Chapter 1 Federal Income Taxation An Overview Instructor

on")

Slide 3 Suppose a tenant came to Jan Corporation’s")

Slide 4 Explain how you might compute the tax")

•")

– File petition")

Tax-exempt interest Nontaxable stock dividends Nontaxable stock rights")

Nontaxable part of pension plan distributions Nontaxable")

“Above-the-line” deductions • Property losses")

• Medical (dental) expenses (in excess of 10%")

Treasury Circular 230: Regulations Governing the Practice of Attorneys,")

- Slides: 105

Chapter 1. Federal Income Taxation— An Overview Instructor Power. Point Slides This file contains illustrative problems that will be used in the lecture to illustrate important concepts and procedures. Updated August 26, 2014 Howard Godfrey, Ph. D. , CPA Professor of Accounting ©Howard Godfrey-2014

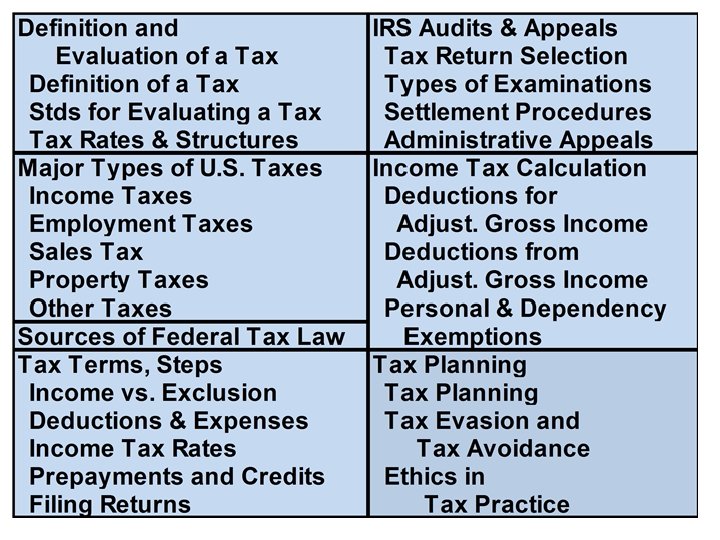

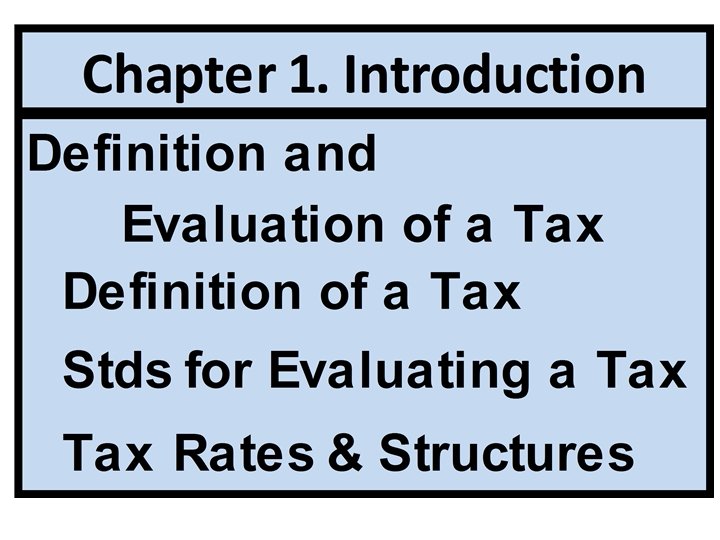

Part-1, 2. Definition and evaluation of a tax. Rate Structures. Part-3. Major Types of Taxes. Part-4. Sources of Federal Income Tax Law. Part-5. Federal taxation terminology. Part-6. IRS audit and appeals in IRS. Part-7. Individual tax calculations. Part-8. Tax planning. Ethical principles

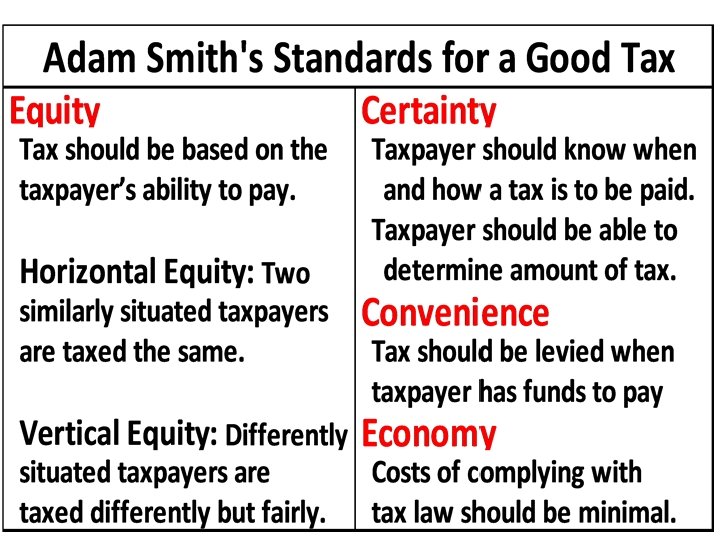

Definition of a Tax • An enforced, involuntary contribution • Required and determined by law • Providing revenue for public and governmental purposes • For which no specific benefits or services are received

Purpose of a Tax • Revenue • Penalty • Social changes • Economic changes • Equity

Tax Rates for Income Tax • Marginal Tax Rate – rate of tax on the next dollar of taxable income • Average Tax Rate – rate equal to the total tax divided by tax base. • Effective Tax Rate – rate equal to the total tax divided by economic income (taxable & nontaxable income).

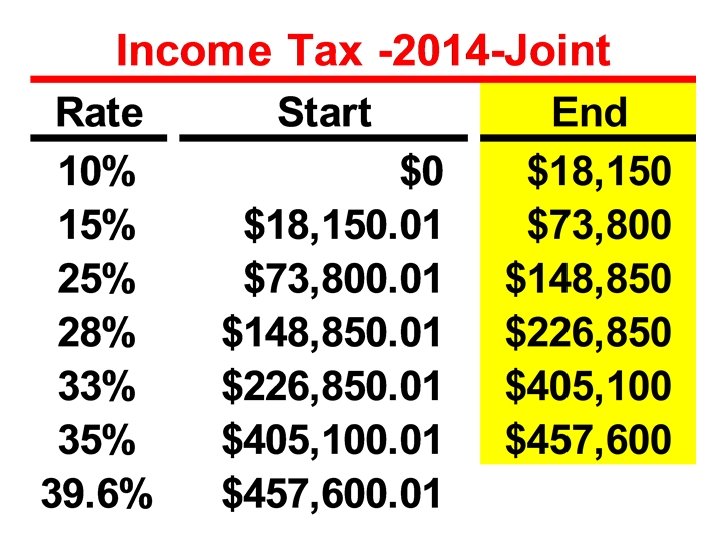

Progressive Tax Rate System • Tax rates increase as income increases • In 1913 rates ranged from 1% to 7% • To finance World War I, top rate was increased to 77% • In 1985, 15 tax brackets from 11% to 50% • 2003 Tax Act reduced top rate from 38. 6% to 35% (rates now 10%, 15%, 28%, 33%, and 35%). • 2012 Tax Act kept rates at 10%, 15%, 25%, 28%, 33%, and 35%, but added 39. 6% rate.

Tax Foundation. In 2009, the top 1% of tax returns earned 16. 9 % of AGI and paid 36. 7% of all federal individual income taxes. Top 5% earned 31. 7% of AGI, but paid 58. 7%. Among tax returns with a positive AGI, taxpayers with an AGI of $159, 643 or more in 2009 were the top 5 percent of income earners. In 2009, around 59 million tax returns (of 137. 98 million tax returns)used exemptions, deductions and tax credits to completely wipe out their federal income tax liability. The average tax rate in 2009 ranged from around 1. 9% of income for the bottom half of tax returns to 24. 0% for the top 1%.

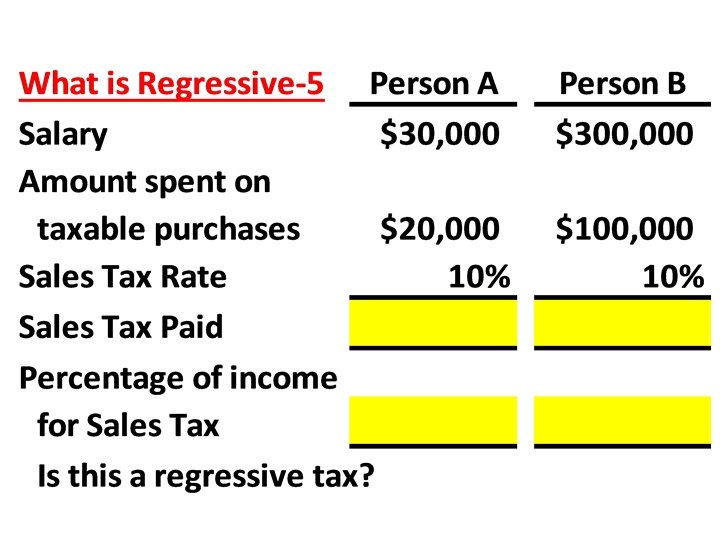

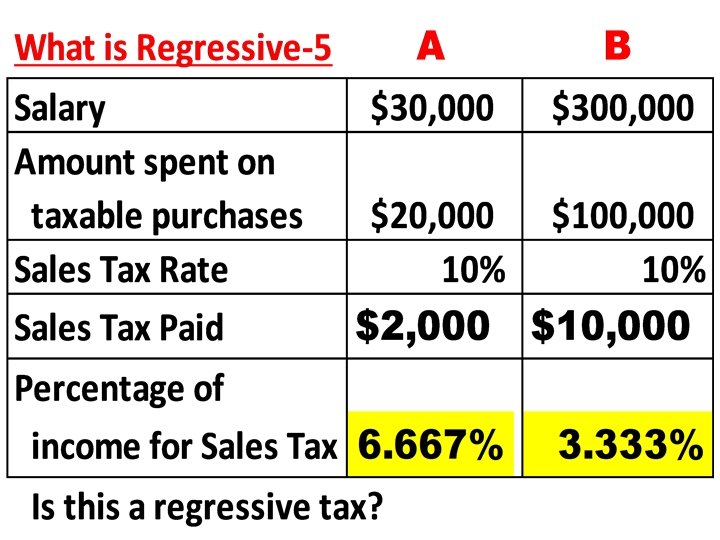

What is regressive? -1 Person A earning $30, 000 per year has a family including a spouse and 4 children. The state has a 10% sales tax. Suppose Person A spends $20, 000 on clothing, auto and other items subject to the sales tax. (Continued)

What is regressive? -2 Person A will pay a sales tax of $2, 000 on the purchases of $20, 000. That is 6. 67% of gross income that goes to sales tax.

What is regressive? -3 Person B earns $300, 000 per yr & has a family including a spouse & 4 children. The state has a 10% sales tax. Person B will likely spend proportionately less than Person A on purchases subject to the sales tax– measured as a percentage of gross income?

What is regressive? -4 Person B may spend only $100, 000 (or less) on consumer purchases. If that is the case, what percentage of this person’s gross income goes to sales taxes? Is the sales tax regressive?

What do you think? -1 Two persons are in the 35% marginal tax bracket because of equal salaries. A earns bonus of $20, 000 taxed at a 35% rate. B has $20, 000 of capital gains taxed at 15 percent. A pays an additional $7, 000 in tax. B pays only $3, 000 in tax on the additional $20, 000 of income. Do we see horizontal equity, which dictates that equal incomes should be taxed equally.

What do you think? -2 A wealthy person invests in municipal bonds, and earned tax-exempt interest of $100, 000. Her neighbor, who is not wealthy, earns a salary of $100, 000. The working person may pay taxes at rates up to 25 to 30 percent. Is this equitable? Both taxpayers have the same inflow of income, but one is able to avoid tax because of his or her wealth and ability to invest in tax-sheltered investments.

What do you think? -3 The individual investing in a municipal bond may accept a market rate of interest of 4%, passing up a market rate of interest of 6% on corporate bonds which pay interest that is taxable. If the individual earned $100, 000 on 4% bonds, she could have earned $150, 000 if she had chosen 6% corporate bonds. You could say that she has paid a tax, by loaning money to a local government at a low interest rate, accepting less interest.

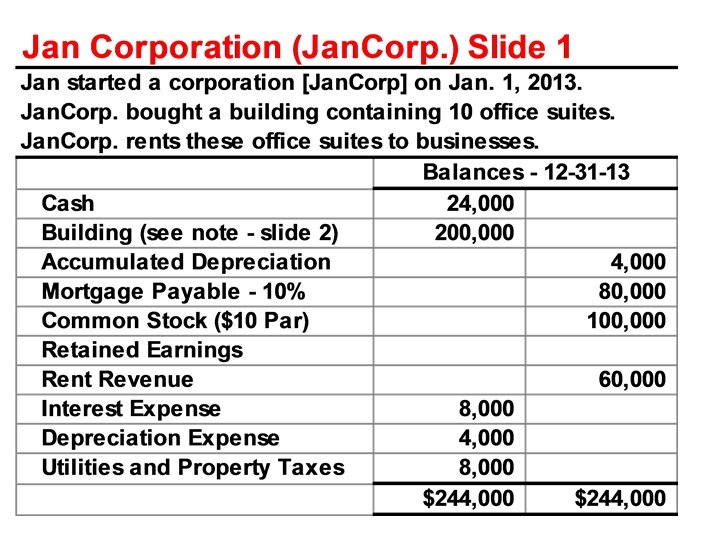

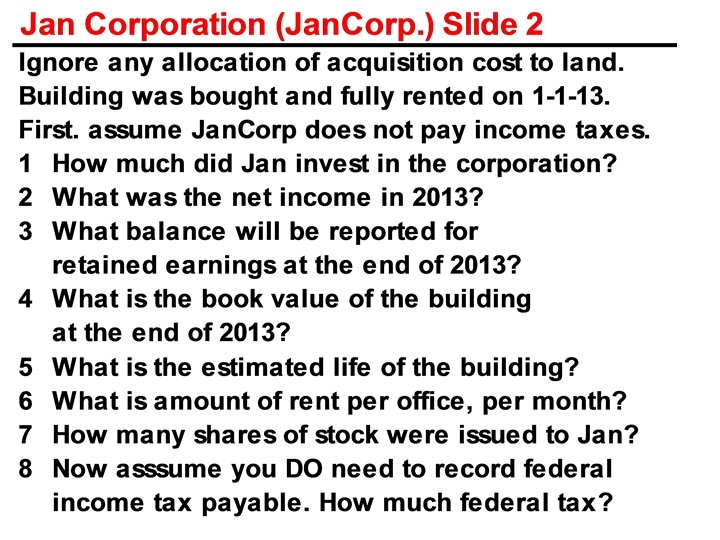

The following four slides have an introductory case, which we can use as a basis for discussing items later in this chapter. Please see how many of the questions you can answer.

Jan Corporation (Jan. Corp. ) Slide 3 Suppose a tenant came to Jan Corporation’s office on 12 -31 -13 and gave a check for rent for one office for 2014. Tenant paid for all of 2014. This transaction was not recorded in the accounts, shown on slide 1 for Jan. Corp. Assume you make the appropriate entry for this check received on 12 -31 -13. How will your entry for this payment change the list of accounts and balances shown on Slide 1 for Jan. Corp? How will it change the amount of federal income tax owed for 2013? See Chapter 19 of Kieso-page 1001 (13 th edition).

Jan Corporation (Jan. Corp. ) Slide 4 Explain how you might compute the tax owed by Jan. Corp for: Sales tax. Property tax. Franchise tax. Income tax. (Ignore statement earlier that the corporation does not pay income tax. )

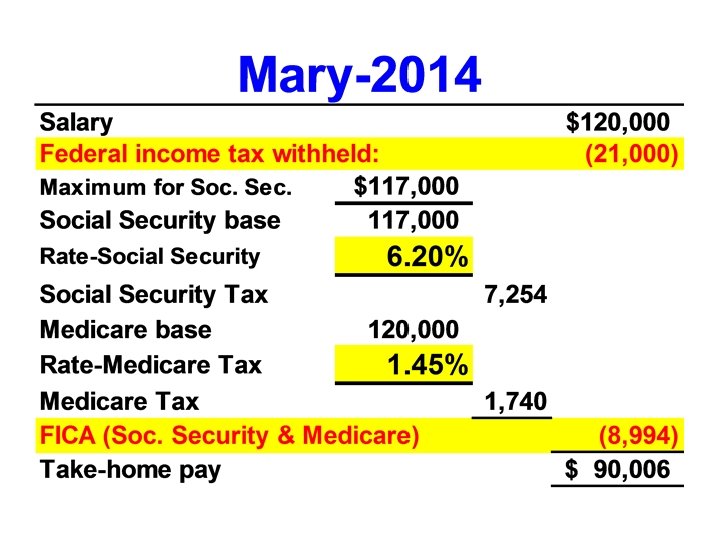

Mary’s salary is $120, 000 per year. Her federal income tax withheld is $21, 000. There is no state income tax. What is her take-home pay for the year? See following slide.

Sources of Federal Income Tax Law

Sources of Fed. Income Tax Law • Legislative – Law (Internal Revenue Code) • Administrative – Treasury Regulations – IRS Pronouncements • Judicial – Supreme Court – Other courts

Income What is Gross Income? What are Exclusions? What is a Deferral?

GAAP vs. Tax What are some differences between tax accounting rules and GAAP Rules?

Deductions What are some types of deductions?

Deduction vs. Credit-Pg 22 • Mary spends $1, 000 for child care for her child. This is necessary for Mary to have a job. • Why would Mary prefer to treat the expenditure as an income tax credit rather than as an income tax deduction?

Deduction vs. Credit-Pg 22 • Mary spends $1, 000 for child care for her child. Why would Mary prefer to treat the expenditure as an income tax credit rather than as an income tax deduction? • A $1, 000 credit reduces tax by $1, 000. A deduction reduces taxable income.

Filing Requirements • Return must be filed annually • Calendar-year individuals file and pay on or before the 15 th day of April – May receive an extension of time to file but not time to pay • Corporate returns due 15 th day of 3 rd month (March 15) • Extensions of time to file – Individuals: 6 months – Corporations: 6 months

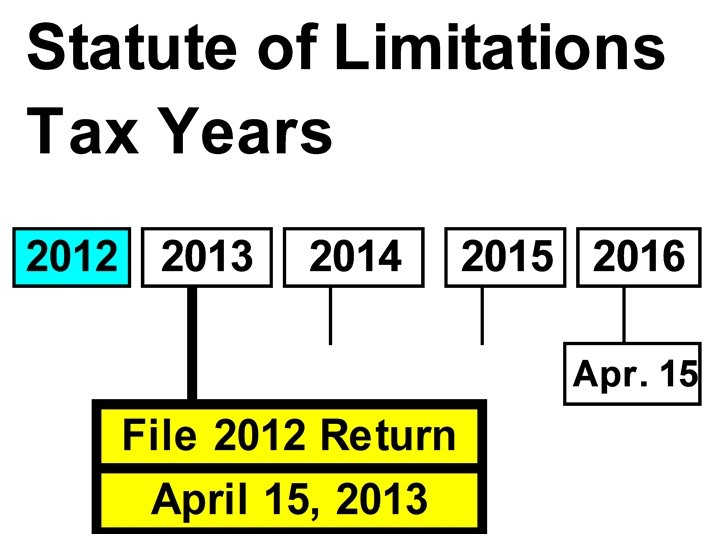

Statute of Limitations. Period of time beyond which legal actions or changes to the tax return cannot be made by taxpayer or IRS • Normally three years from filing date • Extends to six years if income is underreported by 25% of gross income • No limitation for fraud or if no return is filed

Jennifer - Statute of Limitations. Identify the tax issue. Jennifer did not file a tax return for 2007 because she honestly believed that no tax was due. In 2013, the IRS audits Jennifer and the agent proposes a deficiency of $500.

Jennifer - Statute of Limitations. Solution: Will Jennifer be required to pay the $500 deficiency? Does the statute of limitations apply when no tax return is filed?

Stewart - Statute of Limitations. On his 2013 tax return, Stewart inadvertently overstated deductions in excess of 25 percent of the adjusted gross income on the return. In 2013, the IRS audits Steward and the agent proposes a deficiency of $1, 000.

Stewart - Statute of Limitations. Solution: Can the IRS collect the deficiency of $1, 000? Does the statute of limitations prohibit the assessment of additional tax?

Statute of Limitations Refund claims must be initiated by taxpayer within later of – 3 years of filing date for return – 2 years from date tax is paid

Susie Quick filed her 2013 income tax return on February 15, 2014. She later discovered that she failed to take an exemption for her son on the 2013 tax return. Otherwise, the tax return was correct. What is the latest date by which she may file a claim for refund for tax year 2013? a. March 15, 2016. b. April 15, 2016. c. February 15, 2017. d. April 15, 2017. e. April 15, 2020 Ans. d

Jackson Corp. , a calendar-year corporation, mailed its 2013 tax return to the IRS by certified mail on Friday, March 11, 2014. The return, postmarked March 11, 2014, was delivered to the IRS on March 18, 2014. The statute of limitations on Jackson's corporate tax return begins on a. Dec. 31, 2013. b. March 11, 2014. c. March 15, 2014. d. March 18, 2014. CPA Nov. 1994 . Ans. c

Keen, a calendar‑year individual taxpayer, reported a gross income of $100, 000 on his 2008 income tax return. He inadvertently omitted from gross income was a $40, 000 commission that should have been included in 2008. Keen filed his 2008 return on March 15, 2009. To collect the tax on the $40, 000 omission, the Internal Revenue Service must assert a notice of deficiency no later than a. March 15, 2014. b. April 15, 2014. c. March 15, 2015. d. April 15, 2015. Ans. d

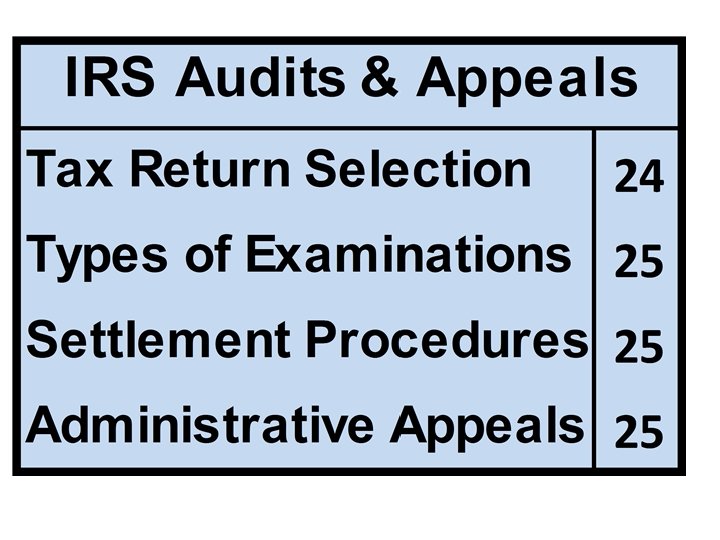

Audit and Appeals Process Selection for Audit • Only about 2% of returns are audited • Procedures used – Discriminant Function System – Taxpayer Compliance Measurement Program – Document perfection & Information matching

Types of Audits –Correspondence audit – verify one or two items in question by mail –Office audit – requires some analysis & IRS judgment through interview –Field audit – typically limited to examination of business returns

Audit and Appeals Process • Settlement Procedure –Report of outcome of audit –Waiver of assessment (Form 870) – 30 -day letter • Appeals –Meeting with IRS Appeals Division – 90 -day letter

Audits and Appeals • 30 -day letter – 30 days to request conference with Appeals Division – Appeals officer can consider hazards of litigation

Audits and Appeals • 90 -day letter (statutory notice of deficiency) – File petition with Tax Court within 90 days – Pay the tax; can then go to court to sue for refund – Take no action and be subject to IRS enforced collection procedures

Which of the following types of IRS audits involves the least extensive audit procedures? a. Office audit b. Field audit c. Correspondence audit. d. all are equally extensive Ans. c

Audit and Appeals. After an audit is concluded, a taxpayer who does not agree with the audit findings will receive a: a. Letter Ruling b. 30 -day letter c. 90 -day letter d. Revenue Ruling Ans. b

Exclusions from Gross Income (All Taxpayers) Tax-exempt interest Nontaxable stock dividends Nontaxable stock rights Proceeds of life insurance policies Tax refunds to the extent no prior tax benefit was received • Disallowed and deferred gains and losses on property transactions • Unrealized gains and losses • • •

Exclusions from Gross Income (Individual Taxpayers Only) Nontaxable part of pension plan distributions Nontaxable portion of Social Security benefits Damages awarded for physical injury Gifts and inheritances Welfare benefits (food stamps, workman’s compensation and family aid) • $250, 000 or $500, 000 gain on sale of personal residence • Scholarships • Qualified employee fringe benefits • • •

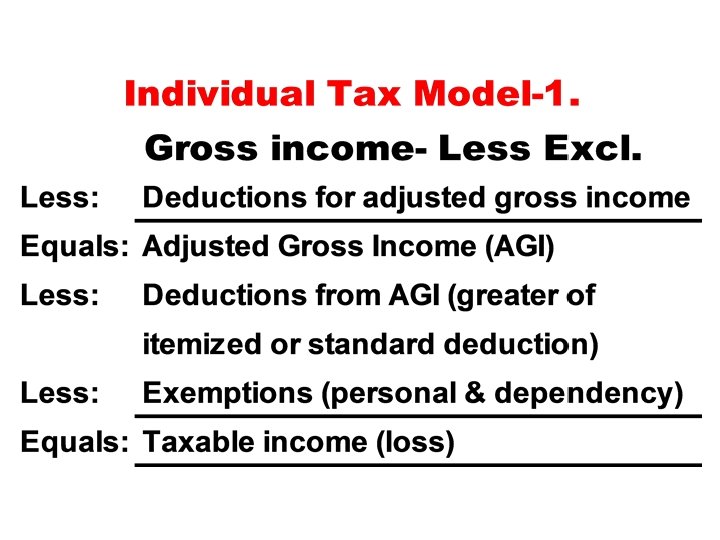

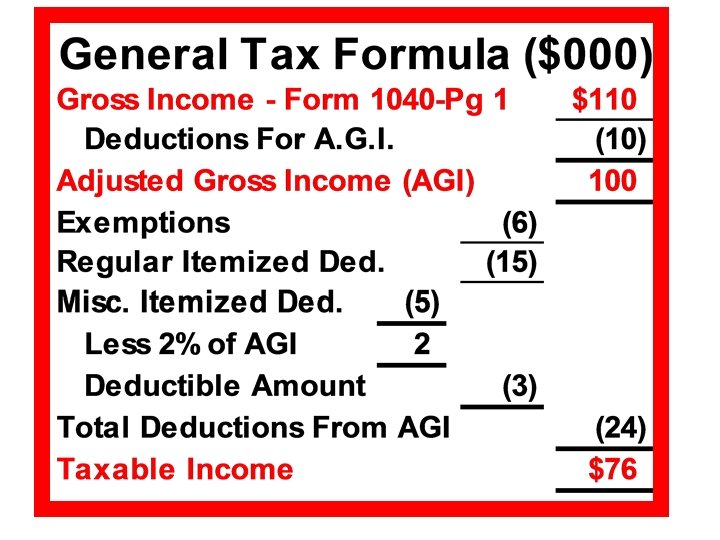

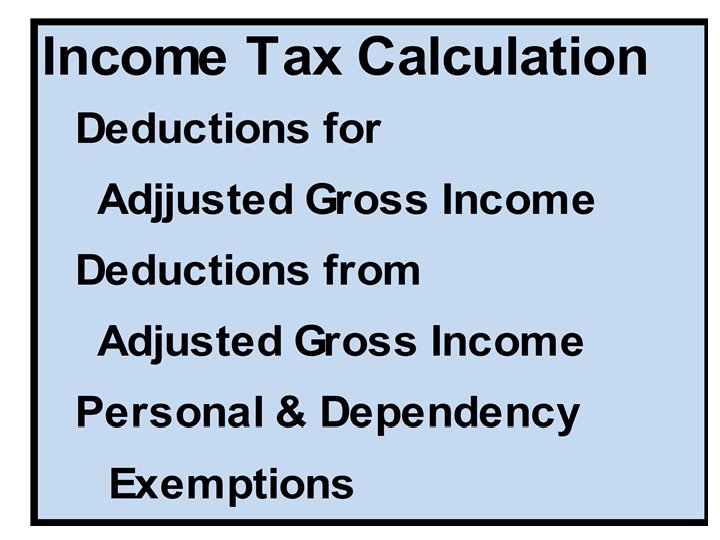

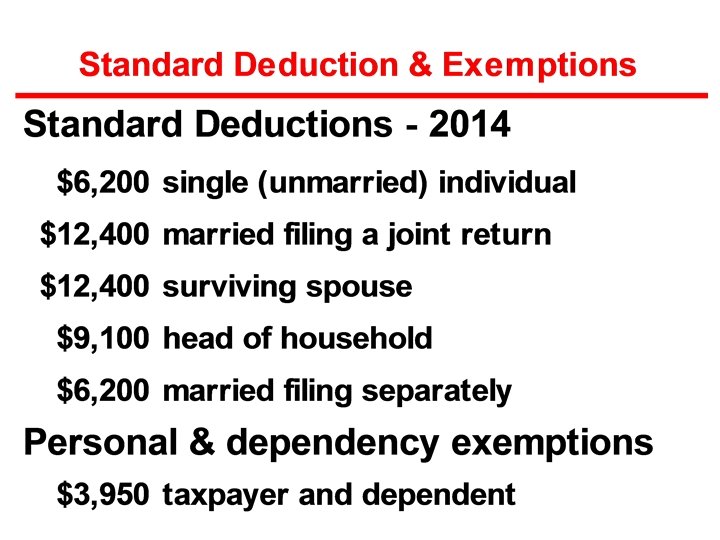

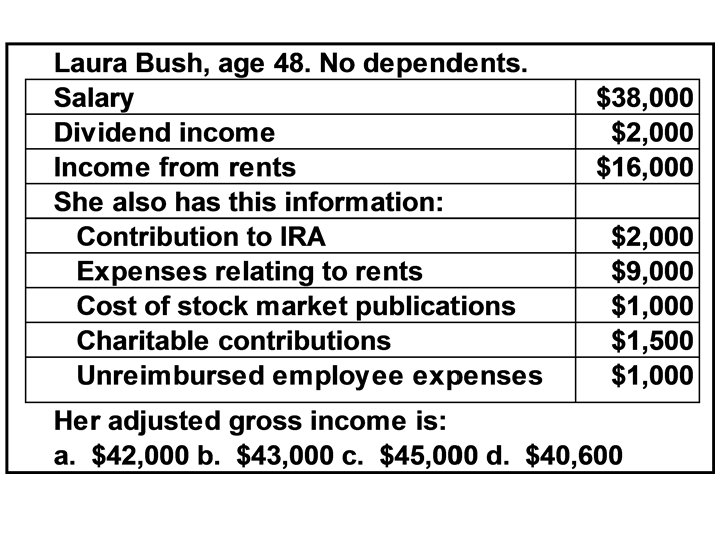

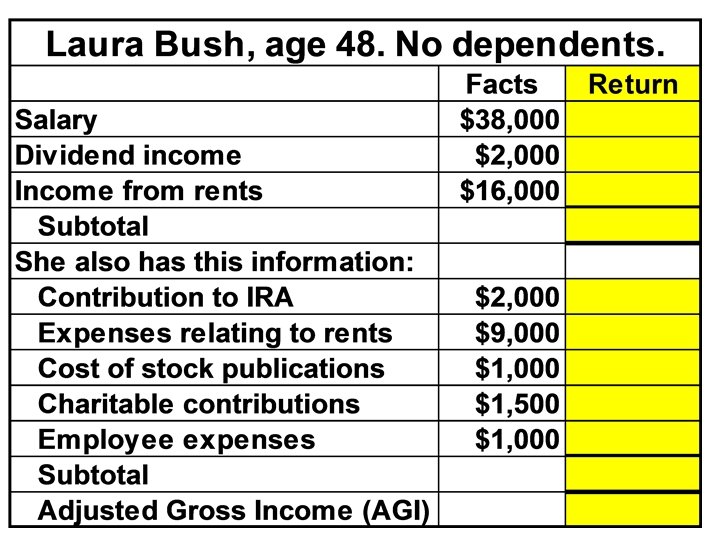

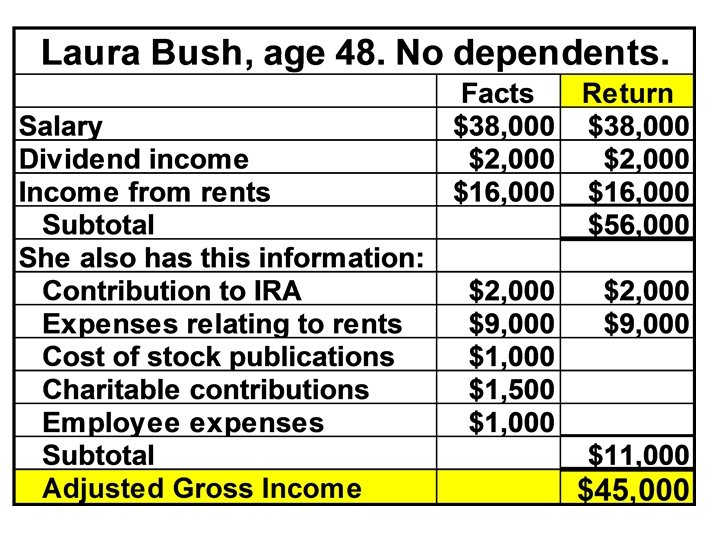

Deductions • Corporations – all business expenses are deductible if ordinary, necessary, and reasonable (unless disallowed by law) • Individuals – Deductions for AGI – Deductions from AGI – greater of itemized deductions or standard deduction – Personal and dependency exemptions

Deductions For AGI – (Form 1040 - Pg 1) “Above-the-line” deductions • Property losses on Schedule D - $3, 000 • Contributions to pension & retirement plans • Health savings account contributions • Moving expenses • One-half of self-employment taxes • Self-employed health insurance premiums • Penalty on early withdrawal of savings • Tuition deduction ($4, 000 limit) • Student loan interest ($2, 500 limit) • Alimony paid

Itemized Deductions – Individuals (Sched. A) • Medical (dental) expenses (in excess of 10% AGI) • Taxes (state, local, and foreign income and property taxes) • Interest (mortgage and investment) • Charitable contributions (up to 50% AGI) • Casualty & theft losses (in excess of 10% AGI) • Miscellaneous including unreimbursed employee business expenses and investment expenses (in excess of 2% AGI) • Gambling losses (up to gambling winnings)

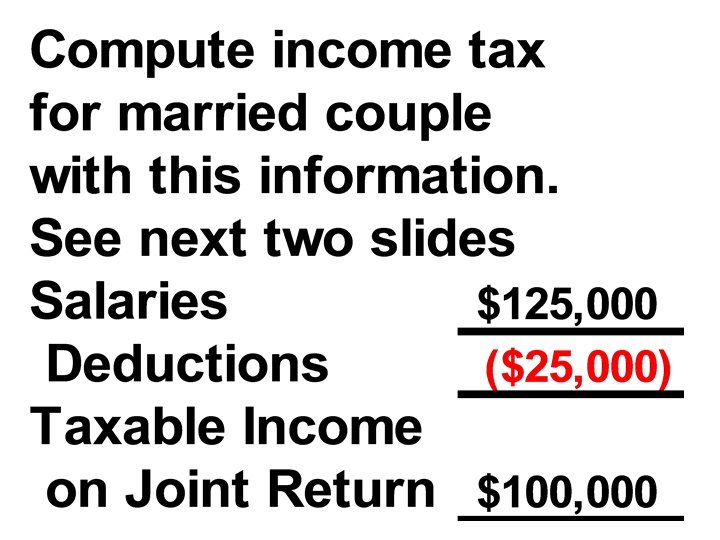

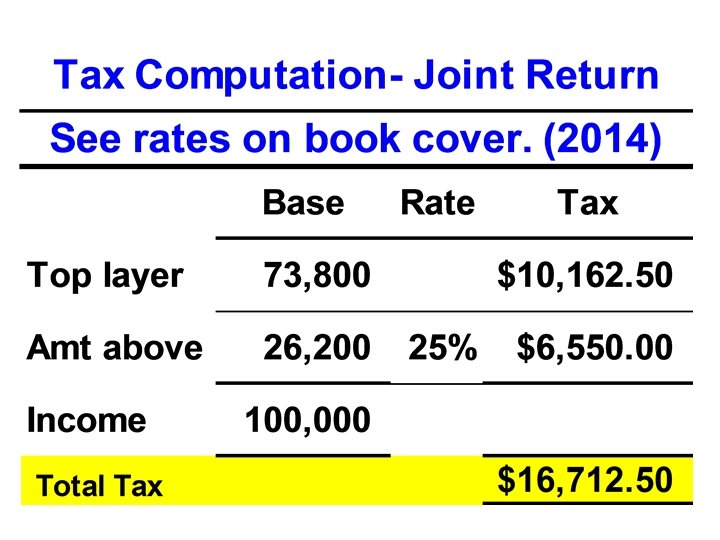

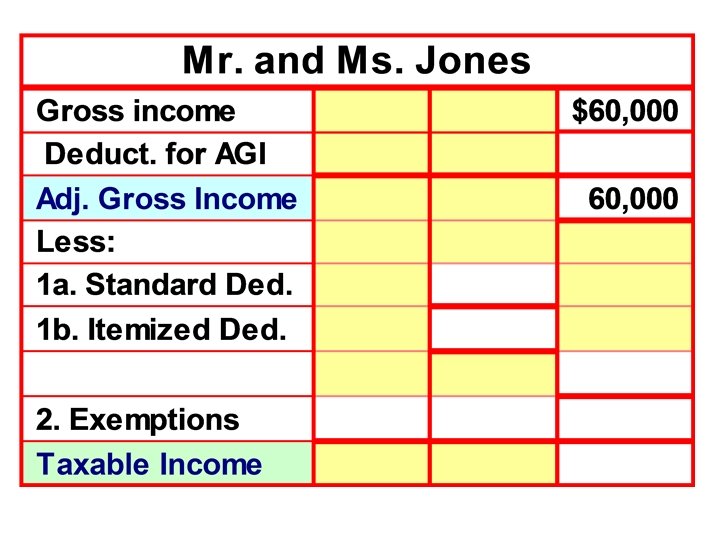

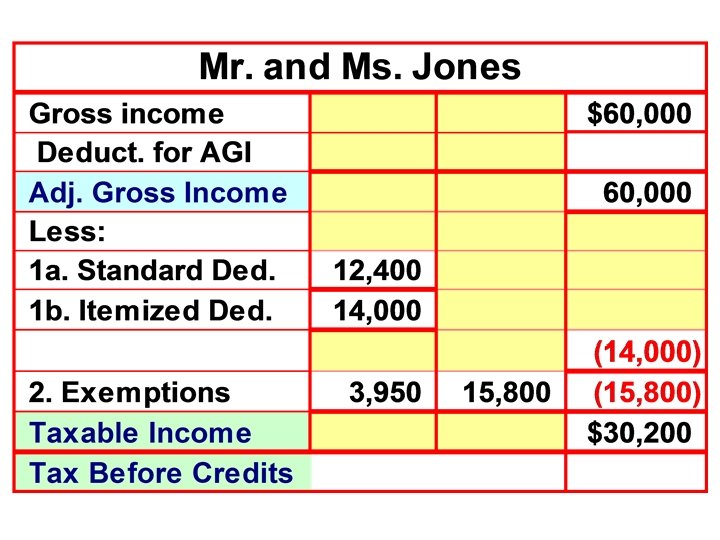

In 2014, Mr. and Ms. Jones have combined salaries of $60, 000. Their only expenditures affecting the tax return are state income taxes of $6, 000, mortgage interest of $7, 000 and real estate taxes of $1, 000. They have two small children whom they support, and file a joint return. What is their taxable income for 2014?

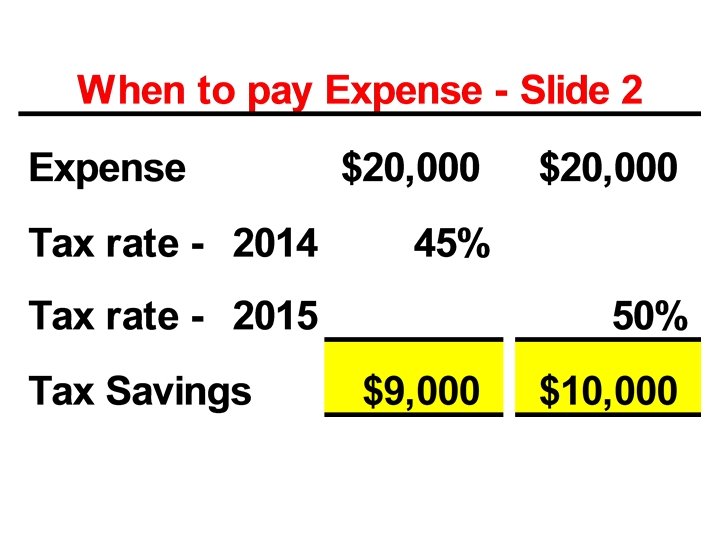

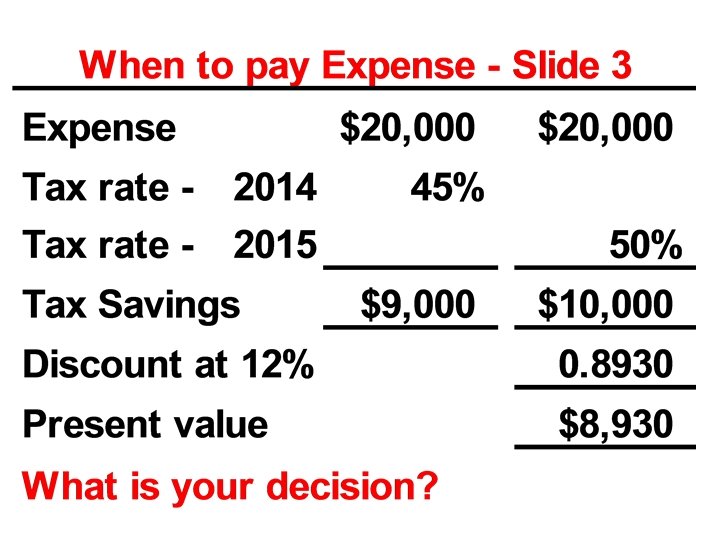

Taxes and Cash Flow • Tax cost is the increase in tax for the period and is a cash outflow • Tax savings is a decrease in tax for a period and is a cash inflow – Expense payment generates an outflow, but deduction generates a tax reduction – Reducing income taxes paid is a pure cash inflow because tax savings are not taxable

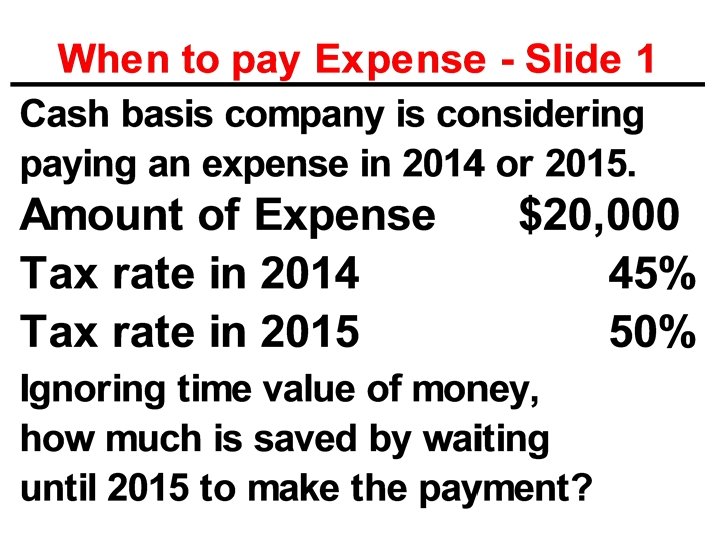

Taxes and Cash Flows • Cash flows in future years are discounted to their present value so they can be compared using comparable dollars • When marginal tax rates are expected to change from year to year, timing of transactions should be controlled to minimize tax costs and maximize tax savings

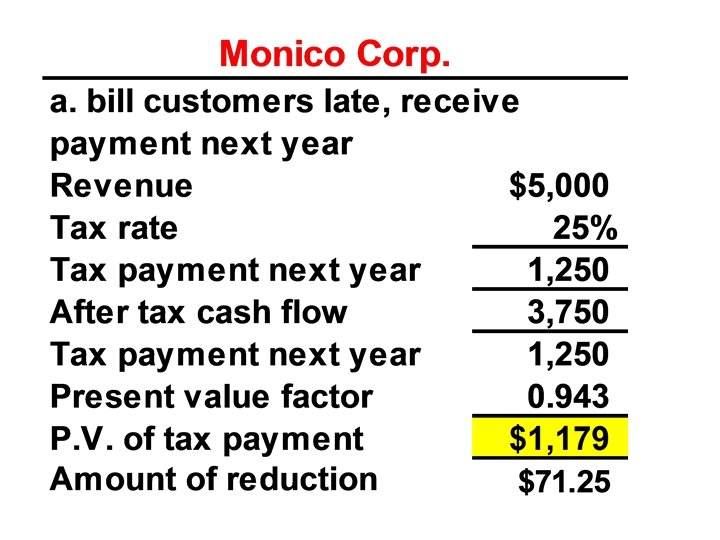

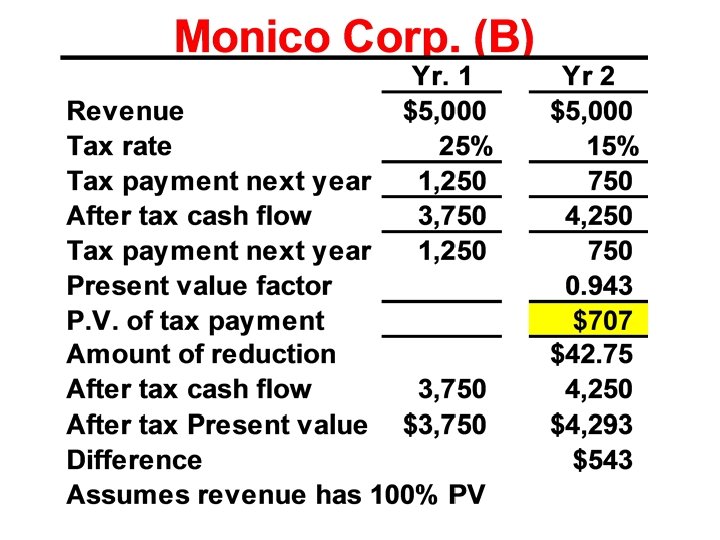

Monico Corp. , a cash basis calendar-year taxpayer, is in the 25 percent marginal tax bracket this year. If it bills its customers at the beginning of December, it will receive $5, 000 of income prior to year-end. If it bills its customers at the end of December, it will not receive the $5, 000 until January of next year.

Monico Corp. a. If it expects its marginal tax rate to remain 25 percent next year, when should it bill its customers? Use a 6 percent discount factor to explain your answer. b. How would your answer change if Monico’s marginal tax rate next year is only 15 percent? Explain. c. How would your answer change if Monico’s marginal tax rate next year is 34 percent? Explain.

Monico Corporation. Solution: a. Monico should wait to bill its customers until the end of December. If Monico’s marginal tax rate is 25%, taxes paid this year would cost $1, 250 ($5, 000 x 25%) resulting in an after-tax cash inflow of $3, 750 ($5, 000 – $1, 250). When considering the time value of money, the cost of the taxes that are deferred until next year will have a present value (cost) of only $1, 179 ($1, 250 x. 943 PV factor) or $71 less ($1, 250 - $1, 179).

Monico Corp. Solution: b. If Monico’s marginal tax rate is 15% in year 2, then its after-tax cash inflow would be $4, 293 [$5, 000 – ($5, 000 x 15% x. 943 PV factor)]. Monico should defer billing its customers because this will result in a $543 higher after-tax cash inflow ($4, 293 - $3, 750).

Monico Corp. Solution: c. If Monico’s marginal tax rate is 34% in year 2, then its after-tax cash inflow would be $3, 397 [$5, 000 – ($5, 000 x 34% x. 943 PV factor)]. Monico should bill its customers in the beginning of December because deferral would result in a $353 after-tax cost ($3, 397 - $3, 750).

A single, wealthy investor earns net rental income of about $400, 000 per year. She does not have significant itemized deductions. She is considering giving some rental property (that generates net rental income of $20, 000 per year) to her elderly mother so that her mother will have income she needs for her living expenses. The investor expects that federal income taxes will be saved with this plan. Which tax planning concept applies here?

Professional Responsibilities • Avoidance versus evasion. • What is the difference between these terms?

Professional Responsibilities • Preparer penalties –Penalties may not be covered by malpractice insurance –Penalties are not deductible –Penalties may result in an IRS review of the preparer’s entire practice –Criminal tax evasion penalties include fines and prison

Professional Responsibilities • Tax professionals have responsibilities to both tax system and to clients • Sources of Guidance – Circular 230 – AICPA Code of Professional Conduct – Statements on Standards for Tax Services

Sources of Guidance. -1 Name three sources of guidance for tax professionals.

Sources of Guidance. -2 (1) Treasury Circular 230: Regulations Governing the Practice of Attorneys, Certified Public Accountants, Enrolled Agents, Actuaries and Appraisers before the Internal Revenue Service. (2) AICPA Code of Professional Conduct. (3) Statements on Standards for Tax Services. These contain guidelines for tax professionals.

SSTS - No. 4 – Slide 1. Statement on Standards for Tax Services No. 4 states that a CPA may use estimates in completing a tax return. When would using estimates be appropriate in tax return preparation?

SSTS - No. 4 – Slide 2. Estimates are appropriate when records are missing (for example, a flood or fire destroying records) or precise information is not available at the time of filing the tax return.

End