Michael C Munger Director Philosophy Politics and Economics

\"Those of us who have looked to the self -interest")

. But our standard is different: externalities!")

")

")

Problem: Too much leverage, too little margin")

The reason this is correct in “all")

,")

and Freddy Mac")

— 90%")

: 3+ Trillions of")

- Slides: 82

Michael C. Munger Director, Philosophy, Politics, and Economics Program Duke University A TRAP BAITED WITH 3 KINDS O’TASTY CHEESE: REAL CAUSES OF PANIC 2008

Why have private financial corporations in the first place? Liquidity Prices Intermediation -transactions costs

A Question Should we bail out firms that are too big to fail?

The Question Should we bail out firms that are too big to fail?

The Question Should we bail out firms that are too big to fail?

The Question Should we bail out firms that are too big to fail?

The Question Should we bail out firms that are too big to fail?

Greenspan's Mea Culpa (10/23/08) "Those of us who have looked to the self -interest of lending institutions to protect shareholder's equity–myself especially–are in a state of shocked disbelief. . . I still do not fully understand why it happened and obviously to the extent that I figure where it happened and why, I will change my views. If the facts change, I will change. "

Why was Greenspan Wrong? The only reason we need a policy of bailing out losers is that we have a policy of bailing out losers. Greenspan assumed a limited kind of rationality. A "rational" investor would recognize that bailouts allow large losers to play with house money.

Why was Greenspan Wrong? Merton's distinction: Investors vs. Customers. FDIC and FSLIC: "bail out" customers of bad banks. Liquidity crisis protection Moral hazard (I look for high returns, don't care if bank is solvent) is real, but manageable.

Why was Greenspan Wrong? Merton's distinction needs to be expanded: Investor/Owners vs. Customers vs. CUSTOMERS. The bailout in 2008 -9 was a bailout of investors…in other firms that were major counterparties in exotic products (derivatives, CDS, CDO). Unlike moral hazard for traditional depositors, this moral hazard problem is not manageable, but unlimited.

Some definitions Bailout: The use of taxpayer funds either to buy assets, or to guarantee the value of assets, of insolvent firms.

Definitions: TBTF Systemically Important Financial Institutions SIFIs will always be bailed out Two features: Solvency/Size External effects of failure

Problem Systemically Important Financial Institutions: Externality more important than solvency SIFI status is therefore endogenous. Yes, investors lose, but competitive advantage in selling to CUSTOMERS My choices to select extra risk, and more leverage, make it more likely that my counterparties will be bailed out. Larger insolvency makes bailout MORE likely

Problem The “SIFI” designation is found in the Dodd-Frank legislation, and the language in that law says: (a) Liquidation required--All financial companies put into receivership under this subchapter shall be liquidated. No taxpayer funds shall be used to prevent the liquidation of any financial company under this subchapter. (b) Recovery of funds--All funds expended in the liquidation of a financial company under this subchapter shall be recovered from the disposition of assets of such financial company, or shall be the responsibility of the financial sector, through assessments. (c) No losses to taxpayers--Taxpayers shall bear no losses from the exercise of any authority under this subchapter.

Problem Mutual benefit: Exists a contract, or agreement, under which everyone would be better off. Looks like this: Governments will not bail out firms Therefore, firms choose best guess risk/leverage for portfolios Insolvency reflects bad production choices, prices allocate scarce resources accurately

Problem The Problem? That agreement, on previous page, is unenforceable, because the incentives facing the enforcer (the state) are timeinconsistent But we tried. Set up the Fed as a Lender of Last Resort Bagehot (1897), Lombard Street.

Bagehot's Lender of Last Resort Bail out only for liquidity crises, not equity. LLR Regs do 3 things: • Lend as much money as necessary directly to troubled banks • At a penalty rate • And only for good collateral (the institution must be technically solvent)

Problem III Lender of last resort Bagehot (1897). But our standard is different: externalities! The size of the externality has (at best) nothing to do with solvency, and may (at worst) be correlated with externality In other words, using size of externality causes larger externalities

Problem is Time Inconsistency "what to do once there is a crisis? " Answer: there would be no crises if we could credibly commit to a policy of no bailouts. (Might or might not be true, need empirical cases) Ann is right, of course, in 2008 -9. But what now?

Here is Circe’s dire warning to Odysseus (Chapman 2000: Chap. XII, lines 56 -89; emphasis added): Sail by them therefore, thy companions First to the Sirens ye shall come, that taint Beforehand causing to stop every ear The minds of all men, whom they can acquaint With sweet soft wax, so close that none may hear With their attractions. Whomsoever shall, A note of all their charmings. Yet may you, For want of knowledge moved, but hear thcall If you affect it, open ear allow Of any Siren, he will so despise To try their motion; but presume not so Both wife and children, for their sorceries, To trust your judgment, when your senses go That never home turns his affection's stream, So loose about you, but give straight command Nor they take joy in him, nor he in them. To all your men, to bind you foot and hand The Sirens will so soften with their song (Shrill, and in sensual appetite so strong) Sure to the mast, that you may safe approve How strong in instigation to their love His loose affections, that he gives them head. Their rapting tunes are. If so much they move, And then observe: They sit amidst a mead, That, spite of all your reason, your will stands And round about it runs a hedge or wall To be enfranchised both of feet and hands, Of dead men's bones, their wither'd skins and all Hung all along upon it; and these men Charge all your men before to slight your charge, And rest so far from fearing to enlarge Were such as they had fawn'd into their fen, And That much more sure they bind you. then their skins hung on their hedge of bones. .

Federal Trade Commission, Washington, DC

But…Did That Big Horse Get Loose, and Pull Us Off a Cliff? You’ve heard it: Worst economic downturn since the Great Depression (not remotely true, not even as bad as ‘ 73, or ‘ 81, in terms of GDP decline. ) Huge financial losses, bankruptcies of hundreds of companies Government bailouts (unprecedented!) Record postwar unemployment (okay, THAT’s true) WHY a crisis? Prices…No Prices, No Liquidity

Document Problem: House Prices

Stock Prices & Volume, ‘ 04 -’ 09

Unemployment Rates, end 2008

Unemployment Rates, end 2011

Unemployment Rates, 11/07– 4/09 2009

Three Deficits Federal Consumer Trade

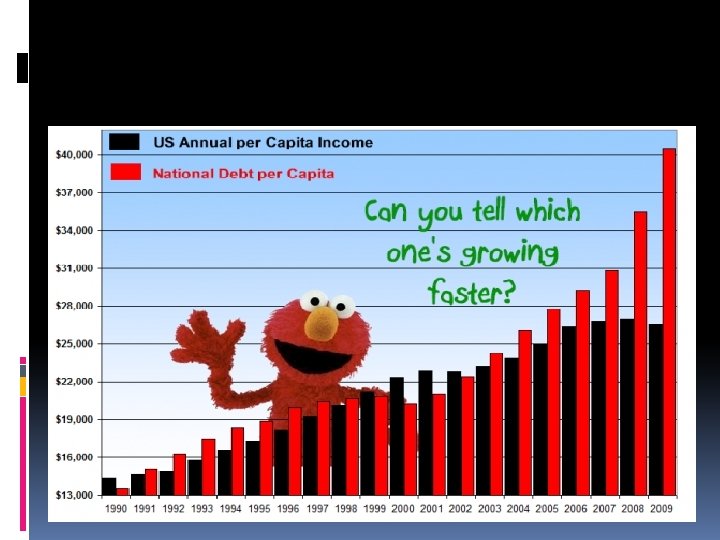

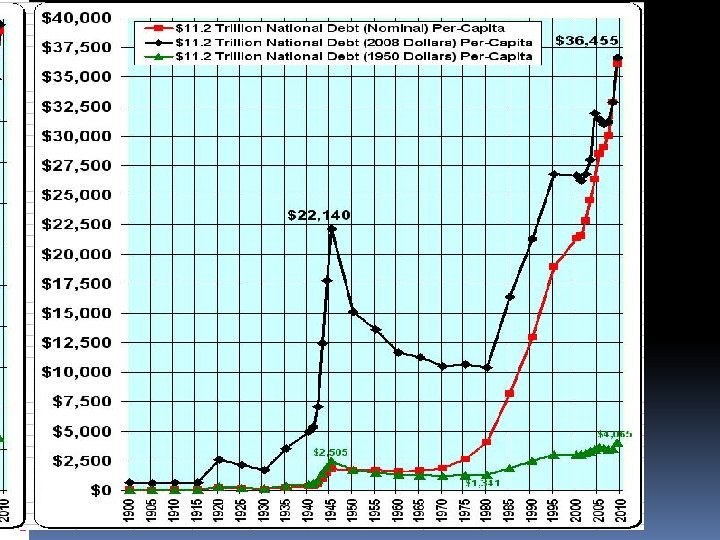

US Federal Debt/capita (‘ 07$)

110% is the Worry Line

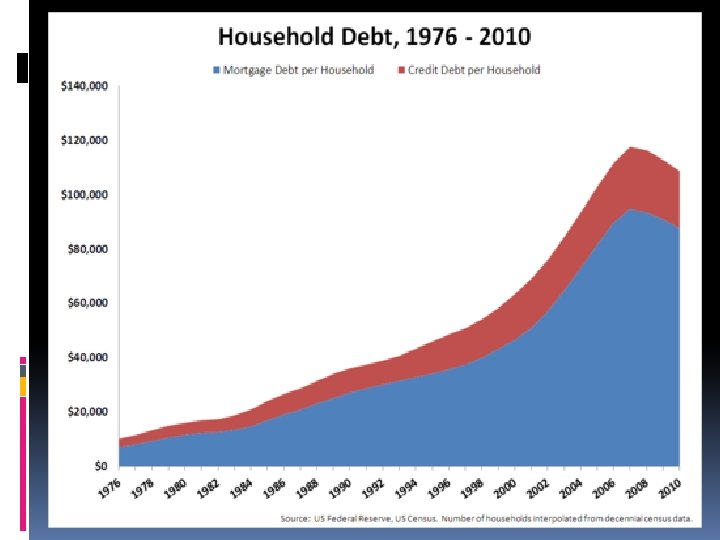

Consumer Debt

Student Loan Debt (US Gov’t)

Trade Deficit

Fiscal Deficit and Trade Deficit are CONNECTED

Competing Diagnoses 1. Greed, Especially Predatory Lending 2. Too Much Government Interference in Housing Markets 3. Too Little Government Regulation of Financial Markets 4. Too Much Debt, Not Enough Saving 5. Death Throes of a Dying Capitalist / Consumerist Order 6. Space Aliens (The “Cordato Thesis”) 7. Normal fluctuations of business cycle, exacerbated by policy mistakes. Inherent in capitalism

The Answer (correct in all unimportant respects…) Problem: Too much leverage, too little margin for error in investment and real estate markets. To take an example, a company with a net worth of US$ 25 billion borrowed 26 times its net worth and creates leveraged funds of US$ 650 billion to invest or lend them. When a small portion of the company's investments turns bad, as is the norm for the industry, the company's capital is under threat. To put things in perspective a 3. 8 percent misjudgment in their books was enough to wipe out their shareholders' capital of $ US 25 billion. And leverage ratios of 40, or 50, to 1 were not uncommon. Prudence? No more than 2 to 1. (May not be comparable, since derivatives seem different from borrowing outright)

The Answer (correct in all unimportant respects…) The reason this is correct in “all unimportant respects” is that it makes us want to ask: “WHY? WHY DID IDIOTS DO THAT? LET’S KILL THEM ALL!” Well, even in the U. S. being an idiot is not a capital crime. In fact, if you are a BIG idiot, the government will bail you out!

My View: A Trap Set by the US Government, and Baited with three types of tasty Cheese

For the first time in history, you could be trapped even if you never leave the house. Just a computer was enough…

Effective? Unfortunately… Each trap could catch many!

Hard Not to Feel Sorry for those poor mice…. But blaming markets for the financial crisis is a lot like blaming the CHEESE! The Bush Administration, and Clinton Administrations, did not realize they were setting a trap. But they were. This is a crisis where markets ran wild, and where government did nothing to control the problem. Government actually made things much worse than was necessary.

To Repeat: A Trap Set by the US Government, and Baited with three types of tasty Cheese

Many Traps--Three Kinds of Cheese, No Waiting!!!!! 1. Equity Purchase Subsidies 2. Artificially Low Interest Rates 3. Guarantee of Permanent Price Increases

1. Equity Purchase Subsidies: Homes Home ownership policy of Bush, also Clinton: Pay low -income people to make a risky investment that they would otherwise rationally avoid. Mortgage Agencies treated like “public utilities” (Bernanke, Paulson). Banks/financial entities both threatened, and bribed, to make loans that could not possibly be paid back. Community Development Block Grants: subsidize the down payment.

1. Equity Purchase Subsidies: Homes PROBLEM: Behavioral economics--people overestimate their prospects, poor people shouldn't take too much risk, because they have little to fall back on. The natural market tendency is too much home ownership, not too little. BACKGROUND: US Federal Reserve Bank Study on the dangers of Home Ownership Subsidies, (Published August of 2008!) http: //www. richmondfed. org/publications/research/region_focus/2008/fall/pdf/cover_story. pdf

1. Equity Purchase Subsidies: Homes Two New York Times Articles: I. “Fannie Mae Eases Credit To Aid Mortgage Lending, ” By STEVEN A. HOLMES, September 30, 1999: “In a move that could help increase home ownership rates among minorities and low-income consumers, the Fannie Mae Corporation is easing the credit requirements on loans that it will purchase from banks and other lenders…. In moving, even tentatively, into this new area of lending, Fannie Mae is taking on significantly more risk, which may not pose any difficulties during flush economic times. But the governmentsubsidized corporation may run into trouble in an economic downturn, prompting a government rescue similar to that of the savings and loan industry in the 1980's. ” Why do it? Clinton Admin and House Democrats…. .

1. Equity Purchase Subsidies: Homes Two New York Times Articles: II. “New Agency Proposed to Oversee Freddie Mac and Fannie Mae, “ By STEPHEN LABATON, September 11, 2003 The Bush administration today recommended the most significant regulatory overhaul in the housing finance industry since the savings and loan crisis a decade ago. . . The plan is an acknowledgment by the administration that oversight of Fannie Mae and Freddie Mac -- which together have issued more than $1. 5 trillion in outstanding debt -- is broken. . (Oxley): ''The current regulator does not have the tools, or the mandate, to adequately regulate these enterprises. We have seen in recent months that mismanagement and questionable accounting practices went largely unnoticed by the Office of Federal Housing Enterprise Oversight, '' the independent agency that now regulates the companies. (CONTINUED ON NEXT SLIDE)

1. Equity Purchase Subsidies: Homes Two New York Times Articles: II. “New Agency Proposed to Oversee Freddie Mac and Fannie Mae, “ By STEPHEN LABATON, September 11, 2003 Among the groups denouncing the proposal today were the National Association of Home Builders and Congressional Democrats who fear that tighter regulation of the companies could sharply reduce their commitment to financing low-income and affordable housing. ''These two entities -- Fannie Mae and Freddie Mac -- are not facing any kind of financial crisis, '' said Representative Barney Frank of Massachusetts, the ranking Democrat on the Financial Services Committee. ''The more people exaggerate these problems, the more pressure there is on these companies, the less we will see in terms of affordable housing. '' Representative Melvin L. Watt, Democrat of North Carolina, agreed. ''I don't see much other than a shell game going on here, moving something from one agency to another and in the process weakening the bargaining power of poorer families and their ability to get affordable housing, '' Mr. Watt said.

1. Equity Purchase Subsidies Government-guaranteed home mortgages, especially when a negligible down payment or no down payment whatever is required, inevitably mean more bad loans than otherwise. They force the general taxpayer to subsidize the bad risks and to defray the losses. They encourage people to “buy” houses that they cannot really afford. They tend eventually to bring about an oversupply of houses as compared with other things. They temporarily overstimulate building, raise the cost of building for everybody (including the buyers of the homes with the guaranteed mortgages), and may mislead the building industry into an eventually costly overexpansion. In brief, in they long run they do not increase overall national production but encourage malinvestment. (my emphasis) ~From Chapter VI "Credit Diverts Production" in Henry Hazlitt's "Economics in One Lesson, " first published in 1946

Artificially Low Interest Rates

Another Way of Computing It…

Artificially Low Interest Rates Why would this matter? Reasons: 1. Subsidy to long term borrowing 2. Subsidize risk-taking, lender of last resort 3. ARMs and Balloons: Nonstandard loans, because money was free

Guarantee of Permanent Price Increases If there is no risk, people take too many risks. Buy a house, zero down, 4 year lock-in of 4% interest, then balloon payment or ARM If house was $200, 000, and it appreciates at 5% per year, that’s more than $40, 000 capital gain. You can refinance, with a $40, 000 down payment and a standard fixed rate mortgage. It’s all free! And so housing prices went up forever…

Guarantee of Permanent Price Increases Example: Interview with Henry Paulson (T-Sec, 2006 -Jan 2009), in 2007: Paulson: “I think what we’re doing is avoiding a market failure that would have forced housing values down in a way that was not in the investors’ interest, and in a way that the market wasn’t intended to work. ” Interviewer: “How can you force values down? Why aren’t values finding their natural level? ” Paulson: “The way values would go down is, as I’ve said, you’d have market failure. ” [After Treasury Department intervention ] “we won’t have housing prices driven down in ways that distort the market. ” The Guarantee: Government SHOULD, and CAN, maintain orderly permanent increases in housing prices.

History: Four Influences How did it actually happen? I have said that the trap was baited with Equity purchase subsidies Artificially low interest rates Government guarantee of intervention to prevent “market failure” of housing price decline But how did the trap close? How did it actually happen? This is as simple as I can make it. Like any simple account, it leaves out a lot of important details. But, it captures the primary moving parts of the crisis.

History: 4 Influences, 4 Slides 1. SECURITIZED DEBT Fannie Mae (1938) and Freddy Mac (1970) set up to “rationalize” the mortgage market—”Securitize. ” At first, worked pretty well. Repackaged and commoditized mortgages, so that people with money could loan to people who wanted to borrow money. Didn’t need banks, except as intermediaries. Home ownership is highly illiquid debt; more extensive loan market, with reselling, allowed for increased liquidity among both borrowers and lenders. Reduced transactions costs, lower rates for borrowers, higher rates for lenders. Problems: Risk status endogenous, increase asymmetric information about repayment rates

History: 4 Influences, 4 Slides 2. INCREASE HOME OWNERSHIP, CONFIDENCE IN MANAGEMENT OF ECONOMY It seemed home ownership was the stairway to the American dream. Encourage home ownership through (a) tax subsidies, (b) explicit subsidies, (c) pressure banks and regulatory agencies to certify “subprime” loans as “conforming. ” Conforming loans require 20% downpayment and 30% cap on monthly income. Both relaxed by regulators, 1994 -1997. Problems: None, as long as home prices go up. But investors either didn’t know, or didn’t care, that regulators were expanding the definition of “conforming” loans. Appeared to be good loans, certified by government agencies as being investment grade assets.

US Homeownership Rates The new loan products are known as the combo / ballon loan, and have lower down payment requirements. Combo loans are the contract of choice for nearly 40% of new loans, explaining much of the increase in homeownership rate since 1994.

Longer Term…Home Owner Rates

At the same point in time, 1997, housing prices started to skyrocket in real terms. Before, housing had been a hedge against inflation, but wealth was built through accumulating equity. Now, with the new loan regime from the Congress and the Clinton administration, and Fred and Fan helping, there was a huge rush of cash chasing houses. US Homeownership Rates

“Real” Housing Prices

Housing Prices vs. CPI

Overall, Shiller Index Not hard to figure out… 1997

Buying vs. Renting

History: 4 Influences, 4 Slides 3. COLLATERALIZED DEBT OBLIGATIONS Collaterlized Debt Obligations (CDO)— 90% repayment rate means an accurate price for bundles, even if no one security could be priced accurately. Problems: 90% repayment rate is endogenous, assumed old regulatory structure. And assumed steady increase in home prices. When repayment rates plummeted, no idea how to price these very complex assets. Imagine what the bankers thought; they must have been incredulous! “We can certify these lousy risks as investment grade, and then we can sell them in bundles at full price to FM/FM, and then bear NO responsibility for anything that happens later? COOOOOL!”

Billions $ History: 4 Influences, 4 Slides

History: 4 Influences, 4 Slides 4. DERIVATIVES, especially Credit Default Swaps Similar to other “hedging” derivatives. “Invented” by JP Morgan analysts in 1997, in 2000 became exempt from most regulation. (Pres. Clinton supported). Like insurance, but NOT insurance. Needn’t own asset, not regulated, and no requirements for reserves or structures of hedged risk layoffs. Problems: “Insurance” aspect of these derivatives meant that no one cared about the underlying assets, and no one investigated repayment rates. And AIG (with its physicists) made huge amounts of money writing these contracts. But like a one-sided betting shop: did not hedge the risk. For many companies, their only assets were these swap contracts after the primary assets defaulted.

Credit Default Swaps

Now, Just One Slide: Cause? Bad regulation: Focus on identities rather than instruments. Market failure, government at least negligent, possibly complicit. CDS’s are NOT insurance. Really, really bad regulation: Government caused the crisis, by subsidizing housing prices, and using government prestige to hoodwink small investors. Certified junk as conforming, allowed fast resale at full price, facilitated by Freddy and Fanny. “Investment houses” turned into “Animal Houses. ” The dilemma: Bad regulation can be worse than no regulation. But good regulation is better still. Test: When you say, “Government should regulate markets, ” take out the word “Government” and substitute “Politicians. ” You sure you still believe that? Confidence, Transparency, Liquidity required for accurate pricing and functioning markets

What Has Obama Administration Done? TARP (carried over from Bush Administration): 3+ Trillions of $? Porkulus (Stimulus for Reelecting Congressmen): Again, 3+ Trillion $ (If not temporary) He is NOT George Bush, a positive worldwide Proposed new regulations of executive compensation “Stress tests, ” not a bad idea, because they finesse “mark to market” valuation Takeovers of large manufacturers, directing bankruptcy Proposed “Financial Product Safety Commission”

What SHOULD have been done? 1. The George W. Bush presidency was not an era of deregulation, but overregulation and failed financial supervision. Sarbanes-Oxley, “ 10, 000 Commandments, ” attempts to prop up housing prices. So, Republicans were primary cause. 2. Don’t bail out! At most, offer lender of last resort function for banks, and liquidity of last resort function for CDOs. 40 cents on the dollar, take it or leave it. Bailing out AIG was just pouring money down a rat hole. Now, again for PIGS? Amazing.

What SHOULD have been done? 3. Stop changing things. Why is unemployment so high? Why won’t banks lend? It’s because no one knows what is going to happen to taxes, regulations, or health care. Regime Uncertainty: regime uncertainty pertains to the likelihood that investors’ private property rights in their capital and the income it yields will be attenuated further by government action. Such attenuations can arise from many sources, ranging from simple taxrate increases, to the imposition of new kinds of taxes, to outright confiscation of private property. Many intermediate threats can arise from various sorts of regulation, for instance, of securities markets, labor markets, and product markets. In any event, the security of private property rights rests not so much on the letter of the law as on the character of the government that enforces, or threatens, presumptive rights. (Higgs, 1997, Independent Review)

What SHOULD have been done? 4. Depend on greed and information to get us out of this. If banks are self-interested, not necessary to bribe them to make loans. 5. Stop politically motivated industry take-overs. Buying debt may be justified (though I’m skeptical. ) But buying debt is WAY better than buying, or seizing, equity shares. 6. Announce freeze on new regulations, and end constant threats of new taxes on profits.

What Will Happen Now? US Securities based on risky mortgages are what toppled financial institutions but it was the government that made the mortgages risky in the first place, by making homeownership statistics the holy grail, for which everything else was to be sacrificed, including commonsense standards for making home loans. Politicians and bureaucrats micro-managing the mortgage sector of the economy is precisely how today's economic disaster began. Why anyone would think that their micromanaging the automobile industry, or executive pay across a wide sweep of other industries, is likely to make things better in the economy is a mystery. THOMAS SOWELL, “Cheap Political Theater, ” http: //townhall. com/columnists/Thomas. Sowell/2009/03/24/cheap_political_theater