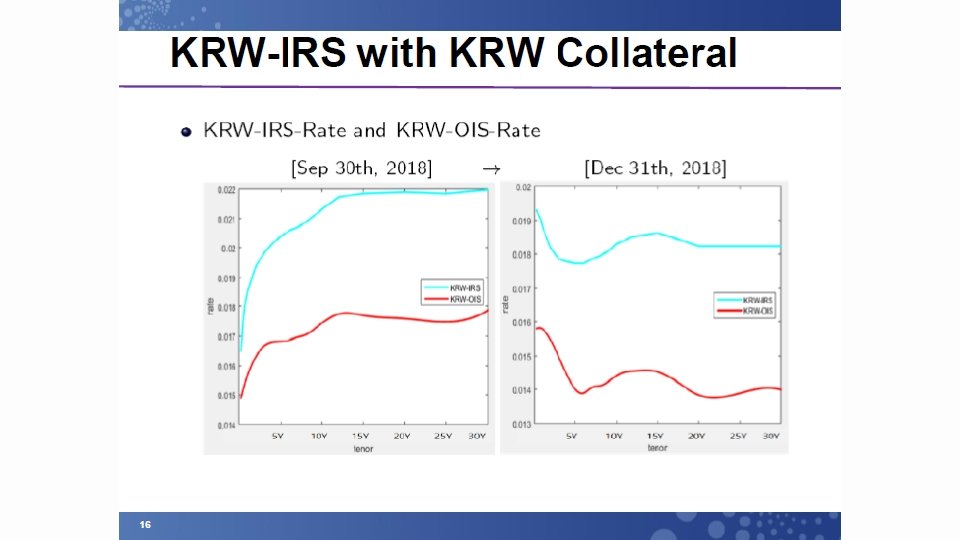

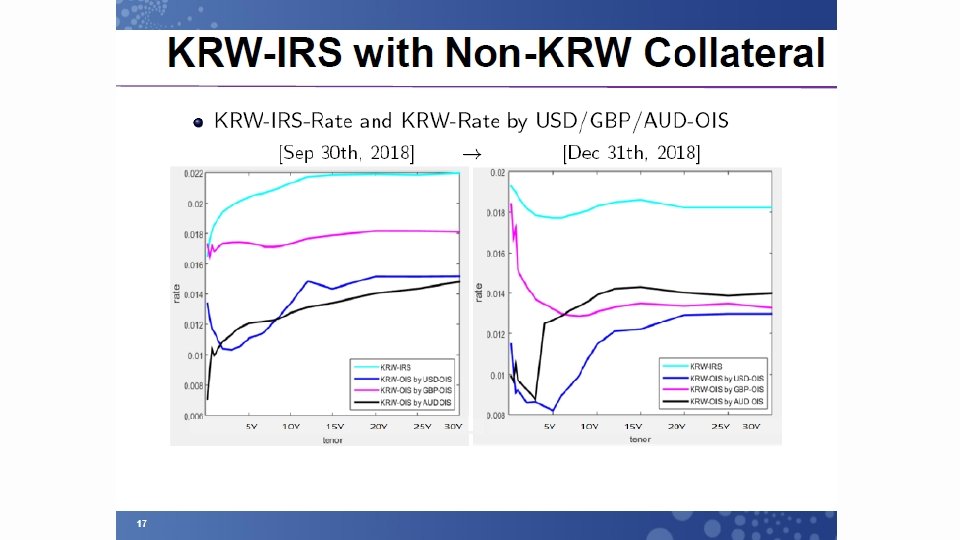

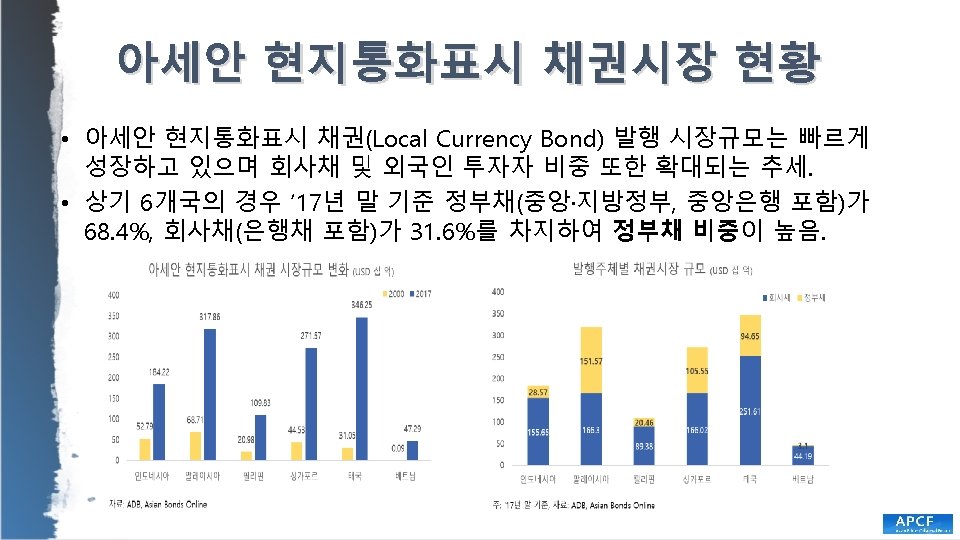

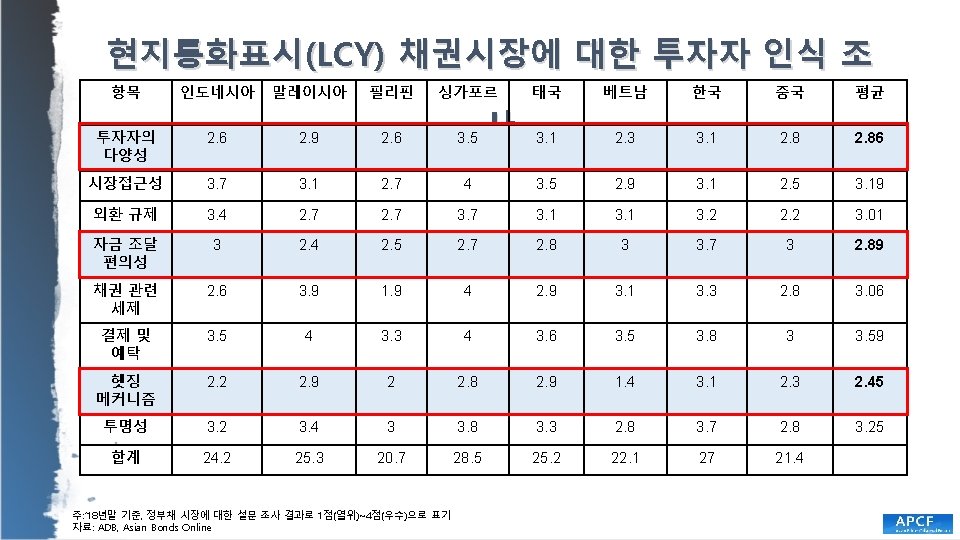

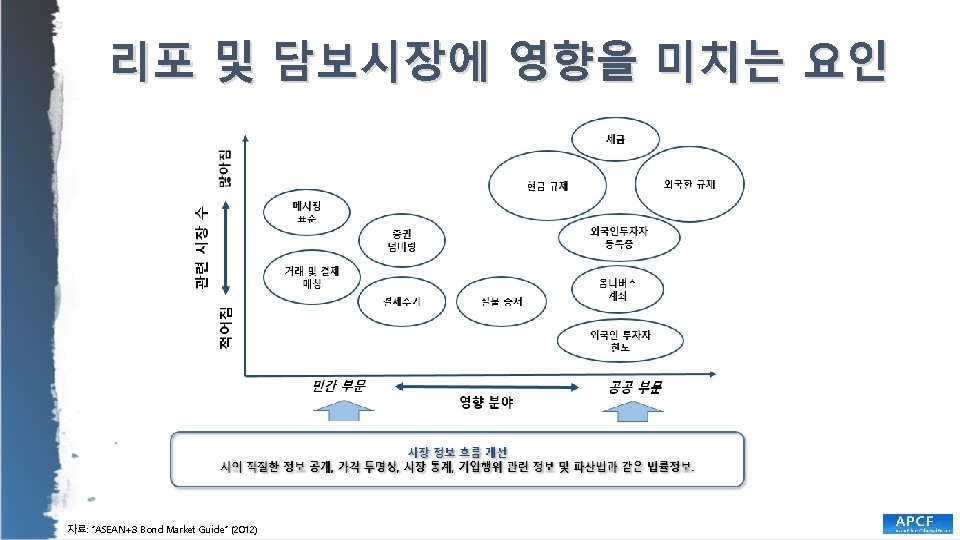

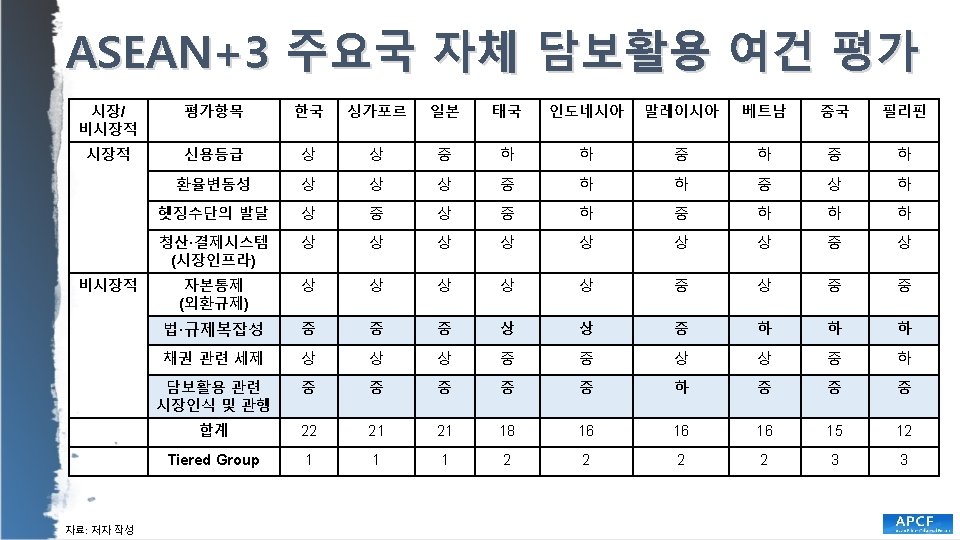

Keynote Speech Manmohan Singh International Monetary FundIMF Collateral

")

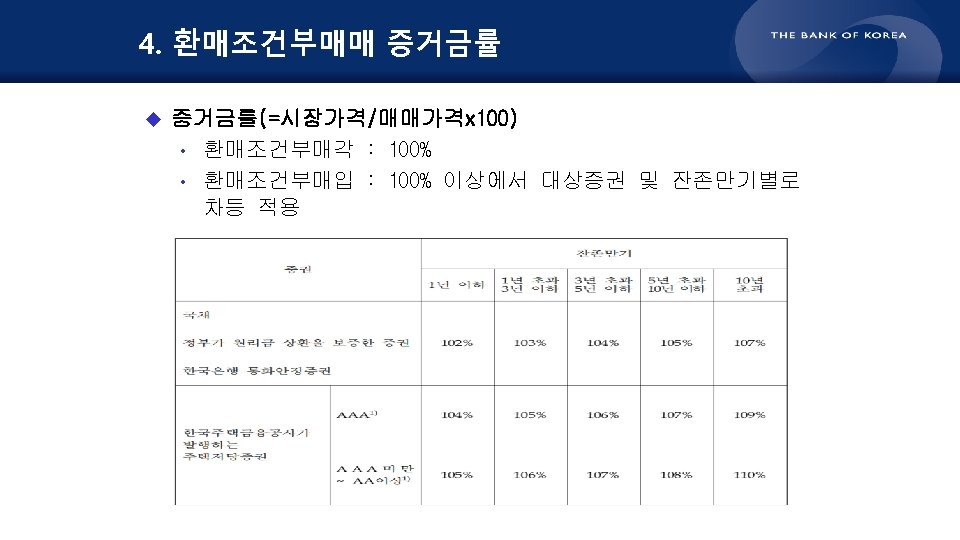

(a) securities-lending improving; (b) access to plumbing")

• Securities in")

• Chart shows the")

IMF")

transactions")

- Slides: 111

Keynote Speech Manmohan Singh International Monetary Fund(IMF)

Collateral Frameworks, Central Bank Balance Sheets, and Implications for Asia ASIAN PRIME COLLATERAL FORUM December 19, 2019, Seoul, South Korea Manmohan Singh Senior Economist, International Monetary Fund Views are of the author(s) only and not of the IMF, its Executive Board, or its management. The paper also does not reflect views of IMF’s team on FSAP or Article IV surveillance work IMF | Monetary and Capital Markets 6

Background/ Summary • QE provided monetary accommodation by buying good collateral such as US Treasuries or Bunds and lowered long-term bond spreads • Some have argued that safe asset shortage, and thus the private sector’s role in creation of safe assets, may have led to the Lehman-era crisis • However, literature largely ignores that changes in supply & demand for bonds in the market (i. e. , good collateral) could also affect the short-term market rates • We call this “reverse transmission”– different than monetary policy transmission from policy rate changes to long term yields. And reverse transmission is weaker now relative to pre-Lehman era. • Good collateral needs to be used; not silo-ed; Asian prime collateral can fill the gap if there is global shortage of safe assets. IMF | Monetary and Capital Markets 7

Market Plumbing: US Banks active in pledged collateral market IMF | Monetary and Capital Markets 8

Market Plumbing: Non-US banks active in pledged collateral market IMF | Monetary and Capital Markets 9

Market Plumbing…. Role of central bank has increased –U. S. (at present, money < collateral) Notes: Blue area is market plumbing; rest is the public-sector balance sheet IMF | Monetary and Capital Markets 10

Eurozone plumbing (at present, collateral < money) (a) securities-lending improving; (b) access to plumbing helps IMF | Monetary and Capital Markets 11

Need for market plumbing to increase (and less central bank plumbing) • Securities in the market are useful as they are used as collateral for short-term market transactions (repo, sec-lending, prime- brokerage, derivative margins) • The traditional view is if central banks were to sell government securities to the market, money is absorbed from the market, and there is tightening of financial conditions. • However, if the central bank removes a large amount (like in QE), repo, sec lending etc. are impaired; market plumbing reduces as there are fewer bonds. • Thus releasing securities (or central bank balance sheet “unwind”) re-activates repo/sec lending etc. , and there is transmission to short-term market rates. IMF | Monetary and Capital Markets 12

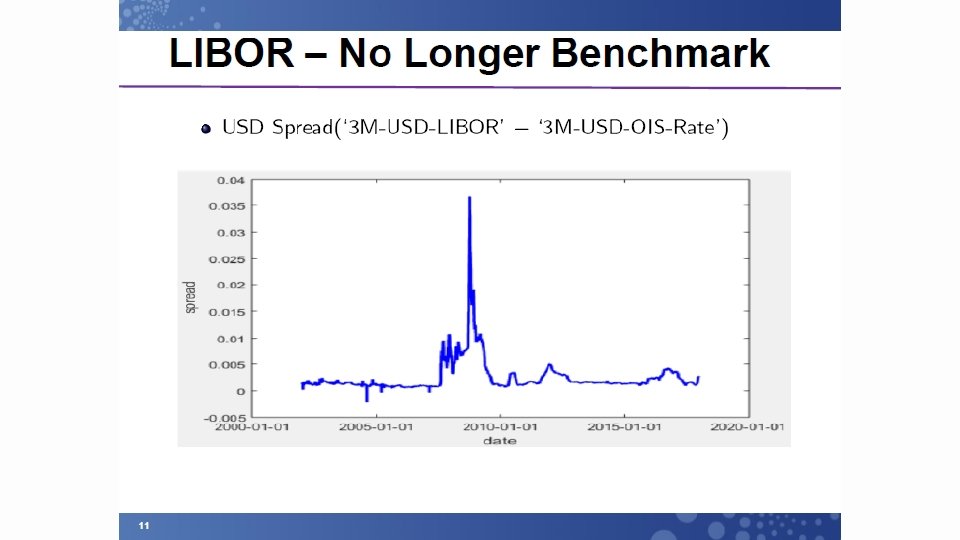

Transmission to short-term rates is now weaker (relative to pre-Lehman) • Chart shows the robustness of Beta(s) over the term structure • Securities with 6– 12 -month outstanding tenor have highest “moneyness” (i. e. , time for reuse, plus limited duration risk). IMF | Monetary and Capital Markets 13

Intuition to QE : money increases; good collateral decreases Lehman-crisis/collateral decrease (LM 1) IMF | Monetary and Capital Markets QE: money increases, collateral decrease (LM 2) 14

Some Policy Issues to Consider… • Collateral to money (or money to collateral) transactions do not happen in vacuum! • Dealer balance sheets space —is now increasing (relatively more elastic than in the aftermath of Lehman & new regulations). • There is need to incentivize use of dealer-balance sheet for market plumbing, and less use of public sector balance sheet. • Excess reserves—a by-product of QE—should not be preferred over good collateral like U. S. treasuries or German bunds; both reserves and collateral are HQLA from regulatory angle; but bonds can be reused; not excess reserves! • In the new regulatory era, balance sheet space is not free. • collateral transactions that straddle sec-lending, prime brokerage and derivatives are more attractive to a bank, relative to repo involving a US Treasury (= low margin and thus unattractive from a bank’s P&L angle). IMF | Monetary and Capital Markets 15

Global Monetary Policy and Role for Asian Collateral Restricting collateral re-use (e. g. , QE) is a tight “money” policy that seems to be at odds with the current policies of key monetary authorities Global demand for Safe Assets (HQLA or Prime Collateral): Demand = Nominal Supply x re-use rate (right hand side is “effective supply” in the global market) If there is cross-border demand for prime Asian collateral, this can change the global equation. Rise of Asia local currency bond market has been phenomenal (well over $10 trillion/ ABF’s Pan. Asian bond index Fund); thus need to leverage this globally. Asia-region has a bias towards equity—and this can be an attractive/diversified collateral as rest of world has a bias towards fixed-income securities as collateral. IMF | Monetary and Capital Markets 16

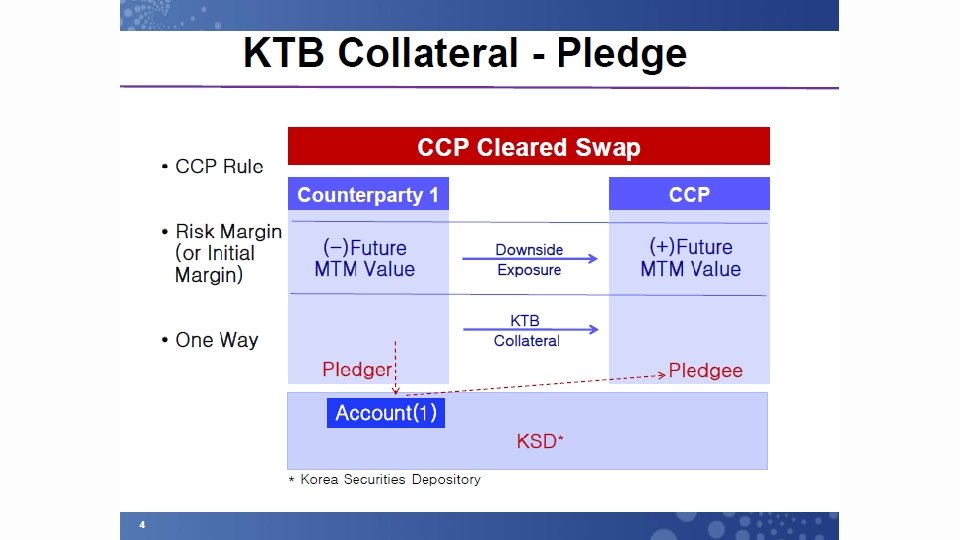

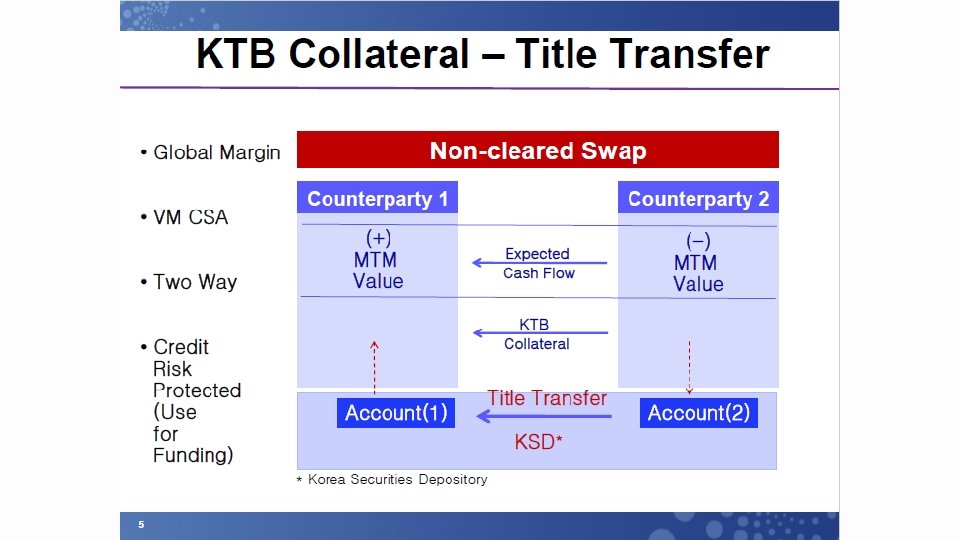

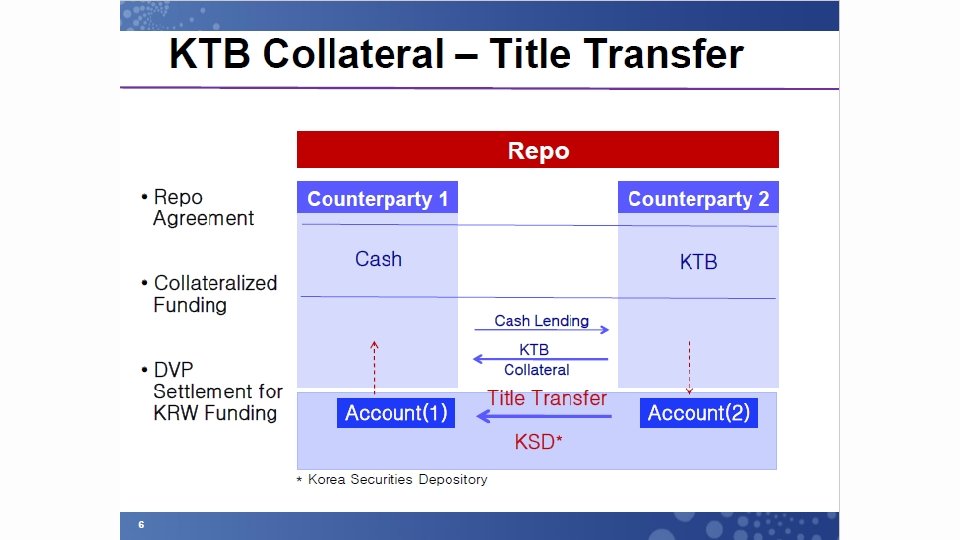

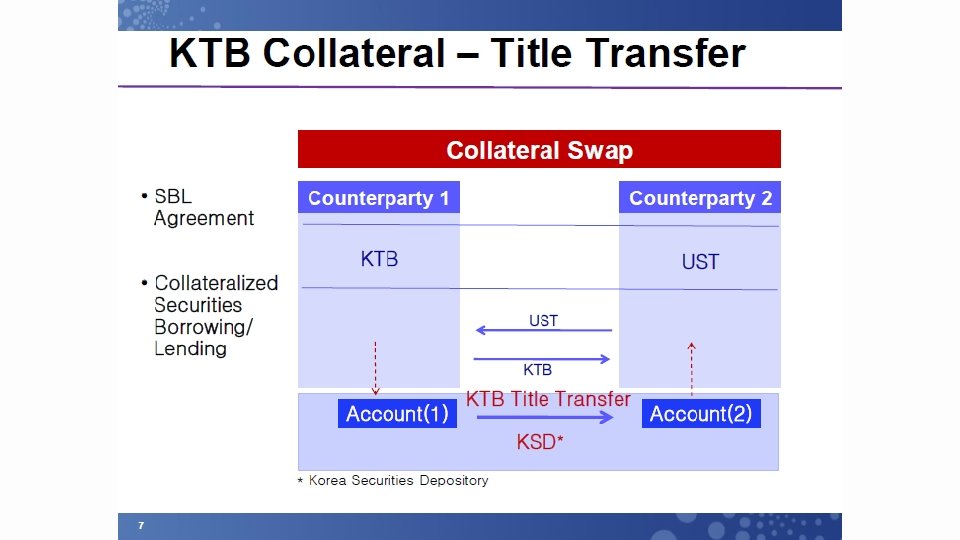

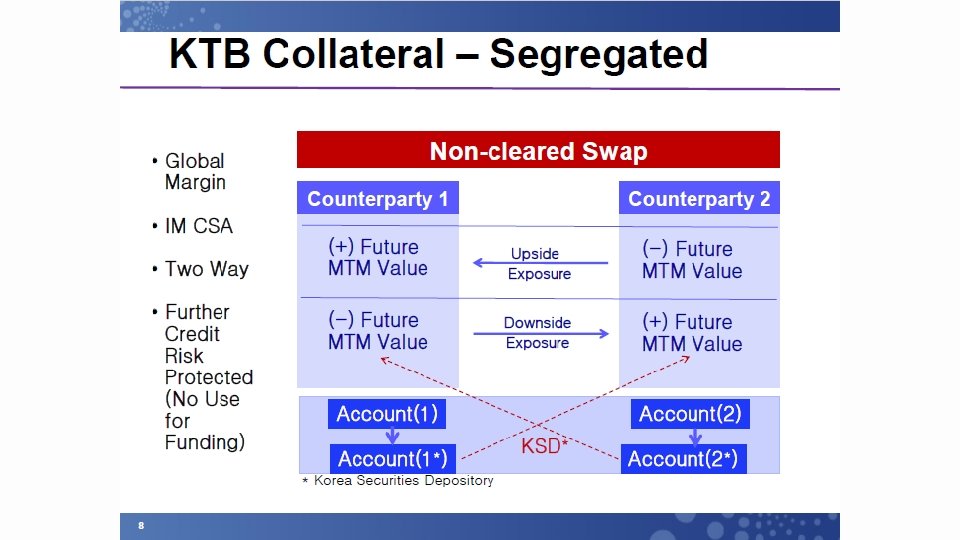

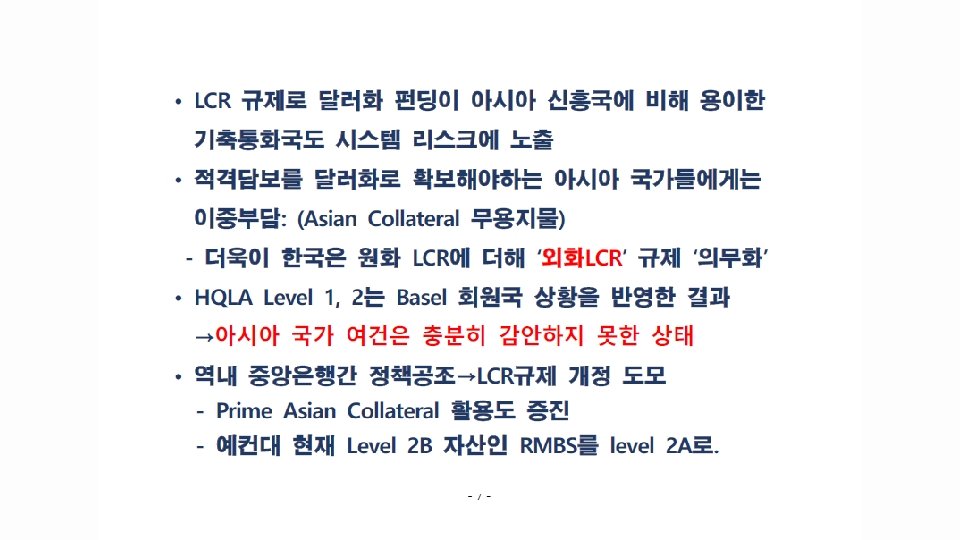

Need offshore demand for Asian collateral However, cross-border use is limited due to local restrictions: § Korean government bonds must be held at Korean Securities Depository § JGBs not widely held by non-Japanese; QQE mutes collateral reuse as JGBs are “silo-ed”. § US Treasuries preferred in Asian time zone as collateral –over JGBs or Aussie bonds Suggestions to improve the ‘Asian plumbing’ § Many countries restrict the repo market access to onshore entities; this needs to change § Role of offshore custodian will be important initially (to get the offshore bid) § Asia focused banks (G-SIBs/D-SIBs) encourage cross-border transactions in Asian collateral § Bilateral plumbing needs to start (e. g. , HK$ and JGBs), and then tri-lateral, then quadrilateral; ……. pooled Asia collateral, or tiered structure may be possible [ need to start Asian plumbing, just like BTPs have access to Eurozone plumbing; then Asian pipes need to connect to global plumbing] IMF | Monetary and Capital Markets 17

COFFEE BREAK

담보가 실물 경제에 미치는 영향 자료: “Central bank operating frameworks and collateral markets” (BIS, 2015)

달라진 중앙은행의 담보중시 운영체제 • 글로벌 금융위기 이후 비전통적 통화정책수단의 활용과 대규모 자산매입으로 인해 담보의 활용도 증가 • Asset-to-GDP 비율은 중앙은행 통화정책의 주요 지표 Central Bank's Asset-to-GDP 70 60 40 Korea Japan 30 China 20 United States 10 0 19 91 19 92 19 93 19 94 19 95 19 96 19 97 19 98 19 99 20 00 20 01 20 02 20 03 20 04 20 05 20 06 20 07 20 08 20 09 20 10 20 11 20 12 20 13 20 14 20 15 20 16 Axis Title 50 Thailand

안정적인 금융구조에 필요한 담보의 중요성 자료: “Realizing Indonesia’s Economic Potential”(Bruer, Luies E. et al. , 2018), 저자 수정

ABMI Open Exchange, Clearing and Settlement Services for Comprehensive Asset Categories Cross-Border Settlement Infrastructure (CSIF) Collateral datasets, haircuts, etc APCF Expand Core ABMI Capacities Comprehensive Credit Guarantee

COFFEE BREAK

Thank you