Inventory Costing and Capacity Analysis Chapter 9 Learning

- Slides: 31

Inventory Costing and Capacity Analysis 存貨成本與產能分析 Chapter 9

Learning Objective 1 Identify what distinguishes variable costing from absorption costing 定義及區別變動成本法 與歸納成本法

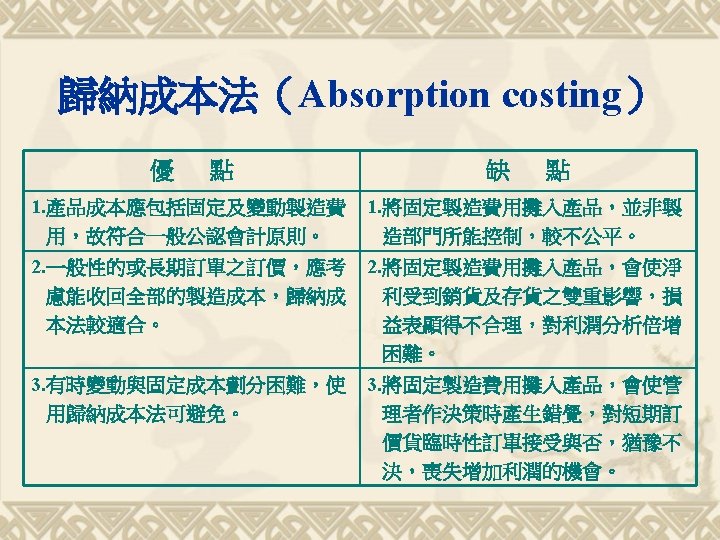

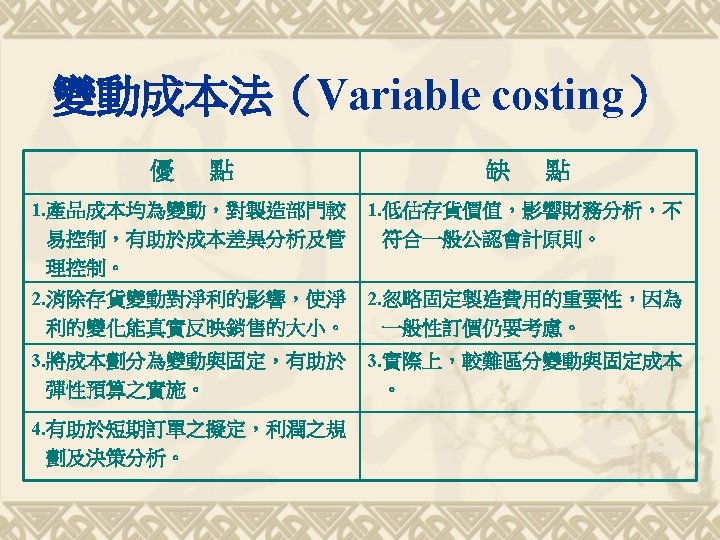

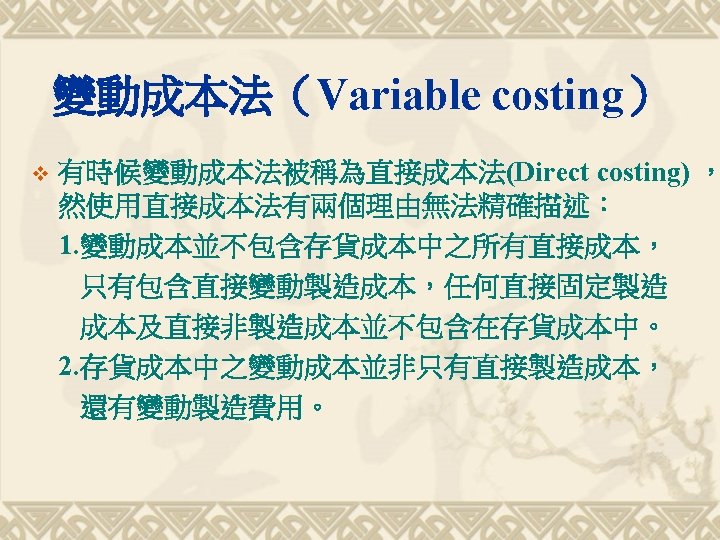

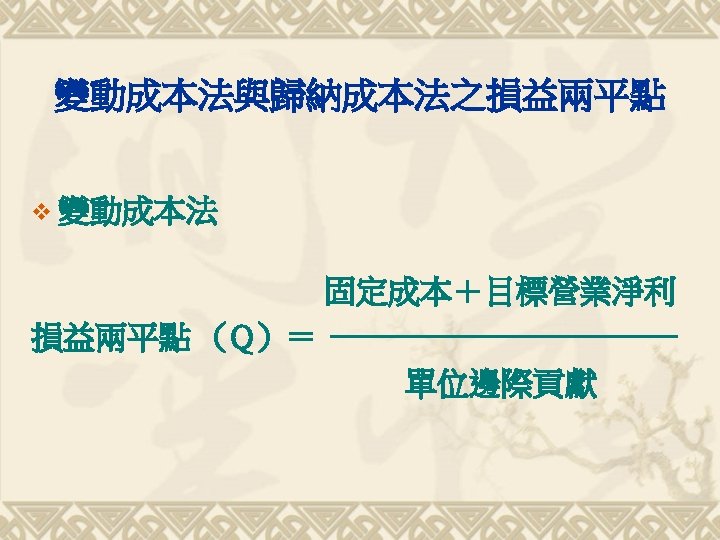

Inventory-Costing Methods The difference between variable costing and Absorption costing is based on the treatment of fixed manufacturing overhead. 變動成本法與歸納成本法之差異基於 對固定製造費用之處理

Learning Objective 2 Prepare income statements under absorption Costing and variable costing 使用歸納成本法與變動成本法 編製損益表

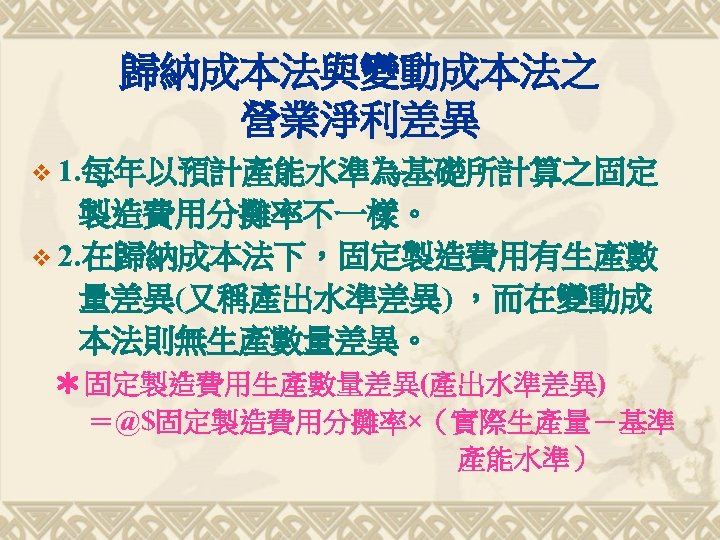

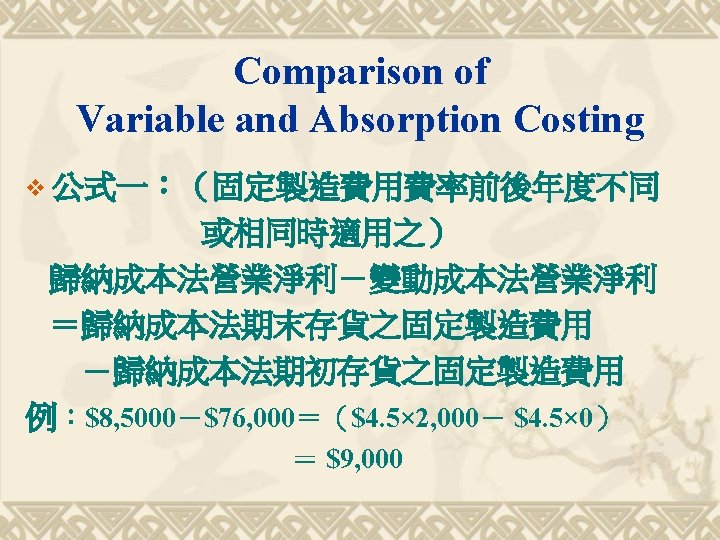

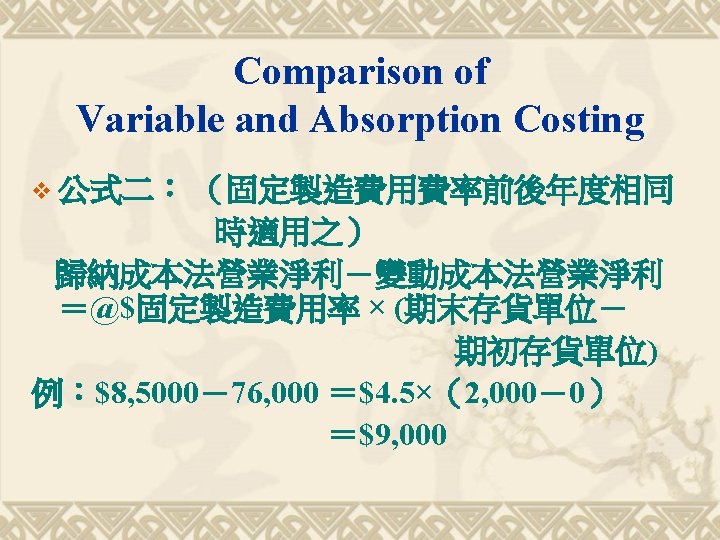

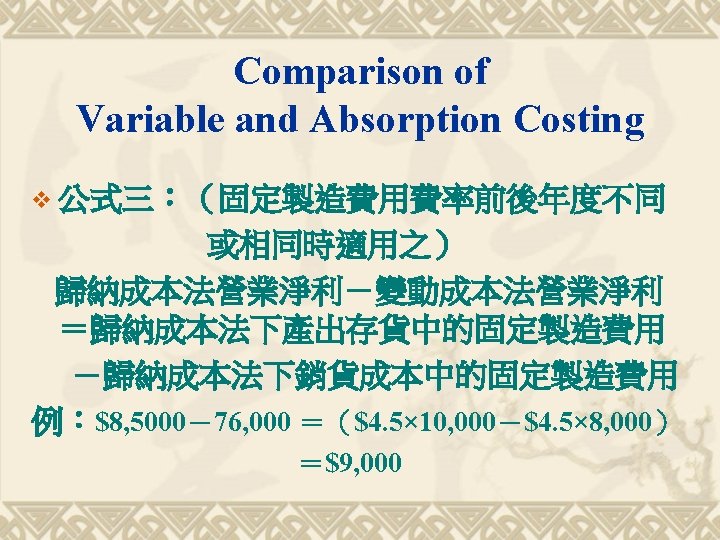

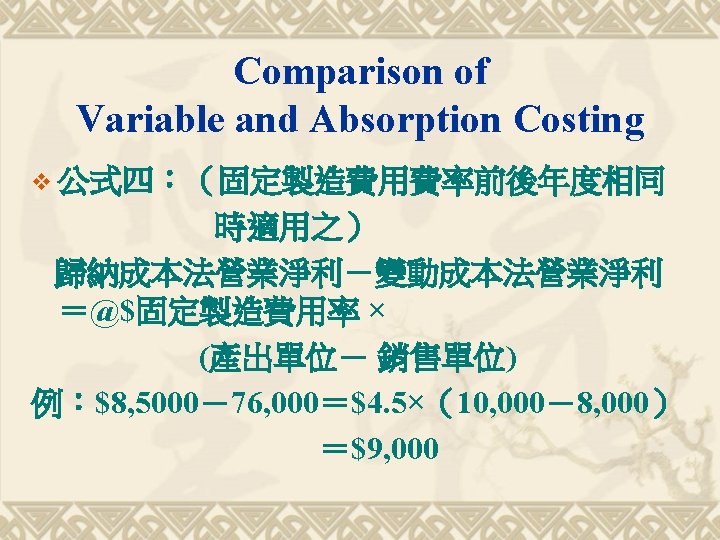

Learning Objective 3 Explain differences in operating income under absorption costing and variable costing 解釋歸納成本法與變動成本法下 營業淨利之差異

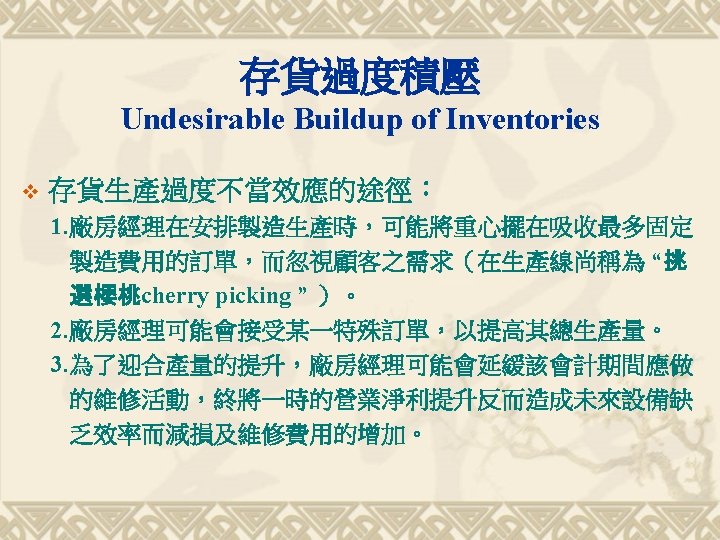

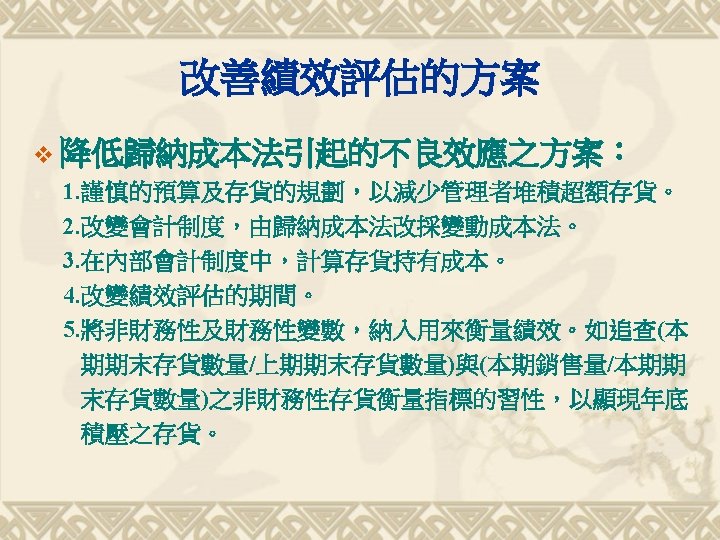

Learning Objective 4 Understand how absorption costing can provide undesirable incentives for managers to build up finished goods inventory 瞭解歸納成本法如何對管理人員 提供不當動機而積壓製成品存貨

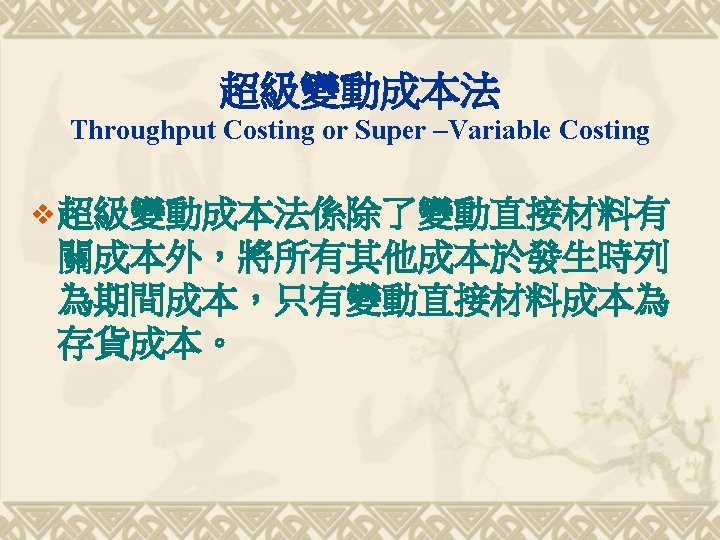

Learning Objective 5 Differentiate throughput costing from variable costing and absorption costing 透過變動成本法及歸納成本法 區別超級變動成本法

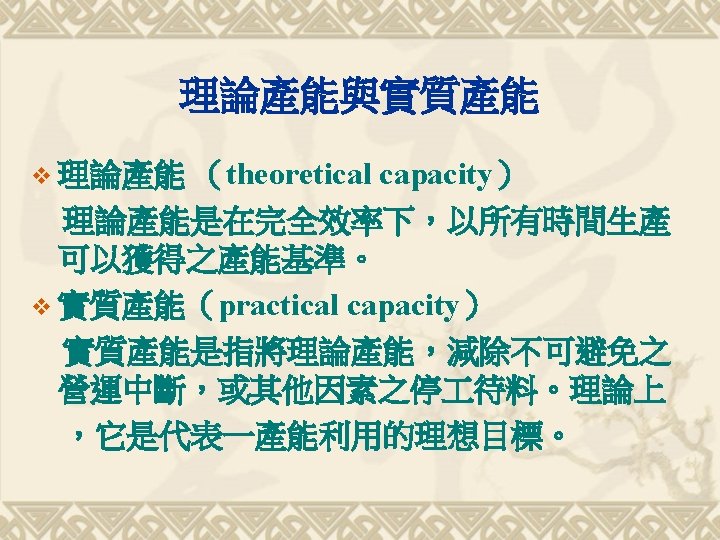

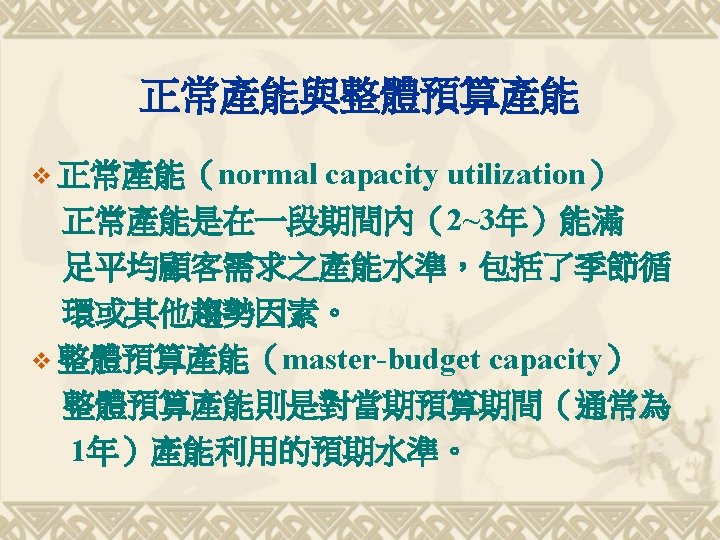

Learning Objective 6 Describe the various capacity concepts that can be used in absorption costing 描述可以使用在歸納成本法 之各種產能觀念

Learning Objective 7 Understand the major factors management considers in choosing a capacity level to compute the budgeted fixed overhead cost rate 瞭解管理當局在選擇產能水準以計算 固定製造費用成本率時之 主要考慮因素

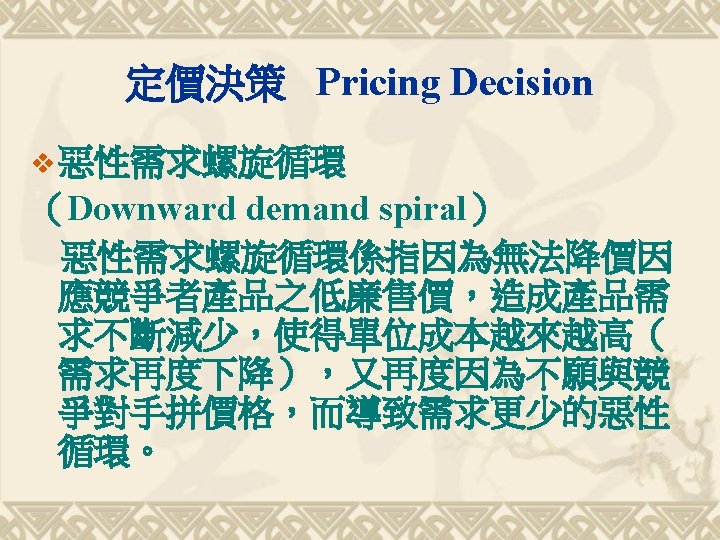

Learning Objective 8 Describe how attempts to recover fixed costs of capacity may lead to price increases and lower demand 描述回收基準產能固定成本時 將如何引導價格增加與較低需求