The Federal Reserves Unconventional Monetary and Credit Policies

: depository")

: holders")

• March 2008")

: “We identified at least 18 former")

from the")

- Slides: 12

The Federal Reserve’s Unconventional Monetary and Credit Policies Scott Burns Ursinus College Lawrence H. White George Mason University Cato Institute Monetary Conference, 15 November 2018.

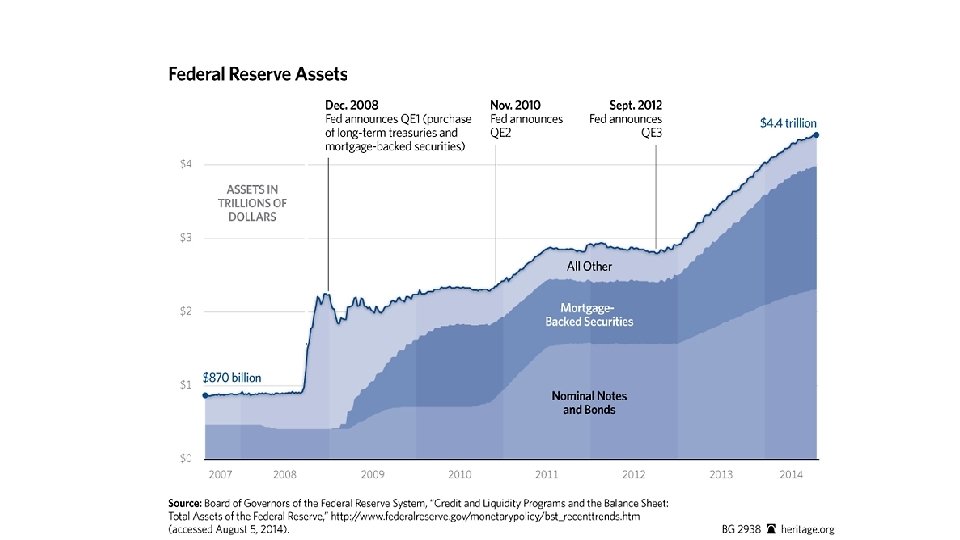

Federal Reserve’s asset portfolio October 2007 TOTAL November 2018 $885. 3 b TOTAL $4141. 9 b Gold certs + SDRs 1. 5% Gold certs + SDRs 0. 4% U. S. Govt. sec. 88. 1% U. S. Govt. sec. 54. 8% Mortgage-backed sec. 0. 0% 40. 3% Repos 5. 6% Mortgage-backed sec. ($1669 b) Loans to banks 0. 0% Repos 0. 0% Other assets 4. 8% Loans to banks 0. 0% Other assets 4. 5%

Quantitative Easing was not a monetary policy M 0 M 2/10

Preferred credit programs and their beneficiaries 1 • Term Auction Facility (Dec. 2007): depository institutions • Dollar Swap Lines (Dec. 2007): foreign-domiciled commercial banks doing US dollar business • Term Securities Lending Facility (Mar. 2008): primary dealers • Primary Dealer Credit Facility (Mar. 2008) • Asset-Backed Commercial Paper Money Market Mutual Fund Liquidity Facility (Sept. 2008) • Commercial Paper Funding Facility (Oct. 2008) • Term Asset-Backed Securities Loan Facility (Nov. 2008): holders of MBS • Bridge Loan to JP Morgan Chase (Mar. 2008): JPMorgan Chase; Bear Stearns shareholders, bondholders, and counterparties • Maiden Lane LLC (Mar. 2008): Same as previous • Revolving AIG Credit Facility (Sept. 2008): AIG and counterparties • Credit extensions to affiliates of some primary dealers (Sept. 2008): four broker-dealer firms

Preferred credit programs and their beneficiaries 2 • Securities Borrowing Facility (Oct. 2008): holders of MBS • Maiden Lane II LLC (Nov. 2008): AIG counterparties, esp. Goldman Sachs • Maiden Lane III LLC (Nov. 10, 2008): same • Citigroup non-recourse lending commitment (Nov. 2008) • Bank of America non-recourse lending commitment (Jan. 2009) • Agency Mortgage-Backed Securities Purchase Program (Nov. 2008): bondholders of Fannie Mae and Freddie Mac • Operation Twist 2 (Sept. 2011; enlarged June 2012): holders and guarantors of MBS, housing finance firms • QE 1 (Jan. 2009), MBS purchases: same • QE 3 (Sept. 2012), ongoing MBS purchases: same

Preferential Credit to Primary Dealers • Primary Dealer Credit Facility (PDCF) • March 2008 – Feb. 2010 • Overnight collateralized loans to primary dealers • “created by the Federal Reserve under the authority of Section 13(3) of the Federal Reserve Act” • Term Securities Lending Facility (TSLF) • March 2008 – Feb. 2010 • Let primary dealers swap riskier assets on their balance sheets for Treasury securities to employ as collateral for PDCF loans • Domestic primary dealers: Citigroup, Goldman Sachs, J. P. Morgan Securities, Merrill Lynch, Morgan Stanley, Well Fargo Securities

Preferential Credit to housing • Board of Governors press release, 6 October 2008: • “The payment of interest on excess reserves will permit the Federal Reserve to expand its balance sheet as necessary to provide the liquidity necessary to support financial stability while implementing the monetary policy that is appropriate in light of the System's macroeconomic objectives. ” • bail outs, targeted lending, MBS purchases; but no rise in M 2 path • Bo. G press release, 25 November 2008, re QE 1’s MBS purchases: • “This action is being taken to reduce the cost and increase the availability of credit for the purchase of houses, which in turn should support housing markets and foster improved conditions in financial markets more generally. ” • Operation Twist 2

Regulatory capture, esp. at FRBNY • GAO (2011): “We identified at least 18 former and current Class A, B, and C directors from 9 Reserve Banks who were affiliated with institutions that used at least one emergency program. ” • “According to FRBNY officials, FRBNY’s Capital Markets Group contacted representatives from primary dealers, commercial paper issuers, and other institutions to gain a sense of how to design and calibrate some of the emergency programs. ” • E. g. , “GE was one of the largest issuers of commercial paper and General Electric was one of the companies FRBNY consulted when creating the emergency program to assist with the commercial paper market. ” • Meanwhile, General Electric’s CEO (Jeffrey Immelt) was a Class B director of FRBNY

Regulatory capture, esp. at FRBNY, cont. • 2008 FRBNY directors also included • JP Morgan Chase CEO (Jamie Dimon) • Lehman Brothers CEO (Richard Fuld) • Goldman Sachs board member (Stephen Friedman, NYFRB board chairman) • JP Morgan Chase, Lehman, and Goldman Sachs were all beneficiaries of Fed credit allocation programs • Esp. , NYFRB had AIG (under its receivership) repay Goldman and others 100 cents on the dollar on CDOs that might have been settled for less (Teitelbaum and Son 2009) • Friedman also led the search to replace Timothy Geithner, and chose William Dudley, who had spent 10 of the previous 12 years as a Goldman Sachs partner, managing director, and chief economist

To end regulatory capture • Dodd-Frank removes Class A directors (commercial bankers) from the process of appointing the FRB presidents • Unfortunate reduction of bankers’ FOMC input • Better reform: legislation to require the Federal Reserve System to leave fiscal and credit-allocation policies to Congress