Introduction Private Equity Course coordinator Stefan Sjgren Course

• Four assignments (groups of 4 -5) (40")

• “Takeovers, corporate breakups, divisional spin-offs,")

Help active")

")

. Region Amount")

- Slides: 68

Introduction: Private Equity Course coordinator: Stefan Sjögren Course adm. Gabriella Jaxdal

Course description Content • This course is issue oriented. The main question is what is the contribution of the capital market to innovation in the economy? The focus is on two special purpose financial intermediaries; • private equity and venture capital funds. We discuss and analyze the operations of the funds, their relations with the investors, limited partners, and with the users of the funds, entrepreneurs. • We also examine the funds in a broader macroeconomic and financial context. The course mixes conceptual presentation, empirical tests and observations, and practical "hands on” techniques. It takes materials from financial economics, from international finance, from development economics and international trade, and from the practice of private equity and venture capital funds. • The various papers assigned as readings are not parts of a textbook, most of them are research papers. Yet, in the class we focus on the managerial aspects as well to create an integrated view of what private equity and venture capital finance is all about.

Online adoptation • Due to the new situation where all courses from now on are based on remote teaching, we have rescheduled the course and changed the examination forms. The new examination will be: – The learning outcomes are assessed through four mandatory group assignments and a written exam (“home exam”). The group assignments (10% each) and the written exam (60%) are weighted together to reach the total points. • The course is divided into four broad topics. Each topic ends with the hand in and discussion of a group assignment. Each group will also be introduced to a PE- or a VC-case. The students should choose one of the cases and use it as basis for answering the questions and assignment connected to each topic, together with the literature.

Learning outcomes Upon completion of the course the student will have the ability to: 1) identify the many dimensions of private equity and venture capital finance. 2) demonstrate knowledge and understanding of the micro economics and macro finance environment in which money is transferred from savers to investors in high risk capital. 3) demonstrate knowledge and understanding of the financial management aspects of high risk capital, in particular the process of valuation, contracting, financing, and exit. 4) demonstrate knowledge and understanding of the modus operandi of the private equity and venture capital industry in Sweden and in the world.

Course evaluation • Overall a good course – The hands on evaluation and calculation is appreciated – Balance between VC and PE – To much to read! – Why a short list? We read a lot of unnecessary things?

Schedule

The Teachers Shubhashis Gangophadhay Is a visiting professor at the School of Business, Economics and Law. He the Dean of the Indian School of Public Policy, Founder and Research Director of the IDF. He received his Ph. D. in Economics from Cornell University and. In 2006, he was awarded a doctorate (honoris causa) by the University of Gothenburg, Sweden. Besides being an Advisor to the Finance Minister, Government of India, Dr. Gangopadhyay has been a Consultant on policies to various ministries including Finance, Planning, Industry and Rural Development. He is currently on the board of IDE-I (International Development Enterprises – India), besides handling a number of high-profile, policy advisory roles. Stefan Sjögren Is Associate Professor at the Department of Business Administration and affiliated to the Centre for Finance at the School of Business, Economics and Law, University of Gothenburg. His research interest covers a broad range of corporate finance issues and includes capital structure, venture capital, capital budgeting, deregulation, law and finance and efficiency measurement. Sjögren is the Director of Ph. D-program at his department and he teaches corporate finance and private equity on master and Ph. D-level. Aineas Mallios Aineas is a lecturer with a Ph. D in Business from the University of Gothenburg and a Research Master in Economics from the University of Luxembourg, as well as a MSc in Finance from the University of St Andrews and a BSc in Public and Business Administration – Finance from the University of Cyprus. His research is in the economics of innovation and corporate finance and he mostly does theoretical work.

Assignment Will be presented by Aineas Mallios

Exams • A written exam (60%) • Four assignments (groups of 4 -5) (40 %)

First week: topic and assignment

Private Equity The broad definition Private equity is money invested in companies that are not publicly traded on a stock exchange or invested as part of buyouts of publicly traded companies in order to make them private companies The narrow definition: 2021 -09 -03

Public markets • • • Has the capacity to spread financial risk of diversified portfolios Investors can customize its risk Transfer large, risky and illiquid projects into small , less risk and tradable securities. • But it comes with a cost - The Agency problem • The rebirth of “active investors”

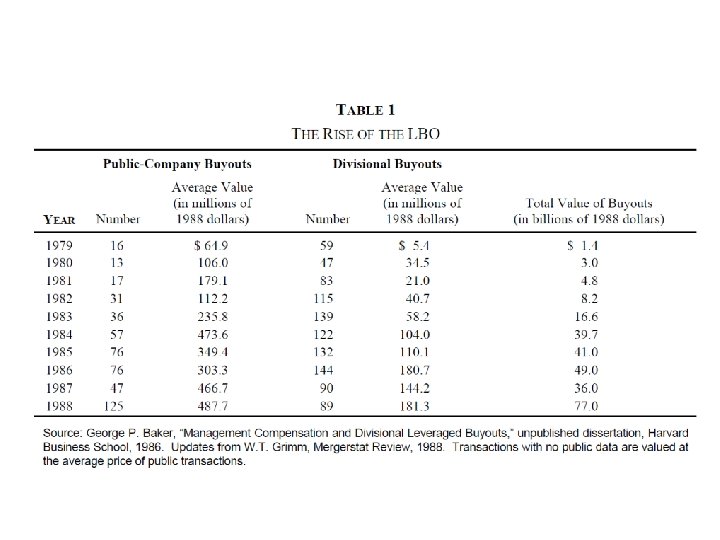

Jensen : ECLIPSE OF THE PUBLIC CORPORATION (1989) • “Takeovers, corporate breakups, divisional spin-offs, leverage buyouts and going private transactions are the most visible manifestation of massive organizational change in the economy” Jensen, p 2. • • • The capital market were in transition The most widespread going private transaction is LBO Entire industries are reshaped • The public corporation is not suitable when – Long term growth is slow – Internally generated funds cannot be invested in profitable projects – Downsizing is the best strategy

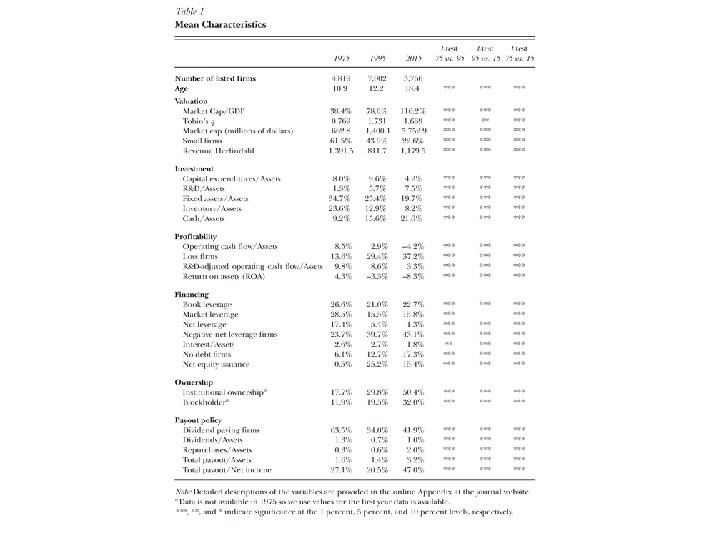

Public market development source Kahle, K. M. , & R. M. Stultz is the US Public Corporation in Trouble

LBO as an efficient intermediary • • • Management incentives are built around a strong relationship between pay and performance LBOs are more decentralized LBOs have well-defined obligations to their creditors and residual claimants LBO create large gains? LBO increase operating efficiency without massive layoffs. LBOs uses debt

Leverage buy out • To aquire a company with borrowed money and use the existing firm’s asset as collateral. • MBO – it is manangers of existing firms that buy the firm with levered equity (debt)

LBO example

The leveraging issue • • • Reduces cash (a substitute for dividends) Help active investors to monitor the firm Insolvency can be less costly with high leverage No impact on operations (transfer of ownership) Creates better capital structures To sell shares that are illiquid • But was Jensen right?

Value creation in the PE and VC industry (Kaiser and Westarp)

Private equity – a response to the problem of agency costs

Venture capital – Solving the problem with asymmetric information • Hidden information – Due diligence, low search costs • Hidden actions – Monitoring, efficient contracts • Risk spreading

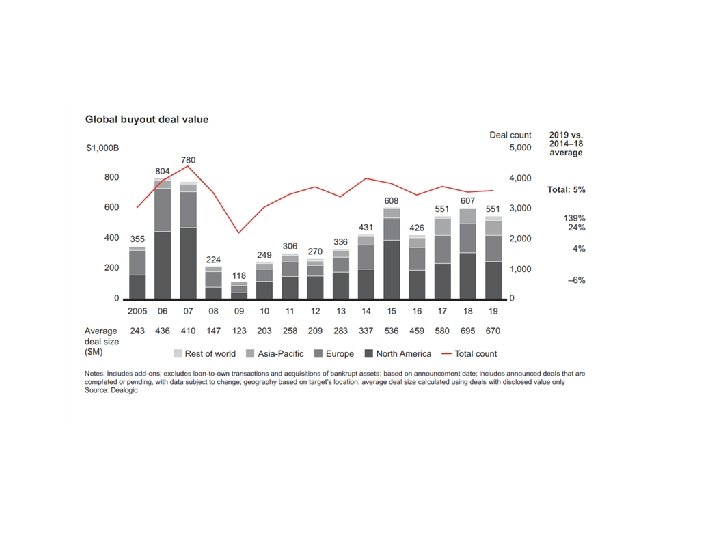

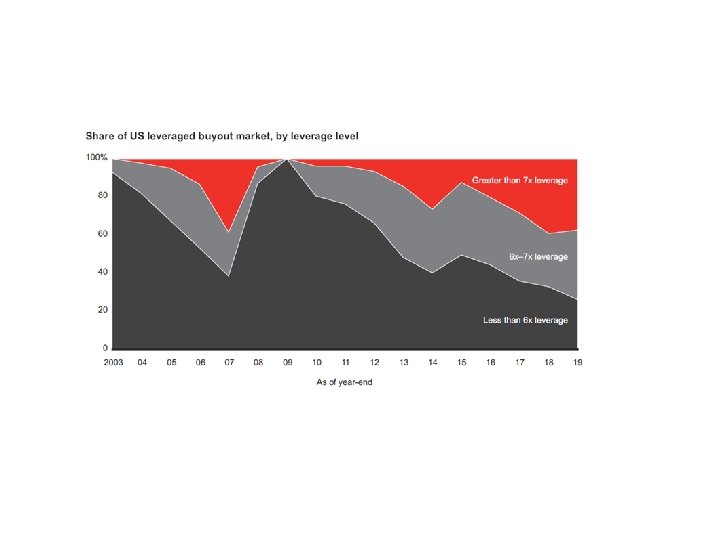

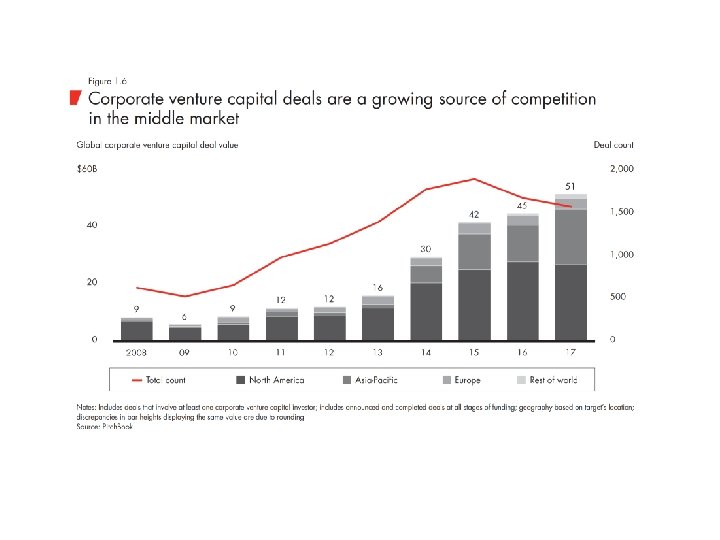

The development of PE and VC

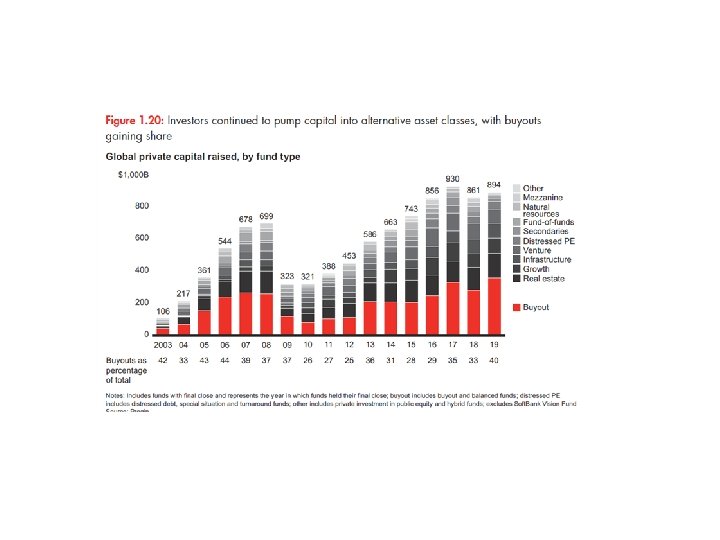

Table 2. 1: Annual Investment by VC Funds from all Countries (Money, # of Deals), Source: Venture Capital Review, 2014, Ernest & Young. Years Total investment ($billion) Number of deals 2008 51. 2 5, 500 2009 35. 4 4, 813 2010 46. 6 5, 438 2011 55. 9 6, 040 2012 49. 5 6, 085 2013 53. 5 6, 551 2014 86. 7 6, 507

Table 2. 2: Geographical Distribution of VC funds 2013, Source: EY (2014). Region Amount invested ($billion Investment rounds % of activity US 33. 1 3, 480 68. 2 Europe 7. 4 1, 395 15. 3 Canada 1. 0 176 2. 1 China 3. 5 314 7. 2 India 1. 8 222 3. 7 Israel 1. 7 166 3. 5

Table 2. 3: The dimensions of the VC industry in the US 1994 and 2014. Source: NVCA year book 2015 1994 2014 % Change Number of VC Firms (GPs) 385 803 108 Number of VC Funds 635 1, 206 90 Number of professionals 3, 735 5, 680 52 Capital under Management ($ billion) 33. 2 156. 5 371 Seed Early stage Expansion Later Stage 2% 32% 42% 25% All Investments Initial stage Industry Companies (numbers) Deals (numbers) Investment ($billion) IT 2, 611 3, 050 35. 7 1, 059 5. 2 Life Sciences 650 827 8. 8 174 1. 2 Non Hi-Tech 404 484 4. 8 177 0. 9 Total 3655 4361 49. 3 1, 410 7. 3

Table 2. 7: Sources of Capital for U. S. VC Funds 2014 , Source: Bloomberg Business. Source of Capital Share of investment in VC funds (%) Public Pension Funds 20 Endowments/Foundations 17 Corporate Pension Funds 7 Insurance Companies 7 Family Offices 14 Financial Institutions 13 Others 22

The structure of the PE and VC partnership

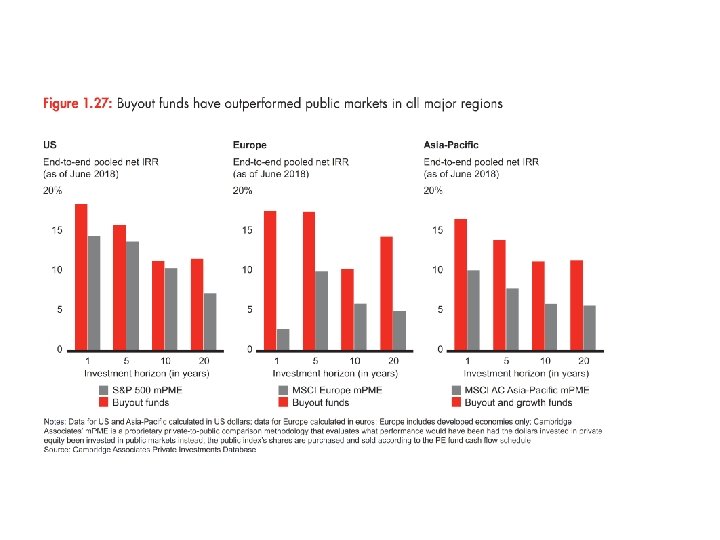

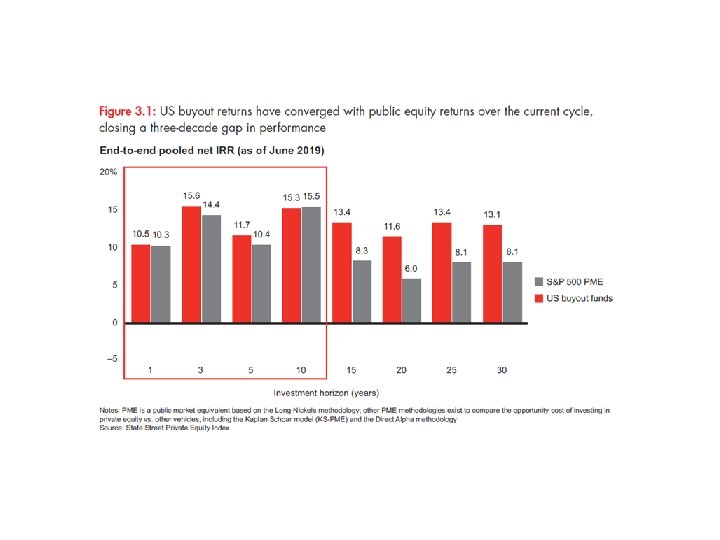

Returns

Returns

Returns

Why low returns? • Value creation is difficult / competitive advantages are rare • LP pick low performing funds • LP are performance-insensitive • Lack of data to determine risk adjusted returns • PE charge excessive rent

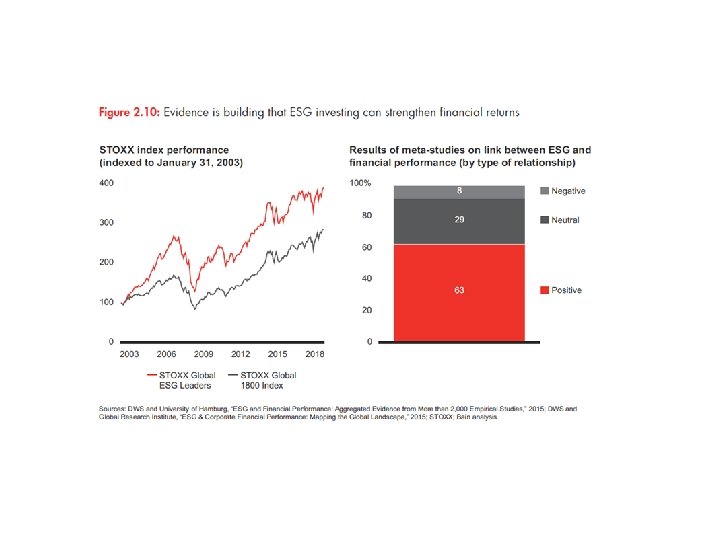

Value creation evidence PE

Value creation evidence PE

Value creation evidence PE • Accounting based data Market data do not exist Operating cash flows increase (PE firms focus on cash flows) Decreased working capital Capital spending on R&D, advertisement, maintenance no significant change – Growth in sales – Partial industrial analyses – – • Wealth transfer hypothesis – Taxes (from government), Employment, debt (from banks), Pension security (employees) • • Undervaluation of previous shareholders Reduction of agency costs ?

Value creation evidence VC

Value creation evidence VC • • Due diligence or helping start up? Skills Monitoring Active involvement Incentive systems Costs for VC envolvment (reduced ownership sharesw) Network There is evidence for VC to help ventures but…. • Why can’t incumbents do the same? ? ? – CVC

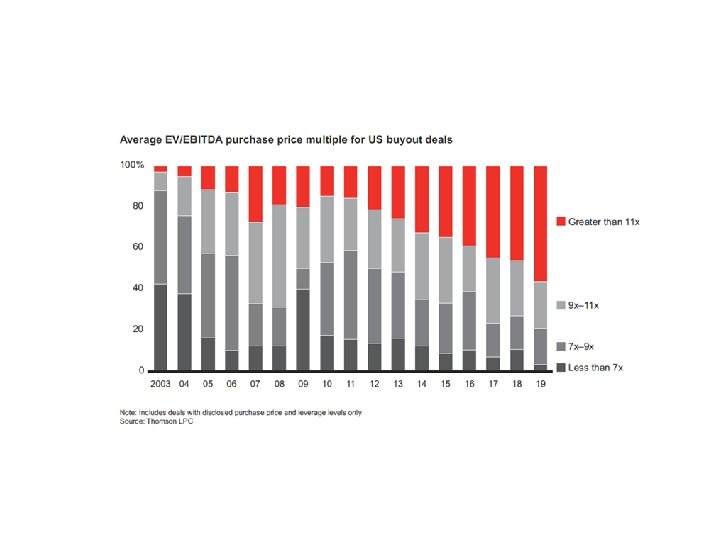

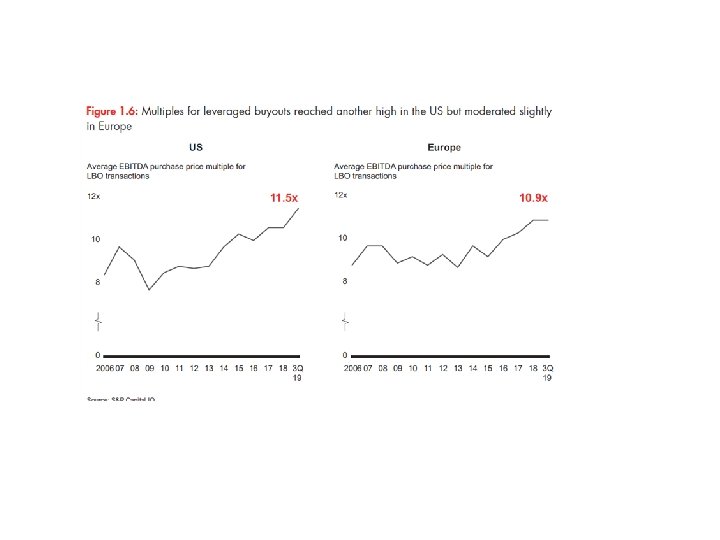

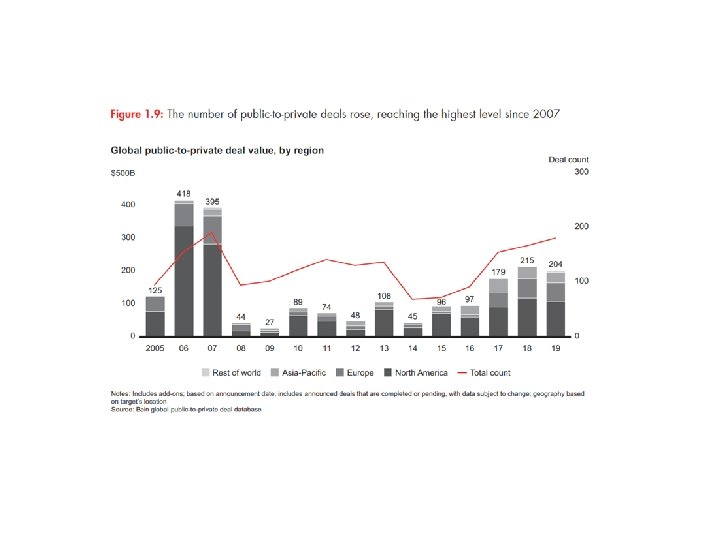

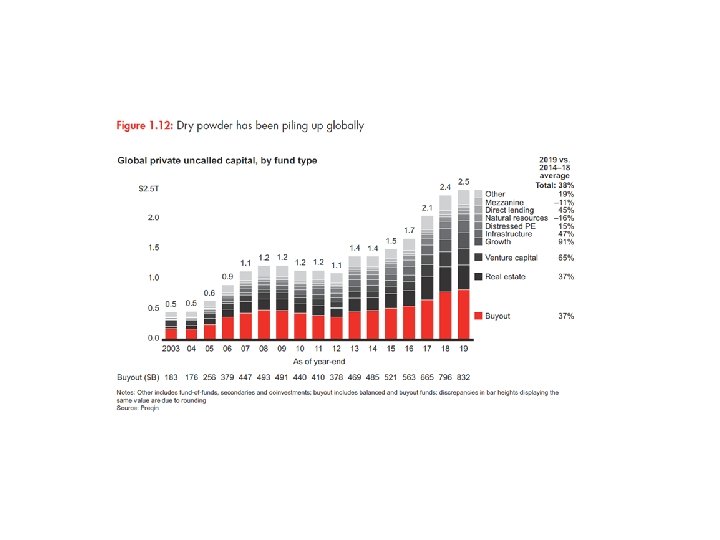

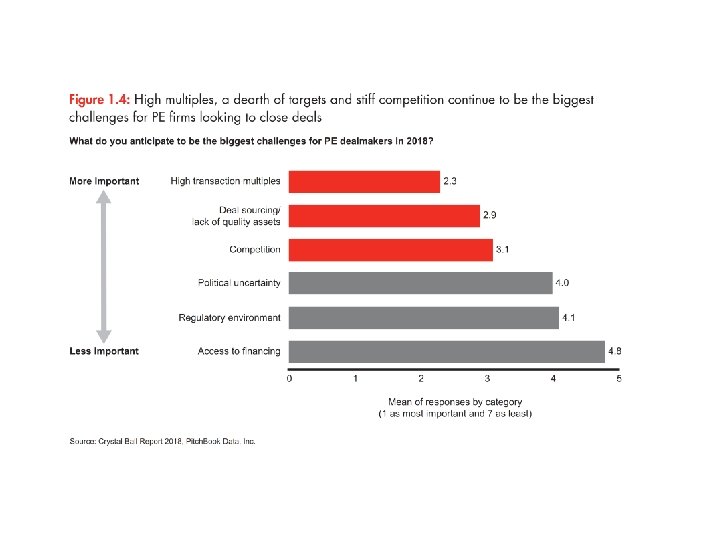

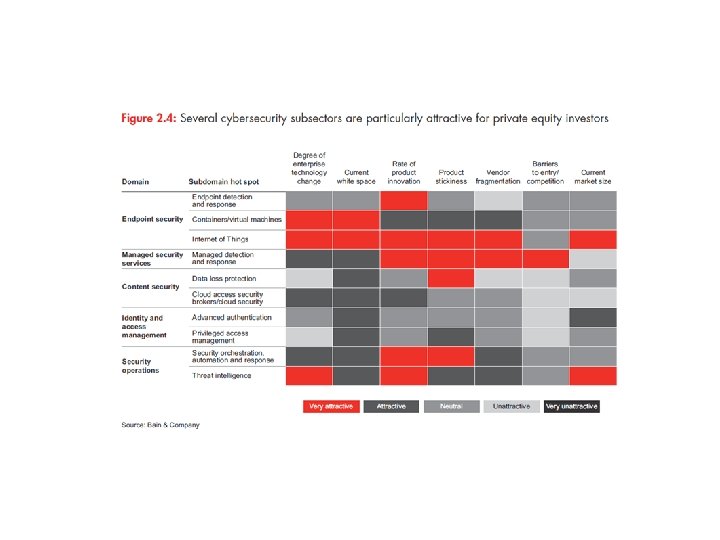

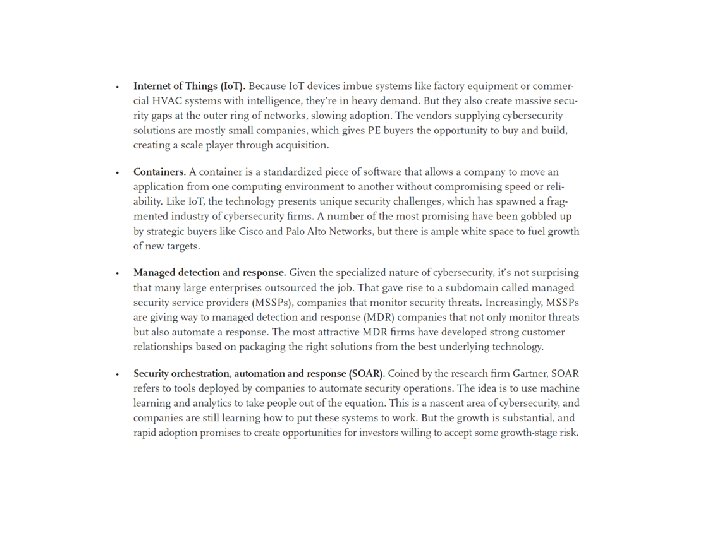

Outlook • Buy-and-Build • A size component • Focus on sectors – ”White space” • • • Platform companies Huge amount of dry powder – driving prices? Due diligence becomes more important Global PE Digitalization and AI

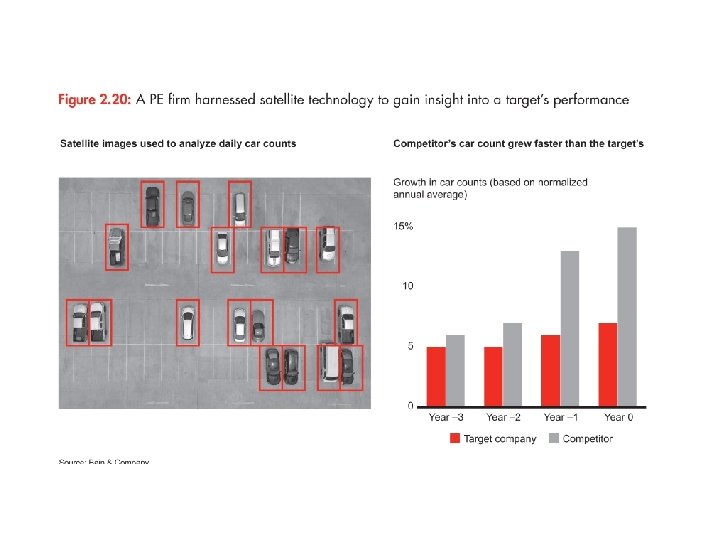

Understading traffic data – an example of digitalization and AI