GST Goods Services Tax Cracking the GST Code

")

• Replace central Excise Duty &")

Sr. No. Particular Intra-State Inter-State Present GST 1. Initial Value")

Sr. No. Particular Intra-State Inter-State Present GST 1. Initial Value")

- Slides: 65

GST – Goods & Services Tax Cracking the GST Code… G – Getting S – Simplified Learning Partner’s T – Tax

Agenda: ü Getting Familiar with GST ü Impact on Dealers of Pesticides, Fertilizers & Agro üPlanning for Future Business / Implementation Challenges ü Accounting Software / IT Systems ü Compliances & Assessment Procedures ü Impact on Pricing

Learning Outcome: At the end of this course, Dealers will be able to achieve the following: üUnderstand various concepts of Goods & Service Tax üUnderstand the impact of new regulation on distribution of pesticides and kind of changes needed to be done üGain an insight on the recording and analyzing the transactions for compliance under GST especially in supply chain & distribution üGetting familiar with the technology and the flow of return filing under GST üKnowing “place of supply rules” and applicability of the same under GST

Ready to Race: On Your Marks Get Set Go • Registration & getting GST Number • Understanding the law and making changes in pricing & invoicing • Learning how to file returns & pay taxes • Setting up the new accounting system under GST

Existing Tax Structure in India Existing Tax Structure Indirect Tax Direct Tax Incom e Tax Wealth Tax Excise Central Tax Service Tax State Tax Custom VAT Entry Tax, luxury tax, Lottery Tax, etc.

Proposed Tax Structure in India Proposed Tax Structure Indirect Tax = GST (Except customs) Direct Tax Income Tax Wealth Tax Intra- state CGST (Central) SGST (State) Inter State IGST (Central)

Key Taxes Subsumed Excise Duty on MRP Service Tax CVD SAD Addnl. Excise Duties Central Excise Duty Taxes on lotteries, betting, gambling Cesses and surcharges on goods and services Surcharg es Central Cesses Luxury Tax Entry Tax (not Octroi) Entertainment Tax (except levied by local bodies) State VAT/Sales Tax CST TO BE PHASED OUT Dual GST

Likely GST Model Import GST Service Tax Other State levies Entry Tax/Octroi Central Excise Value Added Tax . Central GST . IGST State GST

Basis of Charge: • Excise is on? “Manufacture” • VAT is on? “ Sale” • GST will be on? “Supply”

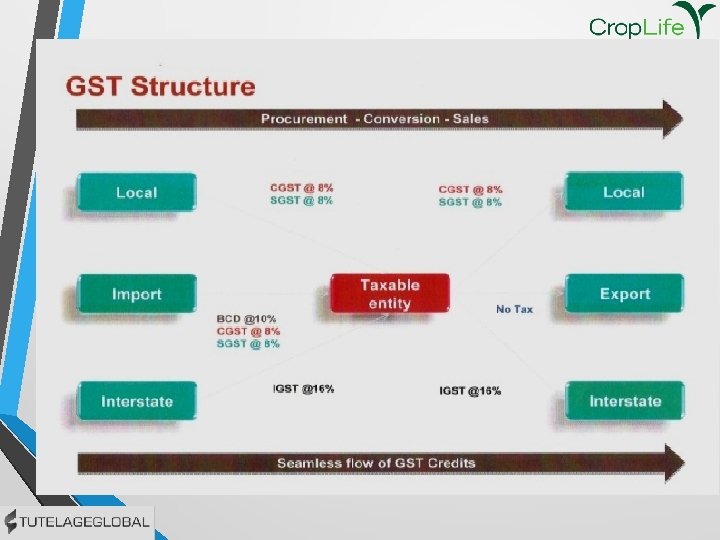

What is GST? IGST CGST SGST ü A new law which simplifies indirect tax in India ü For Crop Life Channel Partners, VAT will now become GST

Model / Components of GST CGST (Central GST) • Replace central Excise Duty & service Tax. • Cover Sale transaction • Administered by CG • Further it is expected that the duty and tax paid on closing stock would be available as credit. • Levied on all intra-state sale/supplies of goods or services. SGST (State GST) • Replace State Vat, Entry Tax, Entertainment Tax, & Luxury Tax. • Cover taxing of Services • Administered by SG • Rate can be a bit higher than CGST rate. • It is expected that the duty and tax paid on closing stock would be available as credit. • Levied on all intra-state sale/supplies of goods or services. IGST (Inter-State GST) • Levied on all inter –state supplies of goods or services which are sold or transferred. • Applicable to imports of goods or services. • Expected to be equal to CGST as well as SGST. • It is expected that the duty and tax paid on closing stock would be available as credit.

Operational Areas to be impacted by GST- CMA’s to play significant role Procurement and Sourcing Current & Future investments Sales and marketing Human Resource Distribution Accounting Logistics Product Pricing Working Capital Profitability

Benefits: • Single Window Scheme • Officers have powers across laws • No GST on farmer selling farm produce • Most Compliances online

Set off of GST Credit IGST Debit IGST Credit CGST Debit SGST Debit

Limits & Other Details • Registration over Turnover of 20 Lacs & 10 Lacs in North Eastern States • Composite Scheme for traders, select manufacturers & restaurants up to 75 lacs • State-wise Single Return to be filed • Most items will get Input Tax Credit (ITC) to avoid Tax on Tax • Exporters to get 80 % refund in seven days

Applicable Rates under GST 12% 18% 5% 28% 0%

Registration Under GST

Likely challenges for tax payers A new tax law – a whole lot of tax controversies Transaction restructuring § Transaction structuring to be reviewed § Procurement pattern and trading models to be analysed – No significant difference between local and interstate under GST? § Billing patterns, local vis-à-vis inter state to be reviewed Transition Costing / Pricing of goods § Transition of credits § Overall pricing of goods – factoring of GST credits § New registrations § Change in contract clauses § Change in rate of taxes § Review of procurement costs § Taxability of transactions spread across regimes Compliance § Treatment of tax paid § Tax computations inventory § New formats for invoices / Re-designing of the entire ERP Records/ Accounting § State-wise sales records § Credit availment and utilization records § Current ERP is aligned as per the current taxes records/ returns/ declarations § Validity of statutory form (Form F/Form C) § Manner of payment of taxes § Change in accounting § New compliance dates § Re-defining the logics § Documentation for § Updating masters movement of goods

How to Register…!!!

Initial Registration

Documentation Checklist

Other Important Points

Migration Process of GST

Registration Liability to Register in GST : Every supplier shall be liable to be registered under this Act in the State from where he makes a taxable supply of goods and/or services if his aggregate turnover in a financial year Region Aggregate Turnover North East India + Sikkim Rs 10 Lakhs Rest of India Rs 20 Lakhs Note: The Aggregate Turnover shall include all supplies made by the taxable person, whether on his own account or made on behalf of all his principals. 25

Migrating to GST Currently registered under VAT/CST Ø All dealers registered with central or state tax authorities and having a valid PAN will be allotted by VAT dept/Excise/Service Tax with a provisional GST no and password. Ø Dealer is required to login website https: //www. gst. gov. in using the ID and Password. Ø Existing Tax payers will be auto-migrated and given a 15 digit provisional PAN based GST ID with following structure. State Code PAN No of Tax Payer Entity Code Blank Check Digit 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 2 7 A A A C T 1 5 0 7 C 1 Z X Ø Using the ID and Password the taxpayer can complete the migration process as per direction by system.

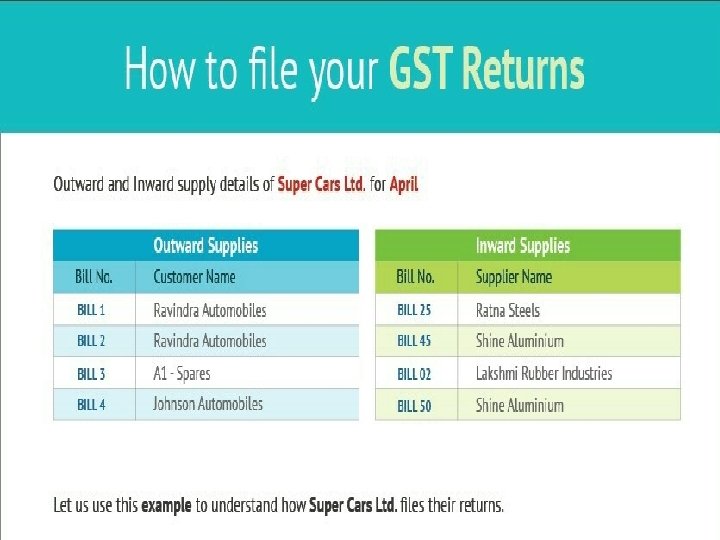

Filing GST Returns

Various Forms Under GST

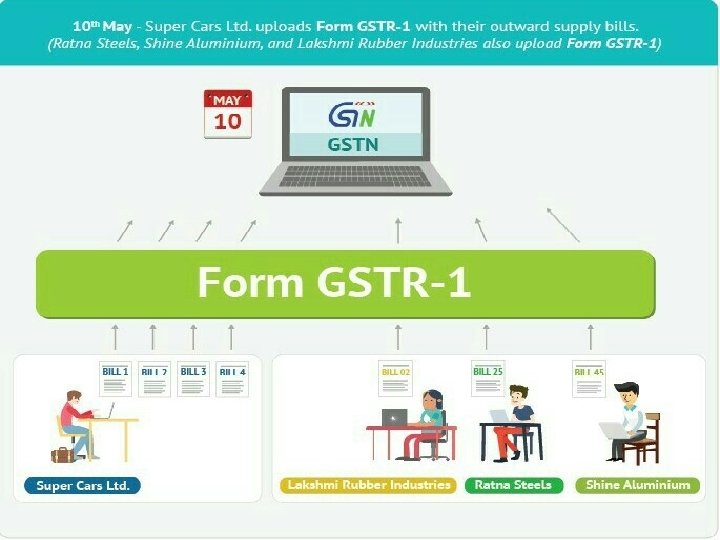

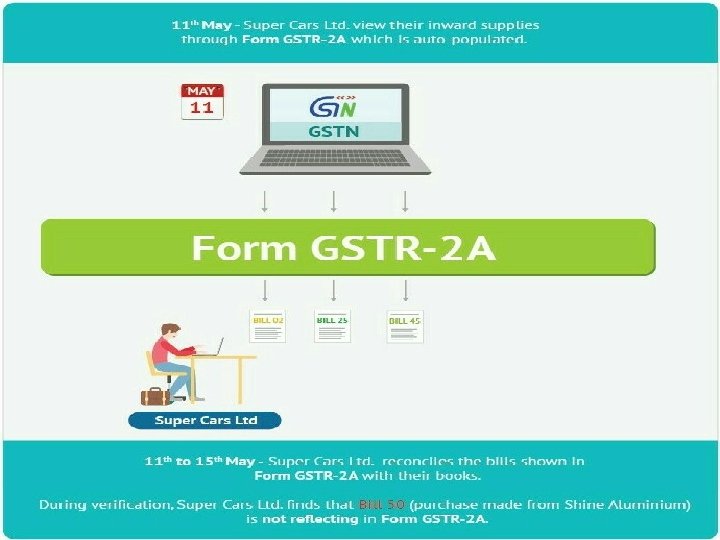

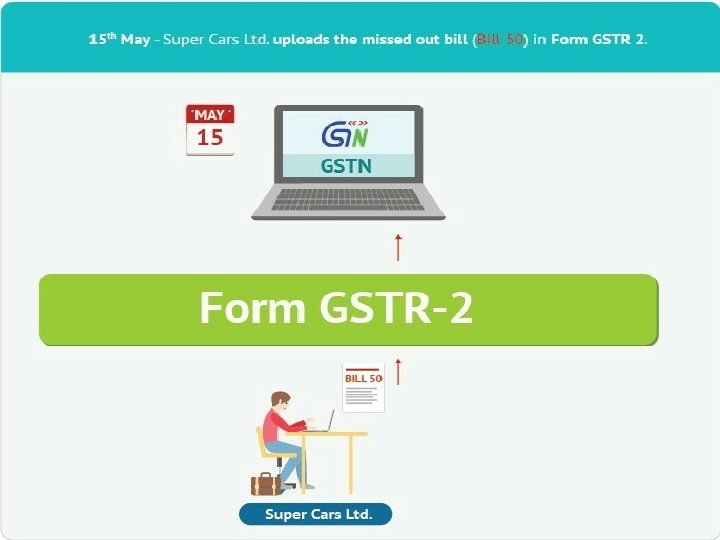

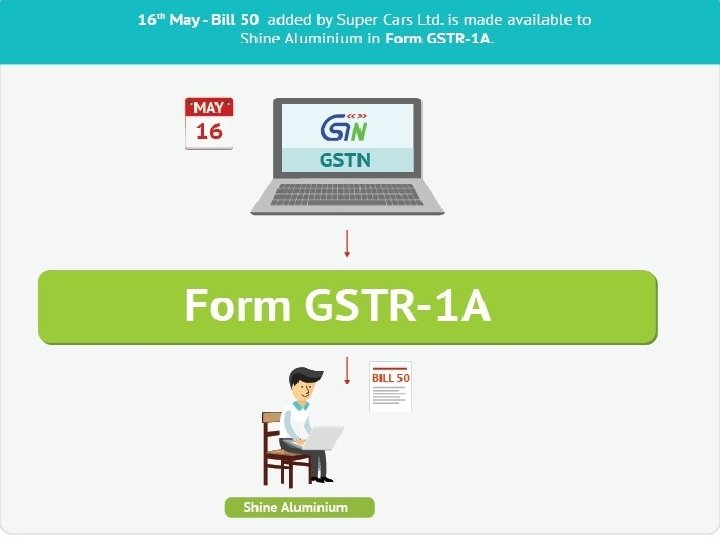

Form Type Frequency Due Date Details to be Furnished Form GSTR-1 Monthly 10 th of succeeding month Furnish details of outward supplies of taxable goods and/or services affected Form GSTR 2 A Monthly On 11 th of succeeding Month Form GSTR-2 Monthly 15 th of succeeding month Auto-populated details of inward supplies made available to the recipient on the basis of Form GSTR 1 furnished by the supplier Details of inward supplies of taxable goods and/or services for claiming input tax credit. Addition (Claims) or modification in Form GSTR-2 A should be submitted in Form GSTR-2. Form GSTR 1 A Monthly 20 th of succeeding month Form GSTR-3 Monthly 20 th of succeeding month Details of outward supplies as added, corrected or deleted by the recipient in Form GSTR-2 will be made available to supplier Monthly return on the basis of finalization of details of outward supplies and inward supplies along with the payment of amount of tax Form GST ITC- Monthly 1 — Communication of acceptance, discrepancy or duplication of input tax credit claim Form GSTR 3 A — — Notice to a registered taxable person who fails to furnish return under section 27 and section 31 Form GSTR-9 Annually 31 st Dec of next fiscal Annual Return – furnish the details of ITC availed and GST paid which includes local, interstate and import/exports.

Composite Tax Payer Return Frequency Type Form GSTR Quarterly -4 A Due Date Details to be Furnished — Details of inward supplies made available to the recipient registered under composition scheme on the basis of Form GSTR-1 furnished by the supplier Form GSTR Quarterly -4 18 th of succeeding month Furnish all outward supply of goods and services. This includes auto-populated details from Form GSTR-4 A, tax payable and payment of tax. 31 st Dec of next fiscal Furnish the consolidated details of quarterly returns filed along with tax payment details. Form GSTR -9 A Annual

Aggregate T/O exceeding One Crore Return Frequency Due Date Type Form Annually GSTR 9 B Details to be furnished Annual, 31 st Dec Reconciliation Statement – of next fiscal audited annual accounts and a reconciliation statement, duly certified.

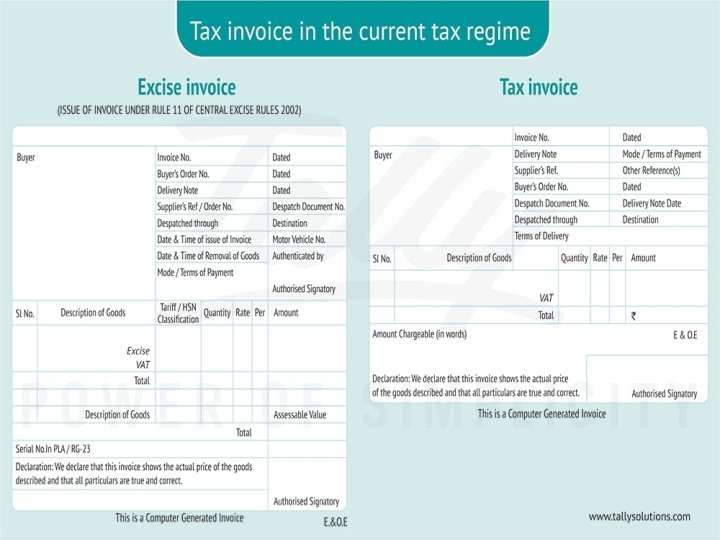

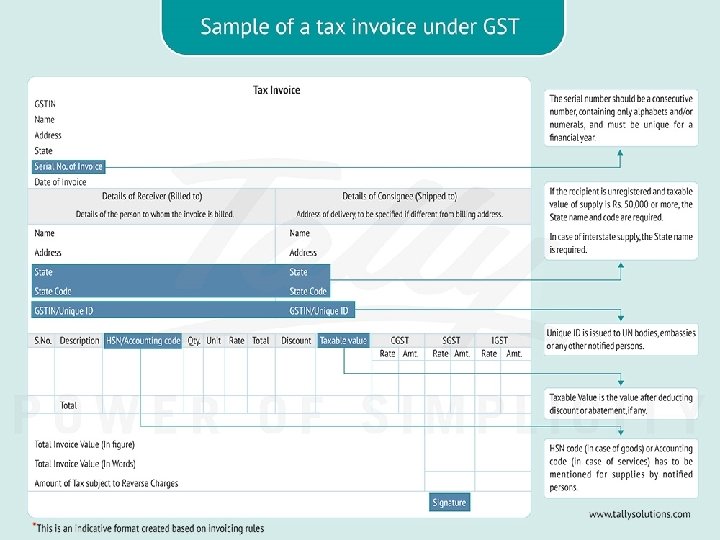

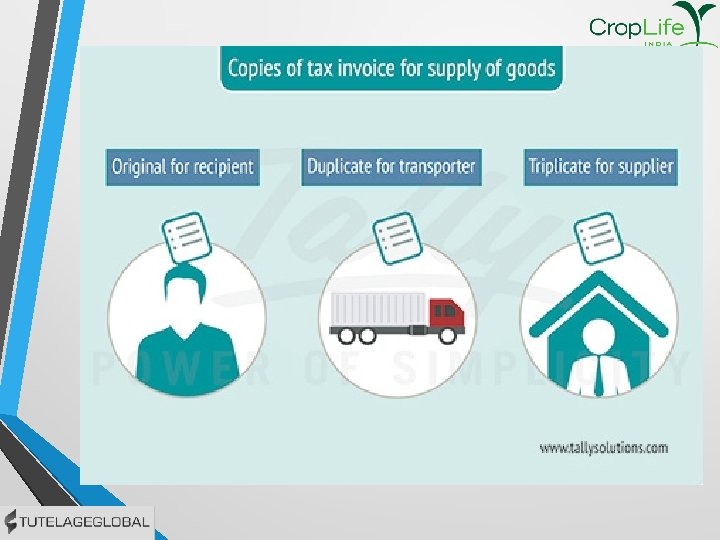

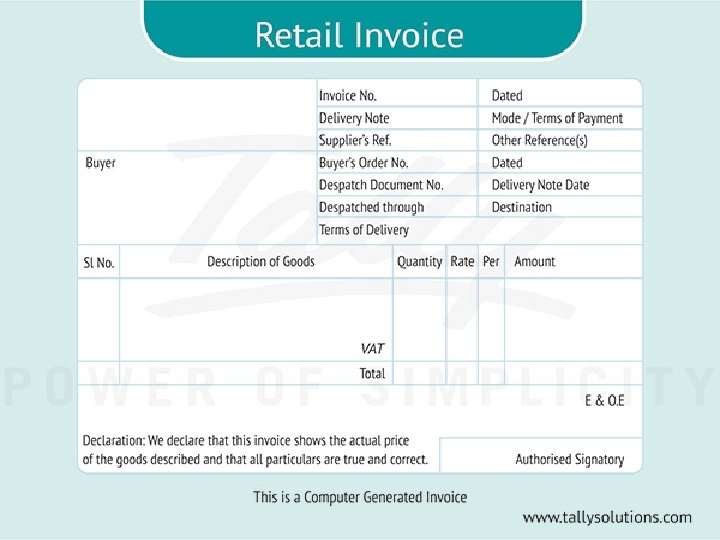

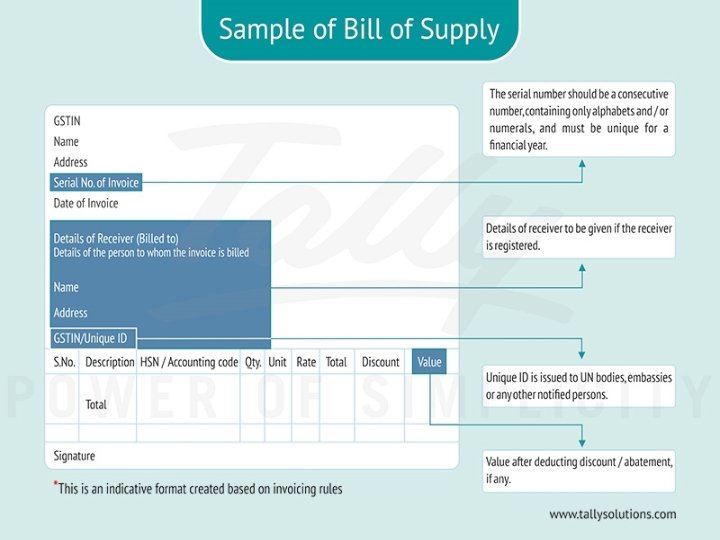

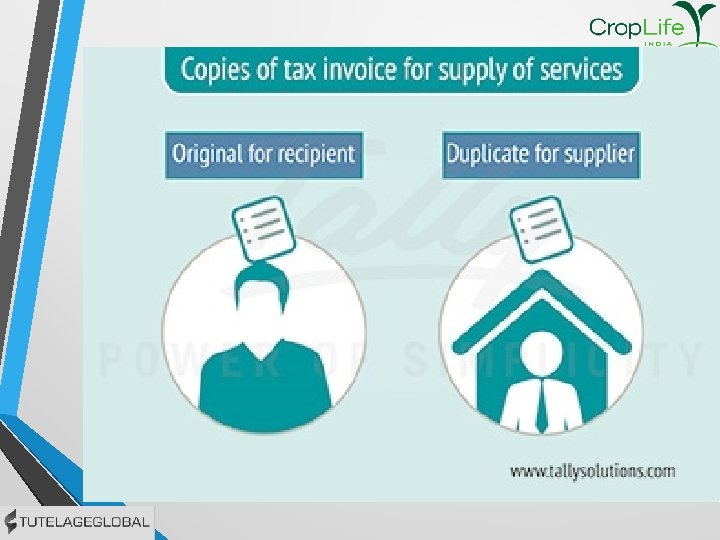

Invoicing Under GST Changes in how invoices are made under GST

Pricing Under GST What happens to Pesticides/fertilizer prices under GST?

Comparison (Trade of Goods) Sr. No. Particular Intra-State Inter-State Present GST 1. Initial Value 121. 00 120. 00 121. 00 120. 00 2. Centre’s Tax 11. 00 12. 10 11. 00 12. 22 3. State (X)’s Tax 13. 31 12. 10 11. 00 1. 10 4. State (Y)’s Tax - - 16. 91 12. 22 5. State’s Total 13. 31 12. 10 27. 91 13. 32 6. Total Tax paid to Govt. 24. 31 24. 20 25. 54 7. Non-Vatable Tax borne by Business Final value paid by Consumer 11. 00 0. 00 38. 91 – Refund Claim 25. 00 146. 41 145. 20 152. 97 8. 1. 10 45 146. 65

Comparison (Trade of Service) Sr. No. Particular Intra-State Inter-State Present GST 1. Initial Value 110. 00 120. 00 2. Centre’s Tax 11. 00 12. 10 3. State (X)’s Tax 0. 00 11. 00 0. 00 4. State (Y)’s Tax - - 0. 00 12. 10 5. State’s Total 0. 00 11. 00 0. 00 12. 10 6. Total Tax paid to Govt. 11. 00 22. 00 12. 10 24. 20 7. Non-Vatable Tax borne by Business 0. 00 8. Final value paid by Consumer 121. 00 132. 00 133. 10 145. 20

Existing Tax Structure Vs GST Sale from Factory - Warehouse – Dealer / Sale from Factory – Dealer (pesticides) Under Existing Tax Structure Sales Price Excise Duty@12. 5% on MRP Amount in ₹ 280. 00 Under GST Regime Sales Price Amount in ₹ 280. 00 37. 5 CGST @ 9% 25. 2 Sub-Total 317. 5 SGST @ 9% 25. 2 VAT @ 6% 19. 05 Purchase Price for Dealer 336. 55 Cost to Dealer (GST ITC Rs 50. 4) Cost to Dealer (VAT Credit Rs 19. 05) 317. 05 Margin 10. 00 Sub Total 330. 4 280. 00 10. 00 290. 00 Sub Total 327. 05 CGST @ 9% 26. 1 VAT @ 6% 19. 62 SGST @ 9% 26. 1 Sale Price of Dealer VAT Payable by Dealer(19. 62 -19. 05) Service availed Service Tax @15% 346. 67 0. 6 Sale Price of Dealer GST Payable by Dealer(52. 2 -50. 04) 10. 00 Service availed 1. 50 GST @ 18% Dealer Can’t avail Credit of Rs 1. 50 on Service 342. 2 1. 8 10. 00 1. 80 Dealer Can utilized ITC of Rs 1. 80 paid on Service availed

Input Tax Credit Conditions for availing Input Tax Credit Ø Under the GST regime, input tax credit can be availed by every registered taxable person on all inputs used or intended to be used in the course of or furtherance of business.

Input Tax Credit “Capital goods” means goods, - the value of which is capitalised in the books of accounts - used or intended to be used in the course or furtherance of business “Input” means - any goods other than capital goods - used or intended to be used in the course or furtherance of business “Input service” means - any service used or intended to be used in the course or furtherance of business “Input tax" in relation to a taxable person, means - the IGST, including that on import of goods, - CGST and SGST charged on any supply of goods or services to him - includes the tax payable under Reverse Charge - but does not include the tax paid under Composition Levy

Impact of GST on retailer List of Input Tax Credit available to Tax Payer: Every registered Taxable Person can avail Input Tax credit on below mentioned purchase of goods and services received for the furtherance of business. 1) GST paid on Cement Purchase 2) GST Paid on purchase on Capital Goods ü ü Motor Vehicle procured for transportation of Goods. ü ü ü ü Godown Rent Furniture, Fixture, Computer, Printer and other office equipment. 3) GST Paid on various Services Telephone Bill Internet Bill Security Service Manpower Service General Insurance Agent Commission Any other Services availed for business

Utilization of Input Tax Credit ØEvery Registered Taxable Person shall be entitled to take credit of input tax in his return and such amount shall be credited to his electronic credit ledger. ØThe Registered Taxable Person shall utilize the Input Tax Credit as the manner explained in below mentioned table. ITC First - Set Off Balance - Set Off Can not be utilized CGST IGST SGST IGST CGST / SGST -

Late Fees, Interest & Penalties under GST

Late Fees Offence Late Fee A person fails to furnish details of Rs. 100 for every day during which the outward or inward supplies, monthly failure continues, subject to a return or final return by the due date maximum of Rs. 5, 000 A person fails to furnish the annual Rs. 100 for every day during which the return by the due date failure continues, subject to a maximum of quarter percent of the person’s turnover in the state where he/she is registered

Interest Offence Interest A person liable to pay tax fails to pay Interest on the tax due will be the tax calculated from the first day on which the tax was due to be paid A person makes an undue or excess Interest on the undue excess claim or claim of input tax credit or undue or excess reduction in output tax liability A recipient of a service fails to pay to Interest on the amount due will be the supplier of the service the added to the recipient’s liability amount towards the value of the service, along with tax payable thereon, within 3 months from the date of issue of invoice by the supplier

Cancellation of Registration The circumstances under which a person’s registration will be cancelled are: • A regular dealer has not furnished returns for a continuous period of 6 months. • A composition dealer has not furnished returns for 3 quarters. • A person who has taken voluntary registration has not commenced business within 6 months from the date of registration. • Registration has been obtained by fraud, willful misstatement or suppression of facts.

Penalties Offence If a person: Supplies goods and/or services without issuing an invoice or issues an incorrect or false invoice Issues an invoice without supply of goods and/or services Collects tax but fails to pay the same to the Government beyond a period of 3 months from the date on which the payment becomes due Who is an e-commerce operator fails to collect tax or collects lesser than the amount required to be collected or fails to pay the tax to the Government Takes input tax credit without actual receipt of goods and/or services either fully or partially Obtains refund of tax by fraud Falsifies or substitutes financial records or produces fake accounts and/or documents or furnishes a false return Liable to be registered, but fails to obtain registration Furnishes false information with regard to registration Transports taxable goods without documents Suppresses turnover leading to evasion of tax Fails to maintain books of accounts and documents Issues an invoice or document by using the identification number of another person Interest Rs. 10, 000 or an amount equivalent to the tax evaded

Penalties A person who aids or Penalty may extend to abets any of the offences Rs. 25, 000 listed above Any offence for which a Penalty may extend to penalty is not separately Rs. 25, 000 provided under the law

Penalties Offence Imprisonment Commits or abets the following: 6 months imprisonment with fine Obstructing or preventing any officer in the discharge of his duties Tampering with or destroying any evidence or documents Failing to supply any information required of him under the law or supplying false information Tax evaded or input tax credit wrongly availed Imprisonment which may extend to 1 year with or refund wrongly taken of an amount fine exceeding Rs. 50 Lakhs, but not exceeding Rs. 1 Crore Tax evaded or input tax credit wrongly availed Non-bailable imprisonment which may extend to or refund wrongly taken of an amount 3 years with fine exceeding Rs. 100 Lakhs, but not exceeding Rs. 2. 5 Crores Tax evaded or input tax credit wrongly availed Non-bailable imprisonment which may extend to or refund wrongly taken of an amount 5 years with fine exceeding Rs. 2. 5 Crores

Accounts and Records Ø Every registered taxable persons shall keep and maintain a true and correct account of, 1. 2. 3. 4. 5. Inward supply of Goods or Service Outward Supply of Goods or Service Stock of Goods Input Tax Credit availed Output Tax Payable and Paid Ø The Registered Taxable person may keep and maintain such accounts in the electronic form. Ø Every registered taxable person required to keep and maintain books of account or other records shall retain them until the expiry of 60 months from the due date of Annual Return for the year such records pertaining. 59

Possible Risk Company Uploads Outward Supply Dealer Uploads Outward Supply Correctly Possible risk for Unregistered Retailer Registered Retailer correctly upload his Inward Supply Unregistered Retailer doesn’t upload The Supply Chain breaks at Unregistered retailer ØGSTN can easily track the purchases made by Unregistered retailer. ØGovt officials may impose huge penalty incase if they found that the retailer is liable to register but not registered.

Electronic Ledgers Register type Type of Form Description Electronic Tax GST PMT – 1 üAll liabilities of a taxable person shall be recorded and liability Register maintained. üAny liability under GST Act will be recorded by debiting the electronic tax liability register. üRegister shall be credited on discharge of or reduction in liability due to any other reason. Electronic Credit GST PMT – 2 üIt shall be credited on availment of Input tax credit or re. Register credited in case of rejection of refund claim. üCredit shall be debited when the credit is utilized to discharge tax liability or the refund of unutilized credit. Electronic Cash GST PMT – 3 üIt will be credited once amount is deposited in it. Register üAmount credited shall be utilized for payment of tax, interest, penalty, fee or any other payment. Identification for each Payment transaction üA UIN shall be generated at the Common Portal for each debit or credit to the electronic cash or credit ledger. üThe UIN relating to discharge of any liability shall be indicated in the corresponding entry in the electronic tax liability register.

Electronic Registers under GST Electronic Liability Register – Ambuja Cement Vendor Name GSTN No Inv Base Amt SGST CGST Goyal Co 27 AAACT 6578 C 1 XZ 1001 20000 2000 Ramji Builder 27 ABCDE 1507 C 1 XZ 1002 10000 1000 3000 Total Liability Electronic Credit Register – Ambuja Cement Vendor Name GSTN No Inv Base Amt SGST CGST Jindal Steel 27 JHGFR 1234 C 1 XZ 1111 15000 1500 Ramji Builder 27 IUUTR 1507 D 1 XZ 2001 11000 1100 2600 Total Input Tax Credit available Electronic Cash Register– Ambuja Cement Date of Deposit Mode of Payment / Utilization SGST CGST 20/05/2017 400 20/05/2017 -400 Available Balance 0 0 ICICI Bank /RTGS

Accounting Software üHandwritten Accounts will no longer work üAccounts have to be maintained on a Computer üYou can choose any accounting software of your choice üA Part / Full Time Accountant to be hired üAnti Virus / Back Up to be taken at regular intervals

Web Resources • • • http: //tutorial. gst. gov. in/userguide/#t=View_FAQs_and_Help_ Documents. htm www. gst. gov. in http: //tutorial. gst. gov. in/faq/#t=I_am_unable_to_access_the_ GST_Common_Portal_available_at_www. gst. gov. in. _How_ca n_I_access_the_site_. htm http: //www. cbec. gov. in/htdocs-cbec/gst-training http: //www. indiancementreview. com/News. aspx? nid=V 4 y 4 r. K nr. O 22 Ny 54 Js 1 m. Tl. A==#sthash. iam 2 oc. Ac. dpbs

Thank You…!!!