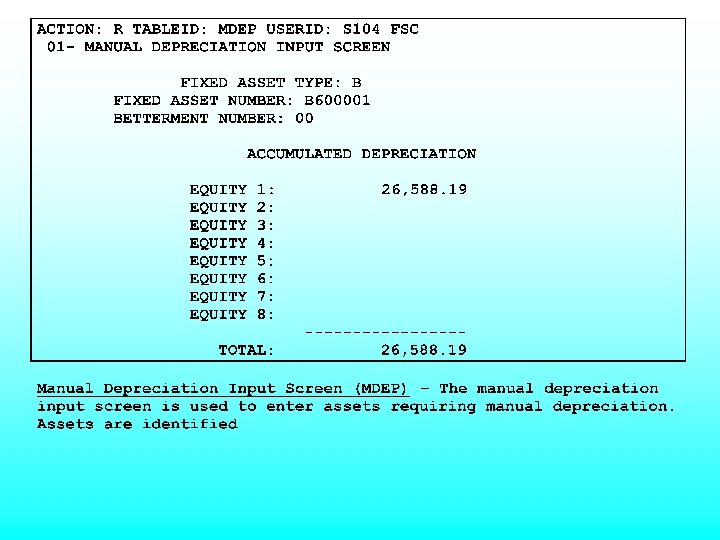

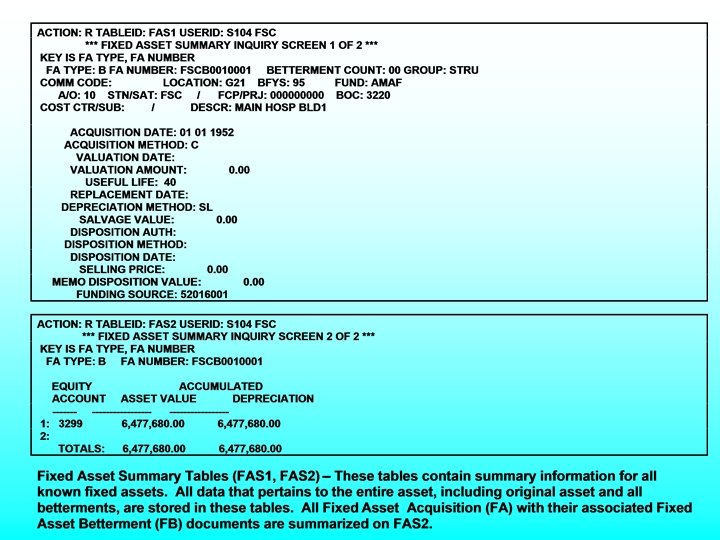

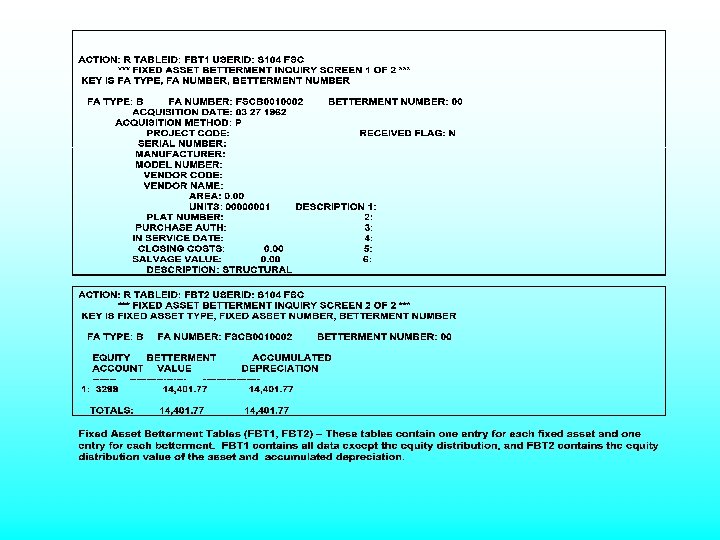

FIXED ASSETS SUBSYSTEM TABLES Inquiry Tables Manual Depreciation Input Screen (MDEP) l Fixed Asset Summary Tables (FAS 1, FAS 2) l Fixed Asset Betterment Tables (FBT 1, FBT 2) l

FIXED ASSETS SUBSYSTEM DOCUMENTS

FIXED ASSETS SUBSYSTEM DOCUMENTS - FA - Acquisition l To establish assets in FAP. l Data is sent via AEMS/MERS interface to generate FA for Personal Property. l FA is manually input in FMS for Real Property. l FMS general ledger is not affected.

FIXED ASSETS SUBSYSTEM DOCUMENTS - FB - Betterment To add a betterment to an asset. l Asset must already be in FAP (FA document). l Value of betterment is added to original asset. l FMS general ledger is not affected. l

FIXED ASSETS SUBSYSTEM DOCUMENTS - FC - Modification To change data sent on a FA or FB document. l Not used to change accounting information. l Post a revised value or useful life to the FA document. l FMS general ledger is not affected. Note: If the selling price is changed, general ledger is affected. l

FIXED ASSETS SUBSYSTEM DOCUMENTS - FR - Transfer To change data sent on a FA document. l Not really a “Transfer”. l Changes accounting data: BOC, FUND, COST CENTER, ACC, STATION NUMBER, LOCATION AND AO. l FMS general ledger is not affected. l

FIXED ASSETS SUBSYSTEM DOCUMENTS - FD - Disposition l To dispose of an asset. l Asset must already be in FAP. l FD Document “removes” the asset from FAP. l FMS general ledger is affected.

Equity Accounts The equity of an asset may be divided into as many as eight different equity accounts on the Fixed Asset Acquisition (FA) document, the Fixed Asset Betterment (FB) document and the Fixed Asset Modification (FC) document within FAP. Currently FAP uses only one equity account on each document. The correct equity account is determined by administration office.

FIXED ASSETS SUBSYSTEM DOCUMENTS l Equity Accounts Currently FAP uses only one equity account on each document. The correct equity account is determined by administration office: l For VBA (AO 20), Cemeteries (AO 40), the Office of General Counsel (AO 02), the Office of Financial Management (AO 04), and Acquisition and Materiel Management (AO 90) use acct. - 3210 Invested Capital l For VHA (AO 10) use acct. - 3299 Capital Investments Medical l For Fund 8180 S and 8129 S use acct. - 3402 Trust Property, Plant, and Equipment **** Equity accounts are not General Ledger Accounts ****

STEPS TO CORRECT EQUITY ACCOUNT Here are the steps to change the equity account from 3210 to 3299: Please go to FBT 2 because if an asset had betterments these steps will need to be done for each betterment number. 1. Screen shot of FBT 2 will show Asset value and accumulated depreciation amount ACTION: R TABLEID: FBT 2 USERID: S 104 RMJ *** FIXED ASSET BETTERMENT INQUIRY SCREEN 2 OF 2 *** KEY IS FIXED ASSET TYPE, FIXED ASSET NUMBER, BETTERMENT NUMBER FA TYPE: B FA NUMBER: 554 BANG 0160 BETTERMENT NUMBER: 00 EQUITY BETTERMENT ACCUMULATED ACCOUNT VALUE DEPRECIATION ------------ 1: 3210 121, 805. 77 30, 738. 90 TOTALS: 121, 805. 77 30, 738. 90

STEPS TO CORRECT EQUITY ACCOUNT 2. FC to change Depreciation method to MC (Manual Calculation) 3. MDEP Search FA number ACTION: R TABLEID: MDEP USERID: S 104 RMJ 01 - MANUAL DEPRECIATION INPUT SCREEN FIXED ASSET TYPE: B FIXED ASSET NUMBER: 554 BANG 0160 BETTERMENT NUMBER: 00 ACCUMULATED DEPRECIATION EQUITY 1: 30, 738. 90 --------- TOTAL: 30, 738. 90 Action: C Equity 1: 2. 00 Total 0. 00 After the change a comment saying a jv needs to be done 4. FC to revise asset value 0. 00 remember line 3210 value 0. 00 Once this accepts go back to FBT 2 to see that 3210 and accumulated depreciation are 0. 00 for both. 5. FC to revise asset value to 121, 805. 77 line 3299 121, 805. 77 Once this accepts to go FBT 2 to see is FA is now 3299 121, 805. 77 6. Update MDEP putting 30, 738. 90. See step 3 Once this has accepted to go FBT 2 to make sure it now reads equity account 3299 asset value $121, 805. 77 and accumulated depreciation 30, 738. 90. 7. FC to change Depreciation method back to SL.

FMS FIXED ASSETS GENERAL LEDGER TRANSACTIONS

GENERAL LEDGER TRANSACTIONS

GENERAL LEDGER TRANSACTIONS COMMND: DOCID: FD 10 FSC 3 N 3276 STATUS: ACCPT 006 -006 OF 001 BATID: SUB STN: 10/23/08 FIXED ASSET DISPOSITION INPUT SCREEN TRANSACTION DATE: ACCOUNTING PERIOD: 01 - FA DISP TYPE NUMBER METH DISP DATE SELLING PRICE DISP AUTH ---------- --------------- E FSC 31212594 O 02 01 2008 0. 00 00000 ASSET: 6525 -532140 ACQD: 05/01/98 WORTH: 117, 602. 91 TYPE V IN COMMND TO VERIFY DISPOSAL OF ABOVE ASSET REPORT NAME-> F. RGLDATV. 100902 FORM-> F 840 LINES-> 599203 PAGES-> 10358 ----------------------------------------------------- 10/09/08 FD FSC 3 N 3276 95 AMAFMC 10 ***** * 1759 61, 224. 07 1750 117, 602. 91 7212 60, 258. 56 6710 3, 879. 72

GENERAL LEDGER TRANSACTIONS COMMND: DOCID: FD 10 FSC 3 N 1409 STATUS: ACCPT 005 -005 OF 001 BATID: SUB STN: 10/23/08 FIXED ASSET DISPOSITION INPUT SCREEN TRANSACTION DATE: ACCOUNTING PERIOD: 01 - FA DISP TYPE NUMBER METH DISP DATE SELLING PRICE DISP AUTH ---------- --------------- E FSC 147229 T 10 21 2008 350000. 00 00000 ASSET: 6525 -439454 ACQD: 06/01/03 WORTH: 948, 189. 25 TYPE V IN COMMND TO VERIFY DISPOSAL OF ABOVE ASSET REPORT NAME-> F. RGLDATV. 102202 FORM-> F 840 LINES-> 489863 PAGES-> 8467 10/22/08 FD FSC 3 N 1409 95 AMAFMC 10 ***** * 1759 505, 176. 26 1750 948, 189. 25 3310 350, 000. 00 6710 5, 452. 09 7212 87, 560. 90

GENERAL LEDGER TRANSACTIONS

GENERAL LEDGER TRANSACTIONS l CAPITAL l LEASE Equipment under Capital Lease • FA Document to record receipt of Equipment in FAP. • SV 9 B to record receipt of Equipment (G/L 1811) and establish liability. • CT 04 to record Principal Payments and reduce liability.

GENERAL LEDGER TRANSACTIONS l CAPITAL LEASE l Building under Capital Lease • FA Document to record receipt of Building in FAP. • SV 9 C to record receipt of Building (G/L 1812) and establish liability. • CT 04 to record Principal Payments and reduce liability.

GENERAL LEDGER TRANSACTIONS Assets in the following appropriations will be moved nightly through an automated process from the acquiring appropriation to the AMAF fund for Real Property. All Personal Property will move to unique AMAF funds as listed below: Treasury Symbol AMAF FUND For Real Property AMAF FUNDS For Personal Property Other Appropriations 0129 AMAFNC National Cemetery Administration 0151 AMAFGE General Operating Expense 0152 AMAFMA Medical Administration 0160 AMAFMC Medical Services 0161 AMAFRE Medical & Prosthetic Research 0162 AMAFMF Medical Facilities 0167 AMAFIT Information Technology 0170 AMAFIG Inspector General

GENERAL LEDGER TRANSACTIONS l Fixed Asset Transfer Program (GN-068) l Daily Report of items transferred (RGLATRV) Standard Voucher Transfer Report (F 871).

GENERAL LEDGER TRANSACTIONS

GENERAL LEDGER TRANSACTIONS Assets in the following funds will NOT be moved to AMAF *** Note: Amounts in construction appropriations 0110 and 0111 and Parking Garage ( real property only) must be Manually moved to AMAF when the asset is placed in service.

GENERAL LEDGER TRANSACTIONS l Work in Process (WIP) (F 876) (SGL 1720) • Transfer costs to the proper Fixed Asset general ledger account. • For Construction (0110 and 0111) Manually transfer to AMAF.

GENERAL LEDGER TRANSACTIONS FY 2006 Issue 53 FSC NEWS FLASH Austin, Texas June 7, 2006 Clearing the F 876 Report The following information should be used as a guide for clearing the F 876 report. General Information This report identifies the Department of Veterans Affairs (VA’s) real property Work in Process (WIP). Effective June 1, 2002, the threshold for recording VA’s capitalized real property assets was increased to $100, 000. The Standard General Ledger (SGL) and Budget Object Codes (BOC) used on this report are: GL – 1720 (Work in Process) BOC – 3215 (Improvements to Land) 3220 (Buildings and Improvements) 3221 (Site Prep for Info Sys Tech) 3225 (Telecommunication Equipment) 3230 (Leasehold Improvements) 3240 (Other Structures and Facilities) Therefore, only transactions with these identifiers will appear on the F 876. This report should be reviewed at least monthly and cleared in a timely manner to ensure a smooth annual closeout. Transaction Codes (TC) and Transaction Types (TT) There are several TC and TT to be used to clear the report depending on the scenario. SV 20/28/29/30 – After Real Property meeting the $100, 000. 00 minimum threshold is placed in service, a SV transaction must be processed to transfer to the appropriate Asset GL. The SV selected is based on the BOC. The asset will then be moved automatically through the GN-68 process to AMAF fund. This procedure takes the transaction off the report. SV 20 (I) – Debits 1712 Credits 1720 SV 28 (I) – Debits 1740 Credits 1720 SV 29 (I) – Debits 1820 Credits 1720 SV 30 (I) – Debits 1730 Credits 1720 Notes: Construction (0110 and 0111) must be manually moved to AMAF when the asset is place in service. Therefore, in addition to the SV 20/28/29/30 transactions, the following also needs to be accomplished:

News. Flash cont. GENERAL LEDGER TRANSACTIONS (Make sure when processing the construction standard voucher to use the same BFYS, FUND, and project from the WIP report. ) GL 1712 (Improvements to Land) SV 76 (I) – Debits 3310 Credits 1712 “Construction Appropriation” Debits 9936 Credits 9935 SV E 2 (I) – Debits 1712 Credits 3310 “AMAF” Debits 9935 Credits 9936 GL 1730 (Buildings and Improvements) SV 71 (I) Debits 3310 Credits 1730 “Construction Appropriation” Debits 9936 Credits 9935 SV D 4 (I) Debits 1730 Credits 3310 “AMAF” Debits 9935 Credits 9936 GL 1820 (Leasehold Improvements) SV 73 (I) Debits 3310 Credits 1820 “Construction Appropriation” Debits 9936 Credits 9935 SV E 9 (I) Debits 1820 Credits 3310 “AMAF” Debits 9935 Credits 9936 GL 1740 (Other Structures and Facilities) SV 72 (I) Debits 3310 Credits 1740 “Construction Appropriation” Debits 9936 Credits 9935 Debits 9936 SV D 6 (I) Debits 1740 Credits 3310 “AMAF” SV D 6 (I) Debits 1740 Debits 9935 Credits 9936 EW 01 – Real property that does not meet the capitalization threshold of $100, 000. 00 will be expensed through the use of EW 01 if the adjustment is made during the same FY as the costs were incurred. A two line document will be accomplished with an increase (I) indicator on line 001 against the appropriate BOC for the expense and a decrease (D) indicator on line 002 against the WIP BOC. SV 49 – Real property recorded in SGL account 1720 that does not meet the capitalization threshold of $100, 000. 00 for which costs were incurred in a prior year will be written off with a SV 49 transaction. This is a Financial Policy decision. The SV 49 (I) posts 7212 debit and 1720 credit. SV 70 – This transaction is used to clean line items off the F 876 report where lines are debits and credits. The SV 70 (I) posts 3310 debit and 1720 credit. In all cases reference the same document ID for each entry on the F 876, and use either I or D as appropriate to zero out the item.

News. Flash cont. GENERAL LEDGER TRANSACTIONS Closing year – During annual close each year, each appropriation which has been expired for 5 years is closed. If a station does not clear the F 876 for the closing year, FSC will process a two line SV 70. Line 001 – the accounting information off the F 876 report will be used with an “I” indicator. Line 002 - AMAF fund with BFY 95 and a “D” indicator will be used. Fund 8180 S/4537 – Use an SV 49 to clean up the F 876 following the process described in the SV 70 paragraph above. References The above information is used as a guide for clearing the report. Specific information relating to this particular subject can be found on the following websites: http: //vaww 1. va. gov/fmshome - Procedures Guide to Field Stations Guide to Fixed Assets http: //www. va. gov/publ/direc/finance/ - OF Bulletins: 02 GA 1. 07, 02 GA 1. 08 and VA Handbook 4511 If you have questions concerning this News Flash, please contact Cheryl Holman at (512) 460 -5204 or Rosa Jimenez at (512) 460 -5046.

GENERAL LEDGER TRANSACTIONS

GENERAL LEDGER TRANSACTIONS l Work in Process (WIP) (F 762) (SGL 1832) • Transfer costs to the proper Fixed Asset general ledger account. • Manually transfer to AMAF (SGL 1830).

GENERAL LEDGER TRANSACTIONS FY 2006 Issue 50 FSC NEWS FLASH Austin, Texas May 18, 2006 Clearing the F 762 Report The following information should be used as a guide for clearing the F 762 report. General Information This report identifies the Department of Veterans Affairs (VA’s) internal use software Work in Process (WIP). Effective October 1, 2001, VA began capturing and capitalizing the costs of software developed for use by VA. This applies to Commercial off-the- shelf (COTS) software, internally developed software with or without a contractor’s assistance, and contractordeveloped software, only during the development phase of a software project. The only costs that should show up on the F 762 are those meeting the software capitalization requirements. The Standard General Ledger (SGL) and Budget Object Code (BOC) used for “Internal Use Software Capitalization” are: GL – 1832 (Internal Use Software in Development) BOC – 3124 (Internal Use Software Capitalized) Therefore, only transactions with these identifiers will appear on the F 762. This report should be reviewed at least monthly and cleared in a timely manner. Transaction Codes (TC) and Transaction Types (TT) There are several TC and TT to be used to clear the report depending on the scenario. SV 3 A – Upon completion of the development phase, a project with a minimum cumulative total cost of $100, 000 in SGL account 1832 will be transferred to SGL 1830 using an SV 3 A transaction. The asset will then be moved automatically through the GN-68 process to the related AMAF_ _ fund in the case of Appropriated Funds. This procedure takes the transaction off the report. The SV 3 A (I) posts an 1830 debit and 1832 credit.

GENERAL LEDGER TRANSACTIONS News. Flash cont. EW 01 – Internal use software projects recorded in SGL account 1832 not meeting the capitalization threshold of $100, 000 will be expensed through the use of EW 01 transaction if the adjustment is made during the same fiscal year as the costs were incurred. Internal use software not meeting the Department’s $100, 000 capitalization threshold will use BOC 3134 – ADP Software – non-capitalized. An EW 01 with an increase indicator on line 001 using BOC 3134 and a decrease indicator on line 002 using BOC 3124 should be processed to expense costs previously capitalized in 1832. SV 50 – Internal use software projects recorded in SGL account 1832 not meeting the capitalization threshold of $100, 000 for which costs were incurred in a prior year will be written off with a SV 50 transaction. This is a Financial Policy decision. The SV 50 (I) posts a 7212 debit and 1832 credit. SV 38 – This transaction is used to clean line items off the F 762 report, where lines are debits and credit. The SV 38 (I) posts a 3310 debit and 1832 credit. In all cases reference the same document ID for each entry on the F 762, use either I or D as appropriate to zero out the item. If the F 762 report does not reference a document ID then reference the same budget fiscal year, fund and project. Funds 8180 S and 4537 B – Use an SV 50 to clean up the F 762 following the process described in the SV 38 paragraph above. Specific information relating to this particular subject can be found on the following Web sites: http: //www. va. gov/publ/direc/finance/ - OF Bulletins: 02 GA 1. 02 and 02 GA 1. 09 http: //vaww 1. va. gov/fmshome - Procedures Guide to Field Stations Guide to Fixed Assets If you have questions concerning this News Flash, please contact Cheryl Holman at (512) 4605204 or Rosa Jimenez at (512) 460 -5046.

GENERAL LEDGER TRANSACTIONS

GENERAL LEDGER TRANSACTIONS l FA Documents sent in error 1. Personal Property (Supply) OA&MM must immediately notify Fiscal Service of the error. 2. Fiscal must check the FAS 2 Table for accumulated depreciation posting.

GENERAL LEDGER TRANSACTIONS 3. Fiscal must remove any accumulated depreciation from the FA (Fixed Asset Acquisition) Document. A. Process a FC transaction for the Fixed Asset to change the depreciation method to MC (Manual Depreciation). B. Update the MDEP table to $0. 00 depreciation for the Fixed Asset.

GENERAL LEDGER TRANSACTIONS 4. Process an FC (Fixed Asset Modification) Document to change the value to $0. 00. 5. Process an FD (Fixed Asset Disposal) Document with a $0. 00 selling price to delete the erroneous FA Document.

GENERAL LEDGER TRANSACTIONS 6. If accumulated depreciation has posted against the general ledger, it must be removed using an SV (Standard Voucher) Document. Note: Following these steps will prevent general ledger entries from being made.

GENERAL LEDGER TRANSACTIONS COMMND: DOCID: FD 10 FSCB 0020010 STATUS: ACCPT 001 -001 OF 001 BATID: SUB STN: 10/23/08 FIXED ASSET DISPOSITION INPUT SCREEN TRANSACTION DATE: ACCOUNTING PERIOD: 01 - FA DISP TYPE NUMBER METH DISP DATE SELLING PRICE DISP AUTH ---------- --------------- B FSCB 0020010 O 10 11 2002 0. 00 FSC-000 -02 ASSET: FSCC 10194 ACQD: 08/30/02 WORTH: 0. 00 TYPE V IN COMMND TO VERIFY DISPOSAL OF ABOVE ASSET

GENERAL LEDGER TRANSACTIONS l Fixed Asset completely depreciated will be drop with a FD document

FIXED ASSETS EXCESS EQUIPMENT

FIXED ASSETS EXCESS EQUIPMENT l An Asset that is determined to be in excess (Property Pending Disposal) must be moved to the excess account (1524) general ledger located in AEMS/MERS, FAP and the FMS general ledger. 1. FD (Fixed Asset Disposition) document for disposal of the asset. 2. Selling price is book value.

FIXED ASSETS EXCESS EQUIPMENT 3. FA (Fixed Asset Acquisition) document for excess equipment. 4. Fiscal must create an SV (Standard Voucher) document (7 C) to reestablish the asset in the general ledger Property Pending Disposal Account (1524).

FIXED ASSETS EXCESS EQUIPMENT SALES l Proceeds used to purchase similar equipment. 1. Proceeds will be deposited into Fund 3845. 2. Proceeds will be available to the VA during the Fiscal year of the sale and for one Fiscal year thereafter and may only be used to purchase similar equipment.

FIXED ASSETS EXCESS EQUIPMENT SALES l If the equipment was originally purchased through supply fund resources, the proceeds will be returned to Supply Fund (Fund 4537 B). l If neither of the first two alternatives above apply, the funds will be deposited into Miscellaneous Receipts (Fund 3220), which return the proceeds to Treasury.

FIXED ASSETS RSD REPORTS

FIXED ASSETS RSD REPORTS 1. Standard Voucher Document Transfer (RGLATRV - Form F 871). 7 -5 2. Fixed Assets Summary Depreciation Report (RFASDRVI - Form F 058). 7 -6

FIXED ASSETS RSD REPORTS 3. Fixed Assets Summary Detail Listing Report (RFADETLV - Form FA 04). 7 -7 4. Fixed Asset Exception Report (RFAFXCV - Form FFA 7). 7 -8

FIXED ASSETS RSD REPORTS 5. General Ledger Reconciliation of FMS and Fixed Asset Report (RFAVGLV - Form F 852). 7 -11 6. Document Processing Report Accepted (RGSADLV 2 - Form F 829) 7 -9 Rejected (RGSGDPV 2 - Form F 97 D)7 -10

FIXED ASSETS RSD REPORTS 7. FMS Inventory Report (RGLLIAV - Form F 832)7 -12

This report provides a list of all standard voucher documents as well as the related originating document information, created during the nightly cycle to move assets to the AMAF funds. This process only impacts the FMS general ledger.

This report summarizes depreciation expense (General Ledger Account 6710) by FY, BFY, and FUND for the current fiscal month.

This report lists a detailed listing of all FA numbers, AO, BOC, Description, Acq. Date, Useful Life, Rpl Date, General Ledger, Asset, Acc Depr, and Differences.

*A=Asset amount less than $100, 000; B=Missing or wrong BOC; L=Questionable useful life

This report lists all the successfully processed transactions.

This report lists rejected transactions which did not process successfully due to errors and are listed on the FMS Document Suspense File table (SUSF).

This report lists General Ledger totals for the asset and accumulated deprecation from the FMS General Ledger and corresponding totals from the Fixed Assets Subsystem. It also displays any out of balance conditions between General Ledger and FAP by General Ledger account and fund.

This monthly report lists all inventories activity during the month by fund, general ledger, document identification number and amount.

This monthly report lists all inventories activity during the month by fund, general ledger, document identification number and amount.

FIXED ASSETS RECONCILIATION

FIXED ASSETS RECONCILIATION l REAL PROPERTY Subsidiary records (FAP) = General Ledger Trial Balance (FMS).

RECONCILIATION l PERSONAL PROPERTY = FMS (GL), AEMS/MERS, FAP

FIXED ASSETS RECONCILIATION l FMS RECONCILIATION TABLES • FAS 2 (Fixed Assets Summary) • GLTS ( General Ledger Trial Balance)

FIXED ASSETS RECONCILIATION l FMS Reconciliation Reports • General Ledger Reconciliation of FMS (Daily)and Fixed Assets Report RFAVGLV Form F 852. • SV Document Transfer Report (Daily) RGLATRV Form F 871.

FIXED ASSETS RECONCILIATION • FMS Inventory Report (Monthly) RGLLIAV Form F 832.

This report lists General Ledger totals for the asset and accumulated deprecation from the FMS General Ledger and corresponding totals from the Fixed Assets Subsystem. It also displays any out of balance conditions between General Ledger and FAP by General Ledger account and fund.

This report provides a list of all standard voucher documents as well as the related originating document information, created during the nightly cycle to move assets to the AMAF funds. This process only impacts the FMS general ledger.

This monthly report lists all inventories activity during the month by fund, general ledger, document identification number and amount.

PRACTICE EXERCISES