Understanding VIX Hedging and Trading Strategies Option Pit

")

- Slides: 73

Understanding VIX Hedging and Trading Strategies Option Pit

Option Pit Disclosure The materials presented from Option Pit LLC are for your informational and educational purposes only. Option Pit LLC nor its employees do not offer investment, legal or tax advice of any kind, and the analysis displayed with various tools does not constitute investment, legal or tax advice and should not be interpreted as such. Using the data and analysis contained in the materials for reasons other than the informational and educational purposes intended is at the user’s own risk. Option Pit LLC is not responsible for any losses that may occur from transactions effected based upon information or analysis contained in the presented materials. Specific trading ideas or strategies discussed in the presentations or materials are entirely illustrative and do not constitute a solicitation of a transaction (or transactions) or a recommendation to execute a particular transaction or implement a particular trading strategy. To the extent that you make use of the concepts with the presentation material, you are solely responsible for the applicable trading or investment decision. Use caution when entering any option transaction and it is recommended you consult with your financial advisor for investment, legal or tax advice relating to options transactions

What You Will Learn • • • What is Volatility What is the VIX What are VIX Options and Futures What causes VIX options to move Ways to trade VIX Ways to use VIX to hedge

Volatility • Volatility is a measure of movement of an underlying instrument over a period of time regardless of direction • The higher the volatility the higher the movement and/or expected movement of the underlying • When we discuss volatility, no matter what how long to expiration, the number is an annualized number

Different Vols • There are 3 main types of volatility traders look at - Historical volatility: how much an underlying has moved in the past over a set number of days - Realized volatility: how much an underlying is actually moving - Implied volatility: how much the market is expecting an underlying to move over a set future time period

Implied Volatility • Q: What makes trading volatility different than trading a stock? • A: Over the long term we know where implied volatility of a stock or index is going to go. We do not know where the stock price is going to go – IV mean reverts

AAPL Stock Is there a Mean? No: look at the 50 and 200 DMA

VXAPL Is there a mean? Yes!!!!

Mean Reversion • A stock price can go anywhere and stay there • While volatility can GO anywhere, it cannot stay anywhere • It must revert to its mean overtime • Understanding this can help with buy and sell decisions

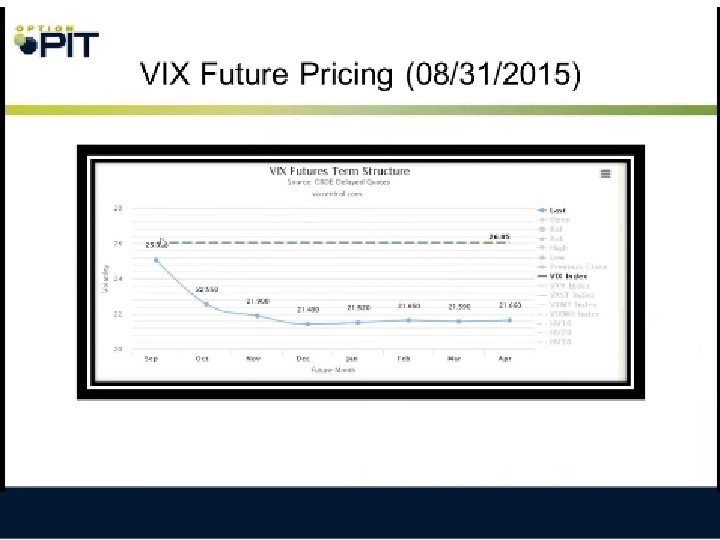

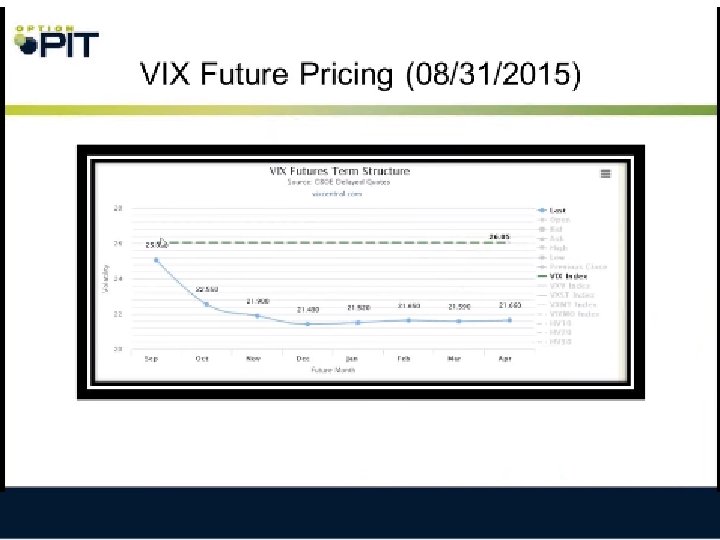

Mean Reversion • Most traders think mean reversion is an instantaneous thing… it is not • Vols can stay low for long periods of time (see 20122014 ½) • Vols can get sky high (see August 2015) and can stay there for longer than many traders realize • Its important not to have a recency bias and understand how high and low vol can get, and how long it can stay there

Vols • When IV’s are low they can stay there for a long time • Money can seem “easy” to make selling premium • Money can go away incredibly fast • The play is to be long vol, long units, short premium – See calendar spreads and modified flies

High vol • When IV is high it will fall back • Spikes can be short – Sometimes they are not (2011, 2015) • IV can stay high for months and then take months to ease back • Long VXX and short time spreads could be the right trade • Short butterflies can work: flat IV and long premium can work • Short wings (not on a ratio) typically can be extremely profitable

The VIX • The CBOE Volatility Index • The purpose of the index is to gauge the buying and selling of options in the S&P 500 – Gauges cost of insurance • The idea is that, when there is more buying over selling, generally, the market is trying to buy protection • When there is more selling than buying, the market is not out seeking protection • When VIX is up, cost of insurance is higher and vice versa

What is the VIX • Similar to the S&P 500, this index is not actually traded – Unlike S&P 500, traders cannot even trade basket to recreate the VIX • The VIX is, essentially, a estimate of implied volatility on the S&P 500 options that has a constant duration of 30 days – Constant Duration means that it attempts to constantly mimic a portfolio with 30 days to expire

What is the VIX • The weighting of the VIX puts more emphasis on At. The-Money options (those trading closest to the underlying) • The weighting of the VIX naturally puts more emphasis on the Out-of-the-Money puts than calls • The VIX Uses the 2 weekly options closest to 30 to expiration – One is equal to or less than 30 days, the other is more than 30 days

VIX Calculation

What is the VIX • The VIX is quoted as a price, but is really a percentage • Volatility, despite not being spoken as a percent, is always a percentage • SO a VIX of 30 is actually 30% annualized volatility – 30% annualized expected movement over the next 30 days

VIX In The 2 Years

VIX Over the Last Few Years

VIX and SPX

The VIX • The VIX negatively correlates with the SPX – When the SPX is up, VIX is generally down – When SPX is down, VIX is generally up • This makes sense, as generally, when the market sells off, volatility does increase – There is also the nature of similar movement against a lower number • In addition, there are some features of the VIX calc that cause it to increase on a sell off

The VIX

VIX Options and Futures • VIX options and futures are NOT options on the cash VIX that is often quoted on TV • VIX futures and options are options on the forward (Future) value of VIX • This means they are an option on a volatility SWAP not on the VIX itself • VIX futures and options will trail movement in the VIX both up and down due to tendencies of volatility to mean revert

Characteristics • VIX futures and options are European exercise • This means they cannot be exercised early • They have a unique settlement procedure as the VIX futures • Based on VIXMO not the VIX itself right now • At 30 day to expiration typically move at a beta of about. 5 to VIX • As time passes beta increases

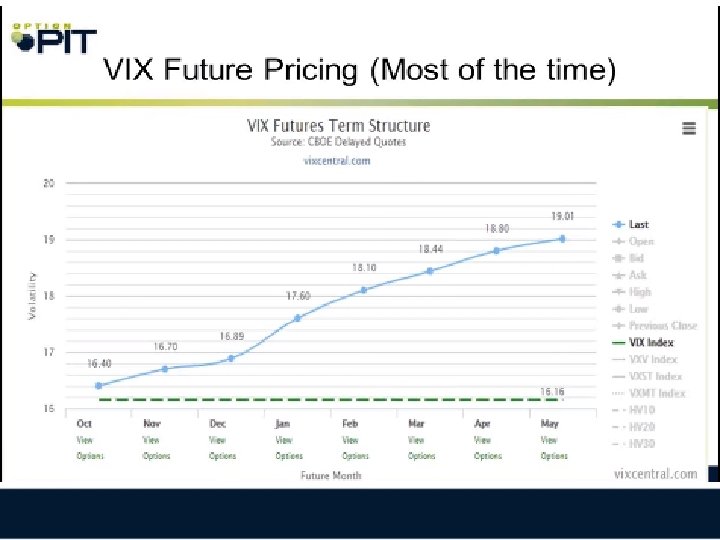

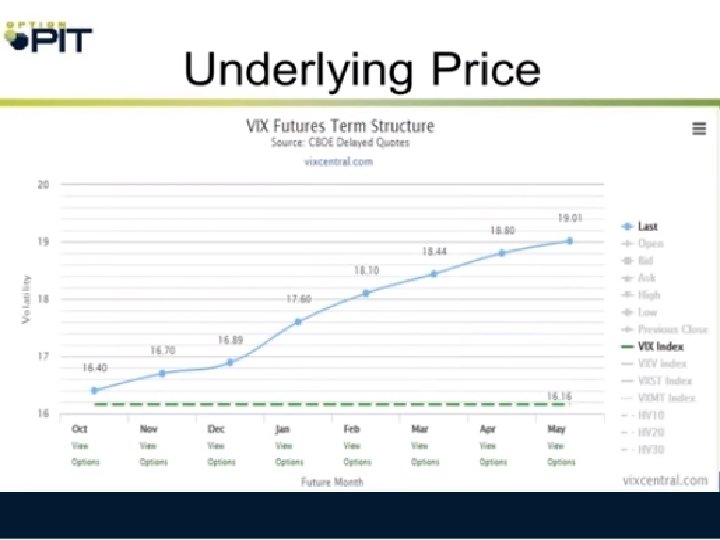

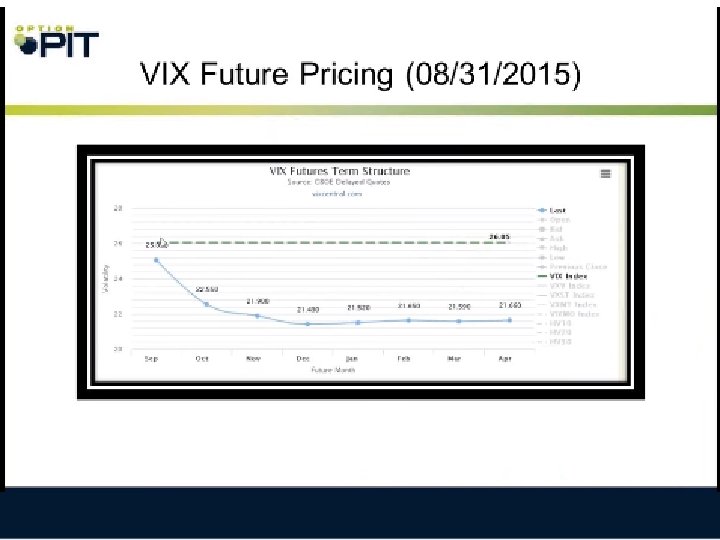

VIX FUTURES (Contango)

VIX FUTURES • The most successful product introduced in the last 20 years • Trade out 8 months • Each month trades independently, NOT like the structure of SPX (which is based solely on carry cost) • Listed weekly futures July 2015 • In contango north 80% of the time (near term contracts are less expensive than long term) • Typically used as hedges against a long portfolio

VIX Options • The most successful option product introduced in the last 20 years • Trade out 8 months • Each month trades independently, NOT like the structure of SPX (which is based solely on carry cost) • Underlying is the future. NOT CASH • Typically used as hedges against a long portfolio

Volume of Options • VIX options are extremely liquid and trade very actively • Trade is over hybrid and Open Outcry trading • Markets are generally Relatively tight in the Near term typically. 05 -. 10 wide (does not trade in pennies)

VIX Activity

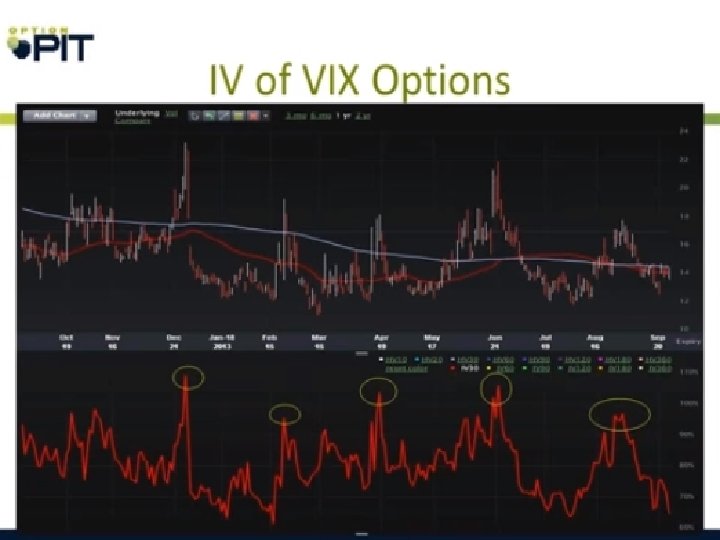

Volatility • The VIX of VIX Options is the VVIX Index • It can often seem very low relative to VIX, again this is because the option volatility is more based on the movement in the VIX futures instead of the VIX options • Futures realized volatility is almost always significantly lower than the cash VIX

VVIX • VVIX will trade as low as the 60 s in slow periods and can threaten 200 when the VIX is high and the market is in panic • In the past when SPX tanks, VVIX can make extremely large highs. Like VIX it may tail off before VIX hits highs.

Volatility • Unlike the VIX relative to SPX, the VIX and VVIX are typically positively correlated • When the VIX is rallying, the VVIX is typically going higher • Especially when the VIX is moving from below its mean back towards its mean • When the VIX is popping and VVIX is not, that can be a sign that smart paper is selling insurance rather than buying it

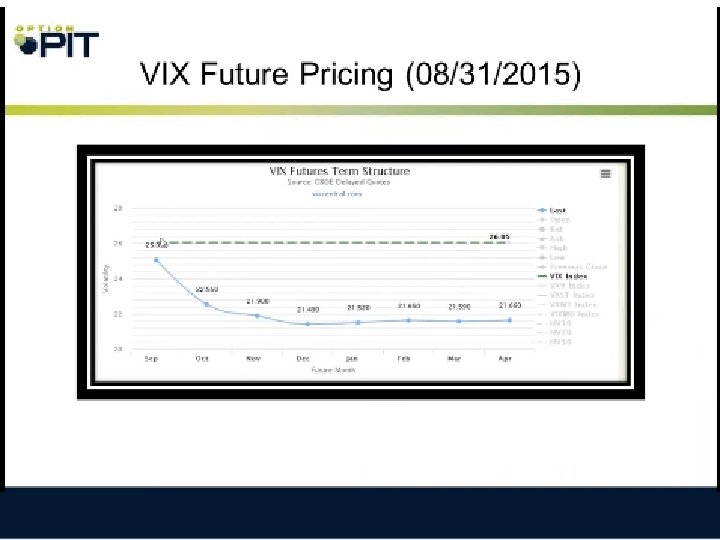

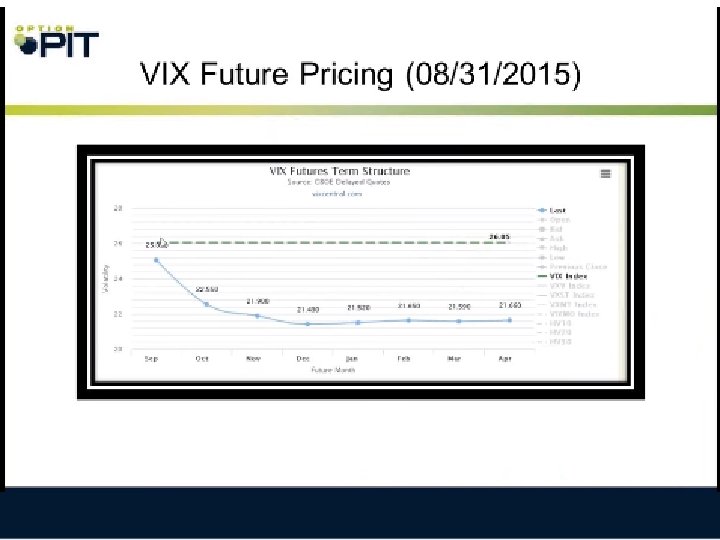

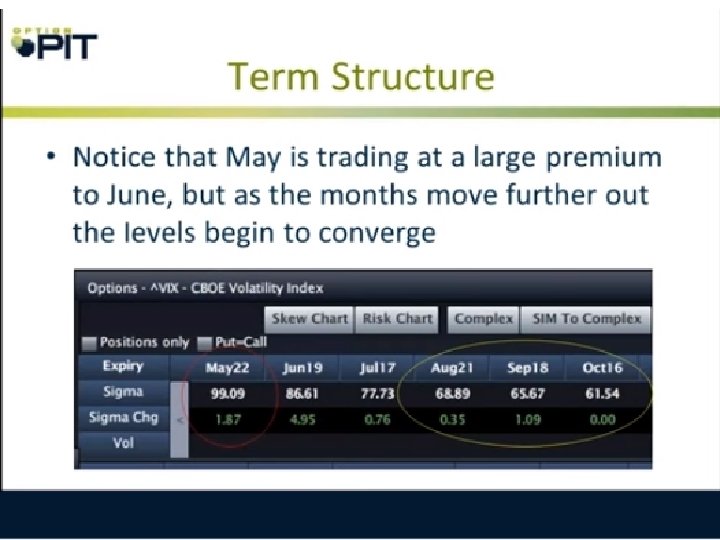

Term Structure • Unlike many equity products, typically near month implied volatility is higher than months further out • This is partially because each month has its ‘own’ underlying and the cash is not the true underlying for the whole set of options • There is a delta in the future movement due to the premium “cushion”

Term Structure • Each option trades vs the future that expires in the same month (big risk in time spreads) • Because each option has its own underlying, many firms do not offer a margining discount on calendars and time spreads • Because VIX options have different underlyings it is entirely possible for a long calendar to trade for a credit -this is unheard of in normal equity options

Term Structure • Each option trades vs the future that expires in the same month (big risk in time spreads) • Because each option has its own underlying, many firms do not offer a margining discount on calendars and time spreads • Because VIX options have different underlyings it is entirely possible for a long calendar to trade for a credit -this is unheard of in normal equity options

Intra Month IV Structure • Normally indexes have what is called backward skew, sometimes called an investment skew • This skew is caused primarily by hedging activities and collaring • The skew is bid to where the “crash” will be

Using Options • Recall that VIX options ATM strike is NOT the cash VIX level but the Futures on a specific date the future ATM was: • ATM for Sep is 25. 20 • ATM for Oct is 22. 70 • ATM for Nov is 22. 05

Trading with Long Contango • Recall that VIX futures are normally in contango • That creates an almost second ‘negative’ theta as the future converges to cash • However, the VIX has a favorable forward skew that trader can take advantage

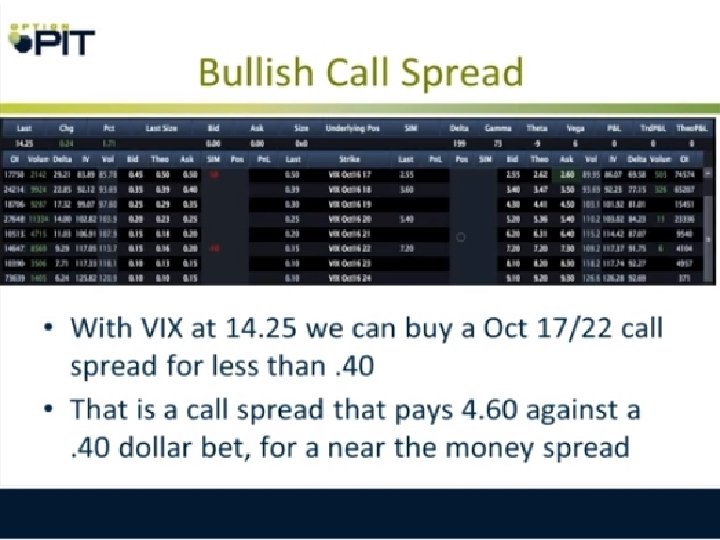

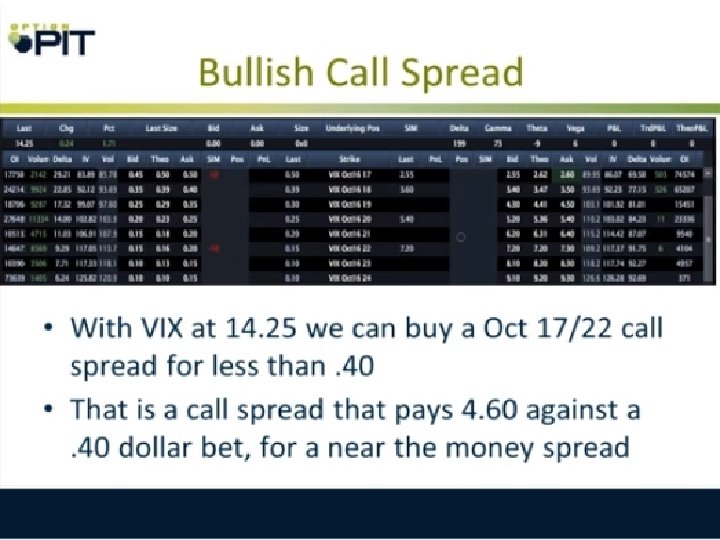

Trading Long • When using options to trade a higher VIX, typically the most favorable call is one that is slightly ITM or ATM • An even more favorable trade is a call debit spread • Buying a call that is ATM and selling an OTM call can allow for bullish verticals with favorable risk reward

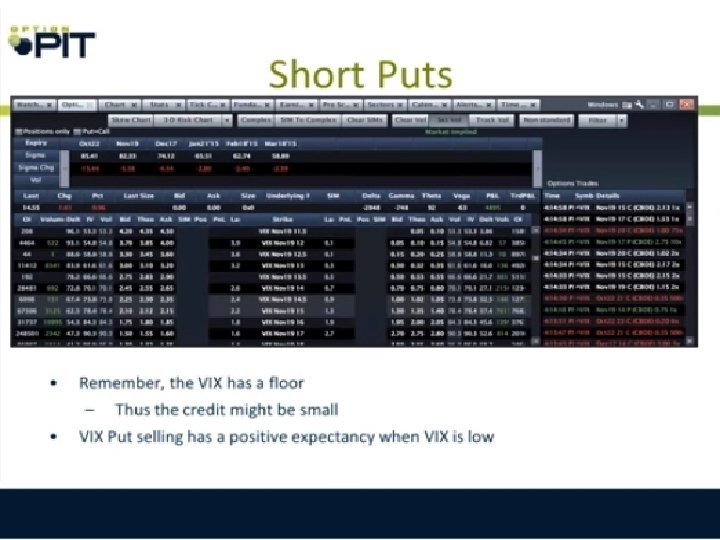

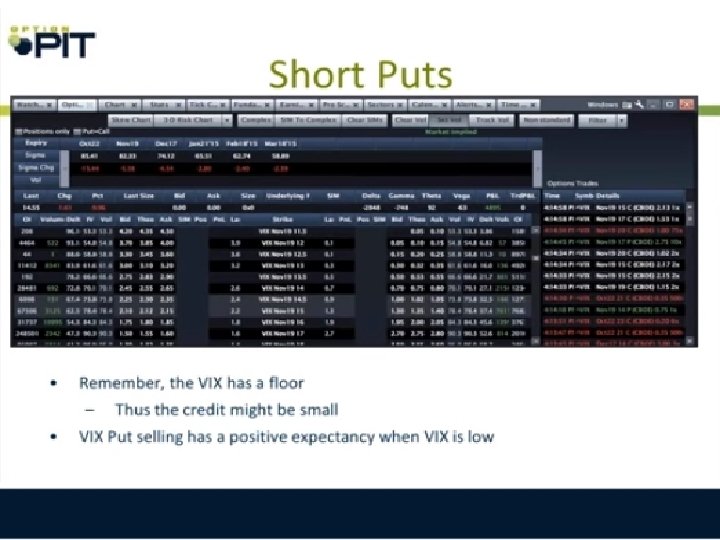

Trading Short with Contango • While a trader usually has contango in his or her face when trading from the long side, one typically has ‘the wind at their back’ when trading from the short side • This makes outright puts a favorable trade • The further OTM the put is the lower the IV • Owning a long put will have favorable characteristics in a falling and stable environment

Trading Short with Contango • While a trader usually has contango in his or her face when trading from the long side, one typically has ‘the wind at their back’ when trading from the short side • This makes outright puts a favorable trade • The further OTM the put is the lower the IV • Owning a long put will have favorable characteristics in a falling and stable environment

Hedging • The VIX is actually a hedging vehicle • The calculation is directly related to how variance swaps trade in a OTC market • A variance swap is an OTC trade where each side bets on how much the market might move over a specified period of time -Based on actual Realized Vol • While there are many circumstances that SPX or SPY are better at hedging a long equity position there are time where VIX does a better job

VIX as a hedge • If one was using a nearer term hedge, the VIX could potentially work better -depending on the timing • Basically, VIX has a sticky strike, if one is hedging FAR out in a bull market, it is going to work better since the put strikes get so far away • If the market stays around where it is, more a wash (although probably a winner) • It loses if the S&P take a quick drop

VIX vs SPX • What is the major issue of using VIX as a hedge? -Backwardation • If I buy a VIX 18 dollar call expiring in Oct, it is highly unlikely that the VIX will be able to move far enough out of the money that the strike no longer hedges -How does it compare with a sharp move in the SPX?

Why Use VIX • What is the major issue of using SPX as a hedge? -Sticky strike issues • If I buy a VIX 18 dollar call expiring in May, it is highly unlikely that the VIX will be able to move far enough out of the money that the strike no longer hedges -When the SPX moves from 1950 to 2125 the hedge stops working

The VIX versus SPX Hedge • • On July 14 th 2015 VIX was hitting year lows The Oct future was around 16. 82 SPX was around 2104 How did they move on the Aug 15 th vol explosion • The VIX Oct 16 call from$2. 50 to $8. 50 with the future is around $6 - 16. 82 to 22. 69 • What did the Jan 2016 1950 -1950 was 43. 20

VIX vs SPX • What is the major issue of using VIX as a hedge? -Backwardation • If I buy a VIX 18 dollar call expiring in Oct, it is highly unlikely that the VIX will be able to move far enough out of the money that the strike no longer hedges -How does it compare with a sharp move in the SPX?

Why Use VIX • What is the major issue of using SPX as a hedge? -Sticky strike issues • If I buy a VIX 18 dollar call expiring in May, it is highly unlikely that the VIX will be able to move far enough out of the money that the strike no longer hedges -When the SPX moves from 1950 to 2125 the hedge stops working

The VIX versus SPX Hedge • • On July 14 th 2015 VIX was hitting year lows The Oct future was around 16. 82 SPX was around 2104 How did they move on the Aug 15 th vol explosion • The VIX Oct 16 call from$2. 50 to $8. 50 with the future is around $6 - 16. 82 to 22. 69 • What did the Jan 2016 1950 -1950 was 43. 20

Smart Hedge • Recall how I explained to trade VIX long from a speculative side • Why in the world would I treat a hedge trade any differently • The only major difference, I might leg the call spread on a hedge trade -buy long when VIX sub 13 -sit and wait -when the underlying rallies a point, sell the spread -DO NOT GET GREEDY, a point should make the hedge close to free

Summary • • VIX options have unique characteristics Each has their own underlying IV and VIX are correlated Bear and bull spreads have different structures • Play the strikes