Semiconductor Industry in Taiwan China Dec 2004 Agenda

• 無晶圓廠的設計公司 (Fabless IC Design House) •")

的商業模式 Traditional IDM (Integrated Device Manufacturing) Intellectual Property R&D Design Mask Wafer Fabrication Packaging")

Labor-Intensive")

• Y 2 K")

- Slides: 33

Semiconductor Industry in Taiwan & China Dec, 2004

Agenda • Semiconductor Industry • IDM, Foundry & fabless design house • Silicon wafer industry • Semiconductor in Taiwan • Semiconductor in China • Page

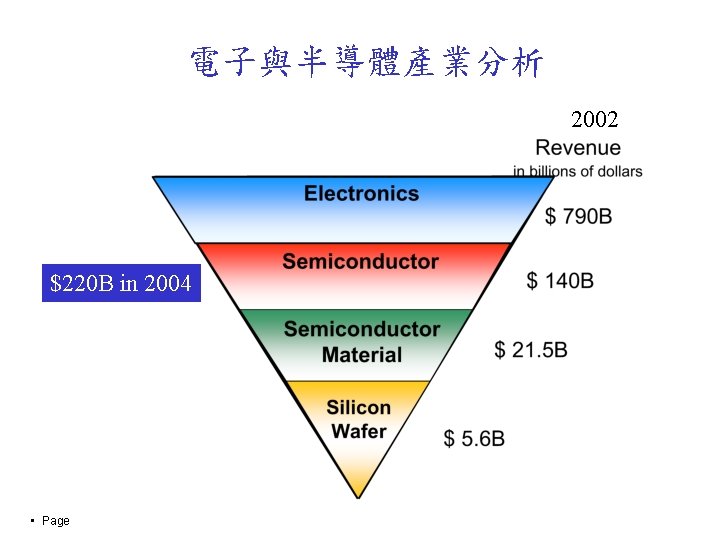

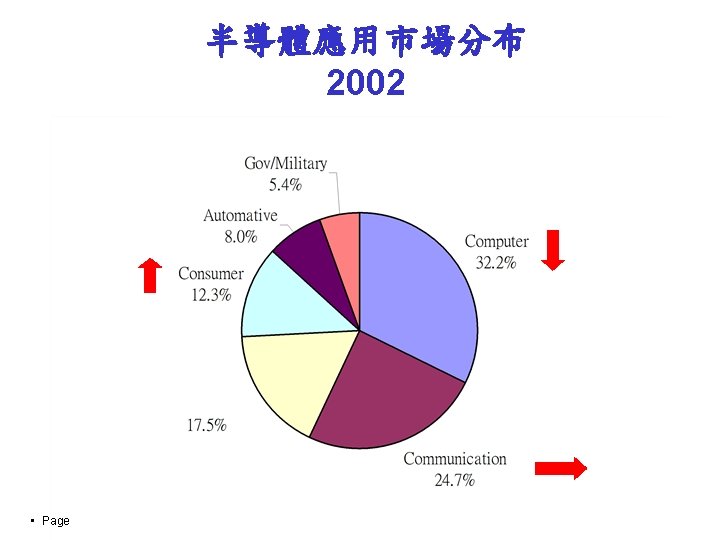

Semiconductor Industry

Semiconductor Sales - Yo. Y % Growth 32% in 2004 0~10% in 2005 • Page

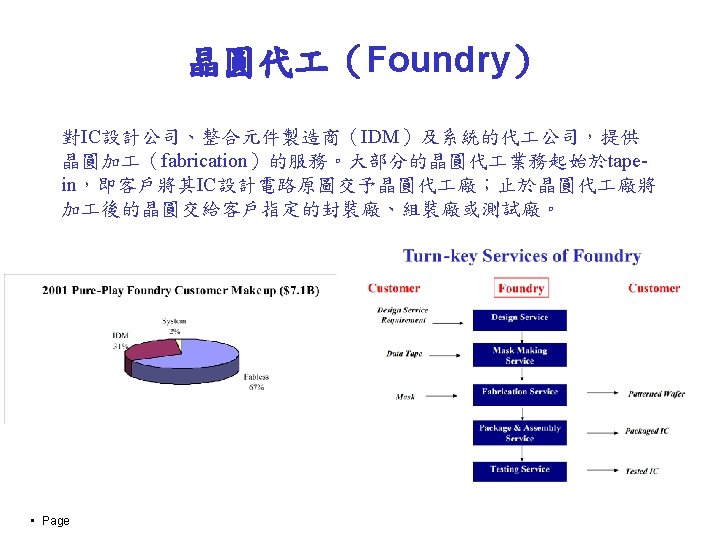

Semiconductor Industry • 整合元件製造商(Integrated Device Manufacturer, IDM) • 無晶圓廠的設計公司 (Fabless IC Design House) • 晶圓代 (Foundry) • 專業晶圓代 (Pure-play Foundry) • Page

整合元件製造商(IDM)的商業模式 Traditional IDM (Integrated Device Manufacturing) Intellectual Property R&D Design Mask Wafer Fabrication Packaging Test Logistics New IDM Distribution Marketing Brand Recognition • Page

What powers foundry growth • Page

Silicon Wafer

Silicon Wafers Substrate for virtually all semiconductor devices Polysilicon Ingot Slicing Polishing Epitaxial Shipping Wafer Size Progression • Page 1960 1964 1973 1979 1985 1991/2000 . 525 in 1 in 3 in 5 in/125 mm 8 in/200 mm 12 in/300 mm

Diameter life cycle • Page

Silicon Wafer Industry Market Share By Competitor 27% 17% 9% 8% 22% 1. Outside of Japan, top 4 are almost same share, ~20%. 2. MEMC is the #1 wafer supplier to pure-play foundry fabs. • Page

Company Overview • Formed in 1959 by Monsanto • In 2003, sales forecast is $800 M. Predicted revenue in 2004 will be $1 B. • 4, 700 employees worldwide as of end 2002 • Globally diverse manufacturing and technology capabilities • Strong customer base. Sales to 23 of top 25 semiconductor companies worldwide • Customer base is diverse with sales in industry segments such as: Analog, ASIC’s, Discrete, Memory, and MPU/MCU • Page

MEMC Manufacturing Locations 20% JV with Samsung Headquarters St. Peters MEMC STP Chonan MKC Utsunomiya MJL Novara/Merano Pasadena Sherman MEMC SW 20% JV with TI MEMC Italy Hsinchu Taisil Kuala Lumpur MEMC KL • Page

Semiconductor Industry in Taiwan

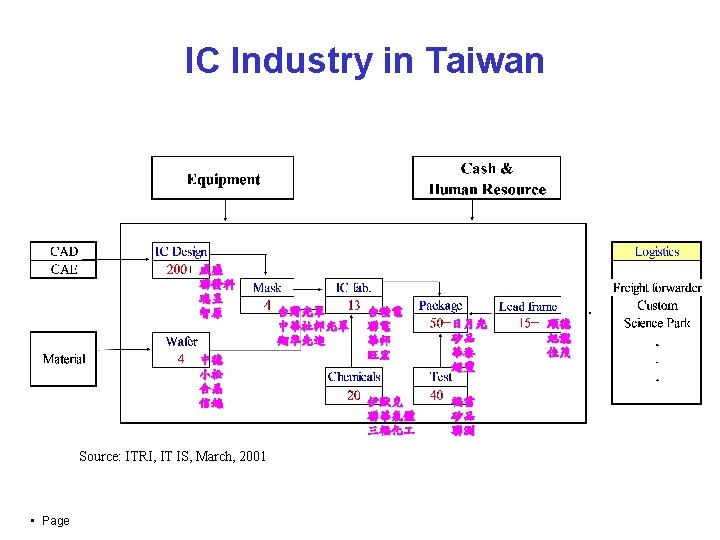

Taiwan IC fab 2004 • Page

Wafer Consumption in Taiwan -by Diameters • Page

Competitiveness of Taiwan’s Enterprises Willingness of Risk-taking Efficiency of Mass Production • Page Ability of Dynamics Management Effectiveness of Logistics Implementation

#1 in the World - Made in Taiwan • • Page Small & Medium-size Companies Specialized Parts/Subsystems Manufacturers Cost & Quality Control Given Dynamic Integration Quick Decisions Fast Responses Flexibility SPEED

Transition of Taiwan’s Economy and Industrial Structure Manufacturing-Led As percentage of GDP (%) Labor-Intensive industry GDP(USM$) 1, 614(1952) GDP/Capita(US$) 196(1952) 60% 40% Investment-Led Capital-Intensive Industry Innovation-Led Technology. Intensive Industry 48, 600(1982) 2, 654(1982) Knowledge. Intensive Industry 290, 540(1999) 13, 235(1999) 63. 9% Services Manufacturing 28. 0% 20% Agriculture 1. 8% 2000 Source : Directorate-General of Budget, Accounting and Statistics, R. O. C. , Monthly Bulletin of Earning and Productivity Statistics, Taiwan • Page

Semiconductor Industry in China

Taiwan’s Successful Experiences Taiwan successfully erodes the market with cost-effective capability. Taiwan America Japan China Europe Star Cow Product Life Cycle • Page Dog

Comparison between Taiwan and China in IC Design The Concept of IP Protection IC Design Capability Quick Response to Market Cost Effective in Software Development Driving Force in Product Standard Huge Domestic Market A Complete IC Infrastructure Taiwan • Page China

China IC fab 2004 • Page

Customer: Fab in China SMIC-BJ 300 mm SGNEC 150 mm SMIC-TJ 200 mm SMIC-SHA 200 mm HHNEC 200 mm GSMC 200 mm ASMC 125/150/200 mm SBM 100 mm HJT 200 mm CSMC 150 mm Sino. MOS 150 mm • Page

IC Industry in China Source: ITRI, IT IS, March, 2001, JH 2004 updated • Page

China vs. Taiwan • Page Next 5 years: 1. 12” fabs in TWN, CMOS, high-end foundry & DRAM 2. 8” fabs in TWN, CMOS, general-purpose foundry 3. 8” fabs in China, CMOS, general-purpose foundry 4. 6” fabs in China, bipolar, Bi. CMOS, high voltage foundry

China Market • 1. 4 B population • Small opportunity x 1. 3 B = Huge business • Big problem /1. 3 B = No problem • City Island Economic • Shanghai is not China. • Beijing is different to Shanghai. • No economic meaning in country site. • After all, China is a communist country. • Page

Silicon cycle • Momentum of last cycle (3 Q/99~4 Q/00) • Y 2 K effect: PC/NB replacement, Wintel upgrade, more DRAM…. . • Booming cell phone market • Momentum of this cycle (2 Q/03~3 Q/04) • PC/NB replacement, Window XP upgrade, more DRAM…. . • New cell phone: color screen, camera…… • New consumer system: DVD, DSC…. . • Momentum of next cycle (3 Q/05~4 Q/06) • Digital TV: LCD panel, cheaper & bigger, home entertainment…. • New cell phone: ipot + PDA © 2003 Gartner, Inc. and/or its Affiliates. All Rights Reserved.