PERSONAL FINANCIAL LITERACY 1 1 CE PFL 1

� Duke University")

� UNC –")

You may transfer money to and from")

details, in depth information about your credit")

� � � Snapshot of a person's financial")

�")

� � � You")

")

- Slides: 111

PERSONAL FINANCIAL LITERACY 1. 1 CE. PFL. 1. 1 Explain how education, income, career, and life choices impact an individual’s financial plan and goals (e. g. , job, wage, salary, college/university, community college, military, workforce, skill development, social security, entrepreneur, rent, mortgage, etc. ).

Earning Power � � Earning power is the ability to earn money in exchange for work. How much you earn depends on the value of your skills in the marketplace. An individual’s value as a worker – the wage or salary received for a specific job – is related to the skill level and education of the worker, the demand for that work in society, and the availability of qualified workers.

Earning Power � � Generally, in our society, people with higher education and more skills earn more money on the job than those with less education and fewer skills. “Human Capital” -The set of skills which an employee acquires on the job, through training and experience, and which increase that employee's value

Socioeconomic Status � The position of an individual on a socialeconomic scale that measures such factors as education, income, type of occupation, place of residence

VALUE OF EDUCATION These figures show that for the average person, finishing high school is worth about $10, 000 more (compared with dropping out). And finishing college nearly doubles the worth of that number to $22, 000 more!

Cost of Education

Cost of Education � Private Universities – Undergraduate (4 year degree) � Duke University - $59, 578 annually $59, 578 x 4 years = $238, 312 for a 4 year degree from Duke University

Cost of Education � Public Universities – Undergraduate (4 year degree) � UNC – Chapel Hill - $24, 120 annually $24, 120 x 4 years = $96, 480 for a four year degree from Carolina

Trade Offs – Cost of Education � Trade off: � Option #1 You spend $89, 360 for a 4 year degree from Carolina Opportunity Cost: time, money, stress OR � Option #2 You graduate high school and work at Taco Bell Opportunity Cost: less money earned, less employable

Distributive Summarizing � � Assessment Prompt #1 1’s: What type of university or college is the most affordable? � 1 � minute 2’s: How will a college education affect your future earning power? � 1 minute

VALUE OF EDUCATION These figures show that for the average person, finishing high school is worth about $10, 000 more (compared with dropping out). And finishing college nearly doubles the worth of that number to $22, 000 more!

Uneducated = Unemployed Education pays in higher earnings and lower unemployment rates Source: www. bls. gov: Employment statistics of the civilian population 25 years and over by educational attainment.

An Employer’s Perspective “Som could eone wh high n’t com o plete scho o l pro finds b com it difficu ably plete lt to any task. ” gh i h a n a c t h “How brig ? ” e b t u o p o r d school “High schoo l can be har d wo high school dropout is p rk. A roba scared of a little hard w bly ork. ” “A high school dropou t didn’t lea some t hings t rn hat are nee d good a ed to be t this jo b!”

Other Employment / Career Options � Military – Enlist in the military � Can � become a lifelong career Entrepreneur – Own your own business � Set your own hours, become your own boss

Military � You can make a career out of the military � Benefits: Retire after 20 years Free healthcare for life Free housing (on post) while serving or a housing allowance to live off post Free food (on base) Increase in rank = increase in salary Pension plan after retirement � Risks: Must live where they tell you May have to live overseas May be put into life threatening situations

Entrepreneurship � Entrepreneur � Willing to take risks � A person who creates a business from scratch. � Self employed � Strong sense of discipline � Be your own boss � Beat the competition

Entrepreneurship � RISKS � No guarantees � No regular paycheck � No boss � Long hours � Assume debt of business � REWARDS � Be your own boss � Keep profits � Control � Satisfaction � Pursue talent and creativity

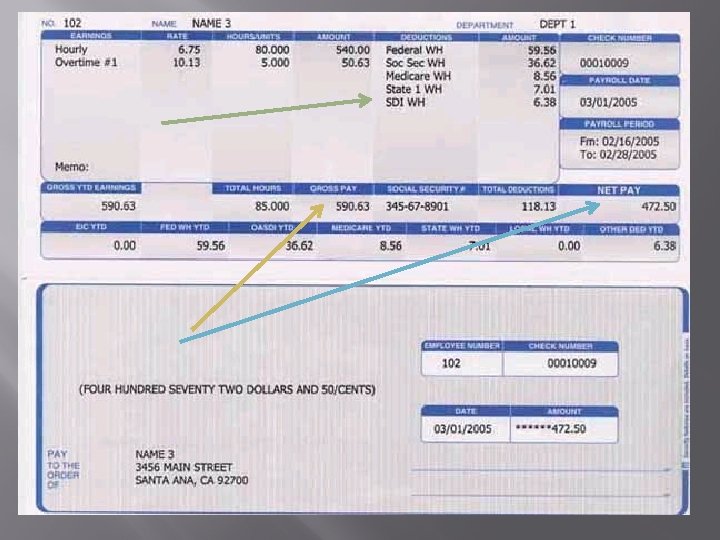

Income - Your Paycheck � Your paycheck includes the following: � Gross Pay - the amount you earned � 40 hours @ $7. 50 per hour = $300 �This is NOT what you bring home � Deductions – what is deducted from your paycheck Federal income tax withheld Social Security withheld Medicare withheld State income tax withheld Other deductions (insurance) � Net Pay – the amount you bring home – DISPOSABLE INCOME

Distributive Summarizing � � Assessment Prompt #2 1’s: What is your gross pay? � 1 � minute 2’s: What do you call the pay you actually receive? � 1 minute

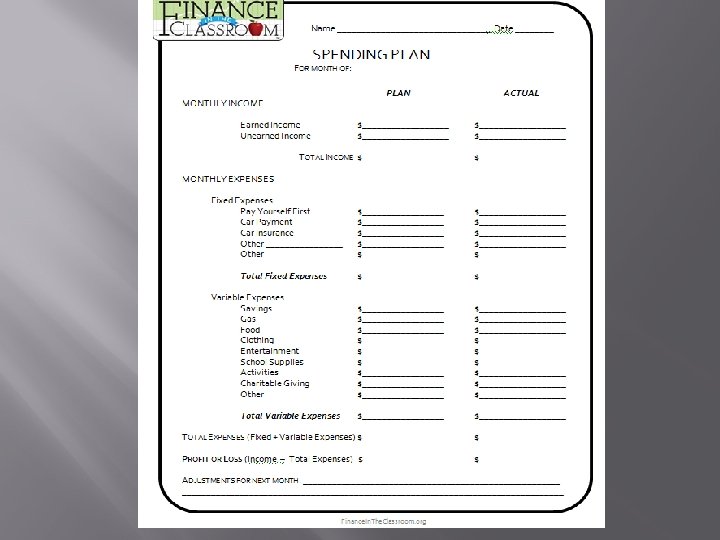

What is a spending plan? � A tool used to record and track projected and actual income and expenses over a period of time. � Income: Money you make � Expenses: Bills you owe � Also called a budget. � Your budget should be balanced. � Income should exceed expenses.

Opportunity Cost of Spending Plans � Consumers may feel like having a budget is confining or restrictive, but it actually gives them more freedom and more options.

Money Management A spending plan can help you: � Put aside money for savings goals � Prepare for regular expenses � Prepare for unexpected expenses � Control how you spend money � Reduce stress and increase confidence � Provide an excuse to calm excessive spending

“Pay Yourself First” � � � Before you pay any bills, you should “Pay yourself first” In other words, put money in a savings account for yourself to insure you have a “nest egg” Considered the “golden rule” of personal finance

Expenses FIXED COSTS – COSTS THAT ARE THE SAME EACH MONTH � Savings � Mortgage (house) payment � Rent � Car payment � Insurance � Daycare VARIABLE COSTS – COSTS THAT CHANGE EACH MONTH � Gas � Food � Clothing � School supplies � Utility bills (electric, water, phone)

Distributive Summarizing � � Assessment Prompt #3 1’s: What is the difference in a fixed expense and a variable expense? � 1 � minute 2’s: Why should you “pay yourself first”? � 1 minute

Discretionary Income � � Income that is left over AFTER your bills are paid Spent on non-essential items � Vacations � Luxuries � Eating Out � Amusement Parks

More expenses than income? � � � Negative cash flow typically results in debt. Part of being financially independent is spending less than you earn.

What is a Checking Account? � � Common financial service used by many consumers Considered a “demand deposit” account because funds are easily accessed � Check � ATM (automated � Debit card � Telephone � Internet � teller machine) Services and fees vary depending upon the financial institution

Withdrawals � � Withdrawals take money from your account Examples include: � Written Checks � ATM Withdrawal (automated – conducted electronically) � Debit card purchase (automated – conducted electronically) � Online debit card purchase (automated – conducted electronically)

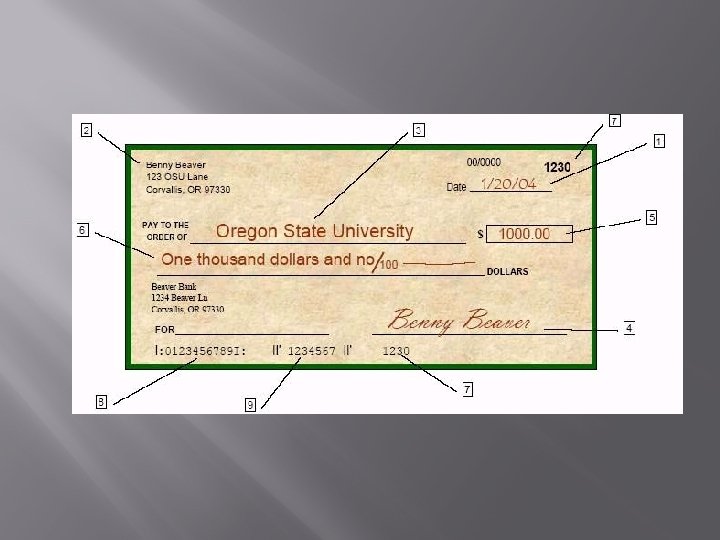

Transfers � Transfers (automated – conducted electronically) You may transfer money to and from your checking account from another account (another checking account or a savings account) You may do this online OR at the bank

Why Do People Use Checking Accounts? � � � Reduces the need to carry large amounts of cash Convenience – useful for paying bills Spending Plan Tool � Keeps � a record of where money is spent Safety – using checks is safer than carrying cash

What is a Check? ¡ � Used at the time of purchase as the form of payment ¡ Considered a withdrawal ¡ Money taken from your account Piece of paper pre-printed with the account holder’s: Name � Address � Financial institution � Identification numbers �

Bouncing a Check � Check written for an amount over the current balance held in the account � ‘Bounces’ due to insufficient funds, or not enough money in the account to cover the check written � This results in an overdraft You “overdraw” the amount of money in your account Some banks allow for overdraft protection by covering the check as a loan � � A fee will be charged to the account holder Harm future opportunities for credit

Endorsing a Check � Endorsement � Signature on the back of a check to approve it to be deposited or cashed � A check must be endorsed to be deposited

Other Checking Components � Checking Account Register � Place to immediately record all monetary transactions for a checking account Written checks, ATM withdrawals, debit card purchases, deposits and additional bank fees �Some checking accounts charge maintenance fees � Checkbook � Contains the checks and the register to track monetary transactions

ATM � � � Automated teller machine, or a cash machine Can be used to withdraw cash and make deposits Additional fees may be assessed if the ATM used is not provided by the financial institution sponsoring the card

Debit Card � � Plastic card that looks like a credit card Electronically connected to a bank account Money is automatically taken from the bank account when purchases are made Requires a PIN (personal identification number) � Confirms account the user is authorized to access the

Pros and Cons - Debit Cards Pros � � � Convenient Small Can be used like a credit card Allows a person to carry less cash Does not allow overspending Cons � � � Can lose track of balance if transactions are not written down Opens checking account up to credit fraud Others can gain access to the account if the card is lost and PIN is known

Deposits � Deposit slip Contains the account holder’s account number and allows money (cash or check) to be deposited into the correct account � Located in the back of the checkbook � � Complete a deposit slip to make a deposit Deposited amount must be recorded in the checking account register to keep the balance current Deposits can be made at an ATM or with a bank teller

Completing a Deposit Slip ¡ Date l The date the deposit is being made

Checking Account Register � Place to record all monetary transactions for a checking account Deposits, checks, ATM use, debit card purchases, additional bank fees � � Used to keep a running balance of the account Remember � Record every transaction!

Check Register � Date � The date the check was written or transaction was made

Monthly Bank Statement � � Lists each monetary transaction and the current account balance for a specified time period Includes: � Dates � Identification for each transaction (number or type, date, amount) � Transaction amounts for withdrawals and/or deposits � Interest earned (if applicable – some checking accounts earn interest) � Fees or charges (if applicable) Bounced check fee Maintenance fee

Monthly Bank Statement � Lists each transaction and current account balance � Deposits � Checks � Debit Card transactions � ATM transactions � Additional fees

Reconciling a Checking Account � Reconcile � Balance the checkbook register each month to the balance shown on the statement � Do this every month to ensure the correct balance in the checkbook � Knowing the correct balance can help to avoid bouncing checks

Checking Account Safety � If a checkbook, ATM, and/or debit card becomes lost or stolen � Immediately report it to the financial institution � File a report with the police � Reported lost/stolen checkbook: � Financial institutions generally do not hold the account holder liable for any fraudulent charges

Safety continued � Reported lost/stolen ATM/debit card: � Within 2 business days Cardholder is only liable for $50. 00 � Longer than 2 business days Could be liable for up to $500. 00 � Varies depending upon the financial institution May not charge the account holder anything if the correct steps were taken to report the lost/stolen card

What is a Savings account? � “Time Deposit” � An account used to deposit money at a bank or credit union and earn interest on the account over time. Interest: Money earned based on the amount of money in your savings account and the interest rate paid to you by the bank – considered an investment – a way to earn money over time � Money can be added or removed from the account by visiting the bank. (Deposit or withdrawal) � Usually � you can add or withdraw funds at any time; however, you will lose interest earned if you withdraw money – the higher the account balance, the more interest you earn. Banks may require a minimum to open or maintain the account.

CREDIT DEFINITIONS Credit Trust given to another person for future payment of a loan, credit card balance, etc. Creditor A person or company to whom a debt is owed. 52

Credit Rating � A measure of a person’s ability and willingness to make credit payments on time.

Credit Report A Consumer Credit Report (CCR) details, in depth information about your credit history, and will also include: Your full name Any alias’s that you have used Social Security Number Current address Previous addresses Your credit report may also contain: Your phone number Age/date of birth Your employer’s details

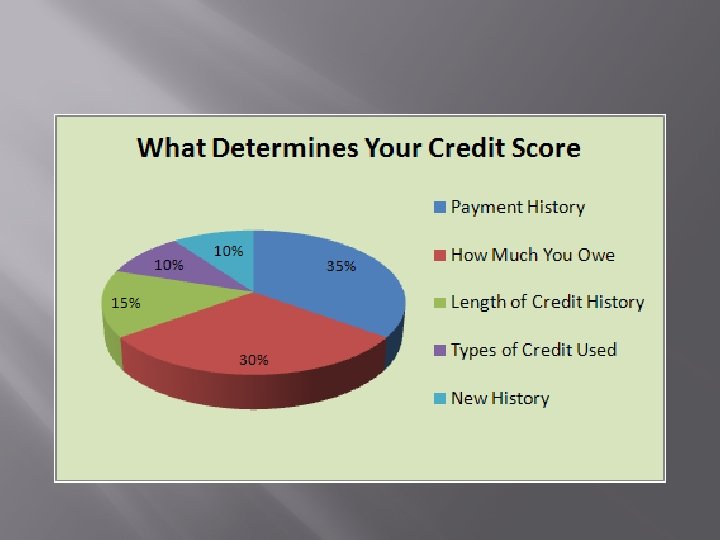

What is a Credit Score? (FICO) � � � Snapshot of a person's financial standing at a particular point in time The one most widely used is the "FICO" score (Fair Isaac Corporation) The FICO score, a three-digit number between 300 and 850

Convenience of Purchase � Buying on credit can be more convenient than using cash. Using credit makes the initial purchase very easy.

Less Risk of Losing Cash at the Time of Purchase � When using cash, you have to worry about someone stealing it. One who loses a credit card has a limited or no liability for unauthorized charges if the card company is notified.

Free Use of Another’s Money � Generally firms do not charge interest if the entire debt is paid by the end of the billing cycle. The buyer uses another’s money for that period of time.

Building a Credit Rating � Some people use credit to develop a good credit rating. Once a good credit rating is established they can get credit for larger purchases such as automobiles, houses, etc.

How to maintain good credit: � � � � Practicing good banking techniques, such as not bouncing checks Paying bills on time and consistently Avoiding bankruptcy Not having a criminal record Having a low number of credit/store cards Removing errors from credit report Maintaining reasonable amounts of unused credit Keeping organized records

Credit Cards � Plastic cards with electronic information that can be used by the holder to make purchases or obtain cash advances using a line of credit made available by the cardissuing financial institution.

Installment Loan � A loan in which the amount of payment and the number of payments are predetermined, such as an automobile loan. � Fixed payment � Set period of time � Set or varying interest rates � Examples: Car loans and mortgages

Revolving Credit � A type of credit that does NOT have a fixed number of payments, such as a credit card. � No stated payoff time � Limit to credit � Minimum monthly payments � Finance charges � Example: credit card

Student Loans � � Loans offered to students to assist in payment of the costs of professional education. These loans usually charger lower interest than other loans, and are also usually issued by the government. Allows a person to finance their education and defer payments until after graduation.

Sources of Credit – Who Can I Borrow Money From? � � � Bank Credit Union Finance Companies Retail Stores Savings & Loan Associations Internet Stores

Good Debt vs. Bad Debt GOOD DEBT � A reasonable Mortgage Loan � Mortgage � � = Home loan A reasonable Auto Loan Student Loans Business Loans Small Credit Load These “GOOD” debts may be needed, but you can over-leverage yourself. In that case, it could be considered a bad debt.

Good Debt vs. Bad Debt BAD DEBT � � � Excessive Credit Card Debt Furniture Loans Computer Loans Retail Store Card Debt Payday Loans Tax Anticipation Loans These “BAD” debts are a generalization. There may be times when you get a loan for something like a computer. REMEMBER, it is always better to save up money beforehand pay cash.

Who Looks at Your Credit? � Lenders � � Credit � Cards � Store Cards � Auto Loans � Mortgages � Personal Loans � Furniture Loans � Computer Loans � � � Utility Companies Cell Phone Companies Insurance Carrier Employers Military (Security Clearance) Rental agents Bank � (checking/savings accts)

What Type of Accounts Build Credit? NO YES � Credit Cards � Store Cards � Auto Loans � Mortgages � Personal Loans � Furniture Loans � Computer Loans � Checking/Savings � Cell Accts Phone � Utilities � Insurance � Rental Agents (Housing) � Employers � Payday Loans � Title Loan Companies

Credit Scores Affect Financial Options � HIGH SCORES � Low interest rate on loans � Ability to receive loans/credit � Reflects borrower is a low risk to lender � Ability to acquire conveniences such as cell phones and credit cards � LOW SCORES � High interest rate on loans � Inability to receive loans/credit � Reflects borrower is high risk for lenders � Inability to acquire conveniences

How Does A Credit Score Help You? � Improves risk assessment � Lenders, Insurance, Employers, Housing � More equal treatment among borrowers � Able to qualify more quickly for credit � Credit “mistakes” will not affect your ability to obtain lending as drastically

How to Build Credit � Open a line of Credit: Credit Card � Buy things you would normally buy, pay off at the end of each month � If you don’t qualify, consider a secured card � Take caution when asking for a co-signer � Buy things you would normally buy during the month � Pay the account off in full at the end of each month

Cost of Credit - Auto � Good Credit History � Pay $15000 � Loan Terms 60 months at � Payment = $297 a month � Total Cost of payments 4. 5% = ($279. 65) x (60 months) = $16, 779 � Poor Credit History � Pay $15000 � Loan Terms 60 months at � Payment = $372 a month � Total Cost of payments 26% = ($449. 11) x (60 months) = $26, 946

Cost of Credit – Mortgage $200, 000 home, 30 year fixed � 750 FICO � 4. 5% � Total Cost of Payments = ($1013. 37) x (360 months) = $364, 680 � 620 FICO � 6% � Total Cost of Payments = ($1199. 10) x (360 months) = $431, 676 DIFFERENCE = $66, 996

TYPES OF CREDIT CARDS Private Label • Issued by a single source • Can only be used at a single source • Examples: Department Stores, Gasoline Companies • BP Gas Card • Belk’s Card General Label • Issued by a single source • Can be used in many places • Examples: Bank Card, Major Credit Card • Discover Card • Bank of America Visa Card 77

Costs of Using Credit � Finance charges A fee charged for the use of credit or the extension of existing credit. � Allow lenders to make a profit on the use of their money � � Interest � � Late fees � � The charge for the privilege of borrowing money, typically expressed as an annual percentage rate (APR). A fee charged when a payment is not received on time Closing costs � The expenses, over and above the price of the property that buyers and sellers normally incur to complete a real estate transaction. (bank and lawyer fees)

SHOPPING FOR A CREDIT CARD DECISIONS, DECISIONS. . . ANNUAL FEE? APR? COMPUTATION METHOD? GRACE PERIOD? FINANCE CHARGE? CREDIT LIMIT? CARD INCENTIVES? 79

QUESTIONS TO ASK WHEN SHOPPING FOR A CREDIT CARD • • 80 Annual fee Annual percentage rate (APR) Minimum payment Computation method Grace period Finance charges Card incentives

The Cost of Using Credit SCENARIO: � Interest Rate 17% � Minimum Payment 2. 5% or $10. 00 Balance Time to Pay Off Interest Charged Total Pay $1, 000. 00 12 years $979. 00 $1, 979. 00 $2, 500. 00 19 years $2, 941. 00 $5, 441. 00 $5, 000. 00 24+ years $6, 210. 00 $11, 210. 00

The Cost of Using Credit SCENARIO: � Interest Rate 24% � Minimum Payment: 4% of current balance or $10 Balance Time to Pay Off Interest Charged Total Pay $2, 000. 00 9 yrs & 9 mo $1, 774. 96 $3774. 96, $6, 000. 00 $5, 775. 08 $11, 775. 08 $9, 774. 89 $10, 000. 00 14 yrs & 4 mo 16 yrs & 5 mo

How long will it take to pay off? (Paying only the minimum payment) � � � You owe $4500 APR = 21% Minimum Payment: 4% of current balance or $15

How much will it cost? (Paying only the minimum payment) � � � You owe $4500 APR = 21% Minimum Payment: 4% of current balance or $15

27” TV ûSuppose you see a TV you want to buy with a retail price of $400. �$400. 00 � cash ûIf you have saved enough in your “buy stuff” account, you can withdraw your money and buy the TV. If you use a credit card, and pay off the balance within the billing cycle, you pay no interest (if it is a credit card which has the grace period).

27” TV On Sale ûIf you shop around and find the same TV for $350, you just saved $50. But what did you save in terms of your ability to earn money? If you are in an average tax bracket of about 20%, you must earn $62. 50 before you can spend $50. So if you avoid spending $50, that is like earning $62. 50. If you earn $10 per hour, you just saved the equivalent of 6 1/4 hours of work! $350. 00 � o o by smart shopping $50 /. 80 = $62. 50 earn $62. 50 / 10 = ~6 1/4 hrs

27” TV $400. 00 using a credit card Paying $26. 00/mo Balance $400. 00 o o Time to Pay Off 18 months Interest Total Pay Charged $59. 00 $459. 00 $59. 00 /. 80 = $74 earn $74 / 10 = ~7. 4 hrs extra to pay the $59.

27” TV $400. 00 Finance Company � 36% A. P. R. � 18 months � $29. 00/month � $123. 00 interest 523 � Total Cost $ � $123 /. 80 = $154 � $154 / 10 = ~15. 4 hrs

27” TV $400. 00 Too Easy Loan � 300% A. P. R. Bad Credit OK ) (Bad � Car Title Pawn 18 months $102. 00 payment/month $1, 433 interest � Total Cost $1833 � $1433 /. 80 = $1791 � 1791 / 10 = 179 hrs � � �

Warning Signs of Credit Abuse � � � Delinquent Payments � Not making payments on time Default Notices � Letters from creditors requesting that you catch your payments up Repossession � Creditors take away property used as collateral when payments are not made � Collateral - Property or other assets that a borrower offers a lender to secure a loan

Financial Consequences of Debt � � Overspending Paying high interest rates Lowers credit score Difficulty getting a loan

Savings is the portion of current income not spent on consumption. Investments Investing is the purchase of assets with the goal of increasing future income.

Risk, Return, and Liquidity � Risk � The chance that the value of an investment will decrease. � Return � The � profit or yield from an investment. Liquidity � The ability of an investment to be converted into cash quickly without loss of value.

Risk, Return, and Liquidity � Savings �Low risk �Low return �High liquidity � Investments �High risk �High return �Low liquidity

DISTRIBUTIVE SUMMARIZATION � THINK-PAIR-SHARE � WRITE DOWN WHETHER YOU ARE MORE LIKELY TO INVEST IN STOCKS, ETC. OR TO PUT YOUR MONEY IN A SAVINGS ACCOUNT. EXPLAIN WHY.

Time Value of Money � The time value of money refers to the fact that a dollar in hand today is worth more than a dollar promised at some future time.

Future Value � � Refers to the amount of money to which an investment will grow over a finite period of time at a given interest rate. Put another way, future value is the cash value of an investment at a particular time in the future.

Stocks � � An investment that represents ownership in a company or corporation. You purchase a portion of the corporation.

Purchasing Stock � A Broker is a person who is licensed to buy and sell stocks, provide investment advice, and collect a commission on each purchase or sale � Purchases stocks on an organized exchange (stock market) � Over ¾ of all stocks are bought and sold on an organized exchange

Stock Certificate

How Well the Stock Market Is Doing Overall � Bull Market � the market is doing well because investors are optimistic about the economy and are purchasing stocks Ø Bear market • the market is doing poorly and investors are not purchasing stocks or selling stocks already owned

SUMMARIZATION � � THINK OF A WAY TO REMEMBER THE DIFFERENCE BETWEEN BULL MARKET AND BEAR MARKET. SHARE WITH THE CLASS WHEN ASKED TO DO SO.

Bonds � Loan of money from a lender to a borrower for a set time period, which pays a fixed rate of interest. � Government bonds Issued by the government to raise money Example: Savings bonds, Liberty bonds (war bonds) � Corporate Issued by corporations to raise money to invest in capital

US Savings Bond

Liberty Bonds (War Bonds)

Mutual Funds � � An investment that pools money from several investors to buy a particular type of investment, such as stocks. Decreases risk because your money is placed in various stocks

Pension Funds � � A fund established by an employer to facilitate and organize the investment of employees' retirement funds contributed by the employer and employees Comes out of your paycheck

Savings � � Place your money in a savings account that gains interest over a set period of time. No penalty for withdrawal

Certificates of Deposits – CD’s � A deposit that earns a fixed interest rate for a specified length of time. � The longer the time period the greater the rate of return. � There is a substantial penalty for early withdrawal.

Money Market Account � A savings account that offers the competitive rate of interest (real rate) in exchange for larger -than-normal deposits.

Risk vs. Return � On average, stocks have a high rate of return � The increase or decrease in the original purchase price of an investment � Higher rate of return = greater risk � Uncertainty � about the outcome of an investment Stocks provide portfolio diversification � Money invested in a variety of investment tools