EC 233 International Finance Overview of Course Topics

varies by length of contract, risk, etc.")

• U. S. on gold standard – world")

• Inflation rate at 5000% in 1991 • Adopts")

is Attempting Currency Integration • Only partially there • These are")

•")

")

= 1. 55%, r(France) = 3. 12% (6")

=")

• In absence of trade barriers, differential inflation rates will")

/(1 + if) – 1")

*(1 + (forward – spot)/spot)) – 1 •")

if = 2. 8% Spot =")

")

- Slides: 75

EC 233 – International Finance

Overview of Course • Topics Covered: • Balance of Payments • Currency valuation • Spot and Forward Markets • Supply and demand for currency and valuation • The euro • The East Asian Financial Crisis • Interest Rate Parity • Purchasing Power Parity

• Short-term Financing • Long-term Financing • Direct Foreign Investment • Developing Nation Debt Crisis • How trade is financed

Balance of Payments • Balance of Trade Major Driver of Finance Flows • Deficit = inflows, Surplus = outflows • Begin with Merchandise Trade Account (just goods) Credit Debit -------Export of Goods/Services Import of Goods/Services (currently minus $524 billion)

Balance on Current Account Credit Debit Exports of Goods/Services Unilateral Transfers Abroad Imports of Goods/Services Unilateral Transfers to U. S. Approximately -450 Billion in 2016 =2. 37% of GDP

Relationship Between Trade Deficit and Capital Flows • diagram

Reading Currency Valuations • Cited against a “reserve” currency • Mexican pesos/U. S. $ or $s per Mexican Peso • 18. 5 pesos/$ • Reserve Currencies: • U. S. $, Canadian $, U. K. £, €, ¥, Swiss Franc, Chinese Yuan • Triangular arbitrage: $/£ * £/C$ = $/C$ • If not equal, sets up arbitrage opportunity

Example $1. 20/euro $1. 30/pound 1. 12 euro/pound • Equilibrium: $/euro * euro/pound = $/pound • $1. 20*1. 12 should = $1. 30 (actually = 1. 34) • Not in equilibrium • $1 million example: Buy $1 m worth of Pounds → 0. 769 Pounds→ 0. 923 euro→$1. 034 (3. 4% ROR)

2 nd Example • Yen/$ =110 • C$/$ = 1. 3 • Yen/C$ = 88 • Show not in equilibrium

Currency Forward Markets • Can lock in 30 - 60 - 90 - and 180 -day rates (others if institution willing to sit on other side) • (Why not for years – risk too high) • Forward market – actually want currency (firms) • Options market – can be just attempt to make money • Mechanism: Agree to buy (Call) or sell (Put) currency at a future date • Since it is an option, can just let it expire (lose fee)

• Cost of option (premium cost) varies by length of contract, risk, etc. • If you own a call on a currency, and that currency rises in value, you can sell the option at a profit before the Strike Period • Example: $/£ = 1. 28, buy six month call, assuming that pound will go up in value • • Buy 100 pounds @ $1. 30 (market also assumes pound will rise in value) Pay $. 10 fee for each contract If pound rises to $1. 35 – Make. 05 per pound or $5. But, paid $10 for contract • Only make money if pound rises above $1. 40

If Pound Goes Down in Value • Allow contract to expire, and lose entire $10 • Caps losses off at $10 • Reason puts/calls popular – leverage investment • Only invested $10 to buy $130 worth of pounds • RORs can be very high • If pound went to $1. 45, make 5 cents per pound or $5 on a $10 investment (50% ROR)

Puts are a Bet Against • Investor is bearish on currency • If pound at $1. 28, agree to SELL pounds at $1. 25 • If pound drops further than that, buy at lower price and immediately resell • Once again, fee is sacrificed, so change has to be large enough to offset lost fee • Class exercise: € = $1. 15, buy put on euro at $1. 09 Invest $2000. At end of period, euro is at $1. 02, fee = 4% of total contract

Answer…. • Get $25 out for every dollar put in • $2000 buys $50, 000 worth of euro @$1. 09 = € 45, 872 • Buy at $1. 02 @ end of period, immediately sell at $1. 09 • Make. 07 per euro or $3211. 04 • Take off fee of $2000 = $1211. 04 return on $2000 investment (60. 5%) ROR

Government Influences on Exchange Rates • Two Channels • Intervention by Fed • Direct (ST) • Through interest rates • Government spending • GDP↑ leads to imports↑ which will depress currency • Exchange Rate Policy – e. g. “strong dollar” (2001)

Currency Arrangements Post Bretton Woods (1944) • U. S. on gold standard – world on dollar standard • To get gold from FF: FF->U. S. $->Gold • U. S. dollar fixed at 1/35 oz. of gold • Mechanism: U. S. runs trade deficit ->gold outflow->U. S. money supply↓->Fall in U. S. GDP->Imports↓ • Adjustment on REAL side • Became unstable in early 1970 s due to spending on Vietnam War • Smithsonian Agreement (1971) devalued dollar (1/42 oz. of gold) • System collapsed completely in 1973 – exchange rates floated

Since 1973, Numerous “Regimes” • Fixed, floating, hard peg, soft peg, pegged to a basket, pegged to a non-currency (SDR), crawling peg, etc. • Some highly unstable (soft pegging) • Hard peg ties nation’s currency to another • Along for the ride • May over-value or under-value currency • Crawling peg graph

Pegged to a Basket – Why significant • Should reduce variability • Since currencies don’t move perfectly together • One currency ↑ while other ↓ • offsetting

Innovations • Bartering: China and Australia • Avoid use of any currency • Commodity Money • Currency “buys” a package of commodities • If value of commodities ↑, commodities worth more than currency – trade in currency to get commodities, forcing price of commodities back down • And vice-versa

Currency Board (Argentina 1992 -2001) • Inflation rate at 5000% in 1991 • Adopts dollar as “currency” • To print a peso, must obtain a $ (1: 1 ratio) • Inflation immediately dropped to just over 10% • Cannot have monetary policy under this system • By 2000, every government action dictated by need to maintain one: one ratio • Exited currency board during deep recession (needed monetary policy)

Full Dollarization • Ecuador, Panama • U. S. Dollar is legal tender • No domestic currency (except coinage in Ecuador) • Monetary policy run by Federal Reserve • Provide stability, but (again) no monetary policy

Currency Integration – The euro • No real corollary to the euro • Replaced 17 currencies by one • Forced coordination of monetary policy • Agreed to limits on fiscal policy – violated extensively • Introduced in 1999 a Unit of Account • Became full currency in 2002 • All other currencies removed from circulation my April 2002 • Will cover euro in detail later in course

Caribbean Community (CARICOM) is Attempting Currency Integration • Only partially there • These are tiny economies – risk much smaller and process much easier • No other integration movements have attempted a common currency • Even ambitious movements (e. g. Mercosur)

Innovative Disasters - Venezuela • Four different currency values • Rate 1: 6. 5 Bolivars/dollar (importation of food and medicine) • Rate 2: 12/$ and 50/$ for importation of other goods – rate available only sporadically through an auction process • Newest rate: 200/$ -> for purchase and sale of foreign currency to individuals and businesses • System impossible to navigate – in the presence of 800% inflation, value of Bolivar will continue to deteriorate

The Asian Financial Crisis • Timeline • Causes • Resolution and Impacts • Abandonment of soft pegging

Euro Week • Began with Maastricht Treaty • Created EU (rather than EC) • Movement towards deeper integration, including common currency • Eventual single state • Dates: • Unit of Exchange 1999 • Full Currency 2002

Euro Conversion Rates Currency Units of national currency for € 1 Belgian franc 40. 3399 Deutsche Mark 1. 95583 Spanish peseta 166. 386 French franc 6. 55957 Irish pound 0. 787564 Italian lira 1936. 27 Luxembourg franc 40. 3399 Dutch guilder 2. 20371 Austrian schilling 13. 7603 Portuguese escudo 200. 482 Finnish markka 5. 94573

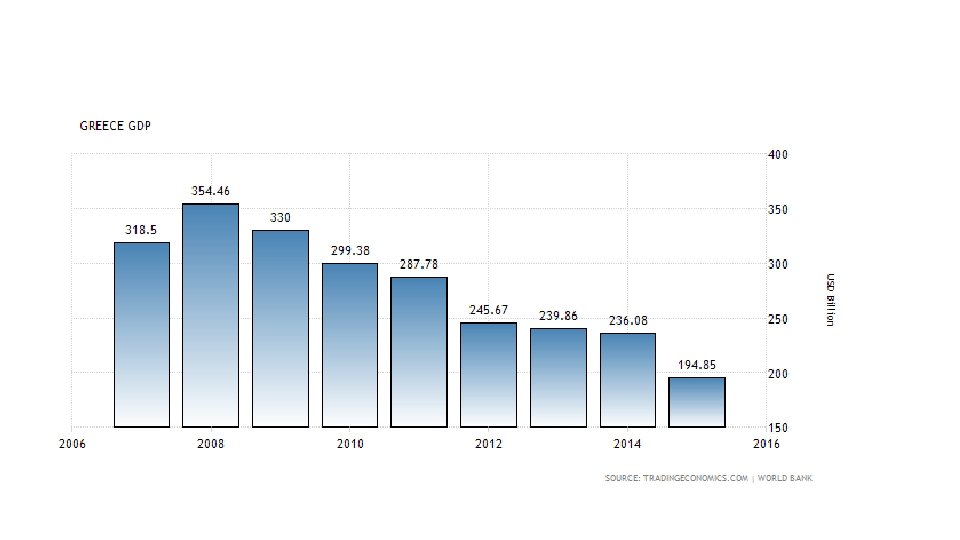

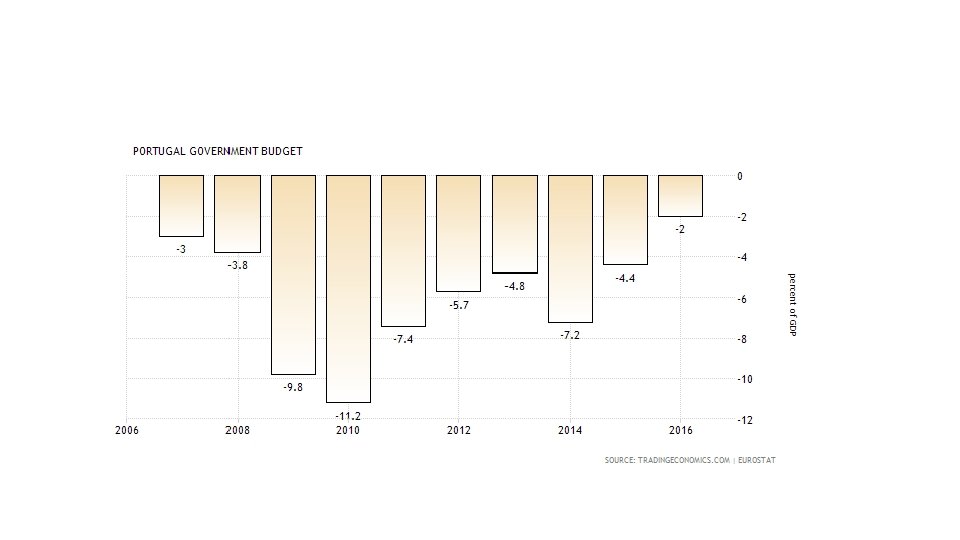

Conditions for Entry • Debt and deficit caps • With penalties – openly violated • Resulted in Greek Tragedy • Note that certain countries (UK, Denmark, Sweden) never entered Eurozone • Remained in EU, however • Additional problem for common currency

Problem with Conditions for Entry • “Eliminated” fiscal Policy if followed • Recession = fall in government revenue • Would then have to cut spending during a recession? ? ? • That would lead to lower gdp and lower tax revenue, which would force further cuts • Keynsian death spiral • Instead, governments ignored • What about monetary policy?

No Real Corollary to Currency Integration • U. S. Free Banking Era (? )

What are Benefits of a Common Currency? • Elimination of currency transaction costs • Transparency • Know what things cost where • Helped further integrate trade between EU nations

Why the Crisis? • Failure to follow debt/deficit guidelines • 60% debt/gdp ratio, 3% deficit/gdp ratio

Resulted in Financial Crises in So-Called PIIGS • Portugal, Ireland, Italy, Greece, Spain • Ireland partly due to real estate speculation • Most have been able to recover – Greece will not recover, possibly ever. • Should have exited EMU

Interest Rate Parity • Covered Interest Arbitrage • Relationship between interest rates and exchange rates • Derivation • p = (1 + ih)/(1 + if) - 1

Examples • What is predicted forward value of £, $/£ = $1. 30 U. S. r = 1. 7% (6 month) GB r = 3. 4% (6 month) p = (1. 017)/(1. 034) – 1 = -0. 01644 $1. 279 = predicted forward value – if not equal to actual forward rate, profit opportunity

IRP Line and Graph

Numerical Example • Let r (US) = 1. 55%, r(France) = 3. 12% (6 month) • $/€ = 1. 14 • What is predicted forward rate of $/€ if IRP holds? • Prove that the ROR is same in both France and the US if IRP holds – use a $1 million investment

Example 2 • If C$/$ = 1. 28 • Interest rate (3 month) = 1. 05 (US), 2. 20 (Canada) • Find predicted value of C$/$ and prove that a $5 million investment returns the same amount in both Canada and the U. S. if IRP holds

Purchasing Power Parity (PPP) • In absence of trade barriers, differential inflation rates will result in offsetting changes in exchange rates • Only works for “tradeables” • Therefor, weaker for U. S. , since economy is not that open • Also called Law of One Price • Reasoning: easier for exchange to move than for goods to move • Forces that get in the way: trade barriers, distance, consumer tastes, product differences, etc.

• Derivation…. . • e = (1 + ih)/(1 + if) – 1 • Example: Note, not limited to six month horizon • ih = 7%, if = 3% • 3. 88% - home currency will rise in value by 3. 88% • Example 2: ih = 6%, if = 2%

Article on PPP

Graph

Direct Foreign Investment • Long-term movement of capital • New investment, purchase of existing firms and real estate purchases • Examples: • Korean auto transplants (Hyundai) • Purchases of west coast real estate by Japanese • Acquisition of U. S. businesses by European firms (Chrysler-Fiat)

Advantages and Disadvantages to Target Country • Jobs, utilization of local resources • History of Japanese auto transplants – from assemblers to full production • “Extraction” of profits • Common criticism of DFI in developing nations • Fallacious assertion – money was not there before • Profits are a small proportion of total expenditures • Political Influence

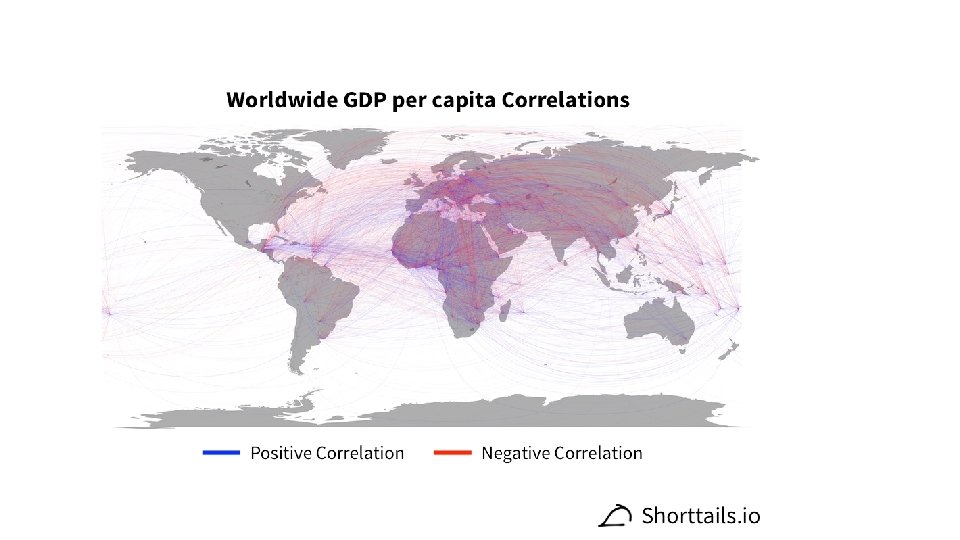

Reasons Behind DFI • Search for cheap inputs, primarily labor • Circumventing a trade barrier • Japanese avoided US VER on cars by building in the US • • • Access to a natural resource (e. g. petroleum) Reducing transportation costs New sources of demand Reacting to exchange rate movements International economies of scale (graph) GDP correlations • Used to be more significant when US economy drove world • GDP correlations now higher • Examples

Country Risk Analysis • Financial, Political, Repayment • Fundamental part of decision to invest overseas

Article on DFI

Short-Term Financing • Purposes • Cover receivables • Project financing • Cash flow mismatch • Could be bank loans or commercial paper

Multinationals can Borrow at Home or Overseas • Cost of borrowing complicated by exchange rate • If borrow overseas…. . • Value of foreign currency up, pay back in more expensive “dollars” • Value of foreign currency down – pay back in cheaper “dollars” • Could lock in value – makes transactions more expensive

Formula Cost of Financing = (1+ rf)*(1 + (forward – spot)/spot)) – 1 • Example: • Let rf = 2. 7% (3 month) • ih = 3. 6% • F = $1. 15/€ • Spot = $1. 11/€ Cost of Financing = (1. 027) * (1 + (1. 15 -1. 12)/1. 12)) – 1 = 1. 027*1. 0446 -1=7. 28%

Example 2 ih = 1. 9% (6 month) if = 2. 8% Spot = $1. 30/£ Forward = $1. 25/£

Generalization • If foreign currency going up in value, foreign financing is expensive • And vice-versa

Long-Term Financing • Review of Present Value analysis • Time Value of Money • Simple Example Cost = $5 million (Year 0) Returns = $3 million, $2 million and $2 million Discount Rate = 6%

Complicated by Exchange Rate Considerations • Appreciating currency makes repatriated money worth more • Firms that operate internationally have to take this into consideration

Example • Building small factory in Spain or U. S. • Expense = $20 million or € 17. 86 m (at $1. 12/euro) • Returns are $5 million in first year, $10 million in year 2 and $10 million in year 3. • Expected value of euro: $1. 15 (1), $1. 18 (2) and $1. 22 (3) • Discount rate in U. S. = 4%, discount rate in Spain = 5% • Evaluate both projects

Second Problem

Other Aspects of Present Value Analysis • Decision Trees • Sensitivity Analysis • Contingent Projects

International Debt Crisis of 1980 s • Causes • Falling growth rates • Rising interest rates • Collapsing commodity prices • Recycling of petro-dollars • Infrastructure spending • Capital flight – replaced by borrowing

Numbers…….

Initial Reactions • Printing money • Export Controls • Moratorium (Peru)

Results • Crisis in U. S. banking system • Bad debt had been widely injecting into U. S. banks, even small ones Inflationary crisis in Latin American nations • 5, 000% inflation in Argentina • 50, 000% in Bolivia

Attempted Solutions • Import restrictions • Debt-Equity swaps • Debt for Rain Forest

Intervention of IMF • Provided loans to keep nations from defaulting • Bundled packages of funds from World Bank, Development Banks, IMF, etc. • Imposed “Conditionality” • Cut government spending and number of government workers • Reduce trade barriers • Monetary restraint • Etc.

• Deeply resented • Argentina did not officially end its dependence on foreign borrowing until 2 years ago • “debt forgiveness” became the rallying cry • Highly Indebted Poor Countries (HIPC) initiative

Payments Methods and International Trade • 5 standard means of payment arrangements • Payment in Advance • Letter of Credit • Sight/Time Draft • Consignment • Open Account

Letter of Credit • Diagram • Most common form of trade for small- to mediumsized firms

Sight/Time Draft

Financing Techniques • Accounts Receivable • Factoring • Letter of Credit • Counter-Trade

Examples of Counter-Trade • Most famous: Pepsi for Stolychnaya Vodka • Reason: Russian Ruble valueless • Could not bill Russian importer • Algeria (Natural Gas)→France • France (Fertilizer)→Algeria • Reason: Algeria had insufficient foreign reserves • China/Australia now trade without reserve currency • Essentially barter