GST GOODS SERVICE TAX by Top GST Experts

by Top GST Experts © Prepared & Presented by")

GST (GOODS & SERVICE TAX) by Top GST Experts © Prepared & Presented by TOP GST EXPERTS

Basics about GST What is GST? ? • GST is a destination based tax on consumption of goods and services. It is proposed to be levied at all stages right from manufacture up to final consumption with credit of taxes paid at previous stages available as setoff. In a nutshell, only value addition will be taxed and burden of tax is to be borne by the final consumer. • Taxable goods and services are not distinguished from one another and are taxed at a single rate in a supply chain till the goods or services reach the consumer. • Exports would be considered as zero-rated supply and imports would be levied the same taxes as domestic goods and services adhering to the destination principle in addition to the Customs Duty which will not be subsumed in the GST.

Why GST is Necessary ? . ISSUE IN EXISTING TAX REGIME • Cascading Effect _ Means tax on tax • Multiple tax leads increase in compliance cost • Due to heavy cost exporters are not able to compete with world • Was Difficult to curb black money”& Corruption • Inefficient dispute resolution system in the current indirect tax regime ( SEZ- Export Zone better in China) GST TAX SYSTEM_ BENEFIT • All Major Indirect Taxes are subsumed into one Tax. Saving in compliance & procedural cost for businessman as well for government • Free flow of Input Tax credit means no cascading effect _ Tax on Tax • Transparency in Tax flow ( Everything will be online through GSTN)eventually help to curb black money & corruption • Effective dispute resolution system will attract foreign investor • Indian market will be more competitive with the world • Overall Growth in economy

GST Bill Finalized & Input credit system CGST CGS T IGST SGS T IGST CGS T SGS T UTGS T

Taxes subsumed under CGST

Taxes subsumed under SGST

Taxes not subsumed under GST Ø Basic Custom Duties Ø Excise on liquor Ø Property Tax Ø Stamp Duty Ø Tax on sale/consumption of electricity

Ø High Speed")

Products not covered under GST Ø Petroleum Crude Ø Motor Spirit(Petrol) Ø High Speed diesel Ø Natural Gas Ø Aviation turbine fuel Ø Liquor Note : -What will be status of Tobacco and Tobacco products under the GST regime? Ans. Tobacco and tobacco products would be subject to GST. In addition, the Centre would have the power to levy Central Excise duty on these products.

Sr. No. Rate Description 1 0% Essential items including")

GST RATES ( Grouping ) Sr. No. Rate Description 1 0% Essential items including food 2 5% Common usage items 3 12% and 18% Standard Rates 4 28% Items which are Currently taxable with (3031%) 5 28% with Cess Luxury and de-merit Goods

Rate applicable under GST on Goods • The Council has broadly approved the GST rates for services at Nil, 5%, 12%, 18% and 28% as listed below. • GST Nil rate (0%): No tax will be imposed on items like fresh meat, fish chicken, eggs, milk, butter milk, curd, natural honey, fresh fruits and vegetables, flour, besan, bread, prasad, salt, bindi. Sindoor, stamps, judicial papers, printed books, newspapers, bangles, handloom etc. • GST 5% Items List Items such as fish fillet, cream, skimmed milk powder, branded paneer, frozen vegetables, coffee, tea, spices, pizza bread, rusk, sabudana, kerosene, coal, medicines, stent, lifeboats will attract tax of 5 percent.

• GST 12% Items list : Frozen meat products , butter, cheese, ghee, dry fruits in packaged form, animal fat, sausage, fruit juices, Bhutia, namkeen, Ayurvedic medicines, tooth powder, agarbatti, colouring books, picture books, umbrella, sewing machine, and cell phones will be under 12 per cent tax slab. • GST 18% Items list : Most items are under this tax slab which include flavoured refined sugar, pasta, cornflakes, pastries and cakes, preserved vegetables, jams, sauces, soups, ice cream, instant food mixes, mineral water, tissues, envelopes, tampons, note books, steel products, printed circuits, camera, speakers and monitors. • GST 28% Items list : Chewing gum, molasses, chocolate not containing cocoa, waffles and wafers coated with chocolate, pan masala, aerated water, paint, deodorants, shaving creams, after shave, hair shampoo, dye, sunscreen, wallpaper, ceramic tiles, water heater, dishwasher, weighing machine, washing machine, ATM, vending machines, vacuum cleaner, shavers, hair clippers, automobiles, motorcycles, aircraft for personal use, and yachts will attract 28 per cent tax – the highest under GST system

Rate applicable under GST on Services • The Council has broadly approved the GST rates for services at Nil, 5%, 12%, 18% and 28% as listed below. • List of Exempted Services : - http: //www. topgstexperts. com/wp-content/uploads/2017/06/GST_-List-of. Sr. Exempted-services-under-GST. pdf No Description of Services GST Rate 1 Transport of goods by rail 5% with ITC of input services 2 Transport of passengers by rail (other than sleeper class) 5% with ITC of input services 3 Services of goods transport agency (GTA) in relation to transportation of goods [other than used household goods for personal use] 5% No ITC 4 Services of goods transport agency in relation to transportation of used household goods for personal use. 5% No ITC 5 Transport of goods in a vessel including services provided or agreed to be provided by a person located in non-taxable territory to a person located in non-taxable territory by way of transportation of goods by a vessel from a place outside India up to the customs station of clearance in India 5% with ITC of input services 6 Renting of motorcab (If fuel cost is borne by the service recipient, then 18% GST will apply) 5% No ITC 7 Transport of passengers, by(i) Air conditioned contract/stage carriage other than motorcab; (ii) a radio taxi. 5% No ITC • http: //gstindiaupdates. com/wp-content/uploads/2017/05/Exemption-List-under-GST. pdf

Sr No Description of Services GST Rate 8 Transport of passengers by air in economy class 5% with ITC of input services 9 Supply of tour operators’ services 5% No ITC 10 Leasing of aircrafts under Schedule II [5 (f)] by a scheduled airlines for scheduled operations 5% with ITC of input services 11 Selling of space for advertisement in print media , Services by way of job work in relation to printing of newspapers 5% with ITC of input services 12 Transport of goods in containers by rail by any person other than Indian Railways 12% With Full ITC 13 Transport of passengers by air in other than economy class 12% With Full ITC 14 Supply of Food/drinks in restaurant not having facility of air-conditioning or central heating at any time during the year and not having licence to serve liquor. 12% With Full ITC 15 Renting of hotels, inns, guest houses, clubs, campsites or other commercial places meant for residential or lodging purposes having room tariff Rs. 1000 and above but less than Rs. 2500 per room per day 12% With Full ITC 16 Services provided by foreman of chit fund in relation to chit 12% with ITC of input services 17 Construction of a complex, building, civil structure or a part thereof, intended for sale to a buyer, wholly or partly. [The value of land is included in the amount charged from the service recipient] 12% With Full ITC but no refund of overflow of ITC

Sr No Description of Services GST Rate 18 Temporary transfer or permitting the use or enjoyment of any Intellectual Property (IP) to attract the same rate as in respect of permanent transfer of IP; 12% with full ITC 19 Supply of Food/drinks in restaurant having licence to serve liquor , Supply of Food/drinks in restaurant having facility of air-conditioning or central heating at any time during the year Supply of Food/drinks in outdoor catering 18% With Full ITC 20 Renting of hotels, inns, guest houses, clubs, campsites or other commercial places meant for residential or lodging purposes where room tariff of Rs. 2500/ and above but less than Rs 5000/- per room per day 18% With Full ITC 21 Bundled service by way of supply of food or any other article of human consumption or any drink, in a premises together with renting of such premises 18% With Full ITC 22 Services by way of admission or access to circus, Indian classical dance including folk dance, theatrical performance, drama 18% With Full ITC 23 Composite supply of Works contract as defined in clause 119 of section 2 of CGST Act 18% With Full ITC 24 Services by way of admission to entertainment events or access to amusement facilities including exhibition of cinematograph films, theme parks, water parks, joy rides, merry-go rounds, go-carting, casinos, race-course, ballet, any sporting event such as IPL and the like 28% With Full ITC 25 Services provided by a race club by way of totalisator or a licensed bookmaker in such club 28% With Full ITC 26 Gambling 28% With Full ITC 27 Supply of Food/drinks in air-conditioned restaurant in 5 -star or above rated Hotel, Accommodation in 28% With Full

Rate applicable For Few Important item under GST Particular Rate Gold and Gold Jewellary 3% Gems and Jewellary 3% Rough Diamond 0. 25% Readymade Garments 12% Readymade Garments Below Rs. 1000/- 5% Fabric & Yarn of Cotton 5% Manmade Yarn 18% All Process of Textile 5% Package Food 5% Fiber Silk & Jute 0% Manmade Fiber 18% List of 66 items on which rate is separately revised. Find the list of Revised rates. : - Click for link

RATE ON SERVICE SECTOR RELATED TO REAL ESTATE SECTOR & WORK CONTRACT Service Construction of a complex, building, civil structure or a part thereof, intended for sale to a buyer, wholly or partly. [The value of land is included in the amount charged from the service recipient] Composite supply of Works contract as defined in clause 119 of section 2 of CGST Act Rate 12% With Full ITC but no refund of overflow of ITC 18% with full ITC Earlier Composite Sales Tax of 5% on the 60% of the Order Value and the Service Tax of 15% on 40% of the Order Value.

Applicability of GST • Every supplier shall be liable to be registered under GST in the state from where he makes taxable supply of goods and/or services if his aggregate turnover in a financial year exceeds threshold limit as announced by GST Council on 24. 09. 2016 of : • 20 lakh; • 10 lakh in North Eastern States including Sikkim. • If you are purchasing or selling goods outside the state irrespective of the limit • If you are receiving or providing services outside the state irrespective of the limit • If you are required to pay tax under reverse charge. • If you are non-resident taxable person irrespective of the limit. • Input Service Distributor

• An aggregator who supplier services under his brand name or his trade name irrespective of the limit mentioned in point 1. • Every electronic Commerce operator like Flipkart, Amazon, etc. , irrespective of the limit • A person who supplies goods and services through electronic commerce. In other words, if you want to sell on Flipkart, Amazon, then you will need to register yourself first irrespective of the limit mentioned in point 1. • Any person who is required to deduct TDS under GST (not under Income Tax Act, 1961). • Every person who is liable to be registered under this Act shall apply for registration in every such State in which he is so liable within thirty days from the date on which he becomes liable to registration, in such manner and subject to such conditions as may be prescribed. • A person having multiple business verticals in a State may obtain a separate registration for each business vertical, subject to such conditions as may be prescribed. • A person, though not liable to be registered under Schedule V, may get himself registered voluntarily, and all provisions of this Act, as are applicable to a registered taxable person, shall taxa apply to such person.

Filling of return and its due date under GST • In the table below, we have provided details of all major returns which are required to be filed under the GST Law. Return Form What to file By Whom? By When? GSTR-1 Outward supplies of taxable goods and/or services effected Registered Taxable Supplier 10 th of the next month GSTR-2 Inward supplies of taxable goods and/or services effected claiming input tax credit. Registered Taxable Recipient 15 th of the next month GSTR-3 Monthly return on the basis of finalization of details of outward supplies and inward supplies along with the payment of amount of tax. Registered Taxable Person 20 th of the next month GSTR-4 Quarterly return for compounding taxable person. Composition Supplier 18 th of the month succeeding quarter GSTR-5 Return for Non-Resident foreign taxable person Non-Resident Taxable Person 20 th of the next month

Return Form What to file By Whom? By When? GSTR-6 Return for Input Service Distributor GSTR-7 Return for authorities deducting tax at source. Tax Deductor 10 th of the next month GSTR-8 Details of supplies effected through ecommerce operator and the amount of tax collected E-commerce Operator/Tax Collector 10 th of the next month GSTR-9 Annual Return Registered Taxable Person 31 st December of next financial year GSTR-10 Final Return Taxable person whose registration has been surrendered or cancelled. Within three months of the date of cancellation order, whichever is later. GSTR-11 Details of inward supplies to be furnished by a person having UIN Person having UIN and claiming refund 28 th of the month following the month for which statement is filed

read with section")

Important definitions 1 “Supply” • Definition of ‘supply’ Under section 2(92) read with section 3 ‘supply’ includes all forms of supply of goods and/or services such as sale, transfer, barter, exchange, license, rental, lease or disposal made or agreed to be made for a consideration by a person in the course or furtherance of business. Schedule I specified the supply. • Supply Includes : • (b) Importation of service, whether or not for a consideration and whether or not in the course or furtherance of business, and • (c) a supply specified in Schedule I, made or agreed to be made without a consideration

Schedule II, in respect of matters mentioned therein, shall apply for determining what is, or is to be treated as a supply of goods or a supply of services. (3) Notwithstanding anything contained in sub-section (1), (a) activities or transactions specified in schedule III; or (b) activities or transactions undertaken by the Central Government, a State Government or any local authority in which they are engaged as public authorities as specified in Schedule IV, shall be treated neither as a supply of goods nor a supply of services. (4) The Central or a State Government may, upon recommendation of the Council, specify, by notification, the transactions that are to be treated as— (a) a supply of goods and not as a supply of services; or (b) a supply of services and not as a supply of goods; or (c) neither a supply of goods nor a supply of services. (5) The tax liability on a composite or a mixed supply shall be determined in the following manner — (a) a composite supply comprising two or more supplies, one of which is a principal supply, shall be treated as a supply of such principal supply; (b) a mixed supply comprising two or more supplies shall be treated as supply of that particular supply which attracts the highest rate of tax.

2. “Goods’’ - Means every kind of movable property other than money and securities but includes actionable claim, growing crops, grass and things attached to or forming part of the land which are agreed to be severed before supply or under a contract of supply 3. “Services’’ - means anything other than goods; Services does not include transaction in money other than an activity relating to the use of money or its conversion by cash or by any other mode, from one form, currency or denomination, to another form, currency or denomination for which a separate consideration is charged. 4. “Aggregate turnover” = Value of all taxable supplies+ exempt supplies+ export of goods and/or services+ all inter-state supplies of a person having same PAN –taxes (CGST+IGST+SGST as the case may be)-* not covered inward supplies on which tax payable under reverse charge

any trade, commerce, manufacture, profession, vocation, adventure, wager or")

5. “Business” includes – (a) any trade, commerce, manufacture, profession, vocation, adventure, wager or any other similar activity, whether or not it is for a pecuniary benefit; (b) any activity or transaction in connection with or incidental or ancillary to (a) above; (c) any activity or transaction in the nature of (a) above, whether or not there is volume, frequency, continuity or regularity of such transaction; (d) supply or acquisition of goods including capital assets and services in connection with commencement or closure of business; (e) provision by a club, association, society, or any such body (for a subscription or any other consideration) of the facilities or benefits to its members, as the case may be; (f) admission, for a consideration, of persons to any premises; and (g) (services supplied by a person as the holder of an office which has been accepted by him in the course or furtherance of his trade, profession or vocation; (h) services provided by a race club by way of totalizator or a license to book maker in such club; Explanation. - Any activity or transaction undertaken by the Central Government, a State Government or any local authority in which they are engaged as public authorities shall be deemed to be business.

")

6. “Consideration” Consideration in relation to the supply of goods or services includes (a) any payment made or to be made, whether in money or otherwise, in respect of, in response to, or for the inducement of, the supply of goods or services, whether by the recipient or by any other person but shall not include any subsidy given by the Central Government or a State Government; (a) The monetary value of any act or forbearance, whether or not voluntary, in respect of, in response to, or for the inducement of, the supply of goods or services, whether by the recipient or by any other person but shall not include any subsidy given by the Central Government or a State Government: PROVIDED that a deposit, whether refundable or not, given in respect of the supply of goods or services shall not be considered as payment made for the supply unless the supplier applies the deposit as consideration for the supply;

Anti Profiteering Clause • What is Anti Profiteering Clause • Clause 171 has been inserted in the GST bill which provides that it is mandatory to pass on the benefit due to reduction in rate of tax or from input tax credit to the consumer by way of commensurate reduction in prices. • Benefited to Consumer • Majorly Impact on Real Estate & Infrastructure sector • Not easy to track whether benefit is passed on to customer or not

Transition Provision for Carry forward of CENVAT credit/Set off Transition Rules are hosted on the Government Website, its salient features are as under: 1. Persons entitled to take transition credit will have to submit a declaration within 90 days (upto 30 th Sept) specifying the credit he wants to take on stocks lying with him on 30 th June. Commissioner can extend this timeline by another 90 days 2. Declaration will have to be submitted in from GST Tran-1 3. In case of capital goods whose part credit was availed in current period and part credit is to be availed under GST, he will have to submit the declaration specifying: a. Amount of credit already availed in the current law b. Amount of credit yet to be availed under the existing law and which he intends to avail under GST period 4. Persons having excise invoices for stocks lying as on 30 th June will be entitled to take full credit of excise mentioned in the invoices 5. Deemed Credit: Persons who do not have excise invoice, will be eligible to take credit in the following manner: a. For goods taxable @ 18% or above - Credit shall be allowed at the rate of 60% of CGST payable on that goods – so if the rate is 18% then credit will be available @ 8. 4% (60% of 9% CGST) b. For goods other than above - Credit shall be allowed at the rate of 40% of CGST payable on that goods – so if the rate is 12% then credit will be available @ 2. 4% (40% of 6% CGST)

6. Credit in the above Deemed Credit scheme will be available only once the said goods are sold and GST is paid. It’s like a cash back scheme. 7. To take the credit in this scheme following conditions will have to be fulfilled: a. such goods were not unconditionally exempt from excise b. the document for procurement of such goods is available c. the stock of goods on which the credit is availed is so stored that it can be easily identified by the registered person. 8. Deemed credit scheme will go on for 6 months from GST date, so stocks lying as on 30 th June have to be sold maximum upto 31 st December, 2017. No credit will be available if these goods are sold after December 2017. 9. Separate return under for GST TRAN-2 will have to be filed. 10. Every person to whom the provision of section 142 (11) (c) applies, shall submit a declaration within 90 days of GST date in form GST TRAN-1 furnishing the proportion of supply on which VAT or service tax has been paid before the GST day but the supply is made after the GST day, and the ITC admissible thereon. 11. Every person to whom the provisions of section 141 (Job worker) apply shall, within 90 days of the GST day, submit a declaration electronically in form GST TRAN-1, specifying therein, the stock held by him on the appointed day. 12. Every person having sent goods on approval under the existing law and to whom section 142 (12) applies shall, within 90 days of the appointed day, submit details of such goods sent on approval in form GST TRAN-1.

What is E-Way bill and it’s applicability under GST • Official shipping document that travels with a shipment, identifies its consignor, consignee, origin and destination, describes the goods, and shows their weight and freight. • The registered person or transporter may at his option, generate and carry the e-way bill if the value of consignment is less than Rs. 50, 000 , for all other case it is mandatory. • During transit one conveyance to other before such transfer and further movement of goods, transporter shall generate a new e-way bill in FORM GST INS-1. • In case multiple consignment in on conveyance consolidated e-way bill in FORM GST INS-2 will need to be generated prior to the movement of goods.

Validity of E-Way bill in GST Note : - E - way bill is postponed as of now at least for a period of 6 months • The e-way bill will remain valid for the period as mentioned in following table from the time of generation of e-way bill SR No Distance Validity Period 1 Less then 100 Km 1 days 2 100 km to 300 Km 3 days 3 300 Km to 500 Km 5 days 4 500 Km to 1000 Km 10 days 5 1000 km and more 15 days

POS of Goods : Domestic Supplies SR No Time Location 1 When movement involved Place where movement terminates for delivery 2 When movement not involved Location at the time of delivery 3 Bill to Ship to model Person on whom bill raised 4 Supplied on board a conveyance Place where goods taken on board 5 Supply by way of erection/ installation Place of such installation/ erection

Input service Distributor • ISD shall take separate registration under GST • Presently, credit is distributed only to the factories and premises registered under service tax. • Under GST, credit of common input services will have to be distributed to all establishments where registration is taken • Credit shall be distributed on the basis of turnover of each taxable person • ISD shall file monthly return in Form GSTR 6 by 13 th of next month

*Small businessmen or professionals* Like")

Concept of Casual Taxable person under GST • 1) *Small businessmen or professionals* Like Architects, Fashion designers, Make-up artists, Trainers, Musicians, etc would need *to register as 'casual taxable person'* if they don't have a principle place of business in the state where they are proving services. This registration required *even if their turnover is below exemption limit* of 20 lakh (Rs 10 lakh in NE states). • 2) *Meaning of 'casual taxable person' as per GST Act is *'One who occasionally undertakes transactions involving supply of goods or services or both in the course or furtherance of business, whether as principal, agent or in any other capacity, in a state or a union territory *where he has no fixed place of business*'. • 3) Facts of each case will determine *whether or not* it would be a case of an inter-state supply or one falling in the category of supply by a casual taxable person. *For example*- A jeweller who has a showroom in Mumbai but participates in an exhibition-cum-sale in another city would fall under casual taxable person. However, if he sends the consignment from his Mumbai store, then it would be an inter-state sale. • 4) *Registration of Casual taxable persons* five days prior to the commencement of business (or in other words, before entering into the transaction for supply of goods or services). The registration certificate is valid for 90 days and can be extended up to another 90 days

Refund Rule Under GST • Refund under normal case - Application to be file in FORM GST RFD -01. This refund can be claimed only if amount shown in GST return of relevant TAX period. Refund claim based on documentary evidence and order passed by proper officer or an appellate authority or tribunal or Cour. • Refund under Unutilised input tax credit – In case of input higher then output rate of tax then in annexure 1 of FORM GST RFD-01 Containing the number of and date of invoices received and issued during a tax period has to be file. • Refund under finalisation of provisional assessment – reference number of final assessment has to be submitted. • Refund upto 2 lack self declaration required for incident of tax has not passed to other person and if Refund is more then 2 lack , if incident of tax has not been passed to other person in annexure 1 of FORM GST RFD-01. • Common portal will issue acknowledgment within 15 days in RFD-02, if any deficiency officer will communicate the deficiency in form GST RFD-03 and if no deficiency found then officer shall issue payment order in FORM GST RFD-05.

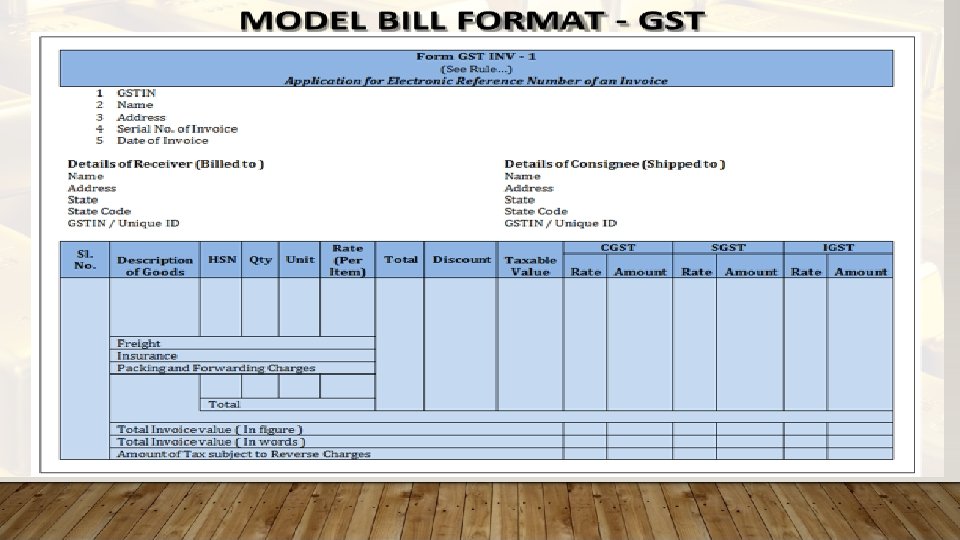

DOCUMENTS REQUIRED FOR PROPER ACCOUNTING IN GST

TAX INVOICE - CONTINUE SUPPLY OF GOODS • Continuous Supply of goods: Provided, or agreed to be provided, continuously or on recurrent basis, under the contract, weather or not be means of wire, cable, pipeline or other conduit and for which the supplier invoices on a regular or periodic basis & includes supply of such goods as may be notified. • Invoice to be issued or at the time of : Each statement is issued Each Such Payment is received

TAX INVOICE – SUPPLY OF SERVICES • Continuous Supply of Services : Means a supply of services which is provided, or agreed to be provided, continuously or on the basis, under a contract, for a period exceeding 3 months with periodic payment obligations & includes supply of such services as may be notified. Invoice to be issued Due Date of the Payment is ascertainable from the contract Yes – On the before the due date of Payment. No - On or before the date of receipt of payment

Impact of GST on Various Sectors

Impact of GST on Manufacturing Sector • No Excise Duty at the time of Manufacture & GST will be applicable on “SUPPLY”. Will be great relief to all Manufacturer. • Reduction in cascading effect ( Like earlier VAT was charged on Value + Excise amount) • Hassle Free Supply of Goods _ because on no Entry Tax/Octroi • Increased Working Capital Requirements (Because Branch Transfer will be treated as supply) • Free Supplies & After Sale discount will be burden on supplier • Valuation of Self Supplies required clarity • Pre packaged products for retail consumption valued on MRP leading higher cost price which is unlikely in GST • Reduction of classification disputes

Impact of GST on Traders & Resellers • Reduction in Cost because of cross input tax credit available • No Cascading effect will reduced cost & ultimate benefit to customer • No need to open multiple branches in different states as claim of interstate purchase & interstate sale is available now. • GST compliance will be burden for small traders & retailers, Comsidering higher no. of returns and montly credit matching concept • Filling of monthly returns with purchase & Sales monthly cross examination helps to curb circulations of dummy purchase and sales invoices in the market

Impact of GST on Service Sector • Services will be costlier but free flow of ITC may curtail the cost to some extent Example : “Services provided by beauty parlour in which goods are used to provide the service to the client, however its providing output service and not trading in goods can not claim input credit on VAT paid on that products” • Number of filing return will increase as against only two half yearly returns in current indirect tax regime • Centralized Registration will become Decentralized Registration in GST ( Will be tough for few industries like Telecommunication Industry) • Services are often delivered through third party vendors and hence, determining point and time of supply is ambiguous. • Reverse and partial charge mechanism likely to continue under GST

GST Impact on import of Goods & Services • With Constitutional Amendments, both CGST and SGST will be levied on import of goods and services into the country. • The incidence of tax will follow the destination principle(Place of supply rules). • Tax revenue in case of SGST will accrue to the State where the imported goods and services are consumed. • Full and complete set-off will be available on the GST paid on import on goods and services. • Thus, import of goods will attract BCD and IGST. It may be noted that import of services, as against service tax at present, in GST regime, will attract IGST. • Basic Custom Duty will continue to there under GST system. However, the additional custom duty in lieu of CVD /Excise and the Special Additional Duty (SAD) in lieu of sales tax/VAT will be subsumed in the import GST. • The import of services will be subject to Central GST and State GST on a reverse charge mechanism. In other words, the GST will be payable by the Importer on a self declaration basis.

GST impact of export of Goods & Services • Export of Goods & Services= Zero rated (Tax-Free/Exempted) • Lower Logistic cost by subsuming Octroi/Entry Tax • Free flow of goods makes Exports faster • Refund of GST paid on Input is also available. • Overall Indian Products will be more competitive Duty Drawback : Earlier there was no provision for duty drawback in GST, but after public & experts opinions, provision of duty drawback has been made in GST which will be a big relief to the exporters.

Impact Of GST on Real Estate Sector

PROVISIONS UNDER EXISTING LAWS Ø Both VAT and Service tax is applicable on construction Ø Place of Provisions for services, under present regime would be location of the immovable property. Ø Ambiguity on taxability of Transfer Development Rights as to whether same are liable for service tax and at what value? ? Ø Currently various credits may not be recorded if opts for composition/abatement Ø Under VAT composition scheme is applicable for builders Ø Due to composition scheme, no higher tax burden Ø No Service tax and VAT is levied if amount received after completion certificate Ø In current indirect tax regime, builder pay taxes on receipt basis(without complying with the POT)

PROVISIONS UNDER PROPOSED GST Ø AS discussed GST rate would be 12% on under Construction Ø Higher side as compared to current rate of 6 to 10% under composition scheme Ø There would be no GST if the entire amount is received after CC or levied “after first occupancy”(Additional condition in GST) Ø Concept of centralised Registration will end and having site in multiple states would require to obtain registration in each state Ø Not beneficial to small projects for small value Ø High Compliance burden (37 returns are to filed)

PROVISIONS UNDER PROPOSED GST Ø Anti-Profiteering Measures (Benefit of price reduction, pass on to the customer) Ø In GST regime, tax needs to be paid on earliest of raising of invoice, receipt of money from customers and completion of services. Ø “Movable Property” excluded from the definition from the “Works Contract” Ø GST needs to be paid slab wise amount received from customer, & need to comply with the same Ø Considering RERA provision with GST, working capital requirement for the builder will increase.

LIKELY ISSUES IN PROPOSED GST Ø No clarity on Valuation of land to be adopted and deduction Ø GST needs to be paid on stock transfers of inputs/capital goods Ø Anti-Profiteering clause Ø Cancellation of flats & increase tax rate under GST Ø Whether the supply of different services would be regarded as mixed supplies?

WORK CONTRACT UNDER EXISTING LAW • Works contracts consists of three kinds of taxable activities as per the current law. It involves supply of goods as well as supply of services. If a new product is created during the works contract, then such manufacture becomes a taxable event. • So, different aspects of one a single activity are taxed by different laws. This causes a lot of confusion regarding treatment and taxability which is why there are so many legal disputes in related to works contracts. • If a new product appears in the process of completing a works contract, Central Excise duty is levied.

WORK CONTRACT UNDER GST Schedule II clearly mentions that the following are supply of service– • construction of a complex, building, civil structure or a part thereof, including a complex or building intended for sale to a buyer, wholly or partly, • works contract including transfer of property in goods (whether as goods or in some other form) involved in the execution of a works contract • This means works contract will be treated as service and tax would be charged accordingly (not as goods or part goods/part services). • Composition scheme is not available to works contractors as it is treated as service under GST. Composition scheme is only available to suppliers of goods. This will be a big blow to the small sub-contractors who cannot opt for composition scheme. They will be forced to register for normal taxation scheme increasing their compliances and costs. • Abatement clarity is yet to receive

OVERALL IMPACT OF GST ON REAL ESTATE SECTOR • The impact of GST on real estate will depend upon the abatement allowed on agreement value, says CRISIL survey. • In the residential segment, completed properties do not attract service tax and so will have no impact of the implementation of GST. • Stamp duty and registration charges (which are state specific and which will not fall under the GST) • Leasing of residential properties does not attract service tax and so will have no impact of the Implementation of GST

Particulars Without GST With GST Cost of Production 5000 Add: Profit Margin 2000 Manufacturer Price 7000 Add: Excise Duty (12. 5%) 875 - Total Value 7875 7000 Add: VAT 13. 5% 1063 - Add: CGST 9% - 630 Add: SGST 9% - 630 Total Invoice Value 8938 8260 Manufacturer to Wholesaler

Wholesaler to Retailer COG to Wholesaler Without GST With GST 8938 8260 894 826 Total value 9832 9086 Add: VAT 13. 5% 1327 - Add: CGST 9% - 818 Add: SGST 9% - 818 11159 10722 1116 1072 12275 11794 1657 - - 2123 13932 13917 - 15 Add: profit Margin(10%) Invoice Value(COG to Retailer) Retailer to Consumer Add: Profit Margin(10%) Total Value Add: VAT 13. 5% Add: CGST/SGST(9%) Total Price to final Consumer Cost saving to Consumer

Structure your business to get maximum benefit from GST • Accounting")

How to (Re) Structure your business to get maximum benefit from GST • Accounting will be the “KEY” for compliance • Restructure your branches _ Now Inter state Sale & Purchase set off is available • Restructure your warehousing Logistic & Supply chain management (Entry Tax & Octroi removed) • File your returns on time _ Profit will not be yours but yes loss is yours ( For Ex. You cant forget to carry forward available credit) • Track Credit mismatch data closely_ Reconciled it every month_ you will not get the credit if your seller don’t pay it

Structure your business to get maximum benefit from GST • Check")

How to (Re) Structure your business to get maximum benefit from GST • Check whether Your existing staff are enough capable to manage your books after GST? ? if No Restructure the compliances system and train your existing staff to tackle with new challenges • Re – costing of your product to fix your margin & selling price • Don’t pay more by trying to save few_ Hire proper consultant • Check your business needs full time accountant or not? • Prepare Invoice/Delivery challans/ Stock maintenance all should be electronic to save cost & time.

Important Links • GST Migration Process : - http: //www. topgstexperts. com/wp-content/uploads/2017/01/service-tax-to-gst-migration-process. pdf • GST Migration status Check : - https: //services. gst. gov. in/services/check-registration-status • GST Registration Website : - www. gst. gov. in • Transition format for transfer of opening Set off/CENVAT credit : - http: //www. topgstexperts. com/wp-content/uploads/2017/06/GSTCENVAT-credit-setoff-transition-Provisions-formats-Topgstexperts. pdf • Transitional Provision/Rules _ Process of the same : - http: //www. topgstexperts. com/wp-content/uploads/2017/06/GST_-transitionrules-provisions-topgstexperts. pdf • Detailed E – way Bill Process : - http: //www. topgstexperts. com/gst_-cbec-proposes-e-way-bill-for-goods-worth-rs-50000 -in-transit/ • Goods & Service Tax Return Filling Process/Rules : - http: //www. topgstexperts. com/wp-content/uploads/2017/06/GST-Return-fillingrules_-procedure_-norms_process_-topgstexperts. pdf • Goods & Service Tax Return various Formats ( Returns/CENVAT carry forward/Refunds) : - http: //www. topgstexperts. com/wpcontent/uploads/2017/06/GST_-Returns_format_GRN-1_Tran-1_GST-formats-_-topgstexperts. pdf • Goods & Service tax (GST) Mismatch Formats : - http: //www. topgstexperts. com/wp-content/uploads/2017/06/GST-Mismatch-Formats_ -Important_-GST-Formats_-topgstexperts. pdf

Important Links • GST Rates on Goods _ HSN Code Wise (Meeting held on 18 th May 2017) : http: //www. topgstexperts. com/wp-content/uploads/2017/06/GST-Rate-on-Goods-_-HSN -Code-wise-scheduled. pdf • GST Rates on Services _ HSN Code Wise : - http: //www. topgstexperts. com/wpcontent/uploads/2017/06/Schedule-of-GST-rates-for-services_-list-of-Exemptedservices. pdf • Revised GST Rates on 66 Items _ : - http: //www. topgstexperts. com/wpcontent/uploads/2017/06/Revised-GST-rates-on-66 -items-Revised-on-11 th-June-2017 for-Certain-Goods. pdf

About Top GST Experts • We would like to be called by a name “GSTexperts“, We are a team of young and Innovative professionals having colossal knowledge and experience in matters of Taxation and Finance. We believe in “Super Market concept” everything under one roof, hence with special efforts we have created a Vibrant & Dynamic team to cater all your Financials & Taxation needs. Our moto is to add value in your “WEALTH”. • We are team of professionals in your service all over India & We are working towards spread our wings in “ALL OVER THE WORLD” Journey may not be easy but, we as a team are confident enough to achieve the goal. • We also have a complete solution for all “START UPs”. We offer all sort of services from set up a new company to till dissolution. We have a team of ICWA, CS, CE, and Advocate to coping of with corporate tax matters from small Entrepreneur to Big Business Giants. By creating a huge team of professionals, we have not restricted our self to few services although we are specialist in GST. • This breadth of experience enables us to quickly identify solutions for our clients and provide them with a unique personal service for all their needs.

Branches 1. Delhi 2. Kutch 3. Surat 4. Ahmedabad 5. Patna 6. Pune 7. Kolkata 8. Madhya Pradesh 9. Jaipur 10. Nashik 11. Punjab 12. Karnataka 13. Hyderabad 14. Chhattisgarh 15. Chennai 16. Kerala 17. Goa Head Office – Mumbai: CA MILIN SHAH (FOUNDER) (Chartered Accountants) 31, 1 st Floor, Sai Dham Shopping Plaza, P. K. Road, Mulund (w), Mumbai-80 Email: topgstexperts@gmail. com/camilinhshah@gmail. com Website: - www. topgstexperts. com To reach us, use Google map: https: //goo. gl/maps/d. HCBHi. Wi. L 6 k Want to reach to our professionals : - avail service just a click away

- Slides: 60