Works Contract Tax Deducted at Source TDS Agenda

")

")

of CGST")

): Ø if the")

:")

Ø A registered works")

")

ØGSTIN by TAN (Income Tax)")

• Return to be")

![Penal Provisions ØLate Payment by Deductor – Interest @ 18 % [51(6)] ØDeductor fails](https://slidetodoc.com/presentation_image_h/d1702b77df8cc71931add0f929d32a67/image-28.jpg "Penal Provisions ØLate Payment by Deductor – Interest @ 18 % [51(6)] ØDeductor fails")

ØTDS on Earlier Supplies ØA Supply qualifying for TDS in")

- Slides: 41

Works Contract & Tax Deducted at Source (TDS)

Agenda Works Contract Tax Deducted at Source (TDS)

Works Contract

Works Contract - Agenda PRESENTATION PLAN Ø Definition of Works Contract Ø Scope of Supply Ø Tax Rate in Works Contract Ø ITC Ø Time of Supply of Service Ø Registration Ø Composition Scheme Ø Invoice Details and Process

Works Contract - Definition “Works Contract” is defined in Section 2 (119) of CGST Act: Definition • “Works Contract” means a contract for building, construction, fabrication, completion, erection, installation, fitting out, improvement, modification, repair, maintenance, renovation, alternation or commissioning of any immovable property wherein transfer of property in goods (whether as goods or in some other form) is involved in execution of such contract

Works Contract - Definition Thus Works Contract has four major components as: 1. There should be a contract 2. For building, construction, fabrication, completion, erection, installation, fitting out, improvement, modification, repair, maintenance, alternation or commissioning 3. Immovable Property 4. Transfer of Property in Goods renovation,

Works Contract – Scope of Supply Under Jharkhand Goods and Services Tax Act, 2017: Ø Schedule II of Act specifies that works contract is treated as Supply Of Service.

Works Contract - Rate of Tax Ø Works contract as defined in clause 119 of section 2 of CGST/SGST Act attracts rate of 18% with full ITC.

Works Contract - Input Tax: Input Taxes are taxes that you pay when you purchase materials (Goods) or services or both for furtherance of your business. ITC: A registered person is entitled to take credit of input tax (ITC) charged on supply of goods or services or both procured by him. Ø ITC also allowed on Capital Goods Ø ITC not allowed for the goods and services for personal use Ø ITC to be allowed in course or furtherance of Business ITC is not eligible under certain situation such as mentioned in sec. 17 of JGST Act, 2017.

Input Tax Example: Construction of Road Input Goods Capital Goods Services from agencies Under sec 17(5)(C) of JGST paid on Bitumen, Stonechips, Cement etc. GST paid on purchase of Machines, Grinders, Mixer etc. GST paid while hiring Labour from agency, Surveyor, Architect etc. GST paid on these Goods, Capital Goods & Services Can be claimed as Credit (ITC) ITC can be used to setoff with your output

Works Contract – Time of Supply of service (Section 13 (2)): Ø if the invoice is issued within the prescribed time limit (within 30 days of supply), the time of supply of services shall be the date of issue of invoice by the supplier or the date of receipt of payment whichever is earlier Ø If the invoice is not issued within 30 days of supply, the time of supply of service shall be the date or the date of provision of service of receipt of payment, whichever is earlier.

Works Contract – Transitional Provision Service provided before applicability of GST(As per section 14): If invoice issued before GST regime but payment received under GST regime, the Time of supply shall be the date of issue of invoice. Ex: If the Bill is issued by the contractor before 30 th June and payment is received in the month of July then the VAT provisions will be applicable on such bills. If invoice issued and payment received under GST regime, the Time of supply shall be the date of invoice or the date of payment receipt, whichever is earlier (GST Provisions will be applicable in such bills)

Works Contract – Registration: Ø As per section 22 every supplier who makes a taxable supply of services in the State and If his aggregate turnover in a financial year exceeds 20 Lakh Rupees (in the entire country under single PAN), he shall be liable to be registered under this section. Compulsory Registration Ø As per section 24 a person making any inter state taxable supply or required to pay tax under reverse charge basis shall also be required to get registered at the time of 1 st such supply irrespective of his aggregate turnover. Ø Whenever he becomes liable under sec 22 or sec 24. he has to apply for registration within 30 days. Ø Registration for DDOs will start from 25 th July, 2017

Works Contract – Registration Composition Scheme: Ø Under GST, Composition scheme is not applicable to service provider except Restaurant and hence Composition Scheme not applicable to works contract.

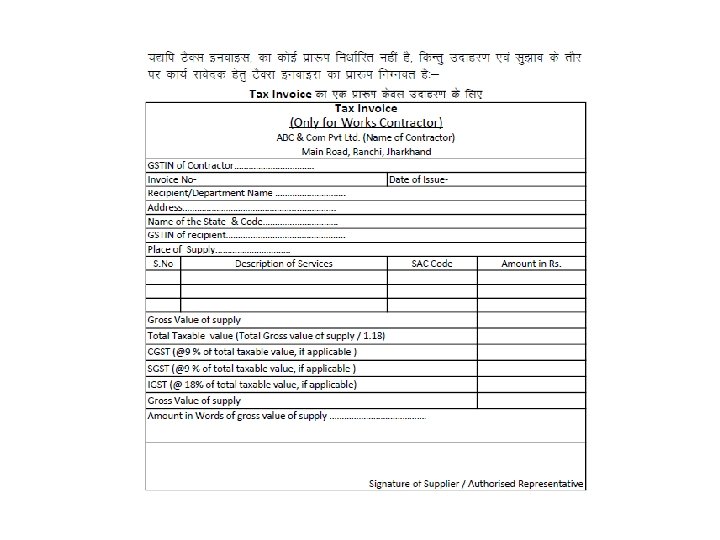

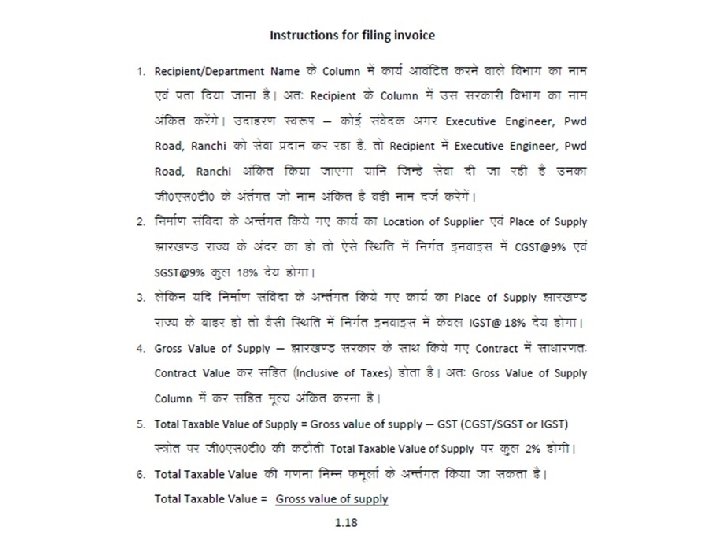

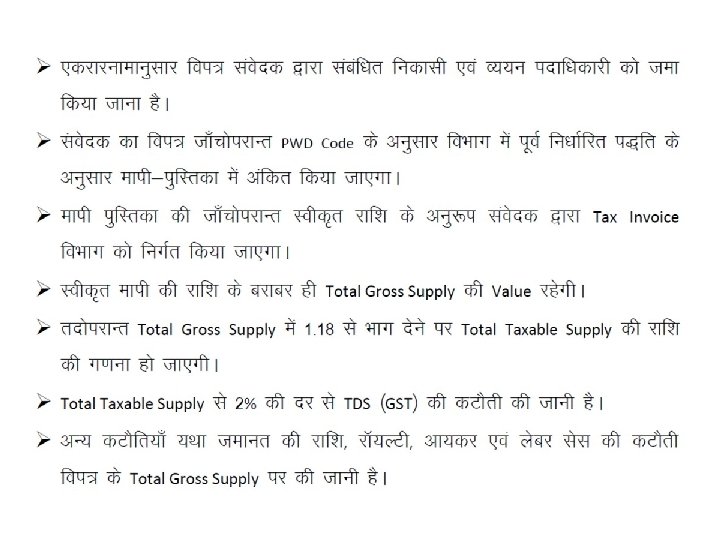

Tax Invoice for Works Contractor Issuance of Tax Invoice(section 31) Ø A registered works contractor supplying taxable services shall issue a tax invoice showing 16 particulars prescribed u/r 46. Ø The said tax invoice shall be issued before or after the provision of services but within a period of 30 days from the date of the supply of service(u/r 47)

Tax Invoice Contents All invoice under GST must have the following information 1. Name, address and GSTIN of the supplier 2. Tax invoice number (it must be generated consecutively and each tax invoice will have a unique number for that financial year) 3. Date of its issue 4. If the buyer (recipient) is registered then the name, address and GSTIN of the recipient 5. If the recipient is not registered AND the value is more than Rs. 50, 000 then the invoice should carry: a) Name and address of the recipient b) address of delivery c) state name and state code 6. HSN code of goods or accounting code of services** 7. Description of the goods/services

Tax Invoice contents All invoice under GST must have the following information 8. Quantity of goods (number) and unit (metre, kg etc. ) Since in case of works contract, it is supply of services so Quantity in such cases is not required. 9. Total value of supply of goods/services 10. Taxable value of supply after adjusting any discount 11. Applicable rate of GST (Rates of CGST, SGST, IGST, UTGST and cess clearly mentioned) 12. Amount of tax(With breakup of amounts of CGST, SGST, IGST, UTGST and cess) 13. Place of supply and name of destination state for inter-state sales 14. Delivery address if it is different from the place of supply 15. Whether GST is payable on reverse charge basis 16. Signature of the supplier.

Tax Deduction at Source (TDS)

TDS Provisions Under GST PRESENTATION PLAN ØLiability ØT. D. S rates and procedure ØRegistration of DDO (TDS deductor) ØReturn filing by DDO ØPenal provisions

Liability to Tax deduction at Source Liability: • On taxable supply-under a contract above 2. 5 Lakh • For DDOs, if contract value of supply is equal to or less than 2. 5 Lakh, then they are neither required to take registration nor deduct TDS. Liability to Deduct: (a) Central Government or State Government; or (b) local authority; or (c) Governmental agencies; or (d) Persons or category as notified by the Govt. on recommendation of GST council

SGST+ CGST or only IGST To deduct tax at the rate of 2% Intra State Supply : • TDS @ - 2 % (1% SGST + 1% CGST) • When supplier and place of supply in Same State (Intra) Inter State Supply: • TDS @ - 2 % IGST (2% only) • When supplier and place of supply in different States (Inter) Ex. Supply to Jharkhand (Recipient) Delivery in JH – SGST + CGST (1 % + 1% = 2%) Delivery from other State - IGST – 2%

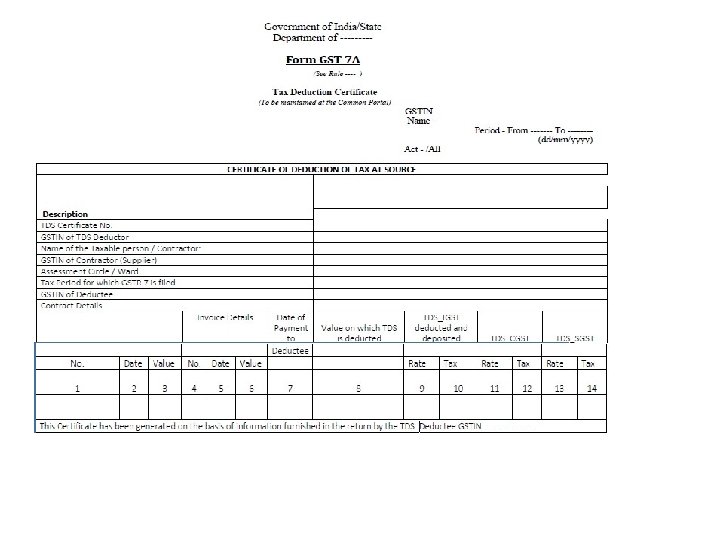

Payment and other Procedures ØPayment to be made through www. gst. gov. in ØPayment at GSTN before 10 th of next month ØCertificate(GSTR-7 A) to deductee within 5 days of filing of return in GSTR 7.

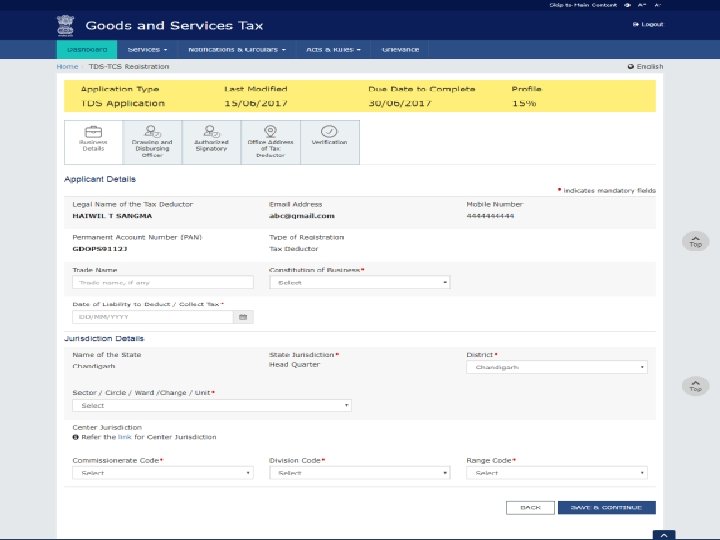

Procedure for registration ØOnline Application at GSTN (GST REG-07) ØGSTIN by TAN (Income Tax) and DSC/Aadhar ØApproval within 3 common working days ØNo query will be made by proper officer ØCertificate download (GSR REG-06) Login Øwww. gst. gov. in

Return • Every TDS deductor to file monthly return (GSTR-07) • Return to be filed only for the month in which there has been some TDS deductions • Not for every month • Due date of Return - 10 th of next month • Deductee to get (GSTR-07) in part-C of his (GSTR-2 A)

Penal Provisions ØLate Payment by Deductor – Interest @ 18 % [51(6)] ØDeductor fails to furnish GSTR-7 A • Penalty Rs. 100/- per day (Maximum Rs. 5000/-) [51(4)] ØFails to deduct tax or Deducts less tax amount or Fails to pay to government ØPenalty-10000/- or equivalent to tax (not deducted or short deducted or not paid) whichever is higher [122(v)]

Transitional Provisions. 140 (13) ØTDS on Earlier Supplies ØA Supply qualifying for TDS in VAT ØSale made prior to GST date ØAnd also an invoice issued prior to GST ØNo TDS to be made under GST ØEarlier Law Provisions to be applicable

Certificate on Bills or Cheque by DDO: 1. If no TDS is being deducted on any works contract then a certificate has to be obtained from DDO that “I am not required to deduct tax at source u/s 51 of JGST, Act 2017” 2. DDO of Works Division should furnish the details of contractor’s tax invoice number and issue date as a certificate on cheques presented in treasury for payment to contractor.

In case of Problem ØGSTN Help Desk – Multi Language ØCBEC help Desk ØToll free Call Centre ØLocal Office ØLaw at different web sites

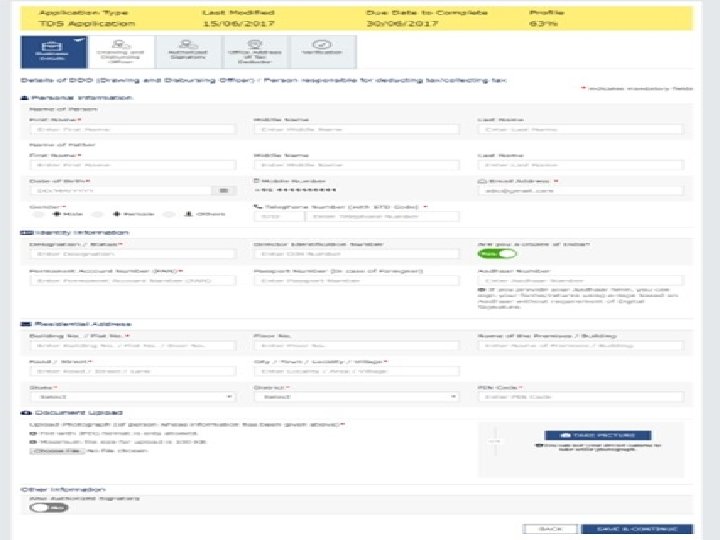

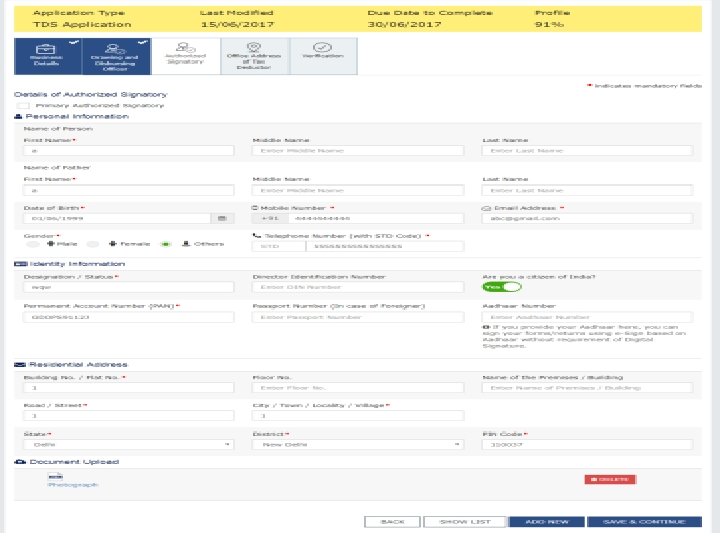

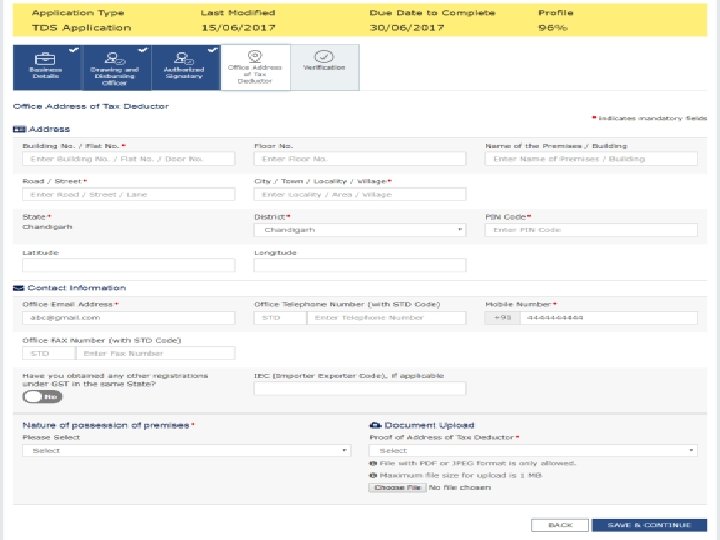

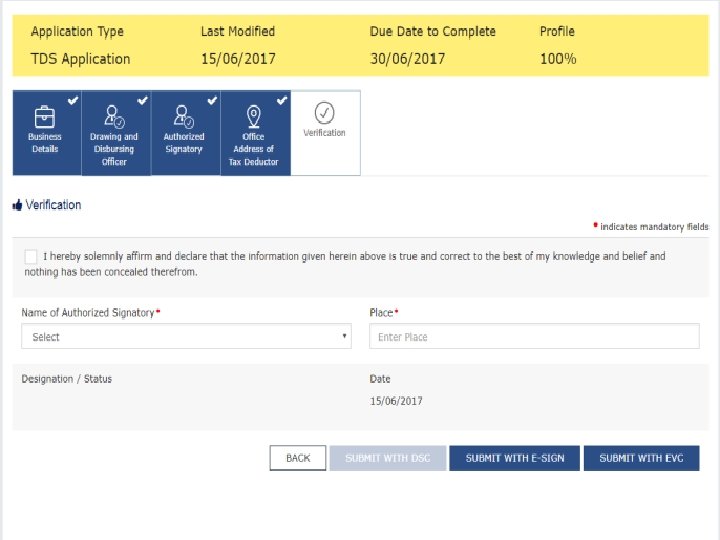

Instruction for filling Application for Registration as Tax Deductor Ø Enter Name of Tax Deductor as recorded on TAN/ PAN of the Business. TAN/PAN shall be verified with Income Tax database. Ø Provide Email Id and Mobile Number of DDO (Drawing and Disbursing Officer) / Person responsible for deducting tax for verification and future communication which will be verified through One Time Passwords to be sent separately, before filling up of the application. Ø Person who is acting as DDO/ Person deducting tax can sign the application Ø All information related to PAN, Aadhaar, DIN, CIN shall be online validated by the system and Acknowledgment Receipt Number will be generated after successful validation of all the filled information. Ø Status of the online filed Application can be tracked on the Common Portal.

Registration Module – Screen Shots