The Federal Reserve System FEDERAL RESERVE SYSTEM The

The seven member Board of Governors plus the President")

")

")

- Slides: 47

The Federal Reserve System

FEDERAL RESERVE SYSTEM The Federal Reserve System is charged with using monetary policy to control the money supply n Regulating the lending activity (deposit creation) of the banking system n

FED INDEPENDENCE Members of the Board of Governors are appointed by the President and approved by the Senate. Their terms are 14 years. n Presidents of the regional Reserve Banks are appointed by each banks Board of Directors. n

FED INDEPENDENCE cont. Fed expenses are paid from its own earnings rather than Congressional appropriations. n Fed policy actions do not have to be ratified by the President or Congress. n

FEDERAL OPEN MARKET COMMITTEE (FOMC) The seven member Board of Governors plus the President of the Federal Reserve Bank of NY and four other Federal Reserve Bank Presidents (serving on a rotating basis) n Meets every six weeks to determine shortrun monetary policy n

Federal Reserve Districts and Federal Reserve Bank Locations Exhibit 1

Functions of the Federal Reserve System Control the money supply n Supply the economy with paper money (Federal Reserve Notes) n Provide check-clearing services n Hold depository institutions' reserves n Supervise member banks n Serve as the lender of last resort n Serve as a fiscal agent for the Treasury n

Check-Clearing Process Exhibit 2

MONETARY POLICY TOOLS Open market operations - the buying and selling of gov’t. securities by the Fed. n discount rate n reserve requirement n

Open Market Operations Exhibit 3

T-Account r =. 10 Assets Reserves Loans Liabilities $35, 000 $165, 000 Demand Deposits $200, 000

Examples If the required-reserve ratio is r=10%, then required reserves are equal to ____. n Excess reserves are equal to ____. n This bank can lend a maximum of _____. n

T-Account r =. 10 Assets Liabilities Reserves $20, 000 Securities $15, 000 Loans $165, 000 Demand Deposits $200, 000

Examples n n If the required-reserve ratio is r=10%, then required reserves are equal to ____. Excess reserves are equal to ____. If the Fed buys $15, 000 worth of government bonds from banks, total reserves will rise to _____ and excess reserves will equal to _____. After the purchase of securities by the Fed, if all banks makes loans until excess reserves equal 0 and there are no cash leakage, checkable deposits can expand by a maximum of _____.

WHY THE FED USES OPEN MARKET OPERATIONS MOST OFTEN more flexible n easily reversed n quick implementation n

MONETARY POLICY TOOLS Open market operations n discount rate - bank borrowing and lending can be influenced by changes in this interest rate n reserve requirement n

DISCOUNT RATE The interest rate that the Fed charges depository institutions that borrow reserves from it.

FEDERAL FUNDS MARKET A market where banks lend reserves to one another, usually for short periods of time

FEDERAL FUNDS RATE The interest rate banks charge one another to borrow reserves in the federal funds market.

POLICY IN ACTION Banks are more likely to borrow from other banks than the Fed n the spread between the disc. rate and the fed. funds rate is the key. n the signal effect of a change in the discount rate is often most important. n

FEDERAL FUNDS RATE TARGET Reports by media frequently stress the Fed’s announcement about changes in the federal funds rate target n The Fed can influence the federal funds rate by altering the amount of reserves in the system n Financial markets normally react to an announcement by the Fed n

MONETARY POLICY TOOLS Open market operations n discount rate n reserve requirement - the size of the simple deposit multiplier can be altered by changing r. n

RESERVE REQUIREMENT The rule that specifies the amount of reserves a bank must hold to back up deposits

POLICY IN ACTION changes in the reserve requirement are probably the least used policy tool n the impact is too large, difficult to control, and hard to reverse in a relatively short time period. n

Fed Monetary Tools and Their Effects on the Money Supply Exhibit 5 FED MONETARY TOOL MONEY SUPPLY OPEN MARKET OPERATION Buys government securities Sells government securities Increases Decreases REQUIRED-RESERVE RATIO (r) Raises r Lowers r Decreases Increases DISCOUNT RATE Raises rate (relative to the federal funds rate) Lowers rate (relative to the federal funds rate) Decreases Increases

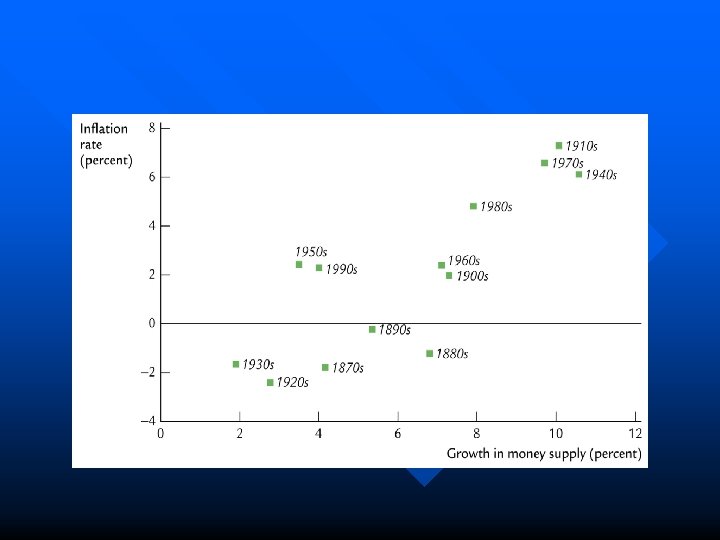

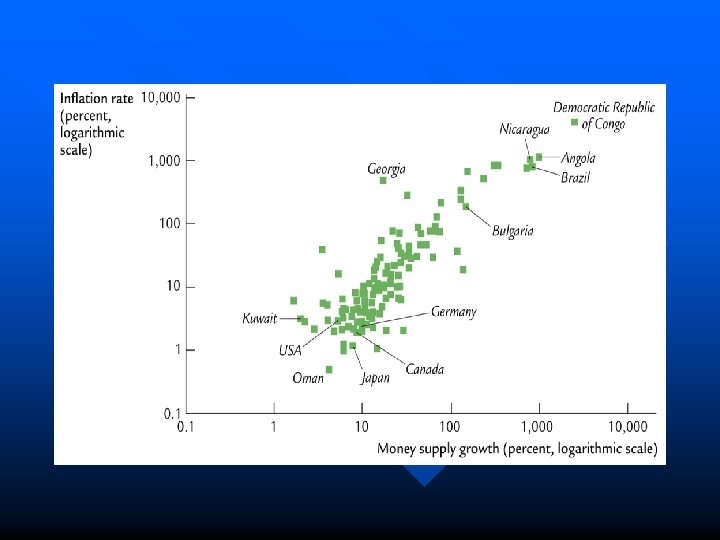

EQUATION OF EXCHANGE MV=P Q n M is the money supply n V is the velocity of money n P is the price level n Q is the real GDP n

MONETARIST POLICIES Changes in the money supply have a direct impact on AD and thereby change nominal GDP. n Equation of Exchange MV = PQ n V is stable n

MONETARIST POLICIES If Real GDP rises by 3% a year, any increase in M greater than 3% will cause increases in the price level. n Increases of less than 3% will inhibit economic growth or cause deflation n the FED should use a money growth rule instead of discretionary policy. n

The Monetarist Position Exhibit 6 B CONDITION INDIVIDUALS ARE HOLDING… SPENDING… GDP… Ms > Md Too much money (Disequilibrium) Increases Rises Ms < Md Too little money (Disequilibrium) Decreases Falls Ms = Md (Equilibrium) Does not change The right amount of money

MONETARIST POLICY OUTCOMES If the economy is initially in long-run equilibrium n an increase in the money supply will increase Price and Real GDP in the short run n in the long-run, only prices will rise n

Monetarism in an AD-AS Framework Exhibit 5 (1 of 4)

MONETARIST POLICY OUTCOMES If the economy is initially in long-run equilibrium n a decrease in money supply will lower the Price level and Real GDP in the short run n only Price level will be lower in the longrun. n

Monetarism in an AD-AS Framework Exhibit 5 (2 of 4)

APPROPRIATE POLICIES n What are the appropriate monetary policies to close a recessionary gap? – buy bonds – decrease discount rate – decrease reserve requirement

APPROPRIATE POLICIES n What are appropriate monetary policies to close an inflationary gap? – sell bonds – increase the discount rate – increase reserve requirements

KEYNESIAN VIEW vs. MONETARIST VIEW n Monetarist View - Changes in money supply can directly affect output in the short run - Changes only price level in the long run

KEYNESIAN VIEW vs. MONETARIST VIEW n Keynesian View - Uses money market model to predict the effect of monetary policy on the interest rate - I and C are tied to the interest rate - Changing the interest rate alter the level of aggregate spending

INTEREST RATES REAL RATE - the rate of return banks must have to cover costs and provide a return to investors n NOMINAL RATE - real rate plus the expected rate of inflation n

DEMAND FOR MONEY The inverse relationship between the quantity of money balances and the interest rate n the interest rate is the opportunity cost of holding money n

Demand for, and Supply of Money Exhibit 1 Interest Rate Supply of Money i 2 i 1 Demand for Money 0 M 2 M 1 Quantity of Money (a) 0 Quantity of Money (b)

Equilibrium in the Money Market Interest Rate S 1 i 2 Excess Supply of Money Equilibrium in the money market i 1 i 3 D 1 Excess Demand for Money 0 M 1 Quantity of Money

BONDS AND INTEREST RATES bonds have a face value n bonds pay a fixed interest payment each year (coupon pmt) n bond prices are determined by the relationship between current interest rates and the bond’s rate n

BONDS AND INTEREST RATES Bond Prices are inversely related to the current interest rate. n If current interest rates are higher than the bond’s rate then the bond will sell below face value n If interest rates fall, bond prices rise n

KEYNESIAN VIEW An expansionary Monetary Policy could fail to stimulate AD Fiscal Policy is more effective n Liquidity Trap - Investment spending may not be increased even at very low interest - All participants prefer hold money - Increase in MS will not reduce int. rate - No increase in AD n

KEYNESIAN VIEW n Pessimistic Business Expectations - Investment demand decreases - Lower interest rates may NOT be associated with higher investment spending - Monetary policy will again prove ineffective