CCI Entrepreneurship Curriculum Module 8 Core Financial and

Cash Flow")

")

from")

2010 Sales")

2010 2009 Change Percentage Cash € 29, 000 €")

- Slides: 74

CCI Entrepreneurship Curriculum Module 8 - Core Financial and Accounting Management Skills

Learning Outcomes v Understand profit and cost analysis and break even analysis; v Understand investing, borrowing and alternative sources of funding and their advantages and disadvantages; v Understand the finance management and planning, learning how they can access to different forms of finance; v Use the language of business and finance.

Module 8 - Overview v Unit 1 - Decoding the jargon – introduction to economic and financial terminology, and Financial Statements v Unit 2 - Introduction to financial management tools for managing financial resources, cost accounting, bookkeeping, cashflow management, breakeven point, cost management and credit control v Closing Session and Evaluation

Mapping to the Business Canvas Where do you think the What you will Learn fits in your Business model canvas – This is not your business plan, it is a path to success.

Unit 1 – Decoding the Jargon – Introduction to Economic and Financial Terminology

Introduction How we use finance in our start-up? v What is Finance? Finance describes the management, creation and study of money, banking, credit, investments, assets and liabilities that make up financial systems, as well as the study of those financial instruments. v How does this relate to you? Through finance you will be able to access different financial instruments. These instruments may enable your idea to have the means to grow

Introduction Why is accounting useful for? v What accountants do? An accountant performs financial functions related to the collection, accuracy, recording, analysis and presentation of a business, organization or company's financial operations. By law, nations require businesses to have accountants audit their annual financial statements. v How do we benefit form accounting information? All stakeholders benefit, first by trusting financial Statements!

Decoding the Jargon Financial Statements v v Balance Sheet Income Statement (P&L) Cash Flow Statement Financial Ratios Very important words to know v Assets and liabilities v Equity Financing products & markets v v Shares & Bonds, Types of Bank loans Stock Market Business Angels & Venture capital v Crowdfunding

Over to You! Reading One Reading Two • Which 3 terms you have heard or you just read that you would like to now more about? 1) … 2) … 3) … • Which 3 terms you have heard or you just read that you would like to now more about? 1)… 2). . . 3)…

Unit 2 – Introduction to Financial Statements

Financial Statements Accounting Cycle simplified Economics Events 31/12/2017 1/1/2017 Financial Statements: 1. Profit or Loss and other comprehensive income 2. Statement of Change in Equity 3. Statement of Financial Position 4. Cash Flow statement 5. Notes

Accounting and Financial Statements The key Accounting Statements are: v Profit Statements (Income Statements) v Balance Sheets v Cash Flow Statements

Financial Vs. Management Accounts v The financial accounts are those you produce annually for revenue, a legal requirement. v Management accounts are optional, can be produced monthly, weekly or quarterly and the purpose is primarily to provide good timely information to management on the company performance to make appropriate decisions about the business. v In times of tight credit, management accounts are increasingly a necessity: the bank and other funders such as state agencies will demand up to date information about the company’s financial position. The last set of accounts will be simply too old.

Financial Vs Management Accounts v Financial accounts must be prepared in line with agreed legal accounting standards. v Management accounts are less legally constrained, but will typically be more detailed as you seek to know which of your products, customers or markets is actually delivering profit. v Such detail is not allowed outside the company for competition reasons, the bank should get total numbers only

Profit & Loss Terms v Sales/ Turnover – income from the sales of products during the period (excluding VAT if the business is VAT registered) v Cost of Sales /direct costs / variable costs – costs that can be directly attributed to the production of a particular product or sale of an item e. g. in the manufacture of a table, the cost of sales will be the cost of raw materials (wood, glue, tools, machine hire) that goes into each table. v Gross Profit / contribution – difference between sales income (turnover) and the cost of sales. v Administration expenses / overheads / fixed costs – covers all operating costs not directly linked to producing a product e. g. rent, utilities, insurance and staff costs (not included in cost of sales) v Profit – difference between the income of your business and its expenses

Profit & Loss Account v My Craft Business v Profit & Loss Account Year End 31 st March 2015 Sales Turnover Less Cost of Sales Gross Profit Administrative Expenses Operating Profit 45, 000 (15, 000) 30, 000 (20, 000) 10, 000

Financial Statements - Profit and Loss Sales Cost of Sales Gross Profit Overheads Operating Profit Pre-tax Profit Post-tax Profit Retained Profit Interest Tax Dividends

P&L vs. Cash v The P&L Account does not show cash flow, which is shown in the Cash Flow Statement. v P&L revenues reflected do not reflect actual CASH receipts v P&L costs do not reflect the actual amount of CASH paid in a given period, because of the accrual principle

P&L: Capital vs. Expense Capital Expenditure v. Expenditure incurred in creating, acquiring, extending or improving an asset for use in the business v. Generates benefits over several accounting periods v. Capital expenditures appear on the balance sheet as a fixed asset - i. e. expense is capitalised

P&L: Capital vs. Expense Revenue Expenditure v. Expenditure incurred in earning revenue or maintaining earning capacity of business v. Benefit used up in current accounting period v. Expense is “written off” and appears in P&L as a cost

Key messages from the P&L v Is turnover growing? v How well re we managing product direct costs (benchmark your gross margin vs. competition) v Overhead cost management – staff and other overhead costs as % of sales v Marketing spend – Are we spending more than we should be on advertising without getting value for money?

Balance Sheet Fixed Assets Shareholder Funds Current Assets Long Term Liabilities • Buildings • Equipment • Cars • Stock • Cash • Debtors • Money you invested • Profits reinvested • Bank loans, Grants Current Liabilities • Creditors Total Assets = Total Liabilities.

Balance Sheet v A “Snapshot” of the business at a particular moment in time v Shows Assets (what is owned), liabilities (what is owed by the company), and Shareholders funds v Total Assets = Total Liabilities. v The total liabilities represents the sources of finance used to fund the assets used

Key Messages from a Balance Sheet v What assets does the business have v. Are assets being used effectively? v. Are assets being replaced and maintained? v How are the assets financed? v. Does the business have a high level of debt? v. Is the business slow to pay suppliers, hence overusing suppliers as a source of financing? v. How much equity do the owners have in the business

Balance Sheet: Definitions v Fixed Assets - assets which remain on the balance sheet for more than one year v. For example, land, buildings, vehicles which are not written off within the next year v Current Assets - assets which are written off within the next year, or which will leave the company within the next year v. For example, computer equipment which is written off in the first year, materials for production

Balance Sheet: Definitions v Current Liabilities - liabilities which must be paid within one year v. For example Short Term Debts, bills payable to trade suppliers v Long Term Liabilities- liabilities not due within the next year v. For example long term bank debt v Share Holders Funds v. Equity invested, retained profits, share premium

Balance Sheet: Shortcomings v Reflects assets at cost or written down cost only ignores market value v Ignores intangible assets other than Goodwill, e. g. R&D, brands, people, market position etc.

Cash Flow Statement v Where has all the money gone? v This statement simply shows cash in and out, and a simple analysis of where the cash came from / went v This is the single most important statement from a viability perspective

Key Messages from CF Statement v The most important aspect of the cash flow statements is that it tells you where your money came from (or disappeared to) under 3 key headings: – Net Cash flow from operations, i. e. from selling what you sell after covering all related expenses – Cash flow from/ to investment – i. e. from buying or selling long term assets – Cash flow to/ from financing activities – i. e. through raising money from the outside world or paying off debts

Key Messages from CF Statement v The really crucial element is cash flow from operations v If your cash is down because you just bought machinery that is temporarily challenging but not fundamental worrying v If you are burning cash in operations that is fatal (only exception is pre commercialisation start up scenario)

Key Questions Using all 3 Statements v Is the business generating enough profit for the owners to justify the capital invested? v Is the business generating enough cash flow from operations to comfortably service the debt? v Is the business generating enough cash flow from operations to maintain the fixed asset base – i. e. replace aging equipment? v Is the business generating enough cash flow to expand without recourse to external funding?

When to Request External Finance v One has to decide how much external finance is required Part of the Business Plan (“Key Resources” on the Canvas) v There are basically three main situations for bank financing: v. Starting up a new business v. Buying a business v. Expanding an existing business v Decide what type of finance is needed for each type of asset need v Be careful: Matching finance with assets is important in order not to have negative repercussions.

What is a Financier looking for? The principles of lending a bank considers before deciding whether to grant a loan or not, include: v Purpose v Amount v Repayment v Term v Integrity v Security - legal purpose? What is the loan for? - correct amount needed for such purpose - how will the loan be repaid, from what sources, examine P&L , CF, income &expenditures - when the loan will be repaid (LT-the riskiest) - is the customer trustworthy? - what is the security, guarantee of the repayment (the second way out? Should be very liquid)

The Bank View of Lending v Pays attention to gearing ratios (balance between equity and debt finance). v The higher the gearing , the higher the interest rate, the higher the default risk. v Dividend vs. interest payment ? v Credit scoring v Pays attention to the business plan (CF, audits)

Types of Bank Finance v. Overdraft v. Credit cards v. Loans v. Commercial Mortgages v. Hire Purchase / Leasing of machinery and vehicles v. Factoring of debtors v. Venture capital (and other equity finance (Initial Public Offering, Partner, Friend and Family etc. ) v There are other more complicated types of finance – a good advice is to fully understand what you a signing up to before you enter in any obligation!

Economic and Financial Terminology Financing products& markets • Funds Types by tenor: • • • Shares & Bonds, Types of Bank loans Stock Market Business Angels& Venture capital Crowdfunding

Security v Most lending needs security. v The more security one has the better the terms of repayment v Types of Security – A mortgage over property/premises – Mortgage on company’s assets (debenture) or a ‘fixed and floating charge’ A guarantee (LG, a third party guarantee) – Assignment of receivables – Pledge on Inventory/stock and shares – Life policies of partners – Letter of Comfort – Bank Guarantee – Personal Guarantee – Warrant

Financial Repercussions Understand that different types of financing have different repercussions on your company: v If you take a loan: • You have to repay the loan in a monthly or yearly basis or you might loose your security v If you raise equity: • By giving ownership of part of your company you do not have to repay in a monthly or yearly basis but you might affect who can make decisions for the company v Loans and giving equity also change how much tax you might pay! • Do ask for the tax repercussions as part of any agreement Source: Certified Manager textbook

Summary of Lending Services

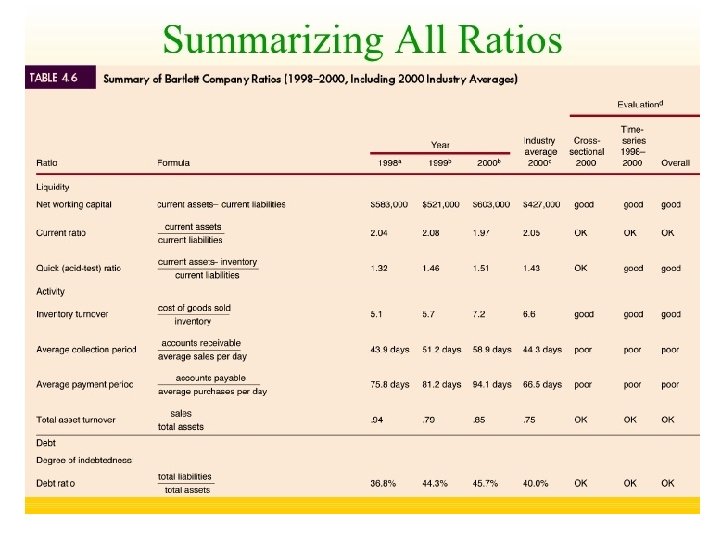

Before we finish Unit 2, we want to look at financial ratios

What are financial ratios? Financial Statements v Financial Ratios v Most powerful indicator of financial health, a combination of data from the same of across financial statements, useful in forecasting. v They are based on categories and provide a faster insight on the company health and potential performance and soundness expectations. v Please see example in the next page Source: https: //image. slidesharecdn. com/financial-ratioanalysis 2674/95/financial-ratio-analysis-31 -728. jpg? cb=1275459605

Unit 3 – Introduction to Accounting

Introduction to Accounting v Accounting and Finance are not just useful talk to Financiers v They are necessary for the effective management of your company. v Managerial accounting emphasizes how the use of such methods can aid the effective management of your company.

How to use Accounting Data to lead to better Decision-making v A useful way in understanding what is going on is to compare years and calculate the percentage change between different variables (gross operating profit, Sales etc. ) v This can be useful to track where things changed over the course of a financial year. v We will work with Some financial Statements to see how your can use them to learn about your business

Case study: The case of Advertorial PLC, a local Advertising company v In this fictitious case study an small Advertising company is looking to see how can finance, economics and accounting can help them become more effective. v Using this case study we will see a range of ways that the company can use to understand what is going on. v We start by understanding how growth rates can help us analyze the shape of a company v VERY IMPORTANT. All methods can only be as good as the data. So if the reported data are wrong, or fraudulent or poorly recorded, one will not get the results that will aid her or him to manage his company better

Calculating Percentage Change Over Time Step 1 - Calculate the change (absolute value) from 2009 to 2010. Step 2 – Divide the amount you found in step 2 with the sales of the previous period. In this case 2009 is our previous (i. e. base period) Now you have a percentage change of sales. Useful to track changes in sales, costs and revenues over time. Increase (Decrease) 2010 Sales revenue € 858, 000 2009 Amount Percentage € 803, 000 € 55, 000 6. 8% € 858, 000 – € 803, 000 = € 55, 000 Amount / Base Year = Percentage 55, 000 / € 803, 000 = 6. 8

Comparative Income Statements For the Years Ended 2010 and 2009 Increase (Decrease) 2010 Sales revenue Cost of goods sold Gross profit Operating expenses Operating income Interest expense Income before income taxes Income tax expense Net income 2009 € 858, 000 € 803, 000 513, 000 509, 000 345, 000 294, 000 244, 000 237, 000 101, 000 57, 000 20, 000 14, 000 Change Percentage € 55, 000 4, 000 51, 000 7, 000 44, 000 6. 8% 0. 8% 17. 3% 3. 0% 77. 2% 42. 9% 81, 000 43, 000 38, 000 88. 4% 33, 000 € 48, 000 17, 000 € 26, 000 16, 000 € 22, 000 94. 1% 84. 6%

Comparative Balance Sheet Increase (Decrease) 2010 2009 Change Percentage Cash € 29, 000 € 32, 000 (3, 000) (9. 4%) Accounts receivables, net 114, 000 85, 000 29, 000 34. 1% Inventory 113, 000 111, 000 2, 000 1. 8% Other current assets 6, 000 8, 000 (2, 000) (25. 0%) Total current assets 262, 000 236, 000 26, 000 11. 0% Property, plant, and equipment, net 507, 000 399, 000 108, 000 27. 1% Assets Current assets: Other noncurrent assets Total assets 18, 000 € 787, 000 9, 000 100. 0% € 644, 000 143, 000 22. 2%

Comparative Balance Sheet Liabilities Current liabilities: 2010 2009 Change Percentage Accounts payable Notes payable € 73, 000 42, 000 € 68, 000 27, 000 5, 000 15, 000 7. 4% 55. 6% Accrued liabilities 27, 000 31, 000 (4, 000) (12. 9%) Total current liabilities Long-term liabilities 142, 000 289, 000 126, 000 198, 000 16, 000 91, 000 12. 7% 46. 0% Total Liabilities 431, 000 324, 000 107, 000 33. 0% Common stock 186, 000 0 0. 0% Retained earnings 170, 000 134, 000 36, 000 26. 9% Total stockholders’ equity 356, 000 320, 000 36, 000 11. 3% Total liabilities and equity € 787, 000 € 644, 000 143, 000 22. 2% Stockholders’ Equity 50

Trend Percentages v Indicates the direction a business is taking over a longer period of time, such as three to ten years. 2010 Sales revenue Trend percentage 2009 € 858, 000 € 780, 000 143% 130% 2008 € 690, 000 115% 2007 2006 € 648, 000 € 618, 000 108% 103% Base Year 2005 € 600, 000 100% v Trend percentages are computed by selecting a base year. v The base-year amounts are set equal to 100%. v The amounts for each following year are expressed as a percentage of the base amount. To compute trend percentages, divide each item for following years by the base-year amount.

Red Flags in Financial Statement Analysis v Movement of sales, inventory, and receivables v Earnings problems v Too much debt v Inability to collect receivables v Inventory buildup 52

Forecasting with Financial Statements v Why Forecast? v Designing Good Forecasting Systems v Key steps and information needed to construct and monitor a Forecast v Forecasting on both cash and profit basis – why do we need both? v Using key performance indicators as part of your planning system

Why Forecast? Motivation Information for external Stakeholders Efficient Use of Resources Forecast Benefits Control Discretionary Spend Coordination Planning

Good Forecast Systems Ownership and Accountability Realistic Good Forecast Systems Top down AND bottom up Multiple Scenarios Well communicated Effective Monitoring and Reporting Systems Flexible

Information Needs v Historic Information v. Internal costs by product and period v. Historic Volumes, and how these were affected by external factors v. A good historic management accounting system is one of your most powerful tools for a good forecasting system

Information Needs v Future Information: v. Internal costs factors v. Resource requirements v. Market trends v. Customer data v. Competitor strategies and resources v. Regulations v. Substitutes v. Supplier information

KPIs to drive your planning process v Your forecast should focus on the key financial targets you are seeking to achieve. Then ask yourself what you need to do to achieve this? v Reality will intercede, but it is important to set clear goals and objectives and work toward these rather than simply drift with the flow

Cash Flow Management v The art of not running out of cash v A combination of: v. Good pricing v. Tight cost management v. Keep costs flexible by minimising fixed costs v. Pulling in cash from customers quickly v. Managing very tight stocks v. Sensible use of supplier credit v. Maintaining good relations with the bank

Cash flow Forecasting v Cashflow forecasts are a pre-requisite for business success v Cash is the life-blood of any business v Cash Flow forecasting enables you to plan for: – How much cash your business will need to keep trading(going) – The timing of when it will be needed – Additional finance application if there is going to be a shortfall – Managing surplus funds – Regulate spending – Draw attention to waste / inefficiency

Cashflow Template Month of Year INCOME Received from Cash Sales Cashflow Template 1 Oct 2 Nov 3 Dec 4 Jan 5 Feb 6 Mar 7 Apr 8 May 9 Jun 10 Jul 11 Aug 12 Sep (A) TOTAL EXPENDITURE Materials Wages & N I Rent & Rates Tele, Stationery & Post Advertising & Promotion Heat & Power Travel/fuel Audit & Accountancy Insurance Framing Sundries Events Drawings (B) TOTAL 0 0 0 (C) Working Monthly Cap 0 0 0 (D) Cum Working Cap 0 0 0 CASH INTRODUCED Own Investment Loans Grants (E) TOTAL 0 0 0 CAPTIAL EXPENDITURE Premises Machinery/Equipment Vehicles HP Loan Repayment (F) TOTAL 0 0 0 (G) MONTHLY BALANCE 0 0 0 (H) OPENING BALANCE 0 0 0 (J) CLOSING BALANCE 0 0 0 TOTAL 0 0 0 0 0 0 0 0

Break Even Calculation Example: • Break even calculation

Testing: Break Even Suppose you have the following Business, calculate the Break even! Solution: • Information given: • Average Doll Sell price € 12, Raw Materials are € 4, Production labour € 8/hour, 15 min for each doll. • Salaries= € 2500/week, Insurance= € 1200/quarter, Rent= € 1500/month, Utilities= € 800/month. • Price per doll= € 12 Var Cost per doll=(8/4)+4= € 6 • Fix Costs per month= (2500*4)+(1200/4)+1500+8 00= € 12, 600. • =>BEQ=FC/(P-VC) • € 12, 600/(12 -6)= 2100 Dolls per month. • BE Sales must be 2100 x 12= € 25, 200 per month.

Cost Management v Good cost data is your first step to manage costs v Benchmark where possible against comparable firms. v. This can be difficult for SMEs as data on competitors who are also SMEs is scant due to limited disclosure requirements.

Cost Management v Know how your costs behave – Fixed costs V’s Variable costs. – Maintaining flexibility by avoiding fixed costs v Good cost measurement systems are – A prerequisite to good cost reduction strategies.

Think Outside the Box v Buying your equipment second hand v Barter your services/ product with another SME v Find cleverer ways of eliminating printing by better use of electronic communication. v Find more cost effective ways to promote your product / service

Cautionary Considerations v Don’t cut costs – at the expense of future growth – Discretionary costs Vs. non discretionary costs. – at the expense of quality v Negotiate costs up front, – ideally on a fixed and defined basis – Try multiple providers if you can v Don’t get Carried away by Volume Discounts – Tying up cash in stock can put you out of business

Avoid Fixed Costs where Possible Minimise Fixed Costs v If at all possible keep your fixed costs low. Fixed costs are the ones that don’t go away when volume of work drops v Keeping these low means that you can handle volume fluctuations without hitting the wall. v It also allows you to enter new business activities and withdraw without incurring huge costs

Credit Control v Traditionally most SMEs relied on rating agencies, banks, other customers, word of mouth etc. to do credit assessments on potential clients v Recent events and current situation suggests that is probably not enough – develop your own analysis skills v For new customers look at financial accounts and if in doubt charge cash

Credit Control v Consider offering a discount if necessary to avoid issuing credit until a relationship has been established. v Discounts can be expensive but tend to dramatically reduce bad debt risks v Direct Debit Payment systems are also becoming increasingly accepted in many sector

Quoting Price v When quoting price keep the product and service delivery as defined as possible v Any change in spec or additional features will entail extra costs, and you should charge for this v Precision in the quote leaves you in a strong position to charge more if the client looks for extras.

Invoicing: Simple Rules v Ensure proof of purchase before delivery – email is enough, but P. O. better v Invoice immediately when you deliver v State credit terms clearly at contract stage v Draft standard terms and conditions – send these to the customer before you deliver. If they do not contest they are binding if reasonable.

Collecting the Money: Simple rules v Collect punctually, promptly and firmly. Most clients will require a bit of gentle prompting v Interest penalties are now due under law, but few companies have the nerve to impose these. However with certain customers it may be useful to quote the law… v Don’t let collections fall behind! Get short term resources in if necessary to clear collection back logs

Summary What we covered? How we use it? v Unit 1 - Decoding the jargon • ………………… v Unit 2 – Introduction to Financial Statements • . . . v Unit 3 - Introduction to financial management tools for managing financial resources, cost accounting, bookkeeping and breakeven point • …………………