Chapter 11 The Revenue Cycle Sales and Cash

.")

are")

- Slides: 73

Chapter 11 The Revenue Cycle: Sales and Cash Collections UAA – ACCT 316 Accounting Information Systems Dr. Fred Barbee

A Brief Overview of Transaction Cycles

A Transaction Cycle is. . . A group of related business activities (transactions).

Transaction Cycles for a Manufacturing Firm

Materials Plant Customers Cash Fin. Goods Cash Labor EXPENDITURE CYCLE CONVERSION CYCLE REVENUE CYCLE Subsystems Purchasing & A/P Cash Disbursements Payroll Subsystems Production Planning and Control Cost Accounting Subsystems Fin. Goods Cash Sales Order Processing and Cash Receipts

Transaction Cycles for a Merchandising Firm

Merchandising Shipments Sale of Merchandise Cash Receipts GL & Fin Rpt Cycle Purchase of Mdse, & Labor, Etc. The Revenue Cycle Merchandise Receipts PP&E, Investments Cash Disbursements

Merchandising Shipments Sale of Merchandise The Expenditure Cash Receipts Cycle GL & Fin Rpt Cycle Purchase of Mdse, & Labor, Etc. PP&E, Investments Cash Disbursements Merchandise Receipts

Merchandising Shipments Sale of Merchandise Cash Receipts The Finance GL & Cycle Fin Rpt Cycle Purchase of Mdse, & Labor, Etc. PP&E, Investments Cash Disbursements Merchandise Receipts

GL & Financial Reporting Merchandising Shipments Sale of Merchandise Cash Receipts GL & Fin Rpt Cycle Purchase of Mdse, & Labor, Etc. PP&E, Investments Cash Disbursements Merchandise Receipts

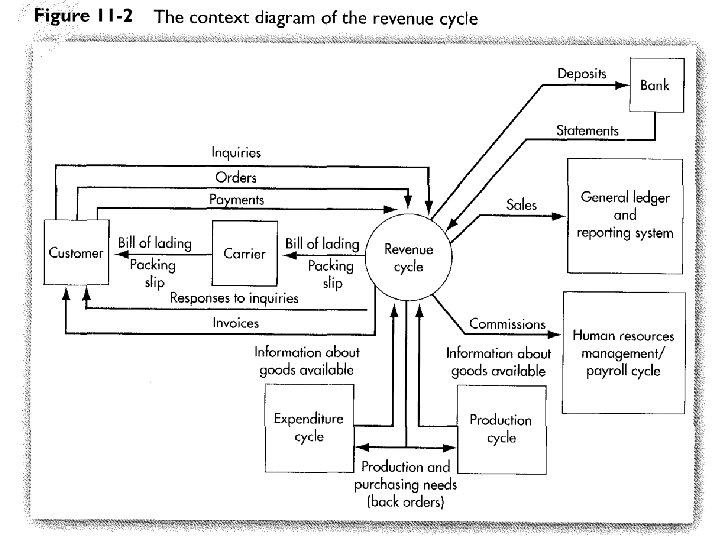

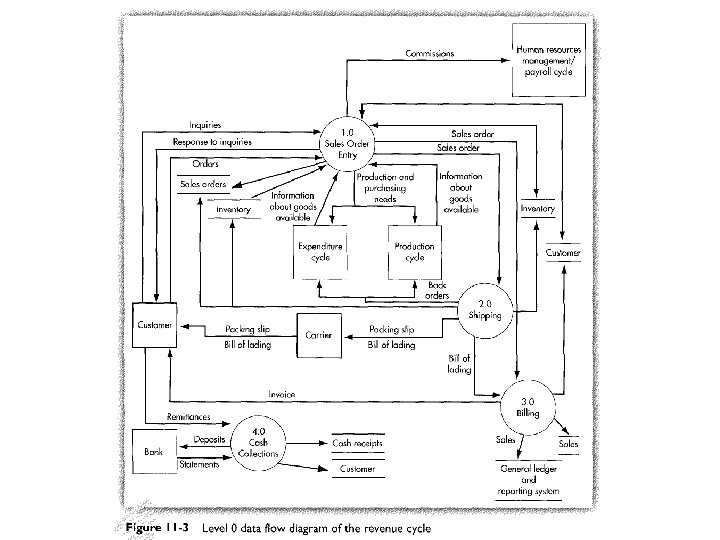

The Revenue Cycle: A Definition

The Revenue Cycle. . . is a recurring set of business activities and related information processing operations associated with providing. . . 1. Goods/Services to customers; and 2. Collecting cash in payment for those sales

Merchandising Shipments Sale of Merchandise Cash Receipts GL & PP&E, The Revenue Fin Rpt Cycle Investments Cyclefrom “Sale” to Spans activities Purchase of Mdse, & Labor, Etc. “Receipt of Cash. ” Key Cash Transactions: Disbursements Merchandise Sales Receipts Cash Receipts

The major purpose of the revenue cycle is to facilitate the exchange of products or services with customers for cash.

The Revenue Cycle Business Activities

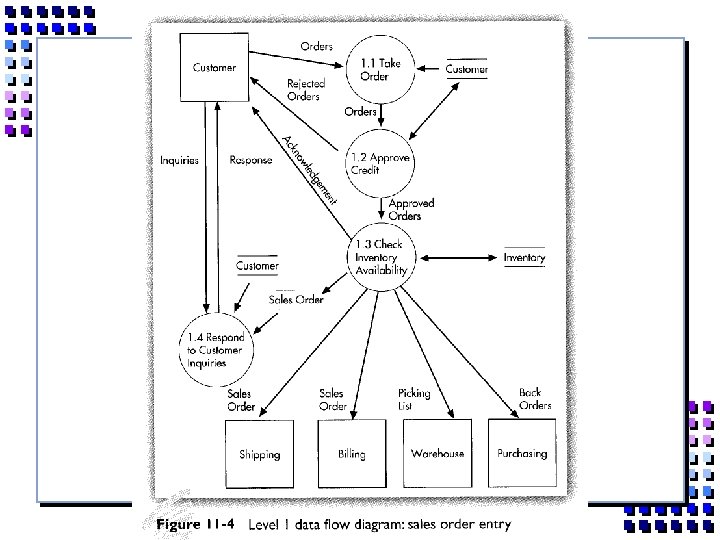

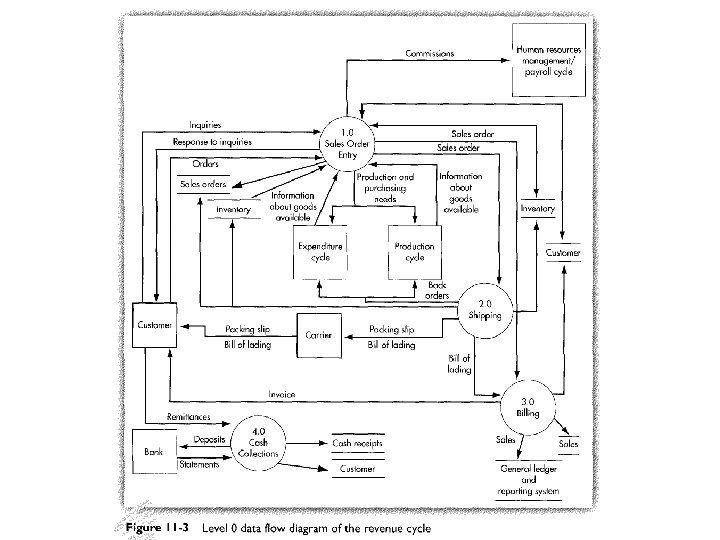

1. 0 Sales Order Entry

Sales Order Entry v Key Decisions and Information Needs – Inventory Availability – Customer Credit Status

Sales Order Entry v Main Activities – Taking customer orders – Credit Approval – Check inventory availability – Respond to customer inquiries

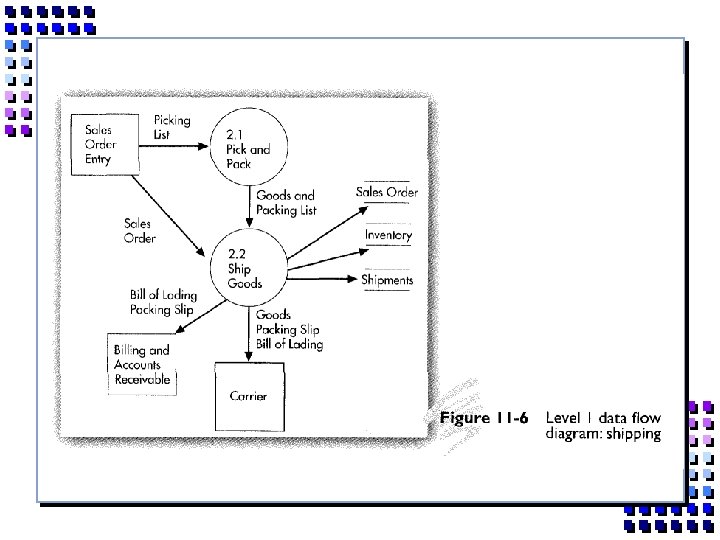

2. 0 Shipping

Shipping v Pick v Ship and Pack the order

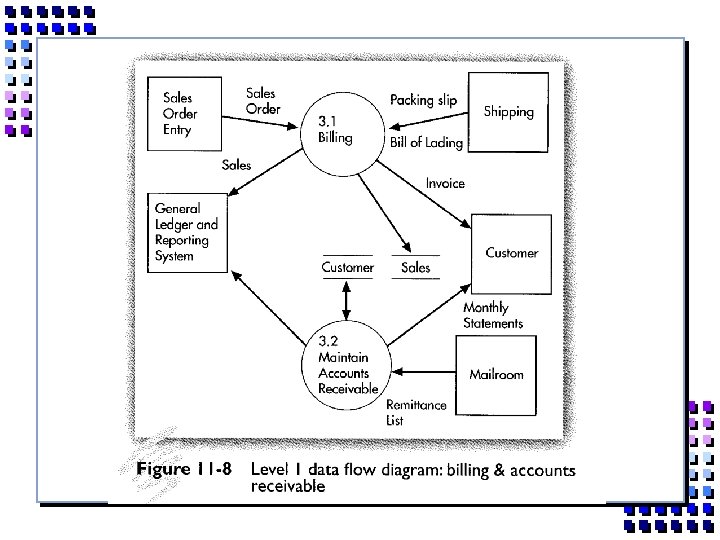

3. 0 Billing

Billing v Maintain Accounts Receivable

4. 0 Cash Collections

The Revenue Cycle: Objectives

Objectives of the Cycle. . . v Record sales orders promptly and accurately. v Verify v Ship v Bill credit worthiness. products or perform services. for products and services in a timely manner.

Objectives of the Cycle. . . v Record and classify cash receipts promptly and accurately. v Post sales and cash receipts to customers’ accounts. v Safeguard products until shipped. v Safeguard cash until deposited.

The Revenue Cycle: Data Input

Sources of Input. . . v Customers v Salespersons v Credit records v Inventory records

Sources of Input. . . v Finished goods warehouse v Suppliers v Shipping department

Forms of Input. . . v Customer v Sales order v Order v Picking acknowledgment list

Forms of Input. . . v Packing v Bill slip of lading v Shipping v Sales notice invoice

Forms of Input. . . v Remittance v Deposit v Back advice slip order v Credit memo v Credit application

A & R s e Sales Sa h s Ca A/R Typical Dis c. Accounts in Allowance the Revenue Bad Deb Cycle ts les

Merchandising Shipments Sale of Merchandise Cash Receipts GL & PP&E, Fin Rpt Cycle Investments The Revenue Cyclefrom “Sale” to Spans activities Purchase of Mdse, & Labor, Etc. “Receipt of Cash. ” Key Cash Transactions: Disbursements Sales Cash Receipts

Typical Accounts. . . v Sales Returns and Allowances v Sales Discounts v Accounts Receivable

Typical Accounts. . . v Bad Debts Expense v Allowance v Inventory v Cash For Doubtful Accounts

Typical Functions of a Revenue Cycle

Obtain Cust. Order Typical Functions of the Revenue Cycle Check Credit Enter Sales Order Ready Goods Shpt. Ship Goods Perform Service Bill Cust. Rec. & Dep. Cash Maintain Records Post Trans.

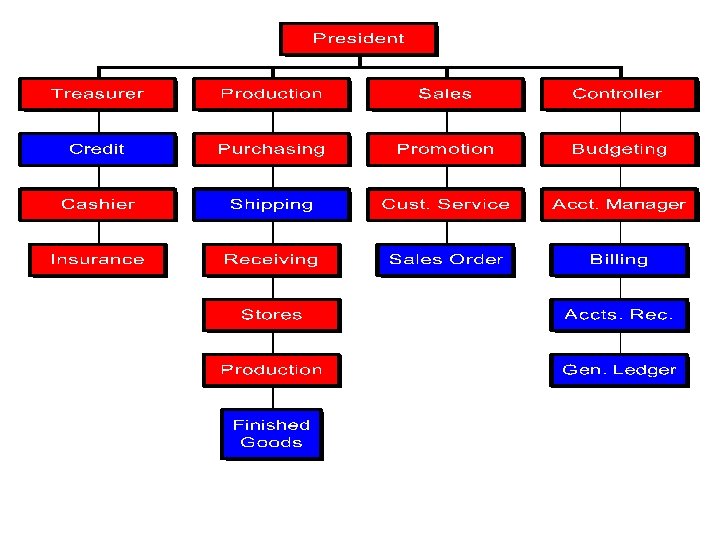

Segregation of Functions

v Transaction authorization should be separate from v transaction processing

v Transaction Custody should be separate from v asset Recordkeeping

The organization should be so structured that the perpetration of a fraud requires. . . collusion between 2 or more individuals.

Organizational Independence

Functional Responsibility in a. . . Sales Order Application System

Functional Responsibility v For sales, control is achieved by separating the transaction’s. . . – Origination – Authorization – Recording – Execution

1 Originate

2 Authorize

3 Execute

4 Record

2 3 1 4 Authorize Execute Originate Record

Functional Responsibility in an. . . Accounts Receivable Application System

Functional Responsibility v For accounts receivable, control is achieved by separating. . . – Authorization of transactions – Recording of transactions – Execution of transactions

1 2 3

Control Objectives, Threats, and Procedures

Control Objectives v All transactions are properly authorized. v All recorded transactions are valid (actually occurred). v All valid, authorized transactions are recorded.

Control Objectives v All transactions are recorded accurately. v Assets (cash, inventory, data) are safeguarded from loss or theft. v Business activities are performed efficiently and effectively.

1. 0 Sales Order Entry

Threats 1. Incomplete or inaccurate customer orders. 2. Credit sales to customers with poor credit. 3. Legitimacy of orders 4. Stockouts, carrying costs, and markdowns.

2. 0 Shipping

Threats 5. 6. Shipping Errors – Wrong merchandise – Wrong quantities – Wrong address Thefts of Inventory

3. 0 Billing

Threats 7. Failure to bill customers. 8. Billing errors. 9. Posting errors in updating accounts receivable.

4. 0 Cash Collections

Threats 10. Theft of cash

General Control Issues

Threats 11. Loss of Data 12. Poor performance