Intercompany profit transactionsplant assets CHAPTER 6 Intercompany profit

內部交易會計處理 p 207 1. An intercompany unrealized gain")

p 217")

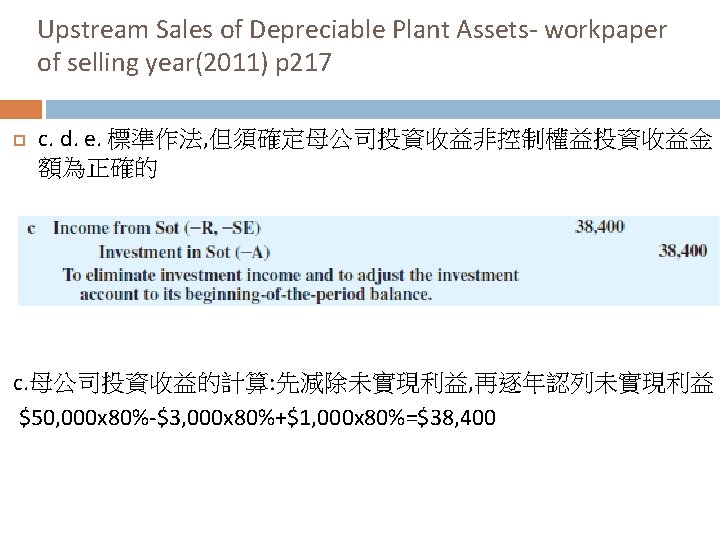

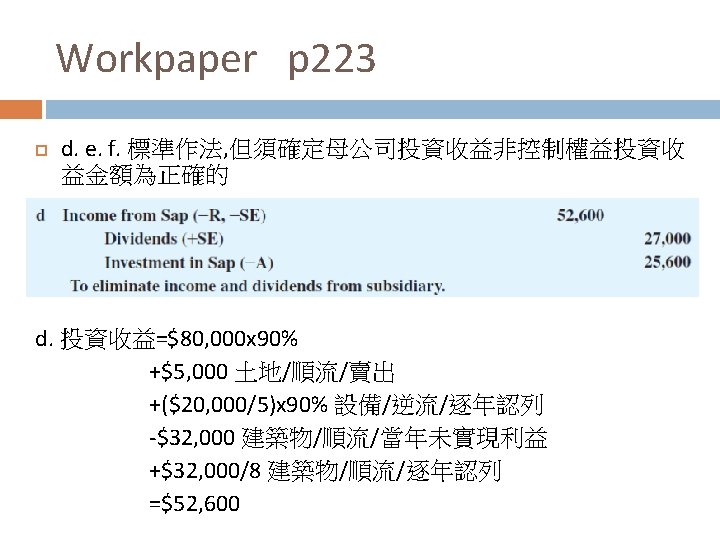

p 217 d. 非控制權益收益的計算: 亦先減除未實現利益,")

")

")

")

")

")

")

")

- Slides: 69

Intercompany profit transactionsplant assets CHAPTER 6

Intercompany profit transactions-plant assets 固定資產內部交易 p 207 The adjustments to eliminate the effects of intercompany profits on plant assets are similar to, but not identical with, those for unrealized inventory profits. 母子公司內固定資產的會計處理程序與存貨內部交易相似但 仍有不同。 Unrealized inventory profits self-correct over any two accounting periods(關於存貨=>投資收益這一期減未實現損益 , 下一期就加回來), but unrealized profits or losses on plant assets affect the financial statements until the related assets are sold outside the consolidated entity or are exhausted through use by the purchasing affiliate(關於固定資產=>隨著固定資產 的使用或賣出去才能承認收益, 也就是說在固定資產報廢或 賣出前皆會影響財報).

Intercompany profits on nondepreciable plant assets 非折舊性固定資產(土地)內部交易會計處理 p 207 1. An intercompany unrealized gain or loss appears in the income statement of the selling affiliate in the year of sale. 賣方在賣資產當年度會產生未實現利得 2. This gain (loss) must be eliminated from investment income in a one-line consolidation by the parent and must be eliminated in preparing consolidated financial statements. 未實現利得(損失)必須在權益法及合併報表做調整

內部交易的方向 p 208 與存貨內部交易類似, 非折舊性資產內部交易的方向 很重要。 Any gain or loss on sales downstream from parent to subsidiary is initially included in parent income and must be eliminated. =>順流交易, 未實現利益在母公司 帳上, 未實現損益100% 消除。 Any gain or loss on sales upstream from subsidiary to parent is initially included in subsidiary income. For the parent, the parent’s proportionate share of unrealized profits should be eliminated. =>逆流交易, 未實現利益 在子公司帳上, 母公司按持股比例消除未實現損益。

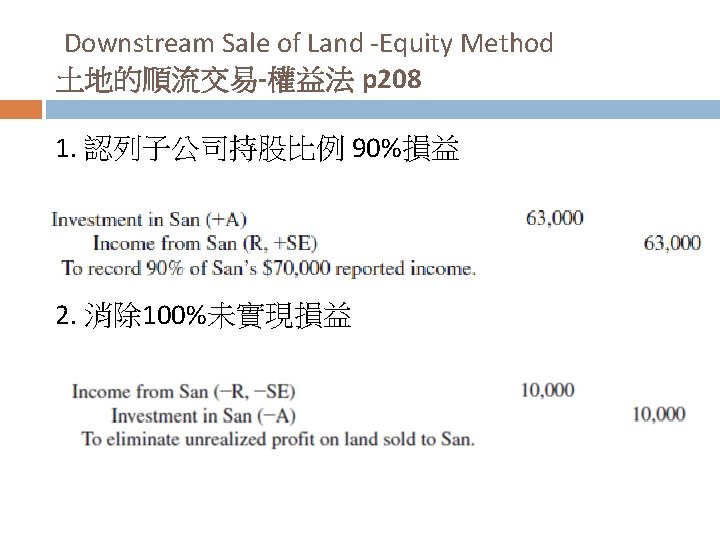

Downstream Sale of Land 土地的順流交易 p 208 Example: P=>S 90% acquire for $270, 000 on 1/1, 2011 (Investment cost = BV & FV of the interest acquired) S’s net income for 2011 was $70, 000, and P’s income, excluding its income from S, was $90, 000. P’s income includes a $10, 000 unrealized gain on land that cost $40, 000 and was sold to S for $50, 000.

Downstream Sale of Land Work paper of the selling year p 208 a. 將土地回復到成本及沖銷未實現利益

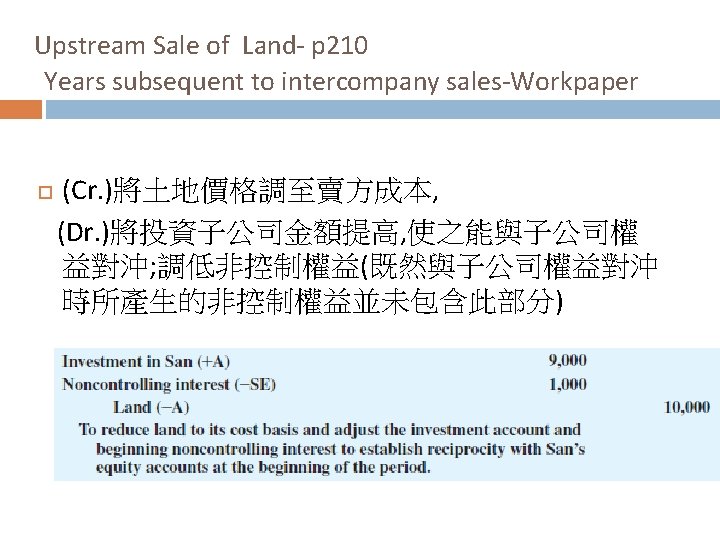

Downstream Sale of Land p 208 Work paper of the next year of selling year a. 將土地回復到成本及回復投資金額(以便與子公 司權益對沖) The investment account balance at 12/31, 2011, is $323, 000. This is $10, 000 less than P’s underlying equity in S of $333, 000 on that date ($370, 000 * 90%).

Downstream Sale of Land Sale in Subsequent Year to Outside Entity p 208 Assume that S uses the land for four years and sells it for $65, 000 in 2015. In the year of sale, S reports a $15, 000 gain ($65, 000 proceeds less $50, 000 cost), However, the gain to the consolidated entity is $25, 000 ($65, 000 proceeds less $40, 000 cost to P

Downstream Sale of Land Sale in Subsequent Year to Outside Entity -Equity Method p 209 認列已實現的未實現損益

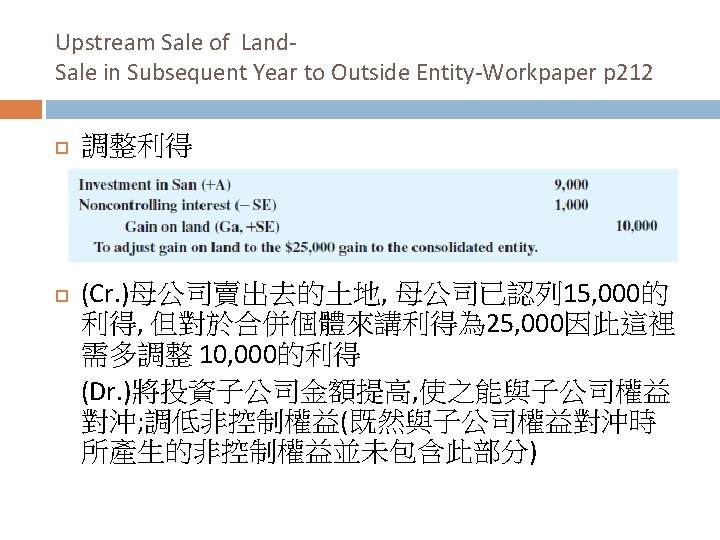

Downstream Sale of Land Sale in Subsequent Year to Outside Entity -Workpaper p 210 調整利得及回復投資金額(以便與子公司權益對 沖) 子公司賣出去的土地成本為 50, 000, 實際成本為 40, 000, 子公司已認列 15, 000(65, 000 -50, 000)的利 得, 因此這裡多調整 10, 000 的利得(65, 00040, 000)-(65, 000 -50, 000)

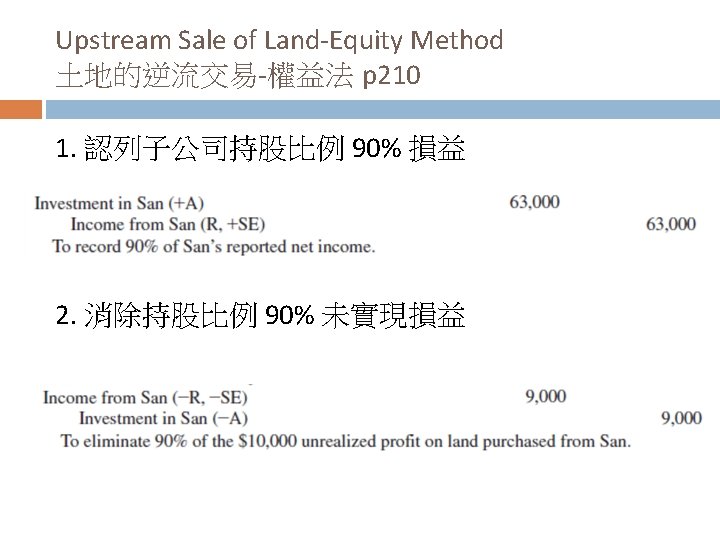

Upstream Sale of Land 土地的逆流交易 p 210 P purchases the land in 2011 from its 90 %-owned S. S’s net income for 2011 is $70, 000, P’s income, excluding its income from S, is $90, 000. The $10, 000 unrealized profit on the intercompany sale of land is now reflected in the income of S, rather than P

Upstream Sale of Land- Noncontrolling interest share 土地的逆流交易-非控制權益投資收益 p 210 We reduce the noncontrolling interest share with its share of the unrealized gain on S’s sale of land to P. $70, 000 x 10% - $10, 000 x 10%=$6, 000

Upstream Sale of Land- EXHIBIT 6 -2 p 211

Sale in Subsequent Year to Outside Entity. Equity Method p 212 認列未實現利得實現

Intercompany Profits on Depreciable Plant Assets p 212 Firms must eliminate the effects of these gains and losses from parent and consolidated financial statements until the consolidated entity realizes them through sale to other entities or through use within the consolidated entity 公司必須消除折舊性固定資產所造成的賣方內部 交易利得及調整合併報表; 隨著買方的使用或再賣 給第三方, 賣方可以認列利得, 合併報表也會隨之調 整

Downstream Sales of Depreciable Plant Assets p 212 Gains or losses appear in the parent’s accounts in the year of sale and must be eliminated by the parent in determining its investment income under the equity method. 在順流交易下, 母公司必須針對未實現利得的部分, 在權益法的部分調整投資收益 Similarly, we eliminate such gains or losses from consolidated statements by removing each gain or loss and reducing the plant assets to their depreciated cost to the consolidated entity. 在合併報表的部分, 固定資產必須回復到成本, 相對 應的利得或損失也必須消除。

Downstream sale at the end of a year p 212 P sells machinery to its 80%-owned S, on 12/31, 2011. The machinery has an undepreciated cost of $50, 000 on this date (cost, $90, 000, and accumulated depreciation, $40, 000), It is sold to Sop for $80, 000

Downstream sale at the end of a year賣出時母子公司個別分錄 p 212

Downstream sale at the end of a year. Equity Method adjustment p 212 母公司權益法中調整投資收益, 將未實現銷售利 得消除 $80, 000 -($90, 000 -$40, 000)=$30, 000

Downstream sale at the end of a year- Workpaper adjustment p 213 將未實現利得消除, 固定資產回復到其成本

Downstream sale at the end of a year. Workpaper adjustment p 213 We could also record this effect Gain on sale of machinery 30, 000 Machinery 10, 000 Accumulated depreciation—machinery 40, 000. Conceptually, this entry is superior because it results in reporting plant assets and accumulated depreciation at the amounts that would have been shown if the intercompany sale had not taken place. From a practical viewpoint, however, the additional detail is usually not justified by cost–benefit considerations, because the same net asset amounts are obtained without the additional recordkeeping costs. The examples in this book reflect the more practical approach.

Downstream sale at the beginning of a yearexample p 213 1. P sells machinery to its 80%-owned S, on 1/1, 2011. =>the machinery would have been depreciated by S during 2011, and any depreciation on the unrealized gain would be considered a piecemeal recognition of the gain during 2011. 1. 若交易未發生, 則每年的相關折舊費用會是多少? 2. 內部交易發生, 在買方帳上每年的折舊費用會是多少? =>每年兩者折舊費用的差異可視為未實現利得的部分認列

Downstream sale at the beginning of a year -example p 213 2. On 1/1, 2011, the date of the intercompany sale, the machinery has a five-year remaining useful life and no expected residual value at 12/31, 2015. (Straight-line) =>a. The entries to record the sale and purchase are the same as for the 12/31 sale; b. S also records depreciation expense of $16, 000 for 2011 ($80, 000, 5 years).

Downstream sale at the beginning of a year-example p 213 c. Of this $16, 000 depreciation, $10, 000 is based on cost to the consolidated entity ($50, 000 cost , 5 years), and $6, 000 is based on the $30, 000 unrealized gain ($30, 000, 5 years). d. The $6, 000 is considered a piecemeal recognition of one-fifth of the $30, 000 unrealized gain on the intercompany transaction. e. Conceptually, this is equivalent to the sale to other entities of one-fifth of the services remaining in the machinery

Downstream sale at the beginning of a year-Equity method adjustment p 213 1. 消除 100% 順流未實現損益 2. 逐步認列未實現損益

Effect of Downstream sale on a consolidation workpaper p 213 合併數字即若無交易發生, 則在母公司帳上, 該固 定資產應有的數字($50, 000, 5 years) 折舊費用 $50, 000/5=$10, 000 固定資產 $50, 000 -$10, 000 = $40, 000

Downstream sale at the beginning of a year-Equity method adjustment for each year p 214 2012, 2013, 2014, and 2015 ($80, 000 -$50, 000)/5=$6, 000 即前述兩者折舊金額的差異, 也就是隨著買方固定資 產的使用逐年認列未實現利益

Downstream sale at the beginning of a year-Equity method adjustment for each year p 214 Year 2011 2012 2013 2014 2015

Downstream sale at the beginning of a year. Workpaper adjustment of subsequent year p 214

Upstream Sales of Depreciable Plant Assets p 214 Upstream sales of depreciable assets from a subsidiary to a parent result in unrealized gains or losses in the subsidiary accounts in the year of sale (unless the assets are sold at book values). 逆流交易-子公司賣固定資產給母公司會在當年 度子公司帳上產生未實現損益

Upstream Sales of Depreciable Plant Assets p 214 In computing parent’s investment income in the year of sale, the parent adjusts its share of the reported income of the subsidiary for (1) its share of any unrealized gain on the sale (2) its share of any piecemeal recognition of such unrealized gain through depreciation. 認列有逆流交易的投資收益時母公司(非控制權益)在 交易當年必須 (1)消除持股比例的未實現損益; (2)經由固定資產的使用折舊, 逐年認列母公司持股比例 的前述未實現利益

Upstream Sales of Depreciable Plant Assets – example p 214 P purchases a truck from its 80%-owned S on 1/1, 2011 (at the beginning of the year) Other information is as follows:

Effect of upstream sale on the affiliates’ separate books- Subsidiary p 216 If S sells the truck to P for $12, 000 cash, S and P make the following journal entries on their separate books

Effect of upstream sale on the affiliates’ separate books- Parent p 216 購買分錄及提列當年度折舊

Effect of upstream sale on the affiliates’ separate books- P p 216 認列當年度調整後投資收益 未實現利得=$12, 000 -$9, 000=$3, 000 母公司部分=$3, 000 x 80%=$2, 400 逐年認列=$2, 400/3=$800

Effect of upstream sale on consolidation workpapers p 216 Investment in S 80% = 80% of the equity of S at 12/31, 2013

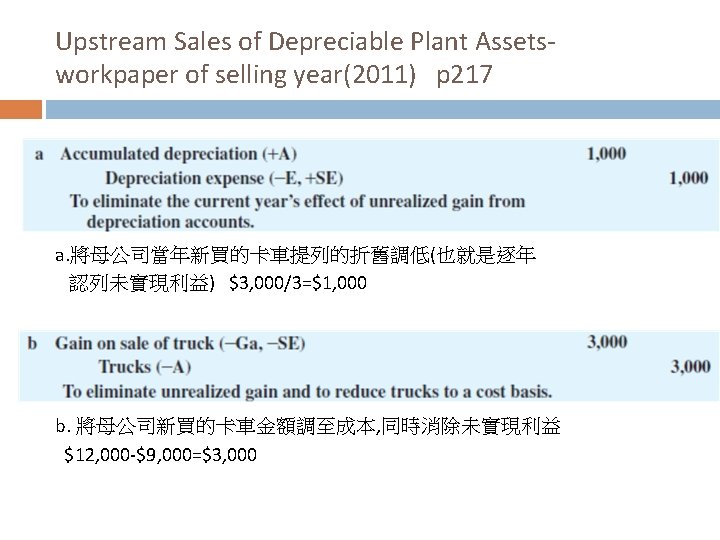

Upstream Sales of Depreciable Plant Assetsworkpaper of selling year(2011) p 217

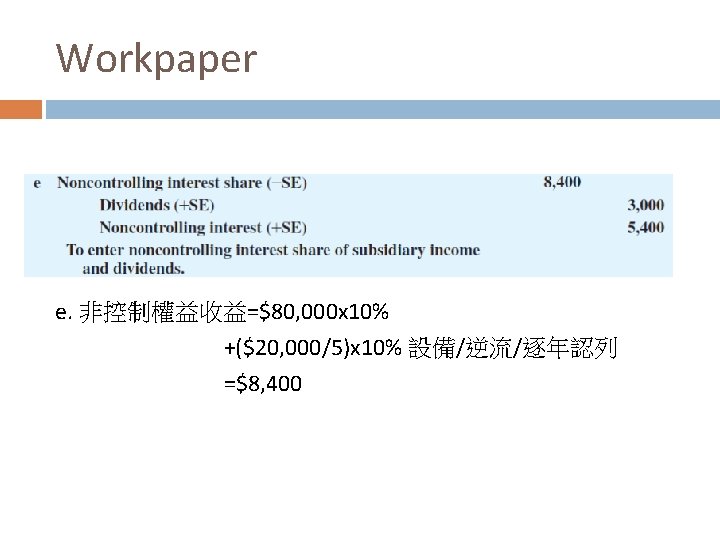

Upstream Sales of Depreciable Plant Assetsworkpaper of selling year(2011) p 217 d. 非控制權益收益的計算: 亦先減除未實現利益, 再逐年認列 投資收益 $50, 000 x 20%-$3, 000 x 20%+$1, 000 x 20%=$9, 600 e. 對沖

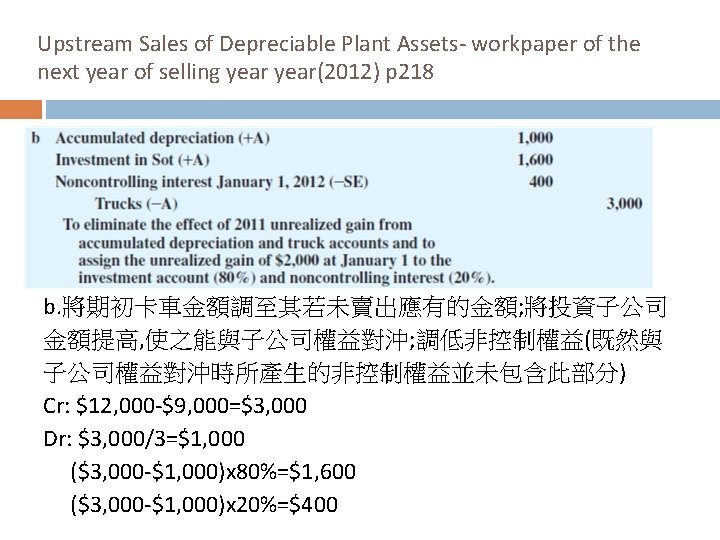

Upstream Sales of Depreciable Plant Assets- workpaper of the next year of selling year(2012) p 218

Upstream Sales of Depreciable Plant Assets- workpaper of the next year of selling year(2012) p 218 a. 將母公司卡車提列的折舊調低(也就是逐年認列未實現利益) $3, 000/3=$1, 000

Upstream Sales of Depreciable Plant Assets- workpaper of the next year of selling year(2012) p 218 c. d. e. 標準作法, 但須確定母公司投資收益非控制權益投資收 益金額為正確的 c. 母公司投資收益計算: 逐年認列未實現利益 $50, 000 x 80%+$1000 x 80%=$40, 800

Upstream Sales of Depreciable Plant Assets- workpaper of the next year of selling year(2012) p 218 d. 非控制權益收益: 亦逐年認列未實現利益 $50, 000 x 20%+$1000 x 20%=$10, 200 e. 對沖

Upstream Sales of Depreciable Plant Assetsworkpaper of the next two year of selling year(2013) p 219

Upstream Sales of Depreciable Plant Assetsworkpaper of the next two year of selling year(2013) p 219 a. 將母公司卡車提列的折舊調低(也就是逐年認列未實現利益) $3, 000/3=$1, 000

Upstream Sales of Depreciable Plant Assetsworkpaper of the next two year of selling year(2013) p 219 b. 將期初卡車金額調至其若未賣出應有的金額; 將投資子公司 金額提高, 使之能與子公司權益對沖; 調低非控制權益(既然與 子公司權益對沖時所產生的非控制權益並未包含此部分) Cr: $12, 000 -$9, 000=$3, 000 Dr: $3, 000/3=$1, 000 x 2=$2, 000 ($3, 000 -$2, 000)x 80%=$800 ($3, 000 -$2, 000)x 20%=$200

Upstream Sales of Depreciable Plant Assets- workpaper of the next two year of selling year(2013) p 220 c. d. e. 標準作法, 但須確定母公司投資收益非控制權益投資收 益金額為正確的 c. 母公司投資收益計算: 逐年認列未實現利益 $50, 000 x 80%+$1000 x 80%=$40, 800

Upstream Sales of Depreciable Plant Assets- workpaper of the next two year of selling year(2013) p 220 d. 非控制權益收益: 亦逐年認列未實現利益 $50, 000 x 20%+$1000 x 20%=$10, 200 e. 對沖

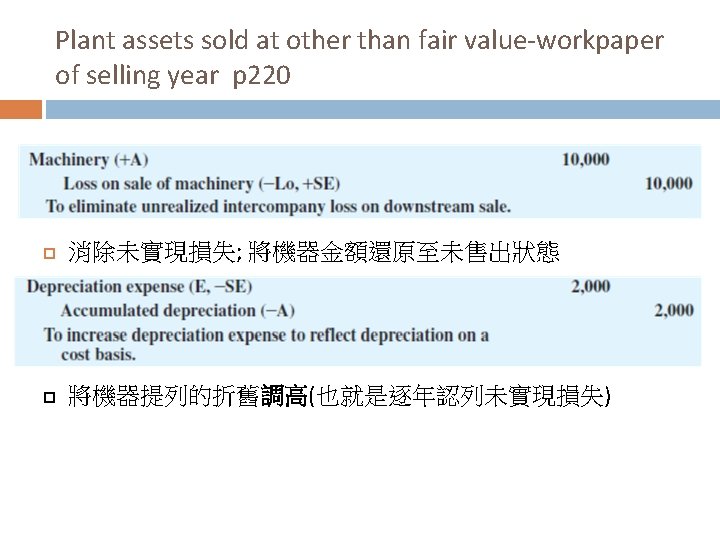

Consolidation with loss on intercompany salep 220 Consolidation procedures to eliminate intercompany unrealized losses are essentially the same as those to eliminate unrealized gains. Assume that a machine had a remaining useful life of 5 years when it was sold on 1/1, 2011, to the 90%owned S for $20, 000. The book value was $30, 000. The parent has a $10, 000 unrealized loss that is recognized on a piecemeal basis over five years

Consolidation with loss on intercompany sale. Equity Method p 220

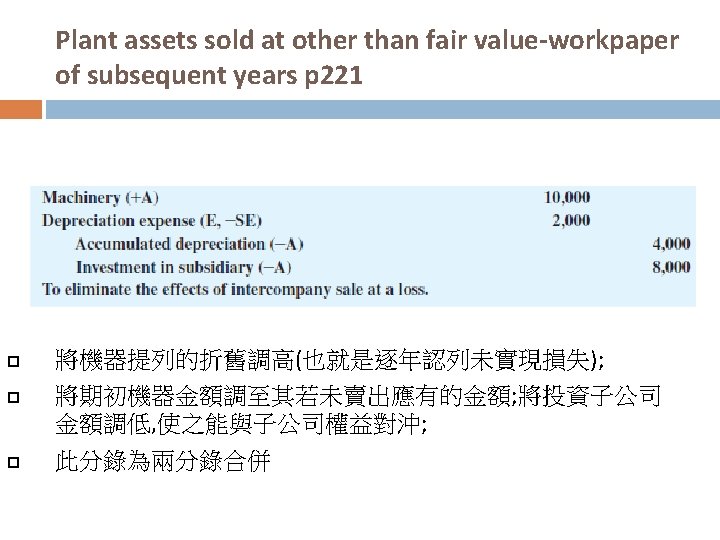

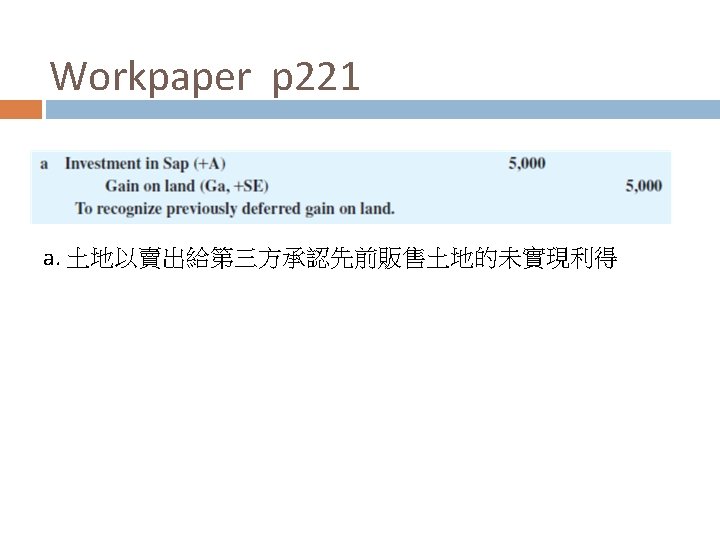

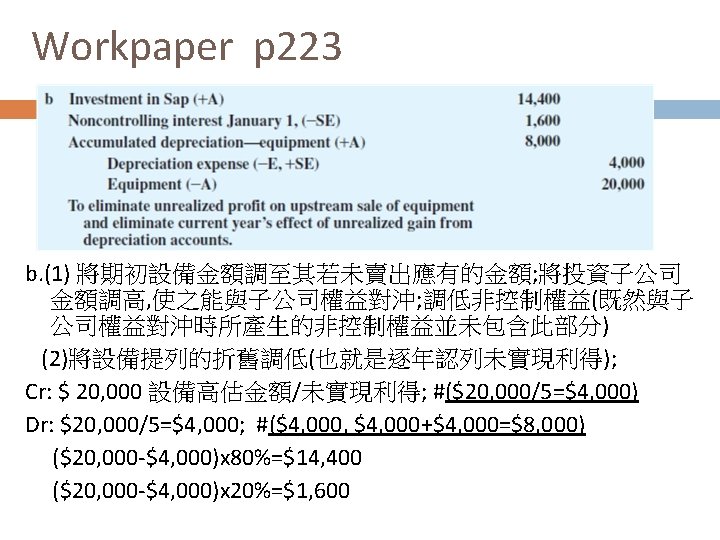

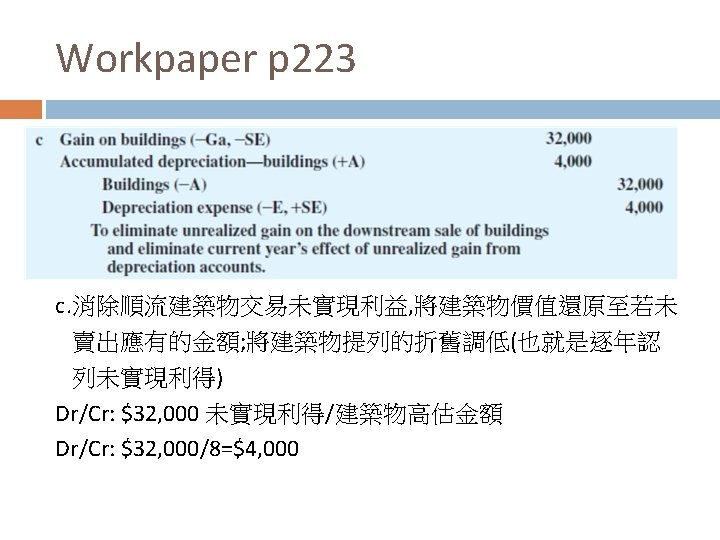

Consolidation Example- upstream and downstream sales of plant assets p 221 1. P acquire S 90% (book value= fair value) for $450, 000 on 1/3, 2011. 2. on 7/1, 2011, P sold land to S at a gain of $5, 000 S resold the land to outside entities during 2013 at a loss to S of $1, 000. 3. on 1/2, 2012, S sold equipment with a five-year remaining useful life to P at a gain of $20, 000. This equipment was still in use by P at 12/31, 2013. 4. on 1/5, 2013, P sold a building to S at a gain of $32, 000. The remaining useful life of the building on this date was 8 years, and S still owned the building at 12/31, 2013.

Equity Method p 221

Workpaper f. 對沖

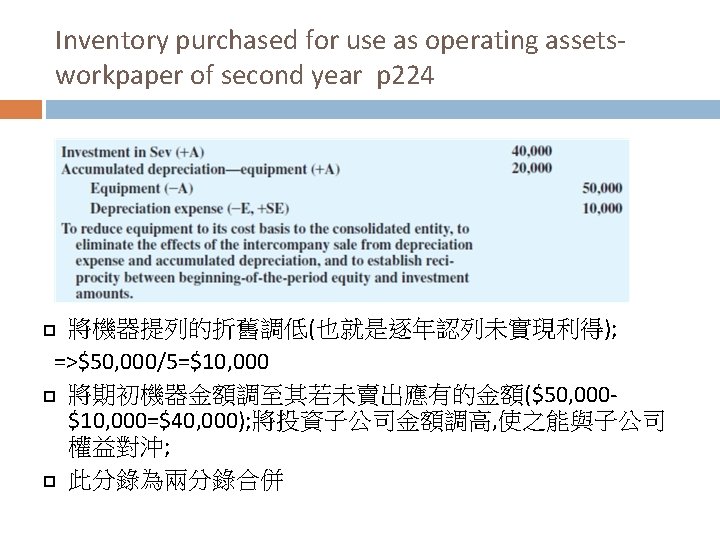

Inventory purchased for use as operating assets p 224 1. P sells a computer that it manufactures at a cost of $150, 000 to 100%-owned S for $200, 000. 2. The computer has a 5 -year expected useful life, (straight-line depreciation) 3. P’s separate income statement includes $200, 000 intercompany sales 4. S’s cost of sales does not include intercompany purchases, because the purchase price is reflected in its plant assets, and the $50, 000 gross profit is reflected in its equipment account.

Inventory purchased for use as operating assetsworkpaper of selling year p 224