Chapter 06 Inventory and Cost of Goods Sold

– unlimited attempts")

Purchased 2. )")

l When we purchase")

Inventory –items a company intends to sell to customers ¡")

")

Balance Sheet (partial) Current assets: Cash $450, 000 Accounts receivable")

¡ 28 Represents the flow of COSTS not ITEMS l First")

¡ 29 Represents the flow of COSTS not ITEMS l Last")

Formula - #1 Formula - #2")

")

")

")

")

Calculate Ending Inventory and Cost of Goods Sold - FIFO")

- Slides: 73

Chapter 06 Inventory and Cost of Goods Sold Mc. Graw-Hill/Irwin © The Mc. Graw-Hill Companies, Inc.

Participation Questions – Chapter 6 ¡ How much ‘inventory’ did Apple sell in 2014? ¡ At what amount is inventory recorded in the balance sheet? l Reduced selling price of inventory, Cost of inventory, or Market selling price of inventory What company was featured in the video we watched showing the receipt and shipment of inventory products? ¡ l ¡ ¡ Apple, Amazon, Fed Ex, or Sears How many inventory costing methods were introduced in this chapter (we only focus on 2, but more were introduced)? l 3, 4, 5, or 6 What inventory costing method does Apple use? l Specific Unit, Weighted Average, FIFO, or LIFO

Announcements ¡ Assignments – Due 2/28/16 l Chapter 5 Homework (Connect) – unlimited attempts l Participation questions for Chapter 5 (Webcourses) – 1 attempt

Questions to be Answered Overall - How has society shaped today’s financial reporting? Chapters 4 – 10 – dive deeper into each area of accounts to understand the associated accounting rules and the impact to the income statement and balance sheet. Chapter 6 – Overall focus on this chapter is 1. ) How we record inventory purchase costs on the balance sheet, 2. ) How do we record sales of inventory, 3. ) How do we calculate the costs of the inventory sold, and 4. ) What is the balance ($ value) in ending inventory after we make a sale.

Part A Understanding Inventory and Cost of Goods Sold 6 -6

Introduction to Inventory – Purchase & Sale Unit Cost = $100 & Unit Sales Price = $150 Purchased 100 units on 1/1/14 and sold 50 units on 1/15/14

Number One Concern!! Accounting for the COST* of Inventory 1. ) Purchased 2. ) Sold * NOT concerned with flow of actual inventory items – only their costs 8

Apple

Warehouse Video - Amazon https: //www. youtube. com/watch? v=i 6 H 7 nf. Hj. Ht. Y ¡ (0: 15 – 2: 50) ¡ Receiving – where is the cost of inventory recorded? ¡ Stock/picker – are they concerned with how much each items costs or how old it is? ¡ Packing/shipping – recognizes the revenue from the sale where? Recognizes the cost of the inventory sold where?

Inventory Purchases- Discounts, Allowances, Returns ¡ Cost of Inventory (COGS) l When we purchase inventory, we are offered discounts, allowances, and returns from the vendor. These are recorded into the INVENTORY account (NO CONTRA ACCOUNTS). l Example - $10, 000 inventory purchase on account and $500 returned two weeks later.

Costs Associated with Purchases ¡ The cost of any asset, such as inventory, is the sum of all the costs incurred to bring the asset to its intended use, less any purchase discounts, allowances, returns, &. l l l 12 Shipping cost Insurance during transit Duties or customs paid (taxes paid to import)

Calculating the “Cost” of Net Purchases + + = Purchase price of inventory items Freight-in, taxes, insurance, etc. Purchase returns Purchase allowances Purchase discounts Net inventory purchases (debit account balance) 13

INVENTORY - Purchase discounts, allowances, and returns – not contra accounts (Each example is independent) Purchase Discounts – reduction in the amount paid for inventory based on payment terms offered by the seller. For example $10, 000 bought with 2/15, n/30 terms. Steps – 1. ) record original inventory purchase transaction – debit inventory and credit A/P. 2. ) Pay for inv. - debit A/P for full value, credit cash paid, and credit inventory for discount. Purchase Allowances – reduction or partial refund of the purchase price of inventory after the purchase has already been recorded. For example, $10, 000 purchased on account, we are offered a $500 allowance. Steps – 1. ) record original inventory purchase transaction – debit inventory and credit A/P. 2. ) Allowance - debit A/P for amount of allowance, credit inventory for amount of allowance. Purchase Returns – return of a product after the purchase of inventory has been recorded. $10, 000 purchased on account and we return $500 of inventory. Steps – 1. ) record original inventory purchase transaction – debit inventory and credit A/P. 2. ) Return - debit A/P for amount of return, credit inventory for amount of return.

Example #2: Inventory Transactions – Freight Charges Oct 19 - Mario purchases 600 units of inventory at $11 per unit on account. Mario pays $300 cash for freight charges associated with the purchase of inventory. 6 -15

Additional Inventory Transactions – Purchase Returns. Mario decides on October 22 to return 50 defective units from the 600 units purchased on October 19 for $11 each. Units were bought on account. 6 -16

Additional Inventory Transactions – Purchase Discounts. Mario on Oct 29, pays for the units purchased on Oct. 19, less a 2% purchase discount. Remaining units were bought on account for $6, 050. 6 -17

Inventory – Purchases (COST) Inventory –items a company intends to sell to customers ¡ Recorded at COST on the balance sheet Check-in #1: What amounts are recorded directly in the inventory account that shows up on the balance sheet: A. ) Purchases B. ) Freight C. ) Purchase Discounts D. ) ALL OF THE ABOVE 18

Apple Balance Sheet (Partial)

Sale of Inventory – Revenue and Cost of Goods Sold Inventory is sold from the inventory account shown on the balance sheet. Two Step Process 1. 2. Recognize Revenue of units sold 1. Debit cash or A/R 2. Credit Revenue Recognize the cost of inventory sold. Amount is transferred from inventory (balance sheet) to cost of goods sold (income statement). The cost of inventory that’s 1. Debit COGS been sold = 20 2. Credit Inventory Cost of Goods Sold

Apple Income Statement 21

22

Merchandise Inventory (for Resale) Balance Sheet (partial) Current assets: Cash $450, 000 Accounts receivable 10, 000 Inventory (900 @ cost of $50) $45, 000 Income Statement (partial) Sales (100 @ $100 selling price) Cost of goods sold (100 @ $50 cost) Gross profit $10, 000 5, 000 $5, 000 Check in #2: If we sell 1 unit of inventory for purchased at $10 a unit for $20 in cash, which part of the required 2 journal entries are correct? A. ) The 2 journal entries will include a debt to revenue and a credit inventory B. ) The 2 journal entries will include a debt to COGS and a credit to cash C. ) The 2 journal entries will include a debt to COGS and a credit to revenue D. ) The 2 journal entries will include a debt to cash and a credit to COGS 23

Four Inventory Costing Methods Specific unit Weighted Average cost First-in, first-out Last-in, first-out (Used by approximately 8. 7 percent of 5, 000 publicly traded companies) Each Method will result in a different • Cost of Good Sold • Ending inventory 24

Main Goal with all of the inventory valuation methods Chapter 6 – Overall focus on this chapter is 1. ) How we record inventory purchase costs on the balance sheet, 2. ) How do we record sales of inventory, 3. ) How do we calculate the costs of the inventory sold, and 4. ) What is the balance in ending inventory after we make a sale. 25 Information needed from each of the 4 inventory valuation methods: ¡ COGS for units sold. ¡ Ending inventory after sale of inventory.

Specific Unit ¡ Used for businesses with unique inventory items l ¡ ¡ 26 Automobiles, fine jewelry, real estate Inventory costed at specific price of the particular unit Too expensive for inventories with common characteristics

Weighted Average Assumes that both cost of goods sold and ending inventory consist of a random mixture of all of the goods available for sale. 27

First-in, First-out (FIFO) ¡ 28 Represents the flow of COSTS not ITEMS l First goods purchased are sold first (costs only) l Focus on Balance Sheet (most recent costs) Balance Sheet Income Statement Ending Inventory COGS Most recent (last) costs Oldest (first) costs

Last-in, First-out (LIFO) ¡ 29 Represents the flow of COSTS not ITEMS l Last goods purchased are sold first (cost only) l Focus on Income Statement (most recent costs) l Tax benefit designed to protect cash flow in industries where prices increase rapidly. Balance Sheet Income Statement Ending Inventory COGS Oldest (first) costs Most recent (last) costs

Apple Computer Annual Report 30

Target Inventory and cost of sales We use the retail inventory method to account for substantially all inventory and the related cost of sales. Under this method, inventory is stated at cost using the last-in, first-out (LIFO) method as determined by applying a cost -to-retail ratio to each merchandise grouping's ending retail value. Cost includes the purchase price as adjusted for vendor income. Since inventory value is adjusted regularly to reflect market conditions, our inventory methodology reflects the lower of cost or market. We reduce inventory for estimated losses related to shrink and markdowns. Our shrink estimate is based on historical losses verified by ongoing physical inventory counts. Historically, our actual physical inventory count results have shown our estimates to be reliable. Markdowns designated for clearance activity are recorded when the salability of the merchandise has diminished. Inventory is at risk of obsolescence if economic conditions change. Relevant economic conditions include changing consumer demand, customer preferences, changing consumer credit markets or increasing competition. We believe these risks are largely mitigated because our inventory typically turns in less than three months. Inventory was $7, 918 million and $7, 596 million at January 28, 2012 and January 29, 2011, respectively, and is further described in Note 11 of the Notes to Consolidated Financial Statements.

Nike ¡ Inventory Valuation - Inventories are stated at lower of cost or market and valued on an average cost basis.

LO 4 Explain the financial statement effects and tax effects of inventory cost flow assumptions Effects of Managers’ Choice of Inventory Reporting Methods Why Choose FIFO? o o o Matches physical flow for most companies. Results in higher assets and net income when inventory costs are rising. Has a balance sheet focus. Why Choose LIFO? o o Results in tax savings when inventory costs are rising. Has an income statement focus. 6 -33

FYI - Consistency Principle ¡ ¡ ¡ Use the same accounting methods from year-to-year Allows investors to compare financial statements from one period to the next Companies are permitted to change methods l 34 Disclose effect on net income & why change made

Part B Recording Inventory Sales Transactions 6 -36

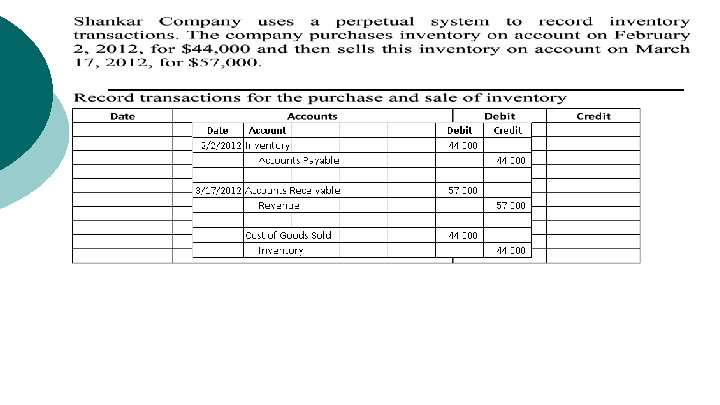

Perpetual inventory system and Periodic inventory system Perpetual Inventory System It maintains a continual—that is, perpetual—tracking of inventory. A continual tracking helps a company to better manage its inventory levels. Periodic Inventory System It does not continually modify inventory amounts, but instead periodically adjusts for purchases and sales of inventory at the end of the reporting period based on a physical count of inventory on hand. 6 -37

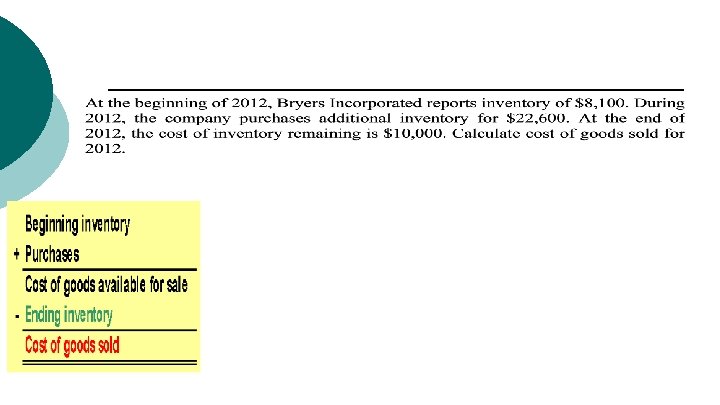

Cost of Goods Sold Formula (simple linear equation) Formula - #1 Formula - #2

Vapoorize video https: //www. youtube. com/watch? v=cpads 8 s 5 mik

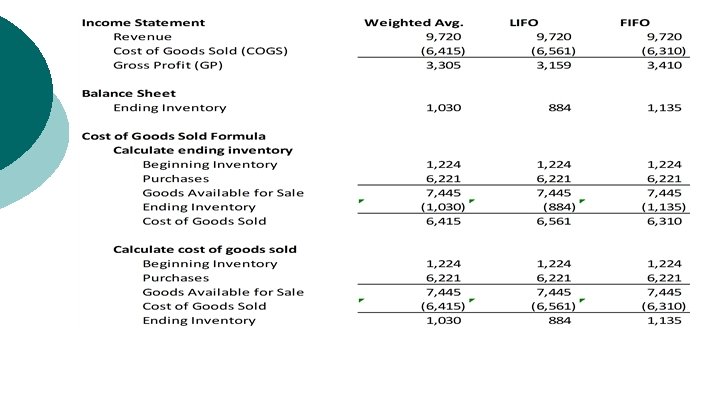

Exercise – On October 26 th, Sell 324 Units for $30 each Beginning Inventory and Purchases Date Beg. inventory Cost per unit Total cost 72 tents $17 $1, 224 103 tents $19 $1, 957 Oct. 19 158 tents $21 $3, 318 Oct. 25 43 tents $22 $946 Oct. 4 40 Units Calculate the cost of goods sold and ending inventory.

Weighted Average Cost: Average cost of inventory units Step 1 – calculate average cost of units in inventory account. Cost of goods available * Average cost per unit Number of units available* *Goods available = Beginning inventory + Purchases Step 2 – calculate COGS for units sold. Cost of goods sold Number of units sold Average cost per unit Step 3 – calculate ending inventory after sale of inventory. Ending inventory Number of units on hand (Ending Inventory) Average cost per unit 41

Calculate COGS and Ending Inventory using Weighted Average

FIFO and LIFO Instructions • Step 1 - Compile a list of inventory purchases made over time, noting the time that the purchase was made, the amount that was purchased and the price. • Step 2 - Calculate FIFO inventory costs by assuming that every item sold came out of the firstpurchased inventory. • By this method, of the 1, 200 units sold, 800 came from the stock purchased at $3 each, and 400 came from the stock purchased at $2. 50 each, for a total cost of (800 x $3. 00) + (400 x $2. 50), for a total of $3, 400. • Ending inventory = 100 x 2. 50 or $250 • Step 3 - Calculate LIFO costs by assuming the reverse, that the most recently purchased inventory is the first to sell. • These 1, 200 units sold are 500 from the August purchase for $2. 50, and 700 from the July purchase at $3. 00. Their total price is (500 x $2. 50) + (700 x $3. 00) for a total of $3, 350. • Ending inventory = 100 x 3. 00 or $300

FIFO

FIFO Cost of goods sold Ending inventory 72 tents $17 $1, 224 43 tents $22 $946 103 tents $19 $1, 957 9 tents $21 $189 149 tents $21 $3, 129 52 tents 324 tents $6, 310 Oldest costs flow through income 45 Newest costs in inventory $1, 135

LIFO

LIFO Cost of goods sold Ending inventory 20 tents $17 $340 103 tents $19 $1, 957 158 tents $21 $3, 318 43 tents $22 $946 324 tents $6, 561 Newest costs flow through income 47 52 tents $17 Oldest costs in inventory $884

Impact of Inventory Methods on Financial Statements Increasing inventory prices Cost of goods sold Ending inventory FIFO Lowest because based on older costs, which are less expensive LIFO Highest because based on Lowest because based on more recent costs, which are older costs, which are less more expensive Copyright © 2010 Pearson Education Inc. Publishing as 49 Highest because based on more recent and expensive costs

Impact of Inventory Methods on Financial Statements Decreasing inventory prices Cost of goods sold Ending inventory FIFO Highest because based on older costs, which are more expensive Lowest because based on more recent, less expensive costs LIFO Lowest because based on more recent costs which are less expensive Highest because based on older, more expensive costs Copyright © 2010 Pearson Education Inc. Publishing as 50

LO 6 Prepare a multiple-step income statement o o o For merchandising companies, sales and purchases of inventory are most important set of transactions , companies report revenues and expenses from these separately from other revenues and expenses. It makes easier for investors and other financial statement users to determine the profitability of a company’s inventory transactions. Use the information for Mario's Game Shop to calculate gross profit on the sale and purchase of inventory. 6 -51

GROSS PROFIT FORMULA 52

¡ Apple Computers

All transactions are on account. Sales Price is $2, 000 per unit. Complete using LIFO.

Example LIFO

Example LIFO (Cont. )

Example LIFO (Cont. )

Example LIFO (Cont. )

Example LIFO (Cont. )

Complete using FIFO

Complete using FIFO

Complete using FIFO

LO 10 Determine the financial statement effects of inventory errors o o Inventory Errors can unknowingly occur in inventory amounts if there are mistakes in a physical count of inventory or in the pricing of inventory quantities. The formula for cost of goods sold, follows 6 -63

Determine the financial statement effects of inventory errors Summary of Effects of Inventory Error in the Current Year. Relationship between Cost of Goods Sold in the Current Year and the Following Year 6 -64

Inventory Amounts – Year 1 End Inv. overstated at $500 versus $400 6 -65

Participation Questions – Chapter 6 ¡ How much ‘inventory’ did Apple sell in 2014? ¡ At what amount is inventory recorded in the balance sheet? l Reduced selling price of inventory, Cost of inventory, or Market selling price of inventory What company was featured in the video we watched showing the receipt and shipment of inventory products? ¡ l ¡ ¡ Apple, Amazon, Fed Ex, or Sears How many inventory costing methods were introduced in this chapter (we only focus on 2, but more were introduced)? l 3, 4, 5, or 6 What inventory costing method does Apple use? l Specific Unit, Weighted Average, FIFO, or LIFO

Apple

1. ) Calculate Ending Inventory and Cost of Goods Sold - FIFO

Questions to be Answered Overall - What is financial reporting’s role in today’s American society? Chapters 4 – 10 – dive deeper into each area of accounts to understand the associated accounting rules and the impact to the income statement and balance sheet. Chapter 6 – Overall focus on this chapter is 1. ) How we record inventory purchase costs on the balance sheet, 2. ) How do we record sales of inventory, 3. ) How do we calculate the costs of the inventory sold, and 4. ) What is the balance in ending inventory after we make a sale.