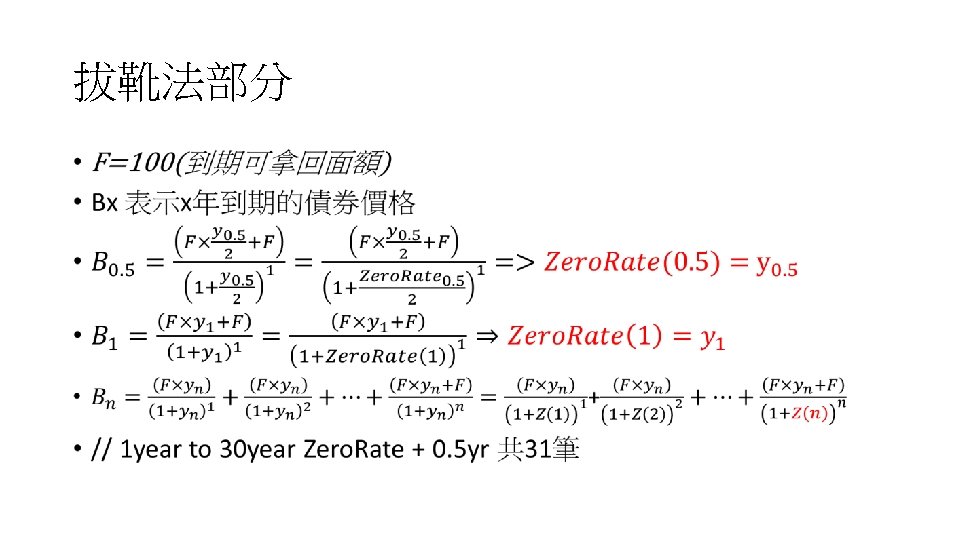

Bullet Bond Hull White model Yield rate Bloomberg

Bullet Bond & Hull White model

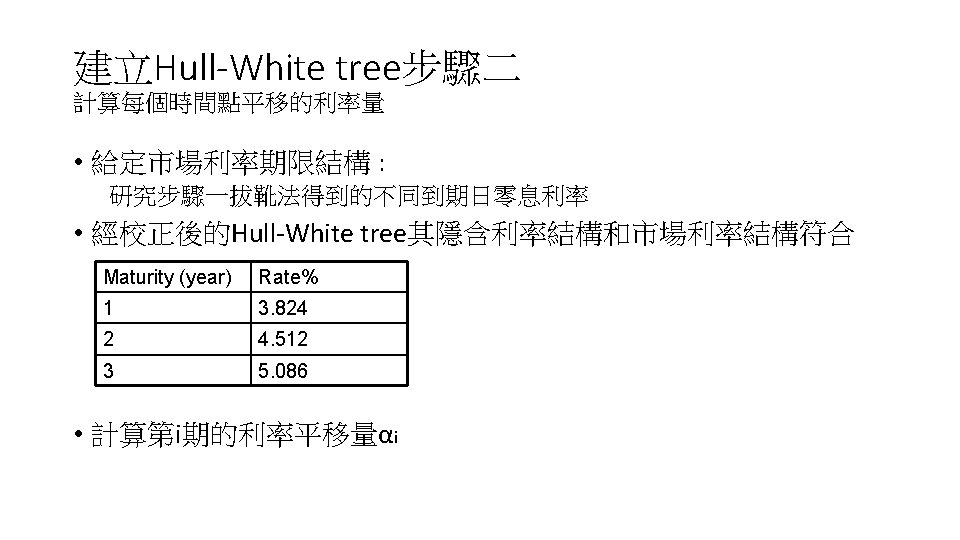

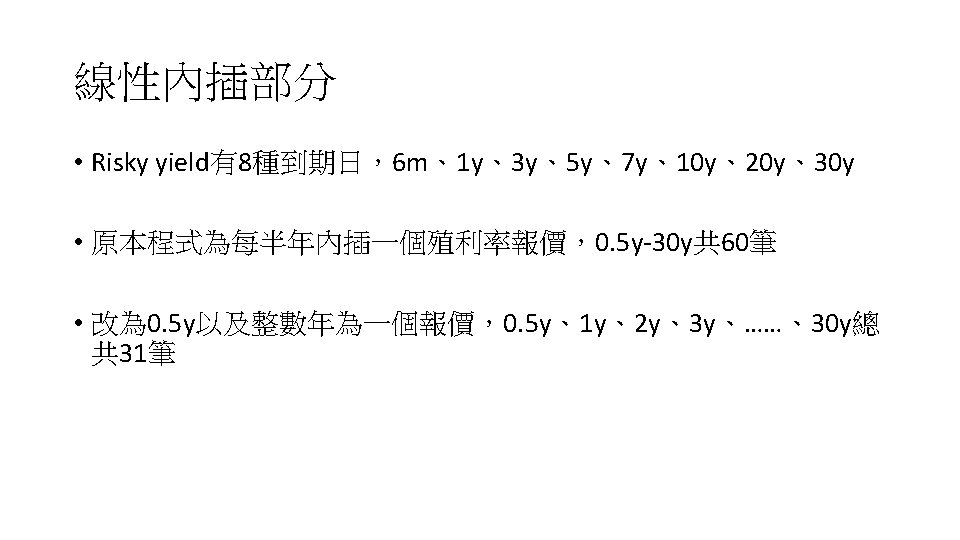

Yield rate • 從Bloomberg 得到 • Risky yield 部分只有 6 M 1 Y 3 Y 5 Y 7 Y 10 Y 20 Y 30 Y 八筆 • 線性內插成 60筆yield (0. 5 Y , 1 Y, 1. 5 Y, 2. 5 Y, ……, 29. 5 Y , 30 Y) 用void linear(double *Yield, double *Data)

")

Zero Rate • 用線性內插法得來的60筆yield rate bootstrap出 60筆零息利率 void bootstrap(double *Zero. Curve, double *Raw. Data)

Bootstrap

• struct date • int year; • int month;")

Day count (t to T) • struct date • int year; • int month; • int day; • double Cal_day(date &date 1, date &date 2) • 比方 2017/8/15 到 2045/2/3

• 抓最接近的index來內插 • 比如T-t =27. 4666666 • 找Zerorate 27. 5年與Zerorate 27年來內插")

Zero. Rate(T-t) • 抓最接近的index來內插 • 比如T-t =27. 4666666 • 找Zerorate 27. 5年與Zerorate 27年來內插

^30*exp(-Zerorate*(T-t))")

Bond price • Bullet bond price = par*(1+implied_r)^30*exp(-Zerorate*(T-t))

Call schedule 舉例

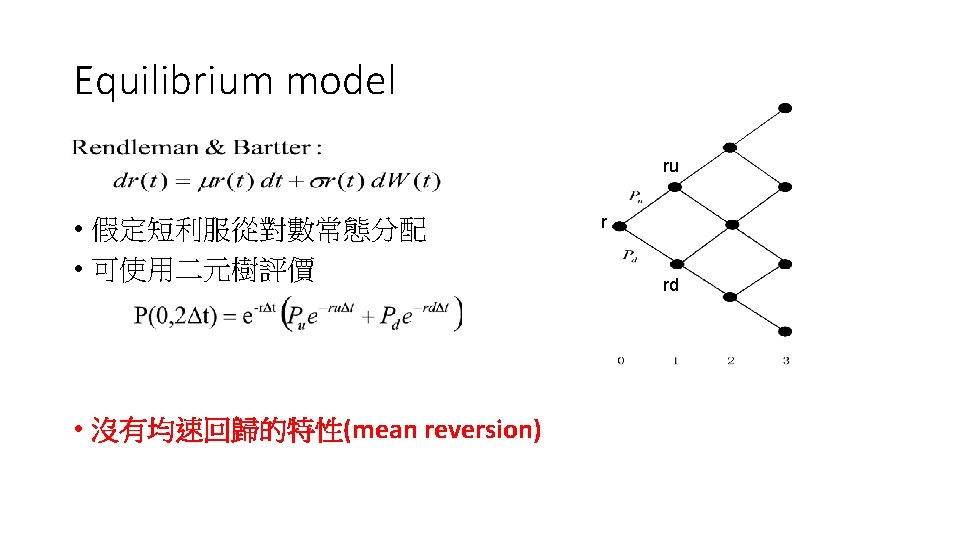

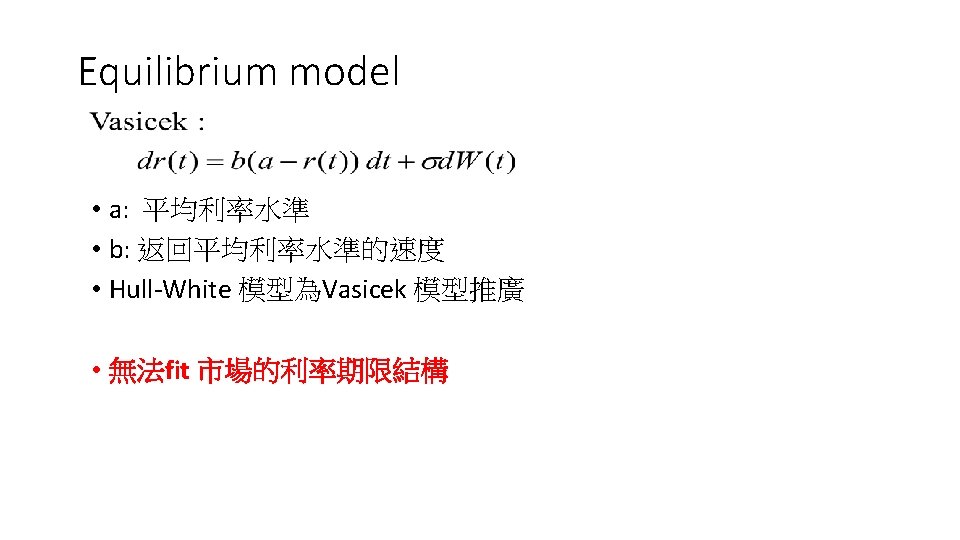

短利模型的種類 • Equilibrium model: • • 對經濟模型做出假設, 進而推出短利的隨機過程 短利隨機過程決定 決定利率期限結構 Rendleman & Bartter model Vasicek model Hull-White model為其推廣 • No arbitrage model: • 通常為Equilibrium model的推廣

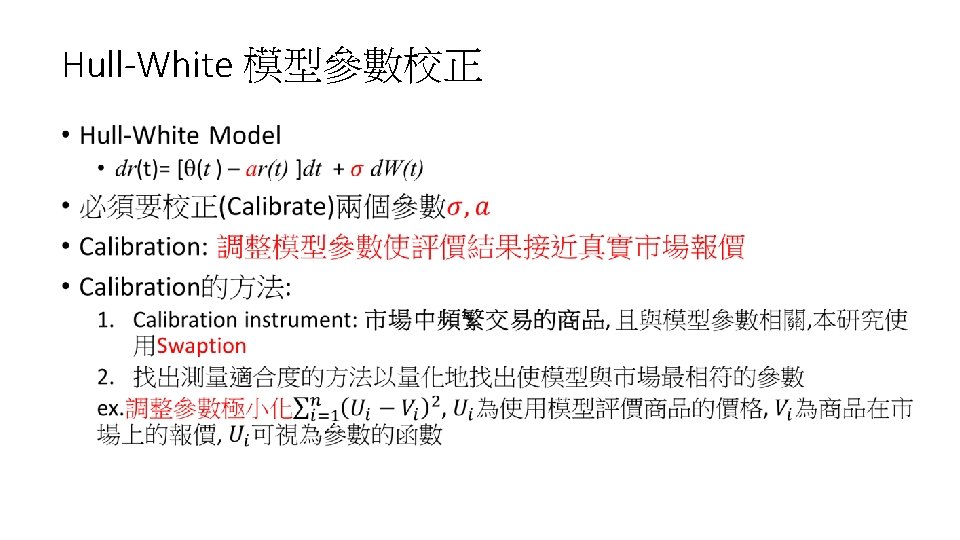

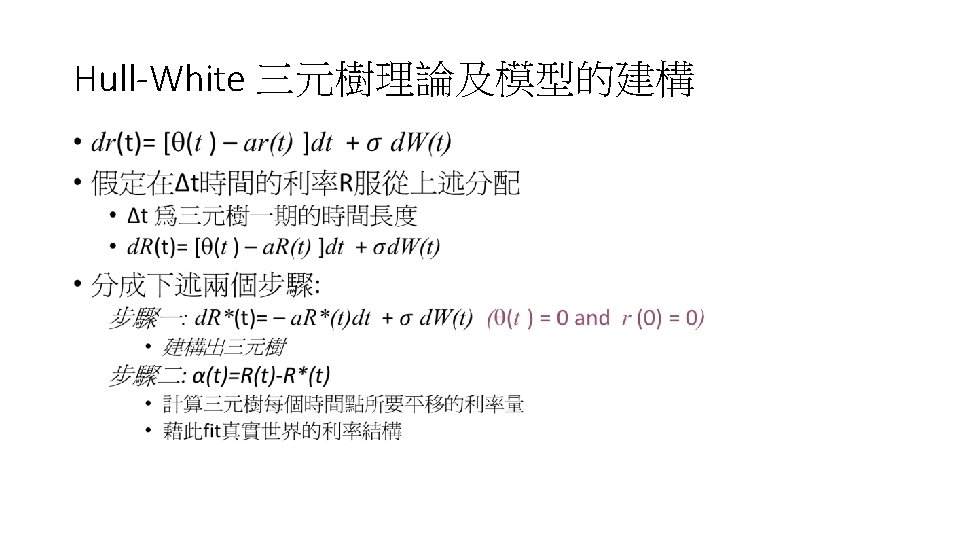

No-arbitrage model 簡介 • No arbitrage model: • • • 包含Equilibrium model的性質 市場的利率結構當作輸入的參數 造出來利率結構和市場觀察到的結構相符 Ho-Lee Model Hull-White Model

No-arbitrage model •

No-arbitrage model •

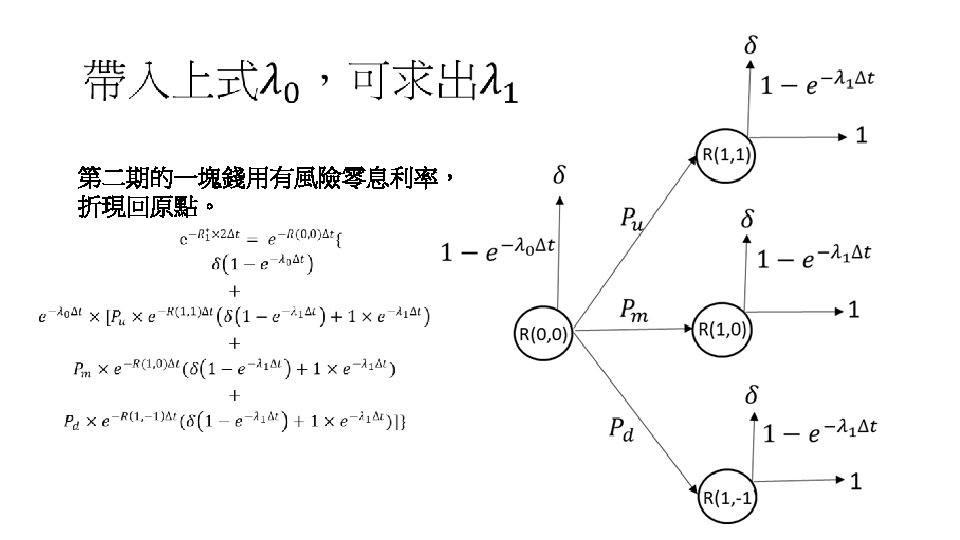

B (1, 1) F (2, 1) G (2,")

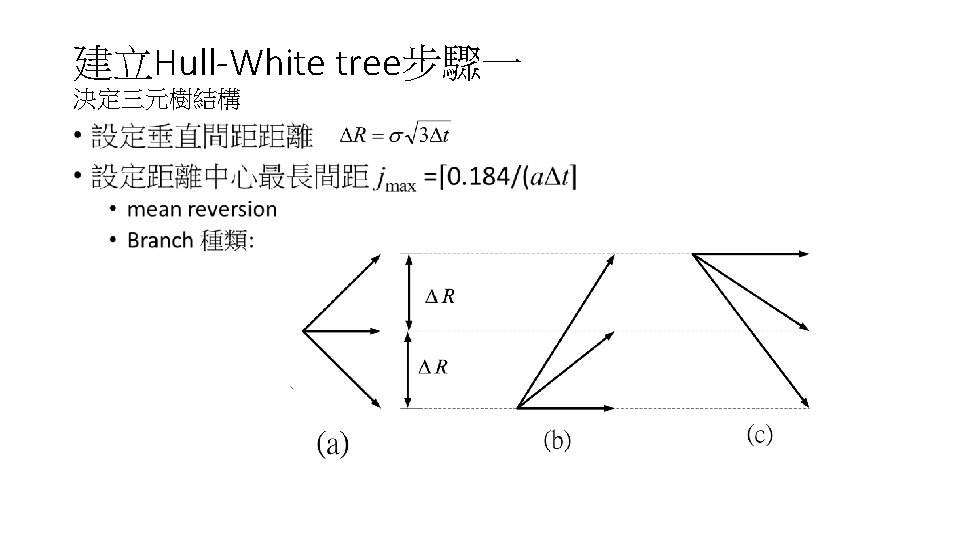

步驟一產生的三元樹 Δt=1 year E (2, 2) B (1, 1) F (2, 1) G (2, 0) C (1, 0) D (1, -1) A (0, 0) H (2, -1) I (2, -2) 對 0 mean reversion Node R A B jmax=2 C D E F G H I 0. 000% 1. 732% 0. 000% -1. 732% 3. 464% 1. 732% 0. 000% -1. 732% -3. 464% pu pm 0. 1667 0. 1217 0. 1667 0. 2217 0. 8867 0. 1217 0. 1667 0. 2217 0. 0867 0. 6666 0. 6566 0. 0266 0. 6566 0. 6666 0. 6566 0. 0266 pd 0. 1667 0. 2217 0. 1667 0. 1217 0. 0867 0. 2217 0. 1667 0. 1217 0. 8867 Let a=0. 1 σ=0. 01

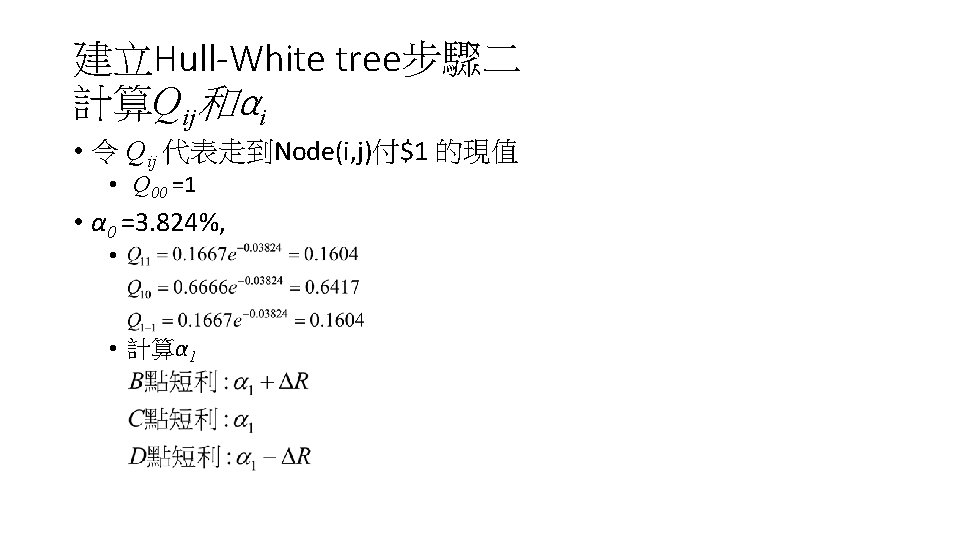

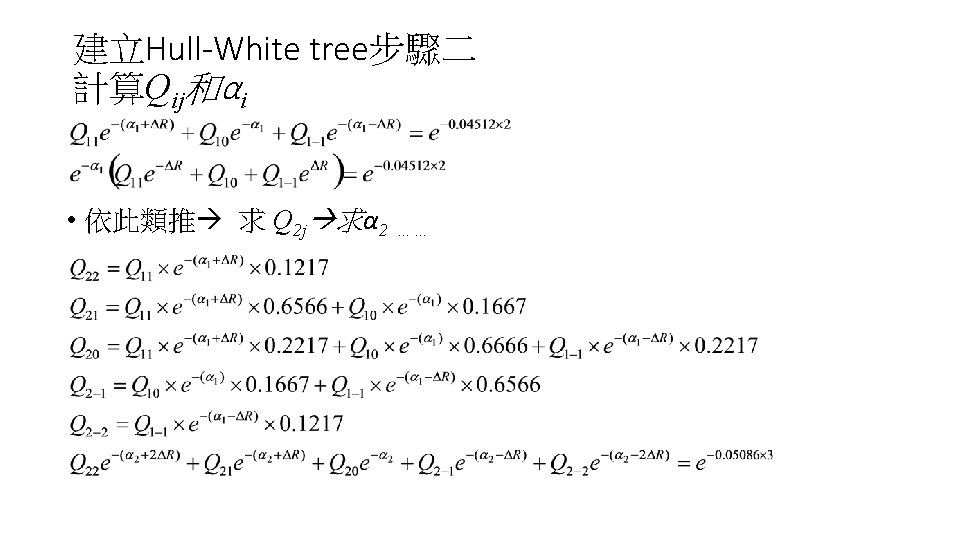

建立Hull-White tree步驟一 決定分支機率: Type A node match mean and variance See the proof in next slide Ex: Node B, F j=1 Node C, G j=0 Node D, H j=-1

Match the Variance

建立Hull-White tree步驟一 決定分支機率: Type B node match mean and variance Ex: Node I j=-2

建立Hull-White tree步驟一 決定分支機率: Type C node match mean and variance Ex: Node E j=2

步驟二校正後的三元樹 E F B G C H A D I 平移 3. 824% Node R pu pm pd A 平移 6. 252% B C D E F G H I 3. 824% 6. 937% 5. 205% 3. 473% 9. 716% 7. 984% 6. 252% 4. 520% 2. 788% 0. 1667 0. 1217 0. 1667 0. 2217 0. 8867 0. 1217 0. 1667 0. 2217 0. 0867 0. 6666 0. 6566 0. 0266 0. 6566 0. 6666 0. 6566 0. 0266 0. 1667 0. 2217 0. 1667 0. 1217 0. 0867 0. 2217 0. 1667 0. 1217 0. 8867 平移 5. 205%

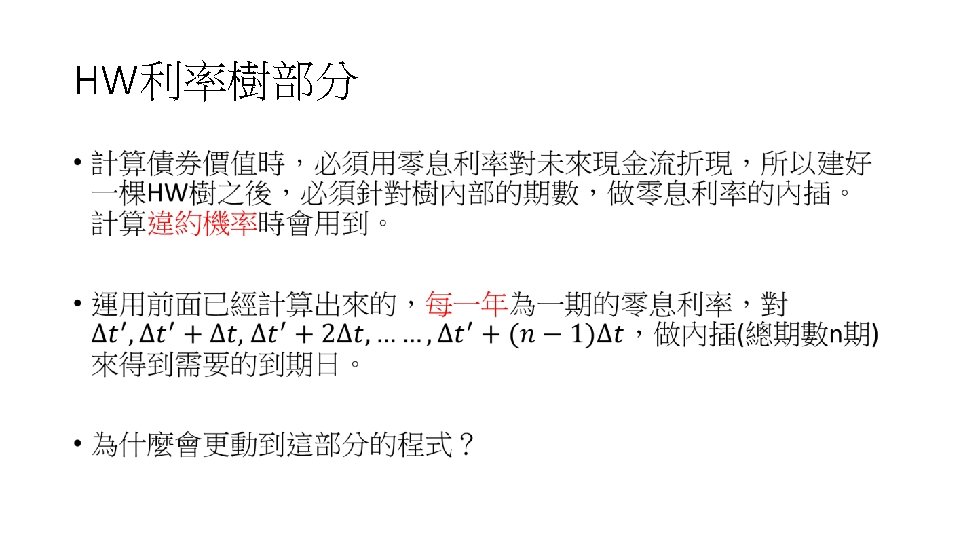

• void linearinterpolation. Risky(double *yield, double *data_yield); • void bootstrap(double *Zero. Curve,")

Bootstrap-1 year(程式更動部分) • void linearinterpolation. Risky(double *yield, double *data_yield); • void bootstrap(double *Zero. Curve, double *Treasury. Yield. Raw. Data, int type, int plusday); • void Rky. Zero. Rate. Interpolation(double* Zero_HW, double *Zero. Rate, int N, double Delta. T_first, double Delta. T)

Recovery rate定義 •

Recovery rate定義的改變 •

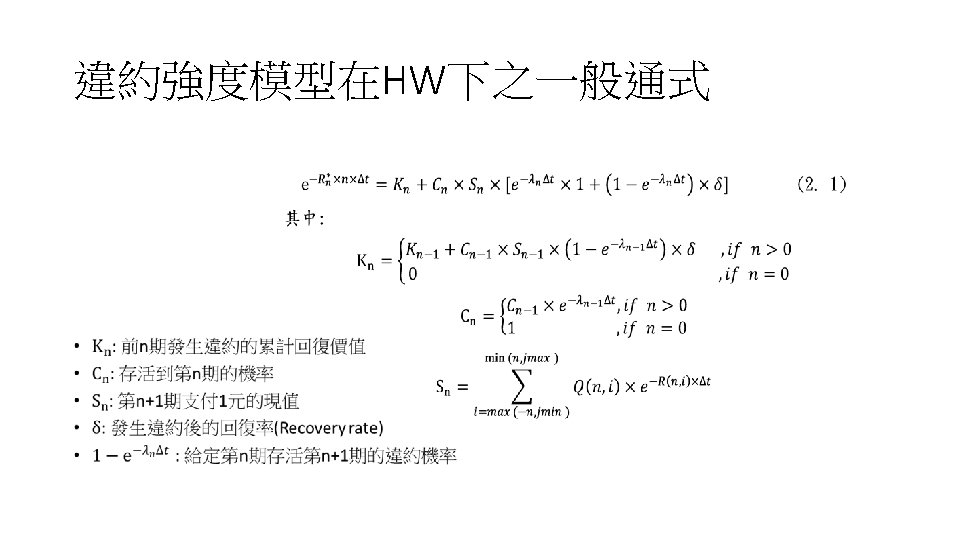

Reduced form model •

- Slides: 40