WELLCOME Teachers Identity Mohi Uddin Lecturer Department Of

3 rd Year Deptt. Of Accounting & Deptt. Of Management")

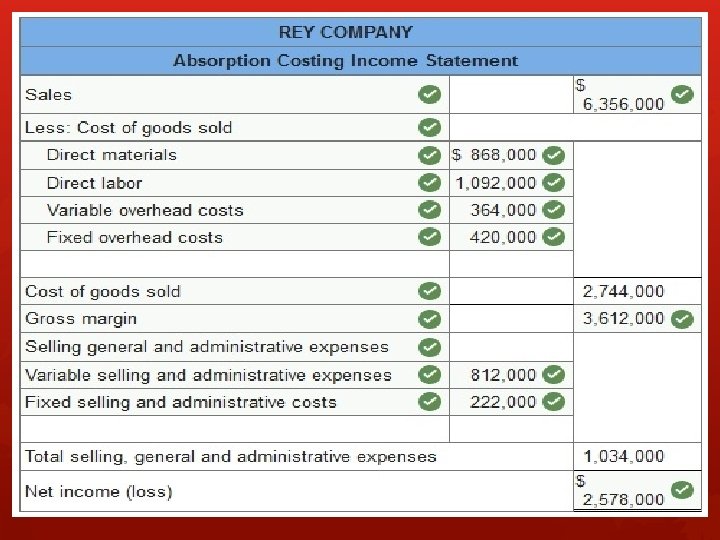

Bike Manufacturing Company presents the")

- Slides: 22

WELLCOME

Teachers Identity Mohi Uddin, Lecturer, Department Of Accounting Govt. Iqbal Memorial College, Daganbhuiyan, Feni.

Class & Subject BBA(Hon’s) 3 rd Year Deptt. Of Accounting & Deptt. Of Management

LEARNING OUTCOMES Define Direct Costing. Define Absorption Costing. Prepare Income Statement Under Direct Costing & Absorption Costing.

Product Cost Periodic Cost

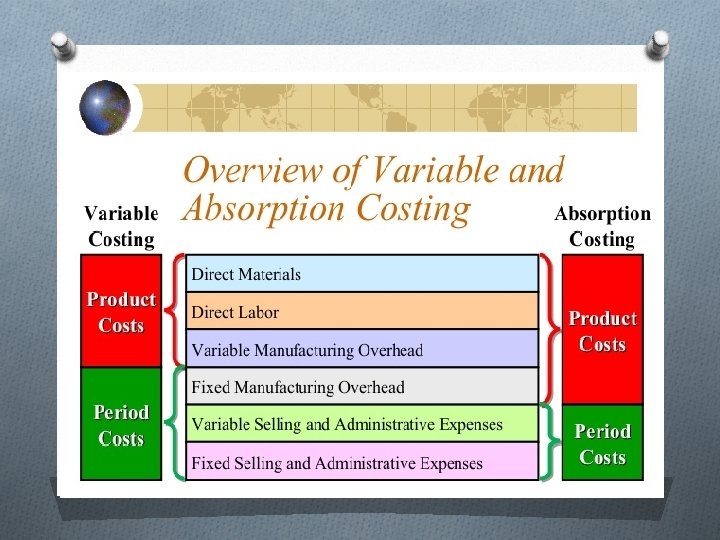

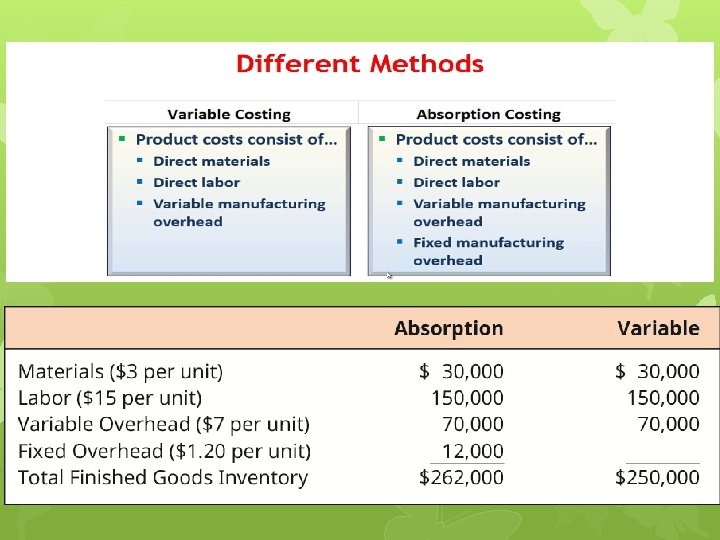

DIRECT/VARIABLE COSTING Direct/Variable costing consists of direct material costs, direct labor costs, and variable manufacturing overheads.

Absorption Costing Absorption costing consists of direct material costs, direct labor costs, variable manufacturing overheads, and fixed manufacturing overheads.

Exercise-1 (Unit product cost under variable and absorption costing) Bike Manufacturing Company presents the following data for 2011: Opening inventory 0 Units Sales 8, 000 Units Production 10, 000 Units Closing inventory 2, 000 Units Direct materials Tk. 240 Direct labor Tk. 280 Variable manufacturing overhead expenses Tk. 100 Variable selling and administrative expenses Tk. 40 Fixed manufacturing overhead expenses Tk. 1200, 000 Fixed selling and administrative expenses Tk. 800, 000 Required: Compute the unit product cost of one bike under: 1. Absorption costing system. 2. Variable costing system.

Computation of unit product cost: Absorption costing Variable costing Direct materials Tk. 240 Direct labor Tk. 280 Variable manufacturing overhead Tk. 100 Tk 100 Fixed manufacturing Overhead Tk. 120* ———— Unit product cost Tk. 740 Tk. 620 *1, 200, 000 / 10, 000 = Tk. 120 Notice: That the fixed manufacturing overhead cost has not been included while computing the cost of one bike under variable costing system.

Exercise-2 The following particulars are available from the books of Sakib & Company: Opening Inventory 2000 Units Ending Inventory 3000 Units Production during the year 9000 Units Normal plant capacity 10000 Units Cost analysis : Selling price per unit Tk. 40 Direct materials per unit 20 Direct labor per unit 6 Variable factory overhead per unit 4 Fixed factory overhead per year 10, 000 Administrative and selling overhead: Variable 4, 000 Fixed Required: (i) Prepare income statement using Direct costing and Absorption costing. (ii) Reconciliation statement. 12, 000

Workings: 1. Selling Units = Opening + Production – Closing = (2, 000 + 9, 000 – 3, 000) Units = 8, 000 Units 2. Calculation of cost per unit Element of Cost Direct materials per unit Direct labor per unit Variable factory overhead per unit Fixed factory overhead per Unit (Tk. 10, 000÷ 10, 000 Unit) Under Direct costing Total Cost Tk 20 06 04 30 - Under Absorption costing Tk 20 06 04 01 31

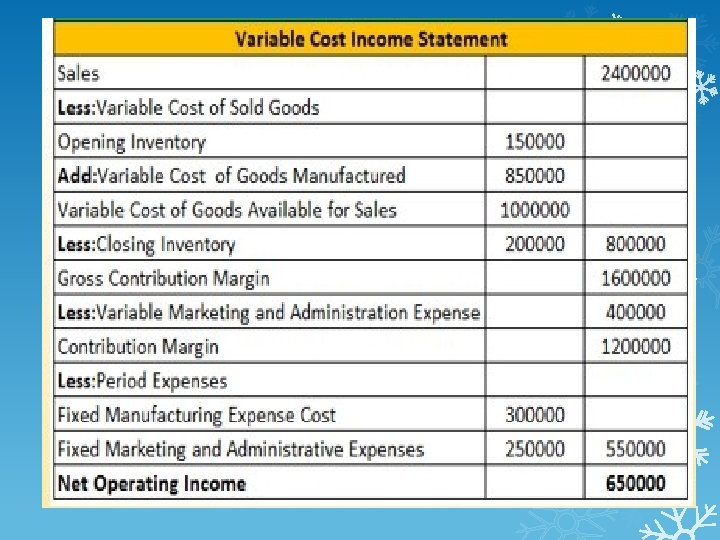

Sakib Company Income statement using Direct costing For the year Ended…………… Particular Tk. Sales(8, 000× 40) Less: Variable cost of goods sold(8, 000× 30) 3, 20, 000 2, 40, 000 Gross Contribution Margin 80, 000 4, 000 Net Contribution Margin Less: Fixed Cost Factory overhead Administrative & Selling O/H 76, 000 Less: Variable administrative & Selling O/H 10, 000 12, 000 Net Income 22, 000 54, 000

Sakib Company Income statement using Absorption costing For the year Ended…………… Particular Sales(8, 000× 40) Less: Cost of goods sold: (8, 000× 31) Add: Under applied fixed factory overhead{(10, 000 -9000)× Tk. 01} Gross Profit Less: Administrative & Selling overhead: Variable Fixed Net Income Tk. 3, 20, 000 2, 48, 000 1, 000 2, 49, 000 71, 000 4, 000 12, 000 16, 000 55, 000

Sakib Company Reconciliation Statement For the year Ended 31 December…… Particular Difference in Profit: Under Absorption Costing Under Direct Costing Difference in Inventory Cost: Change in Inventory(Closing Inventory-Opening Inventory) Under Absorption Costing(3, 000 -2, 000)× 31 Under Direct Costing(3, 000 -2000)× 30 Tk. 55, 000 54, 000 1, 000 30, 000 1, 000

Under Applied Fixed O/H Over Applied Fixed O/H Favorable variance from standard Unavorable variance from standard

Homework The following particulars are available from the books of Sakib & Company: Opening Inventory 1000 Units Ending Inventory 15000 Units Production during the year 4500 Units Normal plant capacity 5000 Units Cost analysis : Selling price per unit Tk. 20 Direct materials per unit 10 Direct labor per unit 3 Variable factory overhead per unit 2 Fixed factory overhead per year 10, 000 Administrative and selling overhead: Variable 2, 000 Fixed Required: (i) Prepare income statement using Direct costing and Absorption costing. (ii) Reconciliation statement. 6, 000