Recommendations for Multiemployer Pension Reform Findings of the

- Slides: 72

Recommendations for Multiemployer Pension Reform Findings of the NCCMP Retirement Security Review Commission Presented to: P PBGC Advisory Committee November 29, 2012 By: Randy G. De. Frehn Executive Director NCCMP 1

Overview • Trends in Retirement Income Provision • Current Challenges Facing Multiemployer Plans • Retirement Security Review Commission • Recommendations for Comprehensive Reform

Trends

Collapsing Pillars Three Pillars of Retirement Security: • Social Security • Private Pensions • Personal Savings

Shift from DB to DC • • Trend over past 30 years Dominant among Corporate plans as the Primary Retirement vehicle – Driven by: • Employers’ Desire to Shift Investment Risk • Vastly reduce administrative cost & complexity • DC Typically supplemental for most multiemployer plans • Objective usually based on capital accumulation, not replacement income target – Complicates Retirement Planning – Eliminates Retirement for most low to Moderte Wage Workers

Positive Correlation Between Union Representation and Pension Coverage “Overall, union workers’ rate of participation in retirement plans—at 80 percent —was greater than that of nonunion workers, which was 48 percent. ”

U. S. Department of Labor, Bureau of Labor Statistics…March 2009 “The only surveyed group that had greater participation in defined -benefit plans than defined contribution plans was union workers. The definedbenefit participation rate was 67 percent for union workers, more than triple the average rate of all private industry workers. ” workers

Why DB?

The More Efficient Approach “… we find that a DB pension plan can offer the same retirement benefit at close to half the cost of a DC retirement savings plan. Specifically, our analysis indicates that the cost to deliver the same level of retirement income to a group of employees is 46% lower in a DB plan than it is in a DC plan. • Longevity risk pooling in a DB plan saves 15%, • Maintenance of a balanced portfolio diversification in a DB plan saves 5%, and • A DB plan’s superior investment returns save 26% …… as compared with a typical DC plan. ”

Current Challenges

Focus on Unfunded Vested Liabilities

Not Your Grandfathers’ Withdrawal Liability • Changing Environment in the Financial Services Industry Has Changed the World for Employers – Tighter Funding Rules from PPA • Higher Contributions to meet Rehabilitation and Funding Improvement Plans Causing Withdrawal Liability to Rise

Not Your Grandfathers’ Withdrawal Liability • Changing Environment in the Financial Services Industry Has Changed the World for Employers – Tighter Funding Rules from PPA • Higher Contributions to meet Rehabilitation and Funding Improvement Plans Causing Withdrawal Liability to Rise – 20 Year Cap Creates Incentives to Leave

Not Your Grandfathers’ Withdrawal Liability • Changing Environment in the Financial Services Industry Has Changed the World for Employers – Tighter Funding Rules from PPA • Higher Contributions to meet Rehabilitation and Funding Improvement Plans Causing Withdrawal Liability to Rise – 20 Year Cap Creates Incentives to Leave – Dodd – Frank Tighter Controls on Lending

Not Your Grandfathers’ Withdrawal Liability • Changing Environment in the Financial Services Industry Has Changed the World for Employers – Tighter Funding Rules from PPA • Higher Contributions to meet Rehabilitation and Funding Improvement Plans Causing Withdrawal Liability to Rise – 20 Year Cap Creates Incentives to Leave – Dodd – Frank Tighter Controls on Lending – FASB’ s New Disclosure Requirements

FASB’s New Disclosure Requirements

FASB’s New Disclosure Requirements Forgive Them Lord, for They Know Not What They Do….

Not Your Grandfathers’ Withdrawal Liability • Changing Environment in the Financial Services Industry Has Changed the World for Employers – Tighter Funding Rules from PPA • Higher Contributions to meet Rehabilitation and Funding Improvement Plans Causing Withdrawal Liability to Rise – – 20 Year Cap Creates Incentives to Leave Dodd – Frank Tighter Controls on Lending FASB’ s New Disclosure Requirements Credit Suisse, Rating Agency Critiques

“We estimate multiemployer pension plans in the U. S. are $369 billion underfunded (52% funded)…” 30

“On an actua basis the me multiemploye pension plan 85% funded… 31

What Can Be Done?

NCCMP “Retirement Security Review Commission”

Background • Why Examine the Multiemployer System Now? – Funding rules sunset in 2014 – Unprecedented challenges • • • Asset volatility Recession Accounting / Ratings agency pressure – Last fundamental change to system was in 1980

Background • Commission Overview – First meeting in August 2011 – Includes Over 40 Organizations • • International unions Employer trade groups Individual large companies Multiemployer plans – Participating Industries • Construction, trucking, retail food, entertainment, machinists, mining, bakery & confectionary, service

Background • Process – – First Monthly Meetings, Evolved to 2 days per month Plus Conference calls among work groups – Sought Expert Advice: • • • Economists policy researchers investment professionals Actuaries representatives of non-US plans

Background • Core Principles –Proposals must protect retirement income security for participants –Proposals must reduce or eliminate the financial risk to the sponsoring employers

Background • Commission Focus Fell into Three Categories – Preservation: • Provisions to strengthen the current system – Remediation: • Measures that target deeply troubled plans – Innovation: • Proposal for alternative plan design structure

Background • Commission Recommendations Are Additional Tools for Plans – Strictly Voluntary: Plans are not required to adopt any new provisions – Trustees of many plans need more flexibility to address challenges

Preservation

Provisions to Strengthen the Current System • Allow Certain Yellow Zone Plans to Elect to Be in Red Zone – Must be projected to enter red zone in next 5 years – Allows early access to all red zone tools – Plan would be considered critical for participant notice purposes – Surcharges would not apply – Use is optional for plans

Provisions to Strengthen the Current System • Extend certain red zone features to All Yellow Zone Plans – Excise tax protection – Ability to accept lower contribution rates – Greater ability to improve benefits if experience allows • Ability to adjust benefits would remain limited to red zone plans

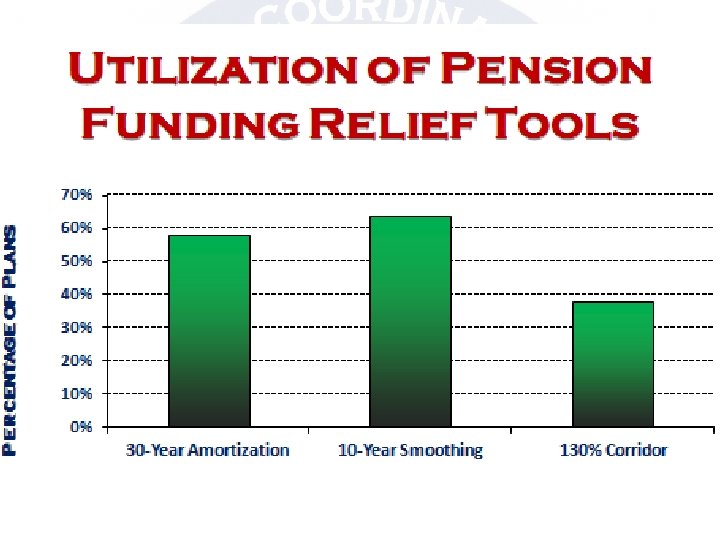

Provisions to Strengthen the Current System • Establish Permanent Funding Relief Provisions Fashioned After Provisions Enacted Post-PPA – Provisions would trigger following a sharp market decline – 30 -year amortization of losses – 5 -year amortization extension – Enhanced asset smoothing – Use of these relief measures would be optional for plans

Provisions to Strengthen the Current System • Other Technical Enhancements – Change Funding Target Starting point to certification date for Funding Improvement Plan (Removes Uncertainty of Predictions) – Treats Single and Multiemployer Plan Survivors equally in Determining who is eligible for PBGC pre-retirement survivor benefits

Provisions to Strengthen the Current System • Other Technical Enhancements – Resolves ‘Revolving Door’ problem for Entry into /Exit from Critical Status – Allow Plans to determine terms re: CBA renewals while in a zone – Assigns priority to Zone Rules over Reorganization rules to resolve Conflicts – Addresses ‘No Action’ yellow zone plans – Contribution Increases required for FIP/RP disregarded for Withdrawal Liability purposes

Provisions to Strengthen the Current System • Mergers and Alliances – Encourage PBGC to facilitate mergers – Allow “Alliances” where Stronger plans may ally with weaker plan to provide economies of scale without taking on legacy costs – Similar to provisions introduced in both Pomeroy / Tiberi and Casey bills

Provisions to Strengthen the Current System • Allow plans to harmonize normal retirement age with Social Security – Non-retired participants only – Participants within 10 years of normal retirement protected – Available to all plans, regardless of funded position – Use of provision is optional – no obligation for plans to change

Provisions to Strengthen the Current System • Other suggestions to strengthen plans – Federal backing for bond offerings use to fund plans – Enhanced tax deductions for contributions above minimum – Allow plans to opt-out of PBGC guarantee in exchange for present value of the guarantee

Remediation

Provisions For Deeply Troubled Plans Current Rules • For the minority of plans facing inevitable insolvency There is no early intervention option – Assets must be depleted and Benefits will be cut to PBGC maximum guarantee level • Approximately $13, 000 per year for full career (30 Year) employee who retires at age 65 – Ability of PBGC to support even this benefit level is in doubt

Key Statistics: PBGC Multiemployer Guaranty Fund Net Program Financials Net Position September 30, 2011 ($2. 770 billion) 2011 Snapshot: Premium Income Investment Income $92 million $91 million Assets Liabilities Net Position September 30, 2012 $1. 807 billion ($2. 467 billion) ($5. 237 billion) billion

PBGC Annual Report 2012 • “The Corporation estimates that, as of September 30, 2012, it is reasonably possible that multiemployer plans may require future financial assistance of approximately $27 billion. • As of September 30, 2010 and 2009, these exposures were estimated at approximately $23 billion and $20 billion, respectively. The significant increase in FY 2012 from prior years is due primarily to new data received for two particularly large plans; and the decrease in interest rates for valuing liabilities. “ – one plan, with a net liability of $20 billion, is in the ―transportation, communication, and utilities industry category; – the other, with a net liability of $6 billion, is in the ―agriculture, mining, and construction industry category Source: PBGC 2012 Annual Report, P. 51.

Provisions For Deeply Troubled Plans • Commission believes that if all of the following are true: a) A plan has taken all reasonable measures to improve funding b) Insolvency is still inevitable c) It is possible to avoid insolvency and preserve benefits above the PBGC maximum guarantee level • Then the trustees should have the authority to suspend a portion of the accrued benefits

Provisions For Deeply Troubled Plans • Key Considerations – Preserving benefits above PBGC guarantee is preferable to insolvency – Will allow some plans to survive for future generations – Protections are needed for especially vulnerable populations – Troubled plans may choose to use this tool based on their individual circumstances and philosophy

Provisions For Deeply Troubled Plans • Criteria for accessing Benefit Suspension Tool: – Insolvency projected within: • 15 years • 20 years if active to inactive ratio exceeds 2: 1 – Plan has taken all reasonable measures to avoid insolvency – After application of suspensions, plan is projected to be solvent

Provisions For Deeply Troubled Plans • Suspension Limitations – Benefits must be preserved at no less than 110% of PBGC guarantee – Suspensions must be no greater than is necessary to avoid insolvency – Any future benefit increases must be accompanied by a comparable restoration of suspended benefits

Provisions For Deeply Troubled Plans • Participant Protections – PBGC approval is required – Application must describe: • Measures taken to improve funding • Summary of proposed suspensions – PBGC has 180 days to consider application • Trustee due diligence will be granted great deference • PBGC inaction will be a deemed approval

Plans are Adopting Alternative Allocation Rules • Alternative allocation rules are for withdrawal liability • Splitting of plans’ Unfunded Vested Benefits (UVBs) between “new employers” and “old employers” – “new employer” UVBs: liabilities associated with service with employers that first participate in the plan after a certain date less assets attributed to the new employers – “old employer” UVBs: the plan’s total UVBs less the UVBs in the “new employer” pool to assure 100% allocation of UVBs • Separate pools are only for purposes of withdrawal liability; The plan continues to have a single funding standard account Source: PBGC Presentation at NCCMP Conference, October 2012 60

Innovation

Alternative Plan Design Structure • Commission Believes that Current Available Options Do Not Meet Needs of All Groups – Defined Benefit Plan – Employers unwilling to accept market risk – Defined Contribution Plan – Highly inefficient vehicle for retirement security • Parties should have ability and be encouraged t to develop new “Flexible models”

Alternative Plan Design Structure • Commission Approach – Avoid DB vs. DC Jargon – Overall Commission Principles, Proposals must: • protect retirement income security for participants • reduce or eliminate the financial risk to the sponsoring employers

Alternative Plan Design Structure • Commission Approach – Attract and retain employers – Promote creative plan designs • Innovation is encouraged – Flexible alternatives include, but are not limited to: – Variable DB plans (Cheiron/UFCW Design) – Target Benefit Plans (similar to Canadian Plans)

Alternative Plan Design Structure • Variable Defined Benefit Plan – Generally fits current DB definition – Comprised of two component parts • Core Benefit • Variable Benefit – Operates under Current Law

Alternative Plan Design Structure • Variable Defined Benefit Plan – Core Benefit is determined using a low assumed rate of return (e. g. 5%) – Variable Benefit is derived from earnings in excess of Core • Can be increased in good years or reduced in years of poor investment performance but benefit cannot go below Core Benefit Value • Participants are assigned “Shares” – Number of Shares are definitely determinable – Value of Shares is variable

Alternative Plan Design Structure • Variable Defined Benefit Plan – Employers remain subject to withdrawal liability as under current rules – Likelihood of incurring liability greatly reduced through conservative management of investments – Can be further reduced by purchase of annuities on retirement – Covered by PBGC Multiemployer Guaranty Fund

Alternative Plan Design Structure • Target Benefit Plan – Operates like but is technically a defined benefit plan not – Neither DB nor DC plans under current code definitions – Designed as a better alternative to moving to current DC design

Alternative Plan Design Structure • Target Benefit Plan – addresses Shortcomings of defined Contribution plans • Benefits are paid as lifetime annuities • Pooling of longevity risks • Ability to Negotiate Fees comparable to current DB fees • Asset diversification to enhance returns

Alternative Plan Design Structure • Target Benefit Plan – Absence of withdrawal liability – Funding standards more conservative than current system – Trustees have increased ability to adjust benefits in event of funding distress – Options depend upon plans’ current Funding level – appropriate protections for vulnerable populations

Alternative Plan Design Structure • Target Benefit Plan – Plan minimum contributions determined by plan actuary – Would permit diverse investments to allow participation in market gains – Builds in participant protections by requiring funding at 120% of expected costs

Alternative Plan Design Structure • Target Benefit Plan – Funding adequacy determined by 15 year projection – Benefit adjustments are required at various points based on current funding and 15 year projection – Additional protections are possible through portfolio immunization and purchase of annuities

Alternative Plan Design Structure • Target Benefit Plan – If a plan fails to meet the long term funding requirements, Trustees are to take corrective actions based on hierarchy of adjustment options – Self Correcting feature distinguishes this design from DB plan – Since PBGC Guaranty Fund only insures DB plans, the Target Plan would not be covered

Alternative Plan Design Structure • Target Benefit Plan – As a last measure, in the event of a catastrophic event the core (nonancillary) benefits of pensioners can be reduced – Reductions subject to protections for vulnerable populations similar to those provided for deeply troubled plans including PBGC oversight

Alternative Plan Design Structure • Key Concepts – Eliminating Withdrawal Liability can remove current employer incentives to leave – Will both preserve and strengthen worker retirement security – For most plans, withdrawal liability is not a significant source of contribution income – Goal of flexible plans is to focus on benefit security from: • willingness of employers to enter and remain in plans • Prudent and conservative management by the trustees

Alternative Plan Design Structure • Transition – Adjustable benefit provisions apply prospectively only to credit earned after adoption – Parties migrating to a flexible benefit design would have access to extended amortization of legacy liabilities

Alternative Plan Design Structure • Transition – Current rules remain in effect for legacy costs • PPA zone statuses • Minimum funding standards • Withdrawal liability • Benefit protections • PBGC Guarantees Apply (to the extent they remain available)

Alternative Plan Design Structure • Transition – Accruals in current plan would ceases, and accruals in new plan would begin – New and old plan can have same provisions – Contribution rates allocated between legacy benefits and future benefits – Longer amortization allowed in legacy plan to ease transition

Next Steps • • • Determine Legislative vs. Regulatory Paths Draft proposed language Educate Congressional Committee Members and Staff and Regulators • PPA rules sunset at the end of 2014 – another election year Target for Congressional Action - 2013

Questions? ? ? 80