Privatization as Scapegoat Everyone Hates Privatization Tim Frye

Voucher/non-voucher,")

steal and steal. They")

Can investing")

")

on impact of YUKOS on stick")

versus Major violations")

steal and steal. They are stealing absolutely")

- Slides: 50

Privatization as Scapegoat: Everyone Hates Privatization Tim Frye tmf 2@Columbia. edu

Motivation Privatization – central element of reforms in the last 25 years from Mexico to Indonesia to Kyrgyzstan More generally, secure property rights critical to economic development and political stability. Benefits seem to outweigh the costs in most, but not all settings (Netter and Megginson 2005)

But Everyone hates privatization Majorities in every post-communist country prefer revising privatization to keeping the status quo

Road Map Public Opinion toward Privatization Almost everyone hates privatization, but why? What can be done? Co-authors: Irina Denisova, Ekaterina Zhuravskaya and Markus Eller

Data “Life in Transition” Survey, EBRD and WB, 2006 28 post-communist countries in Europe and Central Asia Representative sample of 1000 individuals in each country, face-to-face interviews Information on HH income and assets, individual education, employment history, hardships during transition, and attitudes towards markets, democracy, and privatization

Individual attitudes towards revising privatization “In your opinion, what should be done with most privatized companies? They should be… Left in the hands of current owners with no change 2. Renationalized and kept in state hands 3. Renationalized and then re-privatized again using a more transparent process 4. Left in the hands of current owners provided they pay privatized assets’ worth. ” 1.

Responses Renationalize and keep in state hands Leave with Renationalize & current owners Leave with of re-privatize current provided that using a more they pay owners with transparent privatized no change process assets’ worth PERCENT 29. 0 16. 7 34. 8 19. 4 Cumulative 29. 0 45. 7 80. 6 100

% of respondents Responses in selected 10 countries

Interpreting the Data Eighty percent of respondents favor revising privatization in some way… A Majority in every country favor revising privatization in some way

But… Less than a third favor having privatized assets ultimately reside in state hands Inappropriate to equate opposition to privatization with support for nationalization

Who supports expropriation? Even if we consider support for expropriation, that is renationalize or reprivatize == 46% Versus pay tax or leave in hands of current owners == 53%

Part II. Why Macro Level Explanations Not type of privatization (although badly measured) Voucher/non-voucher, sales versus giveaways Weak evidence that early privatizers have less opposition

Not Economic Performance Not Economic performance E. g. , economic growth and inflation rates unrelated Not surprising Hard for economists to pinpoint effects Privatization policies differ Non-random selection of firms into privatization Politicians among others exaggerate costs and benefits of privatization

Not a Soviet Legacy in 17 Latin American countries Latino Barometer Percent Agree with statement “Privatization has been beneficial to the country. ” 1998 2000 2002 46% 35% 28%

Privatization Paradox Even beneficiaries of privatization don’t like it. World Bank 2005 But See Di Tella (2010)

Institutions Matter on Average citizen in more democratic and better governed countries expresses less opposition to expropriating privatized property in postcommunist world.

For some groups institutions matter a great deal • Under democracy high skilled more strongly oppose revising privatization (low skilled equally opposed under autocracy and democracy) Interact Democracy with Market Skills Control for individual level variables And extent of privatization and country wealth

Predicted effect of interaction between democracy and market skills on public support for revising privatization

Change in probability of supporting a revision of privatization moving from high to low skilled. . .

More Generally. , , Suggests a complementarity of economic and political reform Suggests that different coalitions might be needed to support reforms in democracies and autocracies

Individual Level Explanations Older, less skilled, and less healthy support revising privatization More wealthy, and home-owners oppose revising privatization Controlling for country-fixed effects

Empirical strategy § Run Multinomial Logit regressions with probability of choosing each of the 4 outcomes as dependent variable § on the variables of interest (i. e. , individual characteristics) § Perform the following tests on the marginal effects

Results, direct effects: human capital and wealth • Older, less skilled, and less healthy are in favor of privatization revision and have preference for state property (losses from wage decompression) • Education level increases the sense of unfairness • Assets, wealth, and income => against revision and prefer private property; relative income => unfairness (the richest are not in the sample)

Part III. What is to be done? Is privatization unpopular because of the process of privatization? Can privatized assets be made more legitimate after privatization?

Legitimacy of initial distribution of property unimportant “They (factory managers) steal and steal. They are stealing absolutely everything and it is impossible to stop them. But let them steal and take their property. They will then become owners and decent administrators of this property. ” Anatolii Chubais, Head of State Committee on Property of the Russian Federation.

An Alternative View: Legitimacy matters “This golden watch remains mine only as long as everybody around me agrees that it really belongs to me. If 90% of my neighbors should think different, I wouldn’t be able to sleep soundly anymore. ” Anonymous Banker in Russia

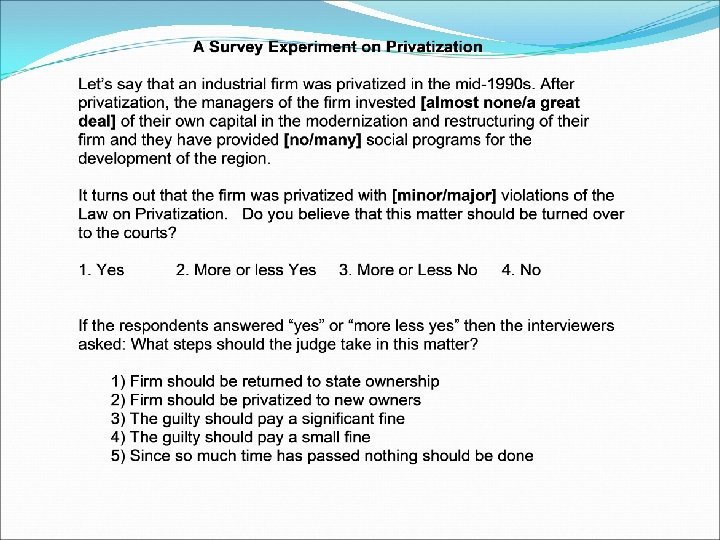

Two arguments: Can providing Public Goods increase support for privatization? (Good Works) Can investing in the firm increase support for privatization? (Good Use)

Survey Details Levada Center 1600 respondents in a nationally representative sample in October 2006 Face to Face Interviews Response Rate 57 percent Call Back 20 percent

Survey Based Experiment Randomly assigned 8 versions of a question. Manipulate type of good works, investment and severity of violations of privatization Differences in responses only due to small changes in question wording. Clean Test

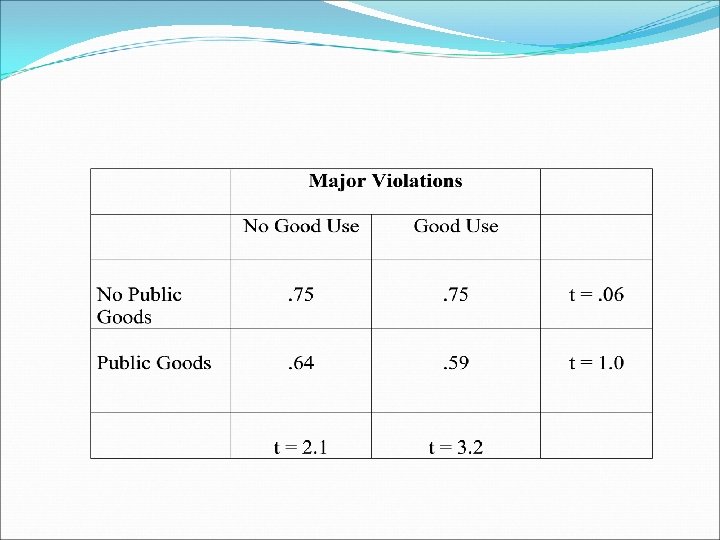

Percentage in Support for Revising Privatization when Violations are Major and….

Percentage in Support for Revising Privatization when violations are Minor and … 0, 8 0, 7 0, 670000000000003 0, 630000003 0, 6 0, 53 0, 5 0, 4 0, 3 0, 2 0, 1 0 No Public Goods/No Investment Public Goods/No investment No Public Goods/Investment

Results from Survey Experiment Public goods provision can increase legitimacy of property rights, but … Only 20 percent of respondents know which firms are providing public goods to the community.

Other Results On its own good use of an asset has little effect on the legitimacy of privatization. No Sweat Equity effect. Process Matters. More severe violations provoke more opposition to privatization.

Conclusion 1990’s era of privatization, 2000’s era of renationalization Algeria, Bolivia, Chad, Dubai, Ecuador, Kazakhstan, Russia, Ukraine, Senegal, Venezuela, Zimbabwe and elsewhere Why so few renationalizations? Is threat of renationalization sufficient? Spillover effects of renationalization

Who Expropriates Broader Literature autocracies and resource booms promote renationalization (Guriev et al. 2011) Autocrats in Latin America use renationalization to their supporters to signal commitment to them Albertus and Menaldo (2011)

Optimistic Note Much opposition from those without market skills Should ease over time Older workers with market skills oppose privatization significantly less Opposition from losses during transition Should also ease over time Support for private property is relative high, even as support for privatization is low

Thank you.

Privatization vs Privatization of the 1990 s in Russia, had many unique features – essentially a political project In some respects, privatization today has more economic basis

President Kirchner on his own privatization “There are companies, like Aguas Argentinas, that should acknowledge that what they did to us is shameful, because they have taken five thousand million dollars and did not even built two pipes”

Impacts of Revising Privatization Sonin and Goryayev (2011) on impact of YUKOS on stick prices of other firms Depressed private oil price, loans for shares firms, and boosted share prices of Gazprom

Minor violations

(Minor) versus Major violations

Major Violations Public Goods Provided N= 176, 160 No Public Goods Provided N = 179, 164 Good Use No Good Use . 24 = renationalization. 17 = reprivatization. 19 = big fine. 03 = small fine. 03 = do nothing. 36 = do not review . 34 = renationalization. 17 = reprivatization. 14 = big fine. 04 = small fine. 03= do nothing. 33 = no review . 39 = do nothing/no review . 36 = do nothing/no review . 33 = renationalization. 23 = reprivatization. 19 = big fine. 06 = small fine. 04 = do nothing. 16 = do not review . 32 = renationalization. 20 = reprivatization. 18 = big fine. 04 = small fine. 03 = do nothing 16= do not review . 20 = do nothing/no review . 19 = do nothing/no review

Probability of Supporting Revision

Minor Violations Public Goods N= 157, 147 No Public Goods N = 144, 138 Investment No Investment . 31 = renationalization. 10 = reprivatization. 12 = big fine. 04 = small fine. 04 = do nothing. 39 = do not review . 22 = renationalization. 18 = reprivatization. 22 = big fine. 03 = small fine. 05= do nothing. 32 = no review . 43 = do nothing/no review . 37 = do nothing/no review . 32 = renationalization. 11 = reprivatization. 24 = big fine. 01 = small fine. 04 = do nothing. 27 = do not review . 32 = renationalization. 20 = reprivatization. 15 = big fine. 03 = small fine. 00 = do nothing. 22 = do not review . 31 = do nothing/no review . 22 = do nothing/no review

Results: major violations

Coasian View of Privatization “They (factory managers) steal and steal. They are stealing absolutely everything and it is impossible to stop them. But let them steal and take their property. They will then become owners and decent administrators of this property. ” Anatolii C hubais, Head of State C ommittee on Property of the Russian Federation. èLegitimacy of initial distribution of property unimportant