PTA Finance Training 2018 SRV Council of PTAs

Fiduciary responsibilities Treasurer &")

•")

– in writing to")

10 to 90 days")

")

")

")

• Receives PTA money • Gives a receipt for")

• Audit the financial records: • mid-term and year-end •")

• Signs “Authorization for Payment” forms following approval. • Signs")

•")

“Two person” rule (not related or living together) – handling")

• Processing cash and checks received – “For Deposit Only”")

• “Cash Verification Form” (CVF) – Two person rule –")

ATM and Credit Cards • Never for purchases or withdrawals •")

Bank Statements School • Mailed to PTA address, not someone’s home")

Five Minute Audit of Bank Statements ü Online payments or ATM")

Reconcile Bank Statements • Bank balance Vs. Treasurer’s records Treasurer records")

2. Audit")

: • ledger of income and")

- Slides: 62

PTA Finance Training 2018 SRV Council of PTAs May 1, 2018 Training 2015 California State PTA Training Edited 05. 01. 2018 by Shirley Lapp, Auditor, SRVCPTA

Remember these points; you can look up everything else. 1. PTA is a Team. 2. PTA runs on other people’s money. 3. Do it the right way. 4. Share what you’re doing. 5. The Toolkit has the answers. 6. Ask for help

The Finance Team Association Members The Financial Secretary The Treasurer Board Members The President The Auditor

Financial Accountability Executive Board (Article V – election of officers) Fiduciary responsibilities Treasurer & Financial Secretary Handling, recording and reporting (Article VI – duties of officers) Auditor (Article VI – duties of officers) Monthly, bi-annual, and on-going

Association Responsibilities The association is the ultimate authority (Bylaws Article VIII, Section 3) • Approves programs • Approve the budget • Authorizes expenses • Releases budgeted funds to the board • Ratifies every check • Approves budget changes • Approves minutes

Association Meeting Notification (Corporations Code 7511 & Bylaws Article VII) – in writing to all eligible voters – place, date, time and general nature of business A Quorum Must be Established (and recorded in meeting minutes)

Association Meeting Notification (Corporations Code 7511 & Bylaws Article VII) 10 to 90 days notice: any time when action items will be presented 10 days notice: for changes in the time or date of a regular meeting 10 days notice: for special meetings; limited business for annual election meeting 30 days notice:

Board Responsibilities The board is subordinate to the association (Bylaws Article VIII, Section 3) • Fiduciary duties: care, loyalty, obedience, use of funds as intended by the donor. • Transparency duties: simple, complete & clear; descriptive account names & memos target the reader Accuracy: categorized and correct

Board Responsibilities The board is subordinate to the association (Bylaws Article VIII, Section 3) • Transacts business as authorized by the association • Authorizes payment of bills within budget limits • Authorizes payment of unbudgeted bills within approved limits

Board Responsibilities The board is subordinate to the association (Bylaws Article VIII, Section 3) • Create committees as needed • Fill vacancies in office • Present reports at association meetings

Financial Secretary (Bylaws Article V) • Receives PTA money • Gives a receipt for PTA money received • Deposits money into a PTA bank account • Gives a copy of the deposit slip to the treasurer • Records money received and deposits • Presents report at board and association meetings

Auditor (Bylaws Article V) • Audit the financial records: • mid-term and year-end • upon resignation of the treasurer or financial sec. • upon resignation of any check-signer • Present audit reports per schedule in bylaws • Verify the completion and filing of taxes • Recommended: 5 -minute audit of bank statements

President (Bylaws Article V) • Signs “Authorization for Payment” forms following approval. • Signs contracts that have been approved by association • May sign PTA checks after proper approval

Treasurer’s Reports The Budget-to-Actual “Treasurer’s Report” Annual Financial Report

Budget Receipts Estimated $1, 000. 00 Dues $32, 000. 00 Fundraiser #1 Total receipts: $33, 000. 00 Expenses $500. 00 Supplies $32, 500. 00 Field trips Total expenses: $33, 000. 00

Budget-to-Actuals Receipts Dues Fundraiser #1 Total receipts: Estimated Actuals $1, 000. 00 $32, 000. 00 $22, 000. 00 $33, 000. 00 $22, 300. 00 $500. 00 $400. 00 $32, 500. 00 $33, 000. 00 $3, 900. 00 Expenses Supplies Field trips Total expenses:

The BUDGET Process • assess the needs of the community (committee & board) • prepare the budget (committee & board) • adopt the budget (association) • change the budget (association) • release funds to the board (association) • report budget-to-actuals to the board

Budget-to-Actual Receipts

Budget-to-Actual Disbursements

Treasurer’s Report Previous balance on April 12, 2015 Income Dues Fundraiser #1 Total income: Expenses Check #500 - Supplies for book fair Check #501 – 3 rd grade field trip Total expenses Ending balance on May 12, 2015 $6, 510. 00 $1, 000. 00 $22, 000. 00 $23, 000. 00 $500. 00 $2, 500. 00 $3, 000. 00 $26, 510. 00

Treasurer’s Report

Treasurer’s Report

Annual Financial Report Income Membership Income Donations Total income: $1, 000. 00 $22, 000. 00 $23, 000. 00 Expenses Program expenses Operating expenses $20, 000. 00 $3, 000. 00 Total expenses $23, 000. 00

Annual Financial Report

Annual Financial Report

Remit to Council/District • membership count and dues monthly • a copy of the approved budget – Current Treasurer • a copy of the approved programs • a copy of the mid-term and year-end audits – Current Auditor • a copy of all government filings (990, RRF-1) – Current Treasurer • insurance premium (annually in the fall) • Workers’ Compensation Annual Payroll Report Revision Coming!

Receipts • • Receipts = Deposits = Bank Statement Receipts are anything of value that the PTA receives. 501(c)(3) status requires records of the source of all funds. Bulk entries are acceptable if supported by the detail. • Detailed Future Fund downloads (name, date, amount, purpose) • Searchable for IRS, deliverables, donation receipts, etc. • Check the financial reports for an entry labeled Undeposited Receipt or Unreceipted Deposit

Credit Card Payments • Financial Secretary balances the credit card payments 10. 00 -. 25 9. 75 Sales and Donations Donor’s Payment Amount Paid Post Receipts Revenue Post Deposit Fees Post Expense Payment – Fees = Processor reports Processor Deposit Bank Statement/Online Deposit • Treasurer balances the bank statement 9. 75 10. 00 Credit +. 25 Debit = Bank Reconciliation

Handling Receipts (money received) “Two person” rule (not related or living together) – handling PTA mail that contains money – handling donations and membership dues – handling cash at a PTA fundraiser

Handling Receipts (cont. ) • Processing cash and checks received – “For Deposit Only” & PTA bank account # – Record all cash and every check on a CVF – Attach adding machine tape totals to CVF

Handling Receipts (cont. ) • “Cash Verification Form” (CVF) – Two person rule – verify and sign CVF – Deposit / attach deposit slip to the form

Authorizing Payments • association “releases” the funds to board • board authorizes payments, • payee cannot authorize payments • president/secretary sign Payment Authorization • treasurer writes check • association ratifies checks

Writing Checks • “Two person” rule –payee cannot sign –signers may not be related or living together • Record checks in the register and ledger • Present a list of checks to association for ratification

Banking Deposits Cash – ALWAYS Checks – Deposit History Credit Cards – Detail List • Every deposit has a corresponding Cash Verification form signed by two people • Deposit is counted by two people – the depositor and the bank teller

Banking (cont. ) ATM and Credit Cards • Never for purchases or withdrawals • Deposit-only card is allowed

Banking (cont. ) Bank Statements School • Mailed to PTA address, not someone’s home • Request copies of checks written • Opened and inspected by an elected officer who isn’t authorized to sign checks.

Banking (cont. ) Five Minute Audit of Bank Statements ü Online payments or ATM withdrawals ü Two authorized signatures on every check ü Deposits and checks match reports

Banking (cont. ) Reconcile Bank Statements • Bank balance Vs. Treasurer’s records Treasurer records reflect real-time

Annual Government Filings Step 1: Prepare your Annual Financial Report You Can Do It! 990 N is fast & easy. Step 2: File with the IRS Gross receipts < $50, 000 990 N Gross receipts > $50, 000 990 EZ or 990 N & 990 Use an outside professional

Annual Government Filings Step 3: File with the FTB Gross receipts < $50, 000 199 N Gross receipts > $50, 000 199 Step 4: File with the AG RRF-1 & 990 EZ, 990

Insurance General liability $1, 000 Directors & officers $1, 000 Bonding Workers’ Compensation $15, 000 1 st $1, 000 is covered

There will be a new form for 2018 -19

Insurance • Follow the Green, Yellow, Red guide These pages are in the actual insurance policy • Follow all PTA financial and approval procedures

Appoint Committees Mid-term Audit pay insurance premium Mid-term Workers’ Compensation form remit dues monthly Assessments, Goals, Plans Preliminary Budget February March January • • • Approve End-of-term Audit Annual Financial Report Approve programs Approve fundraisers Adopt Budget Attend training April December Nov 1 st PTA Meeting Election May October Sept Start of school June August July Last PTA Meeting • Approve preliminary budget • Approve paying summer bills End of Term update bank account signatures end-of-term Audit nonprofit filings (990, 199, RRF-1) Annual Financial Report

Summary of Audit Steps 1. Collect the financial records (see audit checklist) 2. Audit the financial records 3. Make appropriate inquiry of treasurer as needed for clarification, revise as appropriate, with no surprises. 4. Meet with president and financial officers to discuss recommendations and corrections. 5. Complete and sign the Audit Report 6. Present to the board and to the association

Audit Checklist Collect the financial records (see audit checklist): • ledger of income and disbursements • checkbook registry • bank statements • treasurer’s reports • cash verification forms • payment authorization forms (w/ receipts, invoices, etc. • meeting minutes (board and association meetings)

Audit Checklist Verify STARTING BALANCES • • on bank statements on treasurer’s reports on check registry on budget

Audit Checklist Check BANK STATEMENTS • • reconciled monthly match treasurer’s reports match ledger match check registry

Audit Checklist Check MEMBERSHIP and DUES • verify amount collected • verify amount remitted to council or district PTA

Audit Checklist Check MINUTES REPORTS • all expenditures approved in board minutes • all expenditures approved/ratified in association minutes Check AUTHORIZATIONS FOR PAYMENT Check CASH VERIFICATION FORMS and bank deposits Check TREASURER REPORTS

Audit Report Fill in the Audit Report form, discuss with the treasurer and update the report and checklist as appropriate. Verify that taxes have been filed. Present the report to the board answer questions as needed. Present the report to the association. Any association concerns should be addressed confidentially by the board.

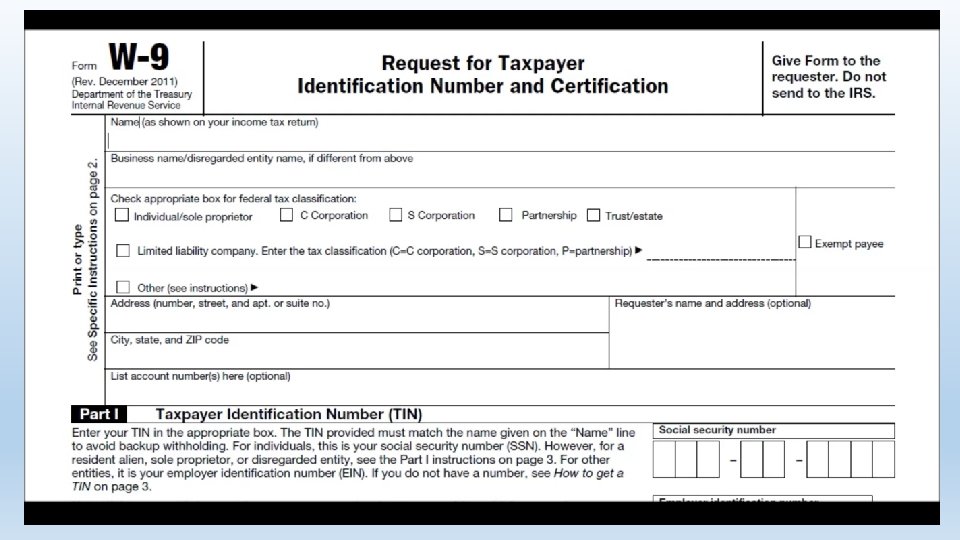

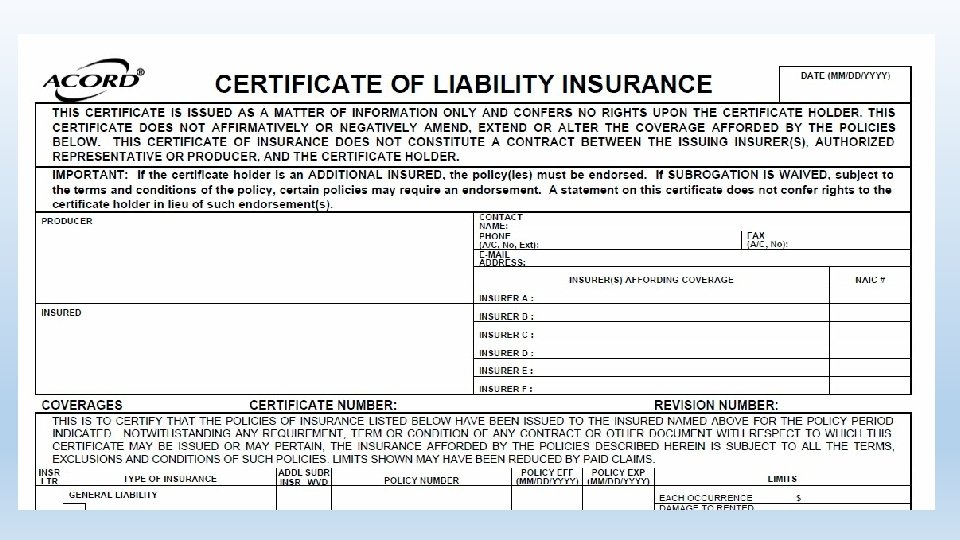

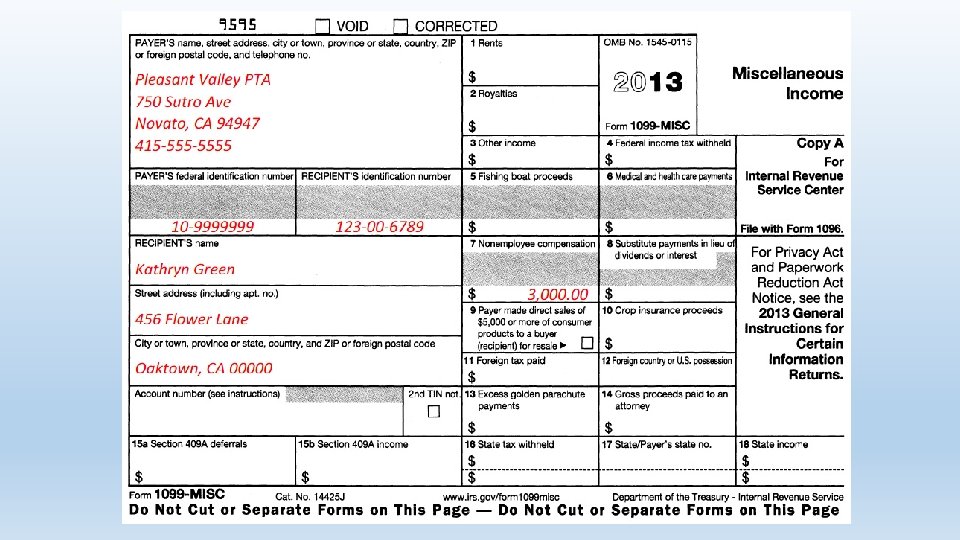

Paying Contractors BEFORE they get their check: 1. W-9 2. Certificate of Insurance 3. 1099 -MISC, online is very easy

Paying Workers PLEASE DON’T! Paying an employee 1. Register with State EDD 2. Personal Income Tax 3. State Disability Insurance

Paying Workers Paying an employee 4. Employment Training Tax 5. Unemployment Insurance 6. Payroll Tax Deposit

Paying Workers Paying an employee 7. Federal Income Tax 8. Social Security 9. Medicare Tax

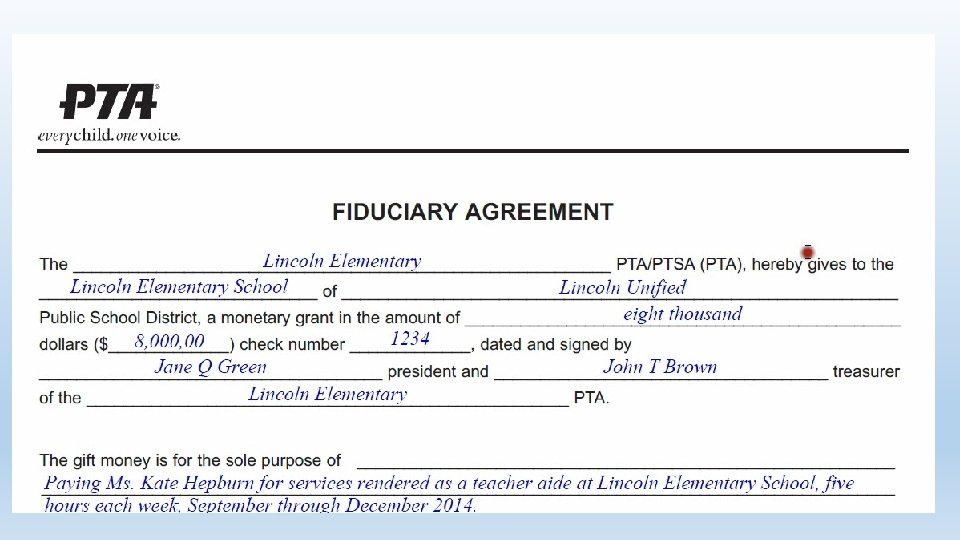

Paying Workers Paying for a school staff position 1. Deposit funds with the school district 2. Fiduciary Agreement form

Resources Running the PTA: http: //toolkit. capta. org/running-your-pta/table-of-contents/ Toolkit: http: //toolkit. capta. org/ Toolkit, Finance Chapter: http: //downloads. capta. org/toolkit/print/Finance. pdf Toolkit, Forms: http: //downloads. capta. org/toolkit/print/Forms. pdf Raffles: http: //oag. ca. gov/charities/raffles SRVCPTA: https: //srvcpta-ca. schoolloop. com/

CAPTA 2018 Convention Exhibits