MAJORITY RULE PROTECTING MINORITY INTERESTS Talk 24 LAW

Obligations of Corporate Management")

")

strict rules with respect to")

question is what is the duty of directors to their corporation")

")

in Maple Leaf Foods Inc. v. Schneider Corp.")

3 B. L. R. (2 d)")

3 O. R. (3 d) 289 (C.")

, 39 O. R. (3")

![Limitations: Gold Reefs Of West Africa, Ltd. [1900 -1903] All E. R. Rep. 746](https://slidetodoc.com/presentation_image_h2/5ddb2f276ee97c96383ef812bae2b820/image-36.jpg "Limitations: Gold Reefs Of West Africa, Ltd. [1900 -1903] All E. R. Rep. 746")

![Confirmed in Greenhalgh v. Arderne Cinemas Ltd. [1950] 2 ALL E. R. 1120 (Eng.](https://slidetodoc.com/presentation_image_h2/5ddb2f276ee97c96383ef812bae2b820/image-37.jpg "Confirmed in Greenhalgh v. Arderne Cinemas Ltd. [1950] 2 ALL E. R. 1120 (Eng.")

: A shareholder may apply to the court for an")

(a) directing or prohibiting any act, (b) regulating the conduct")

varying or setting aside a resolution, (l) requiring the company, within a time")

If a company or its")

: A complainant may, with leave of the court, prosecute")

: The court may grant leave under section")

regarding")

60 Alta. L. R. (2")

![“In the case of the application under s. 232, [derivative action] the applicant was](https://slidetodoc.com/presentation_image_h2/5ddb2f276ee97c96383ef812bae2b820/image-49.jpg "“In the case of the application under s. 232, [derivative action] the applicant was")

actions.")

2 O. R. 132 (Ont. C. A. ) Among the")

, 7 O. R. (2 d) 216 The Ontario")

![Westfair Foods Ltd. v. Watt [1991] A. J. No. 321 • Westfair Foods Ltd.](https://slidetodoc.com/presentation_image_h2/5ddb2f276ee97c96383ef812bae2b820/image-54.jpg "Westfair Foods Ltd. v. Watt [1991] A. J. No. 321 • Westfair Foods Ltd.")

![Classic statement of Lord Wilberforce in Ebrahimi v. Westbourne Galleries Ltd. [1973] A. C.](https://slidetodoc.com/presentation_image_h2/5ddb2f276ee97c96383ef812bae2b820/image-57.jpg "Classic statement of Lord Wilberforce in Ebrahimi v. Westbourne Galleries Ltd. [1973] A. C.")

98 D. L. R. (4 th) 509")

64 O. R. (3")

The term “oppression” connotes an inequality of bargaining power while “unfairness” connotes an")

Where expectations are apparently reasonable on their face but where there is a")

Was the impugned conduct outside the range of reasonable business judgment? (2) Was")

Actual or material loss is not a prerequisite to a finding either of")

![And one last time, BCE Inc. v. 1976 Debentureholders [2008] 3 S. C. R.](https://slidetodoc.com/presentation_image_h2/5ddb2f276ee97c96383ef812bae2b820/image-66.jpg "And one last time, BCE Inc. v. 1976 Debentureholders [2008] 3 S. C. R.")

![Mc. Lachlin C. J. “[84] To establish oppression, the shareholder must show: (1) a](https://slidetodoc.com/presentation_image_h2/5ddb2f276ee97c96383ef812bae2b820/image-69.jpg "Mc. Lachlin C. J. “[84] To establish oppression, the shareholder must show: (1) a")

Thoughts 1. Corporate cases should require leave of the court to proceed, otherwise")

- Slides: 82

MAJORITY RULE & PROTECTING MINORITY INTERESTS Talk 24 LAW 459 003 BUSINESS ORGANIZATIONS Allard School of Law, UBC Fall, 2016 Jon Festinger Q. C. Festinger Law & Strategy http: //bizorg. allard. ubc. ca @jonfestinger jon@fblawstrategy. com

Happy November 30 LAW 459 003 BUSINESS ORGANIZATIONS 28 years ago today Kohlberg Kravis Roberts & Co. buys RJR Nabisco for $25. 07 billion USD.

Evaluations Online at https: //eval. ctlt. ubc. ca/law until Monday December 5 @ 11: 59 PM

Not Lecture Capture Wednesday

AFRAID YOU HAVE TO BRING YOUR OWN STATUTES

Office “Hours” during exams Email me & am happy to come to Allard: jfestinger@telus. net Skype: jon. festinger Phone: o. 604 -568 -9192 c. 604 -837 -6426

Exam Time, Timing Etc. • Monday December 12, 2016 - 9 AM, Room ? ? ? • 3. 5 Hours (Reading time of 30 minutes very highly recommended). • According to the Examination and Grading Rules the average shall be in the 70 -74. 0000% range.

Unit 8: What you need to know… • BCBCA sections 227 -228, 231 -236; [CBCA section 241] • What is the “oppression” remedy (s. 227 & 228) and it’s mechanics? • Enforcement of duty to file records (s. 231) • What is a “derivative action” (s. 232 -236) & what are it’s mechanics? • Robak Industries Ltd. v. Gardner 2007 BCCA 61

Footnote*

QUESTIONS? DISCUSSION?

Now Back to Our Regularly Scheduled Programming…

Finishing…. Unit 7: The (Fiduciary) Obligations of Corporate Management

2 Duties of Directors in Duty of care of directors and officers 122 (1) Every director and officer of a corporation in exercising their powers and discharging their duties shall (a) act honestly and in good faith with a view to the best interests of the corporation; and (b) exercise the care, diligence and skill that a reasonably prudent person would exercise in comparable circumstances. (a) = The Fiduciary Duty (b) = The Duty of Care

Hint… Note the tendency towards strict enforcement of (relatively) strict rules with respect to fiduciary obligations (as opposed to “duty of care” ones). Are strict standards objective or are they a substitute for objectivity? Ducks in a row

TAKE-OVER BIDS

The (multi-million dollar) question is what is the duty of directors to their corporation when confronted with a take-over? And do the directors owe any duties to shareholders?

Principles of Olympia & York • When directors act in the best interests of the company and in good faith, it matters not that they also benefit from their action (in this case by becoming more entrenched in the company). In other words self-entrenchment will not necessarily be inferred where retaining control is secondary to the more important purpose of acting in good faith and in the company best interests. • It is the duty of the directors in a take-over battle to take all reasonable steps to maximize shareholders value. In maximizing shareholder value directors may rely on professional advice as to the adequacy of a bid, and that such reliance will be evidence of acting in good faith and on reasonable grounds.

Difference between… Taking reasonable steps to maximize shareholders value in the context of the best interests of the company & Directors obligation where a company is for sale to conduct an auction of the company’s shares.

The Revlon Principle (NOT OUR LAW)

“However, when Pantry Pride increased its offer to $50 per share, and then to $53, it became apparent to all that the break up of the company was inevitable. The Revlon board’s authorization permitting management to negotiate a merger or buyout with a third party was a recognition that the company was for sale. The duty of the board had thus changed from the preservation of Revlon as a corporate entity to the maximization of the company’s value at a sale for the stockholders’ benefit. This significantly altered the board’s responsibilities. . . It no longer faced threats to corporate policy and effectiveness, or to the stockholders’ interests, from a grossly inadequate bid. The whole question of defensive measures became moot. The directors’ role changed from defenders of the corporate bastion to auctioneers charged with getting the best price for the stockholders at a sale of the company. ”

“Revlon Duty” rejected (for Ontario? ) in Maple Leaf Foods Inc. v. Schneider Corp. (1998) 42 O. R. (3 d) 177 (Ont. C. A. ) “…[Revlon] stands for the proposition that if a company is up for sale, the directors have an obligation to conduct an auction of the company’s shares. Revlon is not the law in Ontario. In Ontario, an auction need not be held every time there is a change in control… An auction is merely one way to prevent the conflicts of interest that may arise when there is a change of control by requiring that directors act in a neutral manner toward a number of bidders…The more recent Paramount decision in the United States…has recast the obligation of directors when there is a bid for change of control as an obligation to seek the best value reasonably available to shareholders in the circumstances. This is a more flexible standard, which recognizes that the particular circumstances are important in determining the best transaction available, and that a board is not limited to considering only the amount of cash or consideration involved…”

Page 407 of the textbook… “One way to make sense of this is that the Supreme Court of Canada’s interpretation in BCE v. 1976 Debentureholders …of the duty of loyalty is such that directors may consider the interests of creditors and other stakeholders, but not that they must do so. Moreover, the rejection of Revlon can also be understood as the rejection of an idea that directors are confined to a short time frame when deciding what is in the best interests of the corporation. ”

Contextualizing the duty of loyalty

347883 Alberta Ltd. v. Producers Pipelines Inc. (1991) 3 B. L. R. (2 d) 237 (C. A. ) • Dealt with a “shareholder’s rights agreement” AKA a poison pill defence, a defensive strategy against corporate takeovers. • A poison pill can be defined as an extra-ordinary manoeuvre by the directors and/or shareholders of the company to be acquired designed to make that target company less attractive to the hopeful acquirer, often by adding burdensome costs if the takeover succeeds. • In 347883 Alberta Ltd. v. Producers Pipelines Inc. the directors of Producers Pipelines Inc. , a public company that the parent company of 347883 Alberta Ltd. wished to acquire, enacted a “shareholders rights agreement”. The shareholders rights agreement was crafted in such a way that 347883 Alberta Ltd. (as a subsidiary of the putative acquirer) would not receive these rights and 347883’s own shares would be greatly diluted.

Sherstobitoff J. A. reviewed the state of the law and concluded: “In summary, when a corporation is faced with susceptibility to a take over bid or an actual take over bid, the directors must exercise their powers in accordance with their overriding duty to act bona fide and in the best interests of the corporation even though they may find themselves, through no fault of their own, in a conflict of interest situation. If, after investigation, they determine that action is necessary to advance the best interests of the company, they may act, but the onus will be on them to show that their acts were reasonable in relation to the threat posed and were directed to the benefit of the corporation and its shareholders as a whole, and not for an improper purpose such as entrenchment of the directors. Since the shareholders have the right to decide to whom and at what price they will sell their shares, defensive action must interfere as little as possible with that right. Accordingly, any defensive action should be put to the shareholders for prior approval where possible, or for subsequent ratification if not possible…Defensive tactics that result in shareholders being deprived of the ability to respond to a takeover bid or to a competing bid are unacceptable. ” The Ontario C. A. set aside the shareholder’s rights agreement.

Brant Investments Ltd. v. Keeprite Inc. (1991) 3 O. R. (3 d) 289 (C. A. ) • Complex corporate transaction where the board of the parent Inter. City Gas purchased 64% of the shares in Keep. Rite Inc. Then Inter. City transferred the shares it had acquired in Keeprite to Inter-City Manufacturing, a subsidiary of Inter-City Gas. Following the recommendation of an independent committee of the board of Keep. Rite Inc. , Keep. Rite Inc. purchased $20 million of assets from two companies that were subsidiaries of Inter-City Manufacturing. An issue of rights to existing shareholders financed the purchase. This rights offering required an amendment to the articles of Keep. Rite Inc. that was passed by a special resolution of the shareholders. • The minority shareholders of Keeprite Inc. objected to the transaction, and brought an oppression action. • Essentially a transaction where the board of a parent proposed to purchase the assets of a subsidiary, and the shareholders of the parent company objected. • Mc. Kinlay J. A. found that now section 241 of the CBCA was not offended by the actions of Keep. Rite Inc. Accordingly the action of the minority shareholders against the company failed.

Mc. Kinlay J. A. : “There can be no doubt that on application under s. 234 the trial judge is required to consider the nature of the impugned acts and the method in which they were carried out. That does not mean that the trial judge should substitute his own business judgment for that of managers, directors, or a committee such as the one involved in assessing this transaction. Indeed, it would generally be impossible for him to do so, regardless of the amount of evidence before him…In short, he does not know enough to make the business decision required. That does not mean that he is not well equipped to make an objective assessment of the very factors which s. 234 requires him to assess. It is important to note that the learned trial judge did not say that business decisions honestly made should not be subjected to examination. What he said was that they should not be subjected to microscopic examination…”

Independent Committees “protect”? ? ? • Brant Investments Ltd. v. Keep. Rite Inc. illustrates the sense of “protection” (real or imagined) that “independent committees” can provide in a corporate setting, particularly in a takeover scenario. • The key seems to be the appearance of objectivity and focus which an independent committee can bring to business judgments regarding “the best interests” of the corporation. • It has become fairly standard practice for independent committees to be convened at the early stages of takeover issues (and others as well) that might prove contentious.

CW Shareholdings Inc. v. WIC Western International Communications Ltd. (1998), 39 O. R. (3 d) 755 (Ont. SC) • Can. West Global wished to acquire all of the shares of WIC at a price of $39 per share. • WIC’s board created a “special committee” to consider the offer. • WIC’s board then recommended that the shareholders not accept Can. West’s offer and passed without the approval of its shareholders a “shareholders rights plan”. • The Ontario Securities Commission identified challenges with the non-independence of WIC’s “special committee” relating to the participation of John Lacey, the CEO of WIC and of Robert Manning, a WIC Director who represented the largest holder of WIC Class A shares, and who was allowed to attend meetings of the special committee, but without voting rights…

The OSC’s position: “From the evidence… it appears clear to us that the Special Committee was set up for purposes of convenience only, and not as an independent committee. In our view, in a take over bid context a committee which includes as an active participant the president and [CEO] of the corporation and a representative of a shareholder which has 50% of the votes, is not an independent committee… In these circumstances, it is our view that we must place less reliance on the review by the Special Committee of the Bid, and possible alternative methods of achieving a more beneficial result to shareholders, than we would if the Special Committee had been truly an independent committee. ”

Mr. Justice Blair saw things differently: “The law as it relates to the general duties of the directors of Canadian corporations is not controversial. The directors must exercise the common law fiduciary and statutory obligations (a) to act honestly and in good faith with a view to the best interests of the corporation, and (b) in doing so, to exercise the care, diligence and skill that a reasonably prudent person would exercise in comparable circumstances…In the context of a hostile takeover bid situations where the corporation is “in play”… the duty is to act in the best interests of the shareholders as a whole and to take active and reasonable steps to maximize shareholder value by conducting an auction… In assessing whether or not directors have met their fiduciary and statutory obligations…Canadian courts have generally approached the subject on the basis of what has become known as the “business judgment rule”. This rule is an extension of the fundamental principle that the business and affairs of a corporation are managed by or under the direction of its board of directors…

…In such cases, the board’s decisions will not be subject to microscopic examination and the Court will be reluctant to interfere and to usurp the board of director’s function in managing the corporation… The directors’ actions are not to be judged against the perfect vision of hindsight, and should be measured against the facts as they existed at the time the impugned decision was made. In addition, the court should be reluctant to substitute its own opinion for that of the directors where the business decision was made in reasonable and informed reliance on the advice of financial and legal advisors appropriately retained and consulted in the circumstances…”

QUESTIONS? DISCUSSION?

MAJORITY RULE & PROTECTING MINORITY INTERESTS

Majority Rule • There must be Annual Meetings of the Shareholders • There can be Special Meetings of the Shareholders to deal with nonordinary matters (“extraordinary”) like conflict of interest contracts, fundamental changes, by-law amendments etc.

Limitations: Gold Reefs Of West Africa, Ltd. [1900 -1903] All E. R. Rep. 746 (Eng. C. A. ) • Gold Reefs altered its articles giving itself a lien on paid up shares which, in effect, addressed the failure of a shareholder, Mr. Zuccani, to pay what was owed in respect of other shares he had that had not been fully paid up. • Zuccani died and executor sued to get the full value of Zuccani’s shares without discount. • Lindley M. R. : “ The power thus conferred on companies to alter the regulations contained in their articles is limited only by the provisions contained in the statute and the conditions contained in the company’s memorandum of association… I can discover no ground for judicially putting any other restrictions on the power conferred by the section than those contained in it. How’s shares shall be transferred, and whether the company shall have any lien on them, are clearly matters of regulation properly prescribed by a company’s articles of association…”

Confirmed in Greenhalgh v. Arderne Cinemas Ltd. [1950] 2 ALL E. R. 1120 (Eng. C. A. ). • Articles of Arderne Cinemas provided that no sale of shares to an outsider would occur. • Majority shareholder, Mr. Mallard wanted to sell control of Arderne Cinemas Ltd. to a third party. Mr. Greenhalgh was a minority shareholder. • The articles of Arderne Cinemas Ltd. were amended by special resolution to permit sale to an outsider, if approved, by simple majority. • Mr. Greenhalgh argued that the article change was invalid.

Evershed M. R. - “hands off” “…It is therefore not necessary to require that persons voting for a special resolution should, so to speak, dissociate themselves altogether from their own prospects and consider whether what is thought to be for the benefit of the company as a going concern. If, as commonly happens, an outside person makes an offer to buy all the shares, prima facie, if the corporators think it a fair offer and vote in favour of the resolution, it is no ground for impeaching the resolution that they are considering their own position as individuals. ”

Is this the shareholder rights “movement” ?

Minority Protections: OPPRESSION BCBCA 227(2): A shareholder may apply to the court for an order under this section on the ground (a) that the affairs of the company are being or have been conducted, or that the powers of the directors are being or have been exercised, in a manner oppressive to one or more of the shareholders, including the applicant, or (b) that some act of the company has been done or is threatened, or that some resolution of the shareholders or of the shareholders holding shares of a class or series of shares has been passed or is proposed, that is unfairly prejudicial to one or more of the shareholders, including the applicant. (3) On an application under this section, the court may, with a view to remedying or bringing to an end the matters complained of and subject to subsection (4) of this section, make any interim or final order it considers appropriate, including an order…

…including an order… (con’d) (a) directing or prohibiting any act, (b) regulating the conduct of the company’s affairs, (c) appointing a receiver or receiver manager, (d) directing an issue or conversion or exchange of shares, (e) appointing directors in place of or in addition to all or any of the directors then in office, (f) removing any director, (g) directing the company, subject to subsections (5) and (6), to purchase some or all of the shares of a shareholder and, if required, to reduce its capital in the manner specified by the court, (h) directing a shareholder to purchase some or all of the shares of any other shareholder, (i) directing the company, subject to subsections (5) and (6), or any other person, to pay to a shareholder all or any part of the money paid by that shareholder for shares of the company, (j) varying or setting aside a transaction to which the company is a party and directing any party to the transaction to compensate any other party to the transaction,

(k) varying or setting aside a resolution, (l) requiring the company, within a time specified by the court, to produce to the court or to an interested person financial statements or an accounting in any form the court may determine, (m) directing the company, subject to subsections (5) and (6), to compensate an aggrieved person, (n) directing correction of the registers or other records of the company, (o) directing that the company be liquidated and dissolved, and appointing one or more liquidators, with or without security, (p) directing that an investigation be made under Division 3 of this Part, (q) requiring the trial of any issue, or (r) authorizing or directing that legal proceedings be commenced in the name of the company against any person on the terms the court directs. NOTE that injunctive relief is available through CBCBA 228

BCBCA Enforcement of duty to file records 231 (1) If a company or its receiver, receiver manager or liquidator has failed to file with the registrar any record required to be filed with the registrar under this Act, any director, shareholder or creditor of the company may provide, to the person required to submit the record to the registrar for filing, notice requiring that person to file the record with the registrar. (2) If the person required to file a record with the registrar under subsection (1) fails to file the record with the registrar within 14 days after receiving the notice referred to in subsection (1), the court may, on the application of any director, shareholder or creditor of the company, (a) order the person to file the record with the registrar within the time the court directs, and (b) direct that the costs of and incidental to the application be paid by the company, by any director or officer of the company or by any other person the court considers appropriate. (3) Neither the making of an order by the court under this section nor compliance with such an order relieves a person from any other liability.

Derivative actions BCBCA 232 (2): A complainant may, with leave of the court, prosecute a legal proceeding in the name and on behalf of a company (a) to enforce a right, duty or obligation owed to the company that could be enforced by the company itself, or (b) to obtain damages for any breach of a right, duty or obligation referred to in paragraph (a) of this subsection. (3) Subsection (2) applies whether the right, duty or obligation arises under this Act or otherwise. (4) With leave of the court, a complainant may, in the name and on behalf of a company, defend a legal proceeding brought against the company.

Granting leave for a derivative action 233(1): The court may grant leave under section 232 (2) or (4), on terms it considers appropriate, if (a) the complainant has made reasonable efforts to cause the directors of the company to prosecute or defend the legal proceeding, (b) notice of the application for leave has been given to the company and to any other person the court may order, (c) the complainant is acting in good faith, and (d) it appears to the court that it is in the best interests of the company for the legal proceeding to be prosecuted or defended.

WHO CAN BRING A DERIVATIVE OR OPPRESSION ACTION? • BCBCA section 232 (1) regarding derivative actions defines “complainant” as “in relation to a company, a shareholder or director…” • BCBCA section 227(1) regarding oppression defines “shareholder” • Both sections provide that their respective action can be brought by “any other person whom the court considers to be an appropriate person…”

First Edmonton Place Ltd. v. 315888 Alberta Ltd. (1988) 60 Alta. L. R. (2 d) 122 (Q. B. ) • Question was whether a creditor of the company was a proper person to be a complainant in the opinion of the court under the Alberta Business Corporations Act? • Note first, that the definition of complainant in that case applies to both oppression and derivative actions. • A landlord (First Edmonton Place) sued three lawyers through the lawyers own company (315888 Alberta Ltd. ) for an alleged debt arising from the occupancy of the landlord’s premises.

Mc. Donald J. : “There are two circumstances in which justice and equity would entitle a creditor to be regarded as “a proper person”. (There may be other circumstances; these two are not intended to exhaust the possibilities. ) The first is if the act or conduct of the directors or management of the corporation which is complained of constituted using the corporation as a vehicle for committing a fraud upon the applicant… Second, the court might hold that the applicant is a “proper person to make an application” for an order under s. 234 [oppression] if the act or conduct of the directors or management of the corporation which is complained of constituted a breach of the underlying expectation of the applicant arising from the circumstances in which the applicant’s relationship with the corporation arose. ”

“In the case of the application under s. 232, [derivative action] the applicant was not a holder of a security or a “creditor” at the time of use of the cash inducement money by the three directors. However, there is some evidence that the cash inducement money was not used for purposes of the corporation and that its use might have been a fraud upon the corporation. If it was a fraud upon the corporation, and if the corporation were entitled to recover the money from the three directors, the applicant may have a genuine interest in advancing the claim to such recovery because the corporation might be liable in damages to the applicant. Therefore the applicant is in my opinion a proper person to make an application under s. 232 and should be granted leave to bring an action in the name and on behalf of the corporation… Moreover, as for the three lawyers, as directors of the corpora tion, permitting themselves as lawyers to occupy the leased premises without paying rent or entering into a lease, whether that conduct constituted a wrong to the corporation is a matter that should be tried.

Other notes… • Also see BCE v. 1976 Debentureholders on derivative (aka representative) actions. • Per Shield Development Co. v. Snyder, [1976] 3 W. W. R. 44 (B. C. S. C. ) the B. C. statute limits common law “derivative” actions: “The legislation does not expressly prohibit the bringing of a common law derivative action but, in my view, such an action is prohibited by necessary implication. I am unable to see how the two remedies could exist side by side without creating confusion to an intolerable degree. ”

Farnham v. Fingold (1973) 2 O. R. 132 (Ont. C. A. ) Among the first Canadian cases to distinguish between a personal action and a derivative action… Jessup J. A. stated: “Certain parts of the statement of claim in particular all or parts of paras. 22, 23, 29, 32, 34, 36 and 37 E are concerned with rights, duties or obligations owed to the defendant Slater Steel Industries Limited or with damage alleged to be suffered by the corporation as a result of the actions of the other defendants. Such matters are properly the subject of a derivative action rather than a class action. ”

Goldex Mines Ltd. v. Revill (1974), 7 O. R. (2 d) 216 The Ontario Court of Appeal dealt with the distinction between derivative actions and oppression claims: “Where a legal wrong is done to shareholders by directors or other shareholders, the injured shareholders suffer a personal wrong, and may seek redress for it in a personal action. That personal action may be by one shareholder alone, or (as will usually be the case) by a class action in which he sues on behalf of himself and all other shareholders in the same interest (usually, all other shareholders save the wrongdoers). Such a class action is nevertheless a personal action. A derivative action, on the other hand, is one in which the wrong is done to the company. It is always a class action, brought in representative form, thereby binding all the shareholders…”

What is Oppression? Nelson Mandela’s prison cell on Robben Island

Westfair Foods Ltd. v. Watt [1991] A. J. No. 321 • Westfair Foods Ltd. had Class A shares carrying a $2 dividend in priority to the common shares. • There were many Class A shareholders and only a single holder of the common shares. • The Class A shares were also entitled to share in surplus assets including retained earning in the event of a liquidation. • Historically all profits beyond the dividend attached to the class A shares would be retained by Westfair Foods Ltd. as earnings. At a certain point the directors of Westfair Foods Ltd. decided to change the policy and the company started paying all of its net earnings to the single common shareholder. • The Class A shareholders claimed the new policy was oppressive to their interests. • Kearns J. A. of the Alberta C. A. found the new policy to be oppressive to the Class A shareholders…

“I cannot put elastic adjectives like “unfair”, “oppressive” or “prejudicial” into watertight compartments. In my view, this repetition of overlapping ideas is only an expression of anxiety by Parliament that one or the other might be given a restrictive meaning… Having concluded that the words charge the courts to impose the obligation of fairness on the parties, I must admit that the admonition offers little guidance to the public, and Parliament has left elucidation to us… We fail in that duty of elucidation, I think, if we merely say “this is fair” or “that is not fair” without ever explaining why we think this or that is fair. Thus I…am not much helped by cases and comments that simply announce that I am to enforce “fair play” or “fair dealing”…I do not understand that the delegation of this duty permits a judge to impose personal standards of fairness.

The company and the shareholders entered voluntarily, not by duty or chance, into a relationship. Our guides are the rules in other contexts, such as contract law, equity, and partnership law, where the courts have also considered just rules to govern voluntary relationships. In very general terms, one clear principle that emerges is that we regulate voluntary relationships by regard to the expectations raised in the mind of a party by the word or deed of the other, and which the first party ordinarily would realize it was encouraging by its words and deeds. This is what we call reasonable expectations, or expectations deserving of protection… I do not…suggest that analysis about expectations deserving protection is the sole basis for rules under the statute. I think, for example, of totally unforeseen windfalls or calamities. This is not such a case, but I dare say that even in those cases the expectations of the parties are a sound starting point…The test then is always facts specific, and cases decided on other facts offer only a limited guide. ”

Classic statement of Lord Wilberforce in Ebrahimi v. Westbourne Galleries Ltd. [1973] A. C. 360 “The foundation of it all lies in the words ‘just and equitable’…The words are a recognition of the fact that a limited company is more than a mere legal entity, with a personality in law of its own; that there is room in company law for recognition of the fact that behind it, or amongst it, there are individuals with rights, expectations and obligations inter se which are not necessarily submerged in the company structure. That structure is defined by the Company Act and by the articles of association by which shareholders agree to be bound. In most companies and in most contexts, this definition is sufficient and exhaustive, equally so whether the company is large or small. The ‘just and equitable’ provision does not, as the respondents suggest, entitle one party to disregard the obligation he assumes by entering a company, nor the court to dispense him from it. It does, as equity always does, enable the court to subject the exercise of legal rights to equitable considerations; considerations, that is, of a personal character arising between one individual and another, which may make it unjust, or inequitable, to insist on legal rights, or to exercise them in a particular way. ”

Deluce Holdings Inc. v. Air Canada (1992) 98 D. L. R. (4 th) 509 (Gen. Div. ) • Air Canada owned 75% of the shares of Air Ontario & De Luce Holdings Ltd. owned the remaining 25%. • The interests of both Air Canada and De Luce Holdings Ltd. were held in “ 152160 Canada Inc. ” • The board of directors of Air Ontario was comprised of 7 nominees of Air Canada and 3 nominees from De Luce. • William De Luce was president of Air Ontario. • Air Canada changed its business strategy to seek 100% control of its regional carriers. • De Luce was asked to resign by the Air Canada board representatives. He refused and was terminated by the board of Air Ontario, which in turn was controlled by Air Canada nominees.

• The “Unanimous Shareholders Agreement” of 152160 Canada Inc. governed the relationship between Air Canada and the De Luce family interests. That agreement provided Air Canada with an option to acquire the De Luce shareholdings in Air Ontario at “fair market value” upon termination either by Air Ontario or 152160 Canada Inc. of the employment of the last of William De Luce of his father Stanley De Luce. Apparently, termination could be “for any reason”. In February 1989 the employment of Stanley De Luce ended and not renewed. In October 1991 William De Luce terminated by a decision of the board of 152160 Canada Inc. • De Luce Holdings Ltd alleged oppression.

• The Court found that Air Canada’s nominee directors had too obviously disregarded the interests of other stakeholders. Whethere were sufficient reasons to terminate Mr. De Luce, it was obvious to the court that the nominee directors had failed to conduct such any legitimate and focused analysis and were in fact guided by Air Canada’s corporate agenda. This sort of behavior was deemed oppressive and in breach of the nominees’ fiduciary duty to Air Ontario. • Blair J. : “In my view, the conduct of Air Canada and its nominee directors, as outlined above, could be found, after a trial, to constitute “oppression” of Deluceco’s interests as a minority shareholder in Air Ontario. While the conduct may not constitute “oppression” in the classic sense of conduct which is “lacking in probity” or “burdensome, harsh and wrongful”, it may nonetheless be conduct which is “unfairly prejudicial” to or which “unfairly disregards” the interests of Deluceco as a minority shareholder, contrary to s. 241 of the C. B. C. A…”

Summary of principles… Killeen J. in Krynen v. Bugg (2003) 64 O. R. (3 d) 393 (S. C. J. ): “A summary of the leading principles and guiding rules…would include the following: (1) The overriding lodestar principle of oppression law is that, when determining whethere has been oppression of a shareholder, the court must determine what the reasonable expectations of that person were according to the arrangements which existed between the principals…Shareholder interests would appear to be intertwined with shareholder expectations. It does not appear to me that the shareholder expectations which are to be considered are those that a shareholder has as his own individual “wish list”. They must be expectations which could be said to have been (or ought to have been considered as) part of the compact of the shareholders.

(2) The term “oppression” connotes an inequality of bargaining power while “unfairness” connotes an obligation to act equitably and impartially in the exercise of power and authority… (3) The terms, “unfair prejudice to” and “unfair disregard of the interests of” require less rigorous tests than oppression. Where on the totality of the evidence the actions and conduct complained of go beyond mere inconvenience and lack of information, and the interests of the complainant have been unfairly disregarded, the complainant will be entitled to a remedy… (4) There is no requirement that bad faith must be shown before an order to rectify a complaint may be made in an oppression case…A useful three part test or approach has been suggested for the application of the business judgment rule:

(5) Where expectations are apparently reasonable on their face but where there is a contract dealing with these expectations, the reasonableness of these expectations cannot prevail over the contract. (6) Reasonable expectations are not necessarily “static” or frozen expectations and may evolve or change as the principals adapt their arrangements from time to time… (7) The business and affairs of a corporation are managed by or under the direction of its board of directors. The “business judgment rule” operates to shield from court intervention business decisions which have been made honestly, prudently, in good faith and on reasonable grounds. In such cases, the board’s decisions will not be subject to microscopic examination and the court will be reluctant to interfere with and usurp the board’s function in managing the corporation…A useful three part test or approach has been suggested for the application of the business judgment rule:

(1) Was the impugned conduct outside the range of reasonable business judgment? (2) Was the impugned conduct inconsistent with the reasonable expectations of the complainant? (3) Did the impugned conduct cause prejudice to the complainant The law as it has evolved in Ontario and Delaware has the common requirements that the court must be satisfied that the directors have acted reasonably and fairly. The court looks to see that the directors made a reasonable decision not a perfect decision. Provided the decision taken is within a range of reasonableness, the court ought not to substitute its opinion for that of the board even though subsequent events may have cast doubt on the board’s determination. As long as the directors have selected one of several reasonable alternatives, deference is accorded to the board’s decision…. This formulation of deference to the decision of the Board is known as the “business judgment rule”…

(8) Actual or material loss is not a prerequisite to a finding either of oppression, unfair prejudice or unfair disregard of interest. The object of the remedies available under s. 248(3) is to prevent the continuation of the misconduct in question if it is established that a harm or detriment, in the sense of infringement of rights or privileges, will follow in the absence of restraining such misconduct…Thus, in establishing unfair disregard of the applicant’s interests as a result of misconduct, there is no requirement that there be actual detriment or loss to the applicant… (9) Wrongful dismissal, standing alone, will not justify a finding of oppression. It is only where the interests of the employee are closely intertwined with his interests as a shareholder, and where the dismissal is part of a pattern of conduct to exclude the complainant from participation in the corporation, that the dismissal can be found to be an act of oppression…

And one last time, BCE Inc. v. 1976 Debentureholders [2008] 3 S. C. R. 560 approved the arrangement as fair and dismissed the claim for oppression. “What is just and equitable is judged by the reasonable expectations of the stakeholders in the context and in regard to the relationships at play. Conduct that may be oppressive in one situation may not be in another. ”

• Re-affirmed the test for an oppression remedy set out by the SCC in BCE Inc. v 1976 Debentureholders. Whethere has been an oppression is to be judged according to “the business realities” and not the “narrow legalities” of each case and what is “just” and “equitable” is judged by the reasonable expectations of the parties in the context and in regard to the relationship at play. • Accordingly, in this case, failure to comply with a technical statutory requirement was not in itself oppressive. The plaintiff did not establish that the corporation prejudiced and unfairly disregarded his interest, which in turn is very much related to the shareholder’s reasonable expectations.

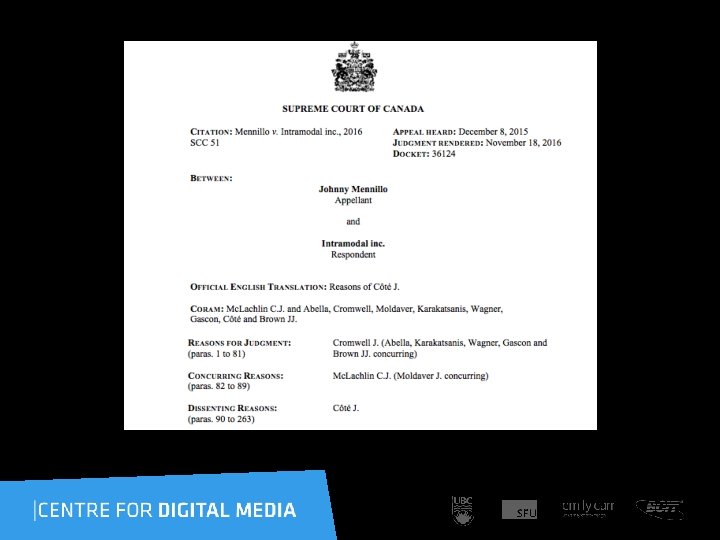

Mc. Lachlin C. J. “[84] To establish oppression, the shareholder must show: (1) a reasonable expectation that the corporation would treat him in a certain way; and (2) that the corporation breached that reasonable expectation (BCE Inc. v. 1976 Debentureholders, 2008 SCC 69, [2008] 3 S. C. R. 560, at para. 68). The action is an equitable action to protect reasonable and legitimate shareholder expectations — the “cornerstone of the oppression remedy” (BCE, at para. 61). Evidence of shareholder expectations is essential to whether conduct has been oppressive in a particular case (BCE, at para. 59; P. Martel, Business Corporations in Canada: Legal and Practical Aspects (loose leaf), at p. 31 67; D. H. Peterson and M. J. Cumming, Shareholder Remedies in Canada (2 nd ed. (loose leaf)), at §§ 17. 41 to 17. 43; D. S. Morritt, S. L. Bjorkquist and A. D. Coleman, The Oppression Remedy (loose leaf), at p. 3 2). ”

Robak Industries Ltd. v. Gardner 2007 BCCA 61 • Gardner was alleged to have conspired with others to injure John Lepinski and the company he wholly owned, Robak Industries Ltd. , by “unlawful means” including seizing control of a public company, “Getty Copper Incorporated”, and its board; discrediting and ousting Mr. Lepinski; setting aside a development agreement and acquiring 100% of Getty South a company related to Getty Copper Incorporated; “applying economic duress to Getty” and “inducing Blake Cassels & Graydon to breach their duties to Getty”. • There were also allegations of defamation in connection with the affairs of Getty Copper Incorporated. • Robak Industries Ltd. ’s claim for damages for the defamatory statements included a “loss in the value of…a substantial interest in the shares of Getty”.

Madam Justice Levine “There are good reasons for not allowing a shareholder to claim the loss in value of its shares where a wrong has been done to the company. As explained by Laskin J. A. in Meditrust (at para. 13); La Forest J. in Hercules (at para. 59), and Mc. Kenzie J. in Rogers at 78 81 (citing Prudential Assurance and Green v. Victor Talking Mach. Co. , 24 F. 2 d 378 (1928) (C. A. 2 nd Circ. )), the rule avoids a multiplicity of actions. Further, and consistent with the legal theory of Foss v. Harbottle, the loss in value of shares of a company is a loss of all of the shareholders, not just one or some of them. There is no logic that would allow only one shareholder to claim that loss, where the claim relates to wrongs done to the company, and all of the shareholders have suffered the loss in value. A single shareholder cannot claim that the loss in value of the shares, per se, is a personal, direct loss…

• Oppression claims are personal to the shareholder, while derivative claims involve harm to the company. • The substantive standard for a finding of liability is different. The issue when it comes to oppression proceeding is whether a complainant’s reasonable expectation has been inequitably violated in an oppressive or unfairly prejudicial manner. A derivative action requires proof of a legal wrong. • Oppression remedies are broad and flexible while those in derivative actions tend to be standard remedies tied to the precise cause of action. • Timing: Oppression proceedings must be brought in a timely manner, while it is not particularly a factor when it comes to derivative actions. • Leave of the court is required to commence a derivative action but not an oppression action. • Oppression claim are generally commenced by way of court petition proceeding, while derivative claims are standard civil claims.

Final (radical)Thoughts 1. Corporate cases should require leave of the court to proceed, otherwise they are diverted to arbitration A 2 J benefits 2. Mandatory ethics education of directors and managers 3. “Berne Convention” on corporate law defining a model statute that works internationally and can be adopted domestically (like copyright)

The future… Will causes of action and remedies in traditional corporate law accommodate: • Diversity on boards and in management • Pay differentials • Etc.

Nevsun Resources

The End

+ the real conundrum - not

THANK YOU!

I have “Class C” shares !