Chapter 9 Obtaining and Protecting Your Credit Learning

Chapter 9 Obtaining and Protecting Your Credit

Learning Objectives 1. Explain the concept of consumer credit 2. Describe the keys to building and maintaining healthy credit 3. Identify ways to protect your identity

Obj 1: Explain the concept of consumer credit Credit WHAT IT IS: money a lender makes available to a borrower with the understanding that the borrower will repay the money in the future The borrower agrees to pay the lender interest INTEREST – the price you pay for the right to use another person’s money; stated as a percentage of the amount borrowed A rental fee paid for using someone else’s money

Types of Credit Non-installment • Credit extended for a short term – 30 days or less • Consumer borrows at the time of purchase and pays off the entire amount in a short time • Issued by: department or furniture stores • Encourages immediate purchases • “ 30 days, same as cash” • Good for people who will receive money soon Installment • Allows more time to repay • Require monthly payments (car loans, mortgage, tuition) • Part of payment goes Revolving Open. End • Example: Credit cards • Users may borrow up to a preset maximum amount • You’ll be given a credit limit (established based on borrowers income, debt, and overall credit) towards the principal (total • Can be used on one purchase or many amount of money owed on • Can repay by the end of loan) month or spread payments • Interest paid every month • Span a few years • Used for expensive items over a longer time • You can continue to make new purchases while you pay off money borrowed in the past

Advantages & Disadvantages of Credit Advantages • Helps you make large purchases sooner (no saving) • Eliminates cash and checks • Helps establish good credit history (which means you may be able to borrow at a lower interest rate) Disadvantages • Can cause long-lasting and serious damage to finances • You may borrow too much and not be able to pay it back • Causes temptation to spend • High interest rates

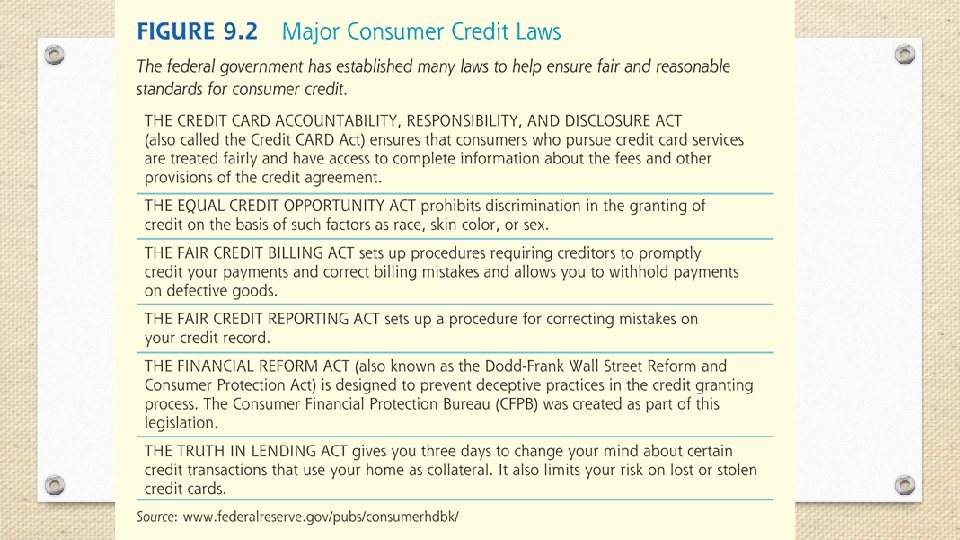

Consumer Financial Protection Bureau • Created as part of Financial Reform Act • It’s goals are to: • Regulate some aspects of online banking • Prevent deceptive practices by banks and other financial institutions • Enforce laws imposed by the Credit CARD Act

Obj 2: Describe the keys to building and maintaining healthy credit Your Credit History • Everyone’s credit history is collected and detailed in a credit report • Looks at: how many times you’ve borrowed money, did you pay it back on time, and were your payments late? • Every time you make a credit purchase, it further establishes your credit history, both good and bad • Signing up for utilities builds credit history • If you don’t pay bills in time, it’ll hurt your credit history

Credit Bureaus and Credit Scoring • Three main credit bureaus = Experian, Equifax, and Trans. Union • They provide credit reports to potential lenders, employers, and others upon request • Everyone can access their credit report once ever 12 months free of charge

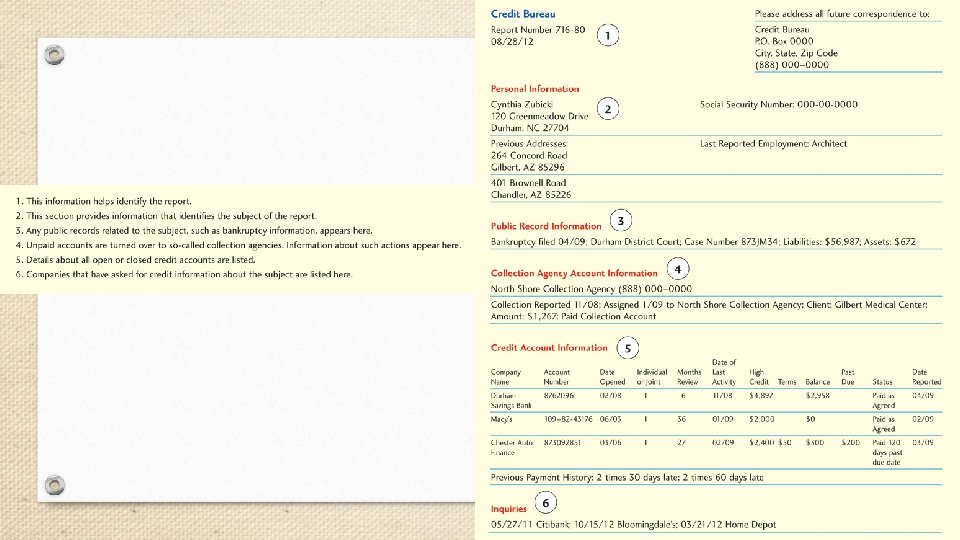

Credit Reports • Shows: • • Number of times you’ve applied for credit and if you pay on time Any unpaid accounts turned over to a collection agency The balance of each of your credit cards The names of companies that have requested credit information about you • Creditors, employers, and insurance companies all look at your credit report • Fair Credit Reporting Act: allows only firms that have a legal purpose to evaluate an individual’s credit access to this information

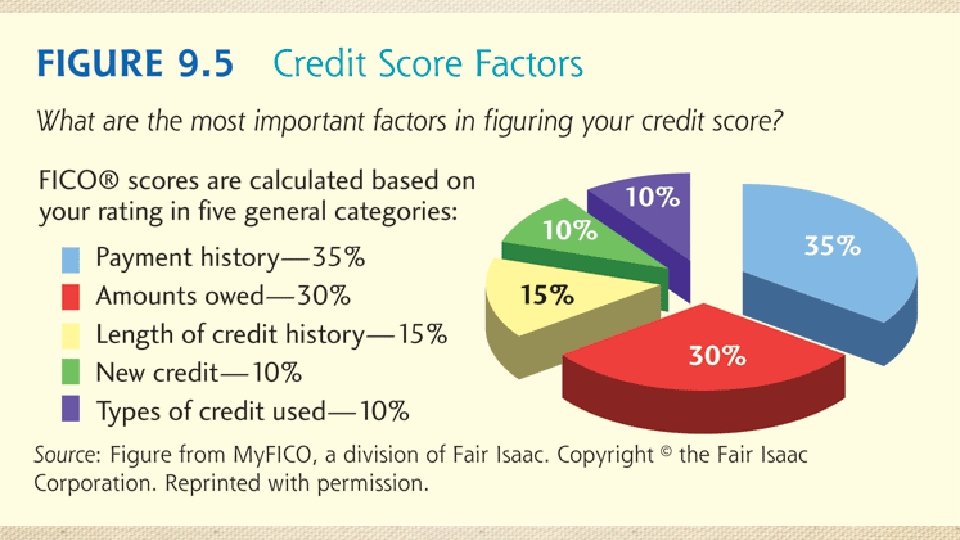

Credit Score • Individuals with HIGHER credit scores get LOWER interest rates on loans • Your credit score is created by a credit bureau • FICO credit scores are calculated on a scale of 300 to 850 • Your payment history is the most important factor in calculating your FICO score • There is also Vantage. Score which ranges from 501 to 990 • It uses a scale similar to the one used by teachers to assign grades (900 is an A, 800 is a B, and so on)

Obj 3: Identify ways to protect your identity Threats to Your Credit Identify Theft: someone uses your personal information without your permission for personal gain Shoulder Surfing: someone in a public place steals your personal information (be cautious when someone stands too close to you) Dumpster Diving: they go through your trash to gather information like credit card receipts, bank statements, or credit card offers

Skimming copying your credit/debit card number from your cards (can be employees of a retail business)

Threats to Your Credit Pretexting • someone poses as someone who needs data for one reason or another – they may act like they’re conducting a survey in order to get your information or like they work at the bank you use Pharming • using an e-mail virus to redirect you from a legitimate Web site to an illegitimate site to obtain your personal information

Phishing : online pretexting – e-mails asking you to verify account information

Basically, use common sense.

If you find inaccurate information in your credit report, you should contact the main credit reporting bureaus and file a dispute

- Slides: 19