LongTerm Care Planning Ahead and Planning for Now

LTC ◦")

compliant long term care annuity �")

- Slides: 32

Long-Term Care: Planning Ahead and Planning for Now UCSB Emeriti/Retiree Center Brad Tisdale, MS, CES, CLTC June 27, 2018

What Causes People to Need Care? � Typically due to normal aging and frailty � However, a long-term care event can happen to anyone at any age. � Our reality: 40% of people who need care under age 65 (USA Today) � Temporary

What Is Reality of Needing Care? � For the general population, 70% of those who turn age 65 will need care at some point in their lives � For the individual, the chance of needing care is either zero (0%) or 100% � American Association for Long-Term Care Insurance

Where is Care Provided • • Home Care Nursing Home Care Adult Day Care • Assisted Living • Nursing Home Care 13% 87% Home Care, Adult Day Care and Assisted Living Source: “Facts and Trends: The Nursing Facility Sourcebook”, American Health Care Association, 2001 & “Older and Younger People with Disabilities: Improving Chronic Care Throughout the Life Span”, Mental Health. About. com, January 2, 2002. In Washington: Adult Day Health Care

What Does Care Cost Today? � The Average Cost for Someone receiving 8 hours of home care per day… ◦ ◦ $30 per hour $240 per day $7, 200 per month $86, 400 per year � Will these costs be higher or lower in future?

What Pays for Care Only 3 Things Pay for Long-Term Care Services 1. Monthly Income (cash) �If not enough income, you liquidate assets to cover the shortfall 2. If low income and assets: Medi-Cal 3. Long-Term Care Insurance

Long-Term Care Insurance � Paying � An for care is about cash flow LTC Policy is like a big checking account ◦ You choose how much is initially in the account ◦ You choose the monthly benefit amount ◦ You select the interest rate on the account ◦ Riders

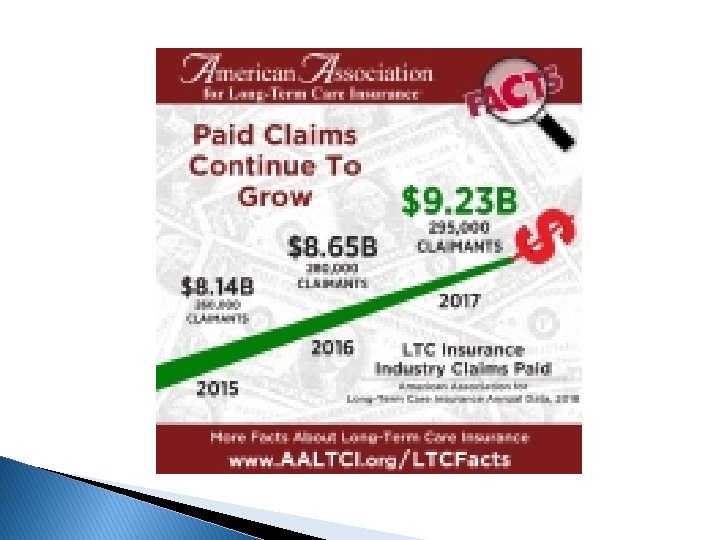

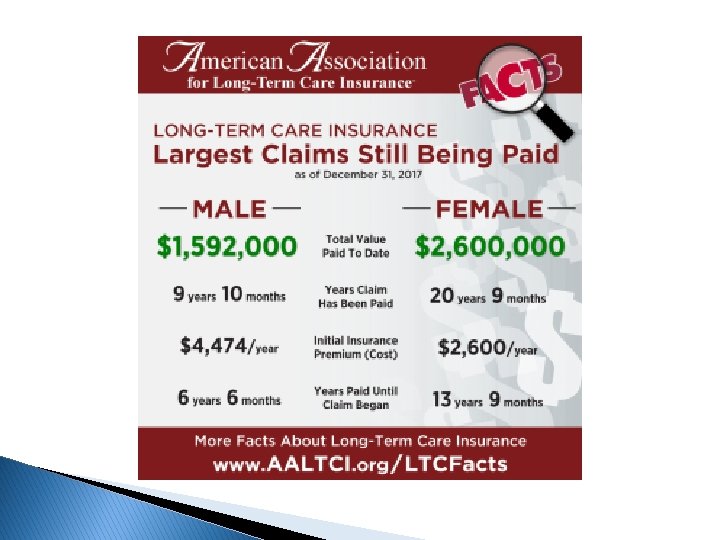

What Are These LTC Numbers? �$9. 23 �$2. 6 Billion Million �$1. 592 Million

LTC Insurance � Two Types of Long-Term Care Insurance 1. Stand-alone (traditional) LTC ◦ Private insurance ◦ Cal. PERS 2. Hybrid or Linked Benefit LTC ◦ Life Insurance chassis ◦ Annuity chassis

Policy Benefit Triggers � Assistance ◦ ◦ ◦ with 2 Activities of Daily Living Bathing Dressing Toileting Transferring Continence Eating � Supervision due to a Cognitive Impairment � Due to aging, frailty, accident or illness

Stand Alone Long-Term Care Insurance • • • Pay an annual or monthly premium until needed Premiums based on age, health and selected benefits Reimburses expenses up to monthly maximum for: ◦ Home and Community Care ◦ Facility Care (Assisted Living, Residential and Skilled) Economical retirement protection “Pennies on the Dollar” No cash value or death benefit

Stand Alone Long-Term Care Insurance • • Private Insurance: ◦ Regulated, Dept of Insurance oversight ◦ Reinsurance ◦ Low risk investment strategy (80% long-term bonds) ◦ Cumulative increase of 20%-60% on some blocks of business ◦ Policies priced much higher today, NAIC rate stabilization Cal. PERS (CA State Employees, Teachers) ◦ Non Regulated program, Board of Director oversight ◦ “Self Funded” Program ◦ High risk investment strategy, 65% stock market ◦ Multiple rate increases since 2002, latest was 85% ◦ Class action lawsuit in progress ◦ Lower premiums and more liberal underwriting than private ◦ Good option for those who may not health qualify for private

Hybrid/Linked Benefit Policies � � Built into a life insurance or annuity policy ◦ HIPAA and Pension Protection Act Compliant Policies can be funded with ◦ Savings, money market, CDs ◦ Cash in existing Annuity or Life Insurance policy ◦ IRA Money � Always pay a benefit � Single, Limited or Lifetime Premiums � Premiums do not increase

Examples of Life Ins with LTC Benefits Self Funding with Leverage 60 Year Old Single Female with 2 children, retired CPA Repositioned $100, 000 into single premium Life Policy with LTC Benefits Total Life/LTC Benefits -- $549, 000 • • Monthly Benefit -- $21, 960 Liquidity – Cash Value in 20 years of $92, 000 Result • • Predictable stream of income to pay for care Payout to beneficiary if care not needed No material change to her balance sheet No ongoing out of pocket premium expense

Examples of Life Ins with LTC Benefits Repurpose Existing Life Insurance, 70/68 Year Old Couple $75, 000 of Cash Value in his life policy; $3, 000 yearly premium • • • Used Cash Value and Premium to purchase Life with LTC Benefits Annual Premium of $6, 400 for continuing LTC Benefits Premium guaranteed not to increase Result • • Joint Policy with Unlimited Long-Term Care Benefits for each Monthly Benefit of - $4, 400 3% Compound Inflation on LTC Benefits $109, 642 Death Benefit if Care not needed (second-to-die) Net New Expense for Long-Term Care Benefits was $3, 400 per year

Long-Term Care Annuities A Pension Protection Act (PPA) compliant long term care annuity � It has HIPAA long-term care benefit triggers ◦ 2 of 6 ADLs ◦ Cognitive Impairment � 1035 Exchange funds from existing annuity � Withdrawals non subject to income tax when used for qualified long-term care expenses

Long-Term Care Annuities A great option for those with: � Low cost basis non-qualified annuities � Cash value in a life insurance policy � Cash earning little or nothing in CD or Money Market Money safe, liquid and growing tax deferred Funds pass to a beneficiary if care not needed

PPA Compliant LTC Annuities � Great � for those who are older or have health issues No Exam or Medical Records: q. Answer NO to: ü Alzheimer’s/Dementia ü Parkinson’s ü Paralysis ü Dialysis ü Organ transplants ü ADL limitations and supportive equipment

Pension Protection Act Case Study from 2010 Couple Ages 66 and 65 Ø Felt Stand-Alone LTC insurance was too expensive Ø May not have health qualified for Stand-Alone LTC Ø Husband had an existing non-qualified annuity with low basis, it was not needed for income • Annuity value of $214, 000 with a $40, 000 basis • Issued 1985 and out of surrender

Pension Protection Act Annuity Example Ø He did a 1035 Exchange to a Pension Protection Act compliant annuity for long-term care Ø This Created a NON TAXABLE bucket of money to pay for care if needed ◦ ◦ ◦ Added his wife to policy as second insured Current Long-Term Care Value is $301, 000 Monthly Benefit of $8, 700 for one or both of them 3. 65 compounding inflation on LTC value Cash Value passes to beneficiary if no care needed

What About Those… Ø Who are receiving care now? ◦ They have no LTC insurance ◦ Concerned about running out of money ◦ How can they cover the gap between monthly income and monthly cost of home care or facility care?

Those Who Need Care Today Ø • Care Plan with Lifetime Income Immediate Needs Annuity ◦ Age and Gender ◦ Current health and medications ◦ ADL needs ◦ Cognitive issues ◦ More health issues means greater monthly income for life ◦ Cannot be medically declined

Those Who Need Care Today Ø Medically Underwritten SPIA Ø Example: ◦ Annuitant: Male, age 82 ◦ Condition: Dementia ◦ Monthly Income Desired: $3, 000 for life �Immediate Care Single Premium: $150, 00 �Traditional SPIA (no health review): $210, 162

Those Who Need Care Today �Is there any life insurance in force on the person who needs care? üPermanent life insurance üTerm life insurance üGroup life insurance

Structured Settlement of Existing Life Insurance Policy Convert a death benefit into cash to pay for long-term care Use cash to fund an Immediate Needs Annuity

LTC Insurance Landscape � Stand Alone Long-Term Care � Life Insurance with Long-Term Care Benefits ◦ Ages 40 -65 ◦ Business Owners ◦ ◦ Ages 40 -75 Don’t want “use it or lose it” LTC policy Have assets on the sideline to leverage Can fund with cash value from an existing policy � PPA Compliant LTC Annuities � Immediate Needs Annuity ◦ Age 50 -75 ◦ Won’t health qualify for stand-along LTC or Life + LTC policy ◦ Have existing annuity with low basis ◦ Age 70 -95 ◦ Already receiving care and in poor health

Long Term Care… It’s the Wildcard! • • Is it possible you could live a relatively long life? If so, is it possible you may become frail at some point and need care over a number of years? ◦ What will providing care look like financially, physically and emotionally your family and loved ones? ◦ What plans have you made for this eventuality?

What Are These LTC Numbers? �$9. 23 �$2. 6 Billion Million �$1. 592 Million

LONG TERM CARE IS NOT A PLACE, IT IS AN EVENT PLANNING AHEAD ALLOWS YOU TO MANAGE THAT EVENT FROM A POSITION OF STRENGTH!

Review and Questions