CH 5 Intercompany Inventory Transactions p 168 Revenue

of this merchandise was then sold to outside")

- Slides: 66

CH 5

Intercompany Inventory Transactions p 168 Revenue on sales between affiliates cannot be recognized until merchandise is sold outside of the consolidated entity. The sale of inventory by one company to an affiliate produces reciprocal sales and purchases (cost of goods sold) accounts when the purchaser has a periodic inventory system (perpetual inventory system) We eliminate reciprocal sales and cost of goods sold (or purchases) amounts in preparing a consolidated income statement

Elimination of Intercompany Purchases and Sales P 168 The workpaper elimination under a perpetual inventory system (used throughout this book) is a debit to sales and a credit to cost of goods sold. The reason is that a perpetual inventory system includes intercompany purchases in a separate cost of goods sold account of the purchasing affiliate when it is sold to outside third parties.

Elimination of Intercompany Purchases and Sales p 168/169 P formed a subsidiary, S, in 2011 to retail a special line of P’s merchandise. All S’s purchases are made from P at 20 percent above P’s cost. During 2011, P sold merchandise that cost $40, 000 to S for $48, 000, and S sold all the merchandise to its customers for $60, 000.

Separate books

Workpaper p 169 In addition to eliminating intercompany profit items, it is necessary to eliminate intercompany receivables and payables in consolidation

Elimination of Unrealized Profit in Ending Inventory p 169 The ending inventory of the purchasing affiliate reflects any unrealized profit or loss on intercompany sales because that inventory reflects the intercompany transfer price rather than cost to the consolidated entity

Elimination of Unrealized Profit in Ending Inventory p 169 During 2012 P sold merchandise that cost $60, 000 to Sep for $72, 000 S sold all but $12, 000 of this merchandise to its customers for $75, 000

Separate Books p 169/p 170

p 170 $50, 000 (or 5/6) of this merchandise was then sold to outside entities for $75, 000. $10, 000 (or 1/6) remains in inventory at year-end. The consolidated entity realizes a gross profit of $25, 000

Workpaper p 170

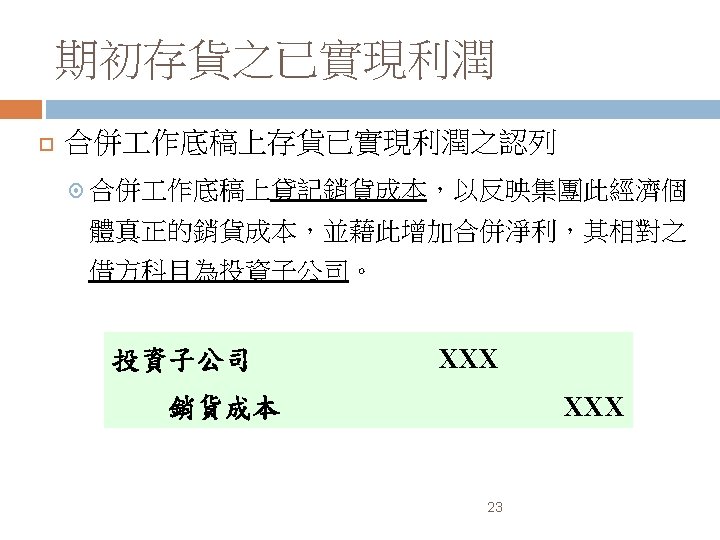

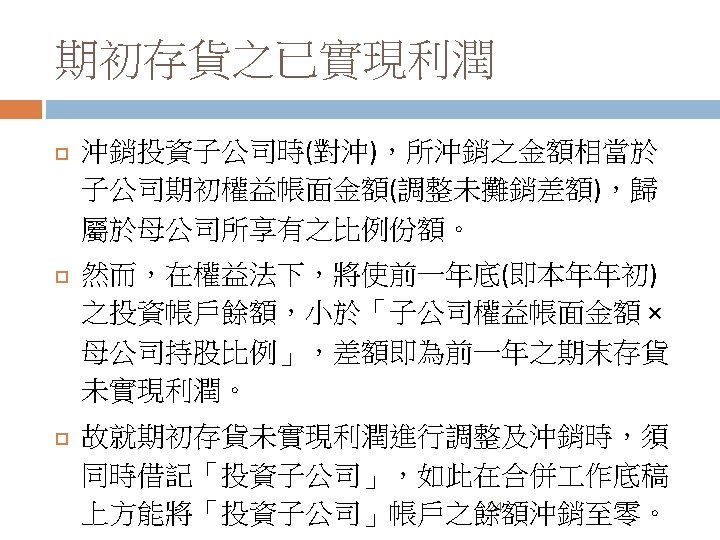

Equity Method p 171 On 12/31, 2012, P defers $2, 000 intercompany profit. P’s one-line consolidation entry reduces income from Sep by the $2, 000 unrealized profit in the ending inventory and accordingly reduces the Investment in S account by $2, 000.

Elimination of Unrealized Profit in Beginning Inventory p 171 During 2013, P sold merchandise that cost $80, 000 to S for $96, 000, S sold 75 % of the merchandise for $90, 000. S also sold the items in the beginning inventory with a transfer price of $12, 000 to its customers for $15, 000.

Separate books p 171

p 172 $60, 000 of this merchandise, plus $10, 000 beginning inventory, was sold for $105, 000. $20, 000 remained in inventory at year-end 2013. The consolidated entity realized a gross profit of $35, 000.

Workpaper p 172

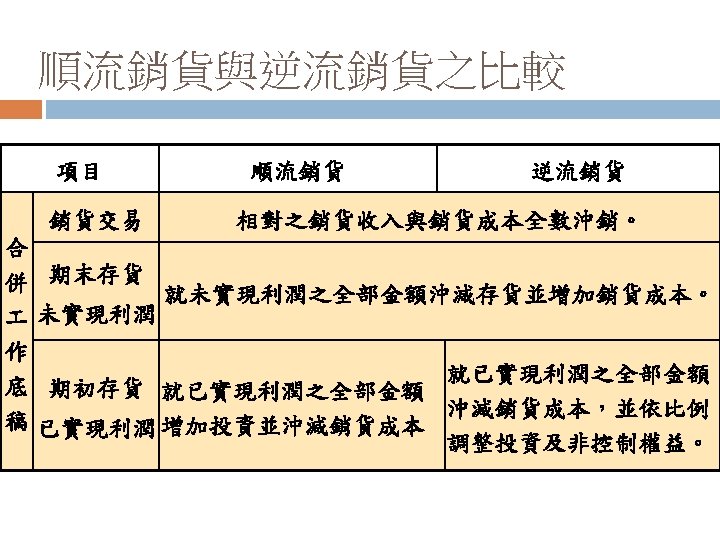

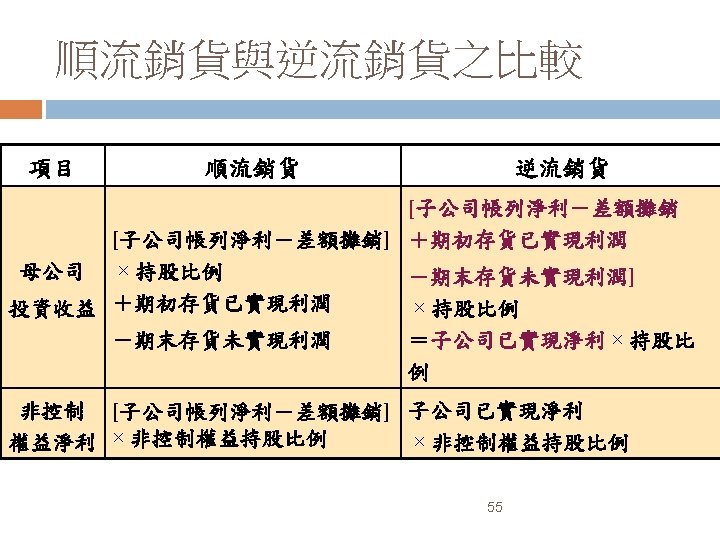

Downstream and Upstream Sales p 172/p 173 A downstream sale is a sale by a parent to a subsidiary An upstream sale is a sale by a subsidiary to its parent. Consolidated statements eliminate reciprocal sales and cost of goods sold amounts regardless of whether the sales are upstream or downstream.

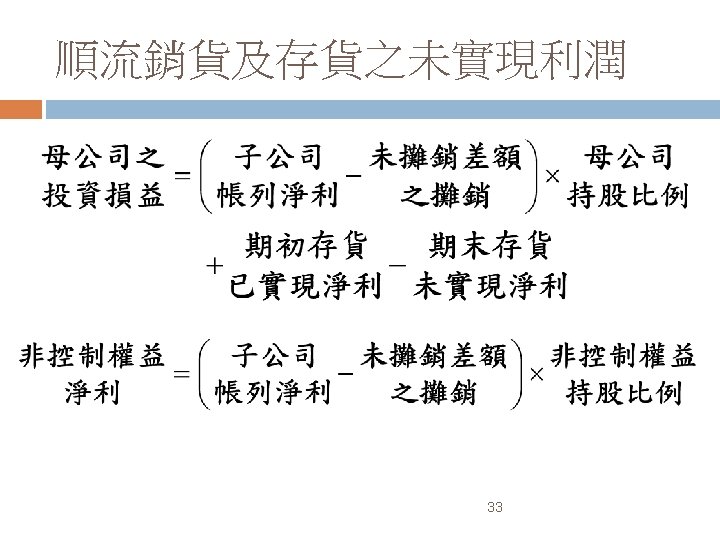

Downstream and Upstream Sales p 173 We also eliminate any unrealized gross profit in ending inventory in its entirety for both downstream and upstream sales. However, the effect of unrealized profits in ending inventory on separate parent statements (as investor) and on consolidated financial statements (which show income to the controlling and noncontrolling stockholders) is determined by both the direction of the intercompany sales activity and the percentage ownership of the subsidiary, except for 100 percentowned subsidiaries that have no noncontrolling ownership.

Downstream and Upstream Sales p 173 In the case of downstream sales, the parent’s separate income includes the full amount of any unrealized profit (included in its sales and cost of sales accounts), and the subsidiary’s income is unaffected. When sales are upstream, the subsidiary’s net income includes the full amount of any unrealized profit (included in its sales and cost of sales accounts), and the parent’s separate income is unaffected

Downstream and Upstream Sales p 173 The noncontrolling interest share may be affected if the subsidiary’s net income includes unrealized profit (the upstream situation). It is not affected if the parent’s separate income includes unrealized profit (the downstream situation) because the noncontrolling shareholders have an interest only in the income of the subsidiary.

Downstream and Upstream Sales p 173 Unrealized profits and losses from upstream sales are allocated proportionately between consolidated net income (controlling interests) and noncontrolling interest share (noncontrolling interests) throughout this book.

Downstream and Upstream Effects on Income Computations p 173 Assume that the separate incomes of a parent and its 80%-owned subsidiary for 2011 are as follows

Noncontrolling interest share computation p 176 Intercompany sales during the year are $100, 000, and the 12/ 31, 2011, inventory includes $20, 000 unrealized profit. Downstream $50, 000 net income of subsidiary * 20% = $10, 000 Upstream ($50, 000 net income of subsidiary - $20, 000 unrealized) * 20% = $6, 000

Consolidated net income computation p 174

Unrealized Profits from Downstream Sales p 175 P owns 90% S. Separate income statements of P and S for 2011, before consideration of unrealized profits

Unrealized Profits from Downstream Sales p 175 P’s sales include $15, 000 to S at a profit of $6, 250, and S’s 12/31, 2011, Inventory includes 40% of the merchandise from the intercompany transaction. P’s operating income reflects the $2, 500 unrealized profit in S’s inventory ($6, 000 transfer price less $3, 500 cost).

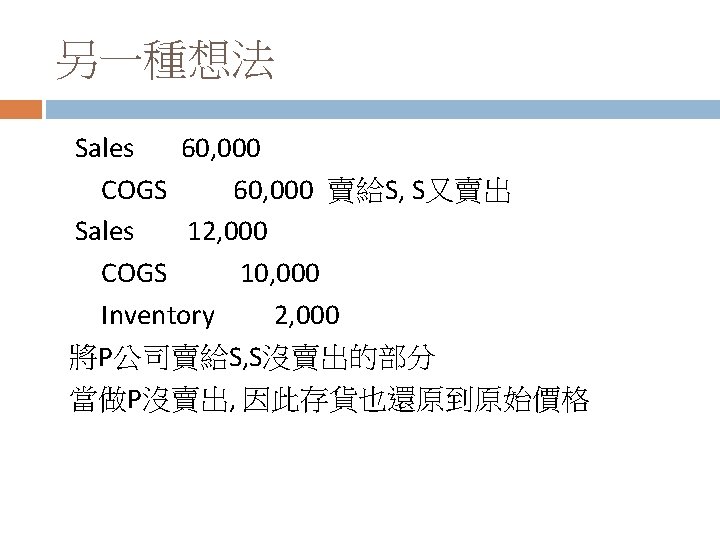

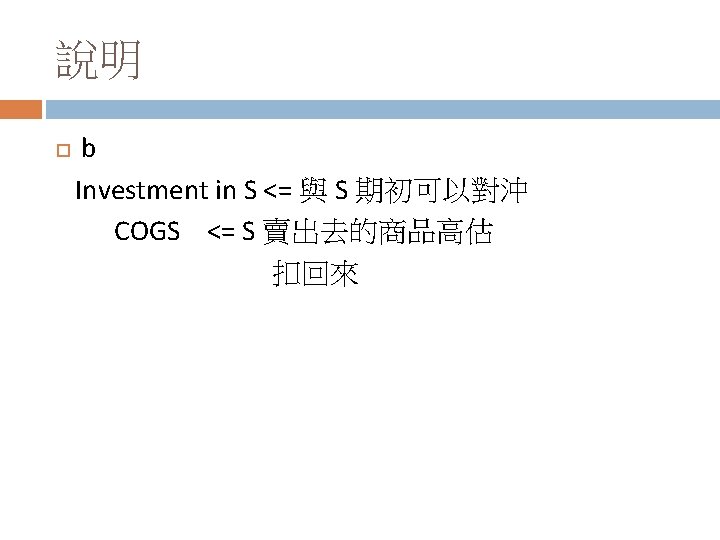

Equity method-順流本期未賣出

Recognition of Intercompany Profit upon Sale to Outside Entities P 176 the merchandise acquired from P during 2011 is sold by S during 2012, and there are no intercompany transactions between P and S during 2012. Separate income statements for 2012 before consideration of the $2, 500 unrealized profit in S’s beginning inventory

Equity Method-順流本期已賣出

Unrealized Profits from Upstream Sales p 178 S sells merchandise that it purchased for $7, 500 to P for $20, 000 during 2011 and that P sold 60 % of the merchandise to outsiders during the year for $15, 000. At year-end the unrealized inventory profit is $5, 000 (cost $3, 000, but included in P’s inventory at $8, 000)

Equity Method-逆流年底未實現

Equity method-逆流本期已賣出

Consolidation example-Intercompany Profits From Downstream Sales p 180 S is a 90%-owned subsidiary of P, acquired for $94, 500 cash on 7/1, 2011, when S’s net assets consisted of $100, 000 capital stock and $5, 000 retained earnings. (The cost of P’s 90% interest in S was equal to book value and fair value of the interest acquired ($105, 000 × 90%), and accordingly, no allocation to identifiable and unidentifiable assets was necessary)

Equity Method-順流 p 181

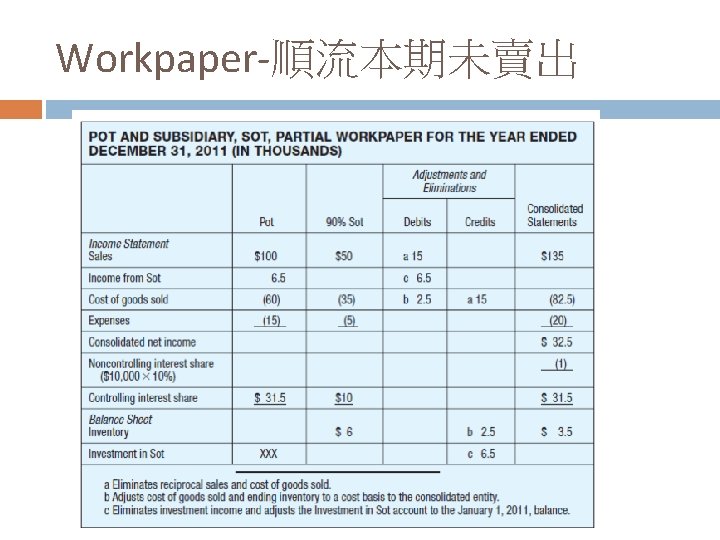

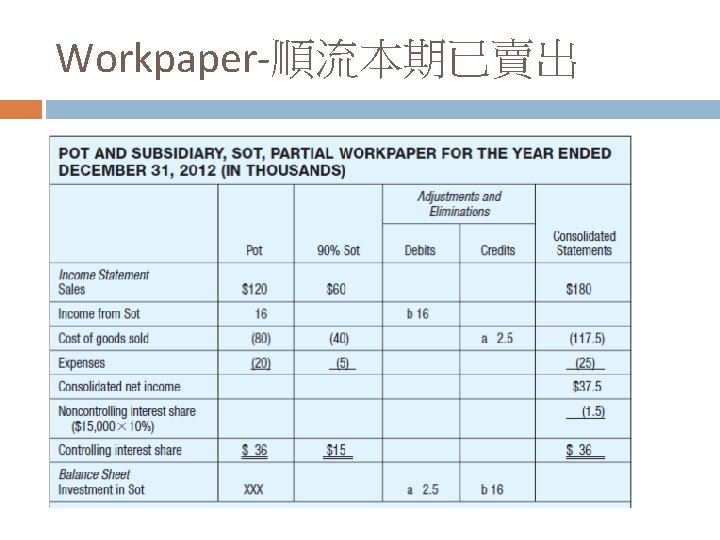

Workpaper-順流

Workpaper-順流

Workpaper-順流

Consolidation example-Intercompany Profits From Upstream Sales p 183 S is an 80%-owned subsidiary of P, acquired for $480, 000 on 1/2, 2011, when S’s stockholders’ equity consisted of $500, 000 capital stock and $100, 000 retained earnings.

Equity Method-逆流 p 183

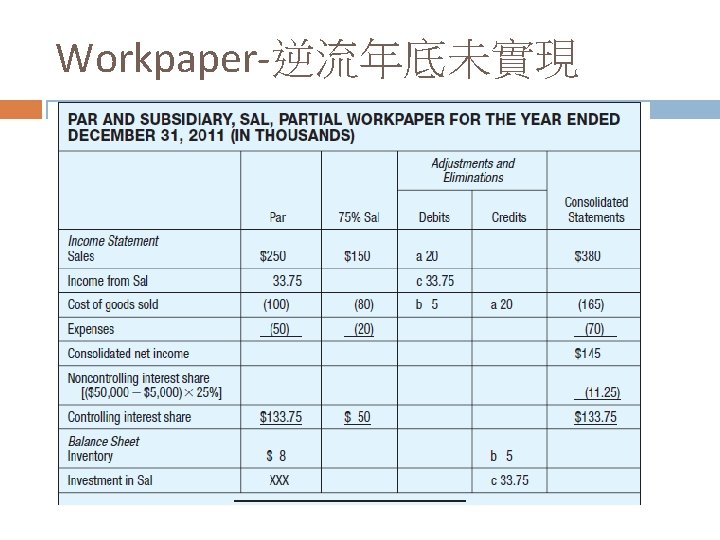

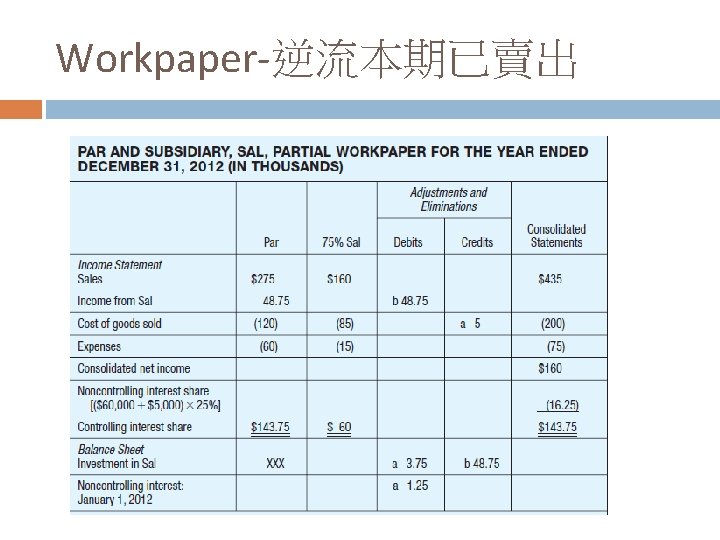

Working paper entries-逆流 p 185

Working paper entries-逆流 p 185

Noncontrolling Interest-逆流 p 185

Workpaper-逆流