KOOROORA COMMODITIES GRAIN FARMING AND GRAIN TRADING PROJECT

Prepared by Sinogie")

has operated a large wheat farm")

Kooroora Commodities will be involved in the following businesses:")

Between leaving the farm and arriving at Newcastle or")

As worldwide demand for food grows, grain prices will")

Roberts Farming has many decades of experience in large-scale grain")

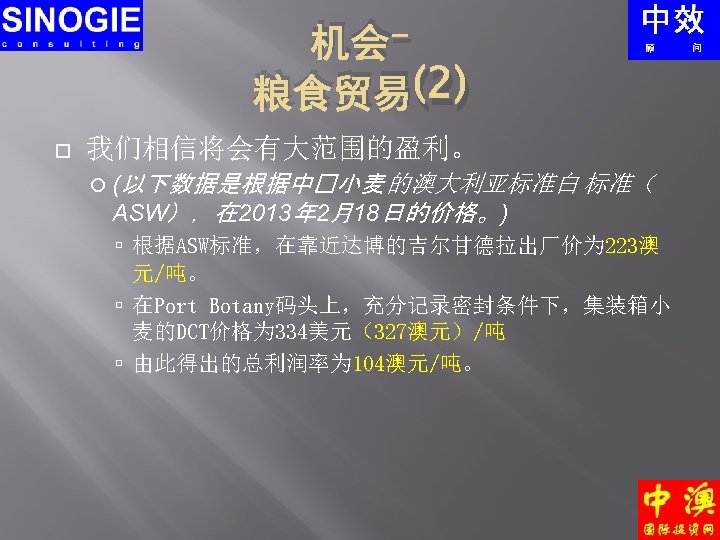

We believe there is significant scope for profit.")

The difference between the farm-gate price at Gilgandra")

The A$ 21 -41 margin that we believe")

RF’s roadtrains will be used to transport")

RF will transport grain as required from")

Carob trees take some time to reach full maturity. KC’s trees")

At current prices, the farm-gate price of carob pods is A$")

As we are making a conservative income projection, we are not")

Australian wheat-farming land is very undervalued: high-quality farmland")

There is currently a severe shortage of")

The ideal solution would be for a")

KC’s primary business plan is to store")

- Slides: 72

KOOROORA COMMODITIES GRAIN FARMING AND GRAIN TRADING PROJECT. Pre-NDA presentation (English) Prepared by Sinogie Consulting Group

Introduction This is an opportunity to invest in a project which will be able to secure 40, 000 tonnes of wheat or more per year, and deliver it to China at far lower prices than are currently possible. We have identified a gross margin of approximately US$ 31 per tonne: this equates to a gross profit of US$ 1. 24 million per year, or an ROE of around 10%. A Chinese investor with the ability to sell wheat directly to Chinese end-users would be able to further increase this margin.

What is the investment? Our client (Roberts Farming) has operated a large wheat farm close to Dubbo, NSW, for 60 years. The investor would be taking a stake in a new entity, Kooroora Commodities will be part owned by Roberts Farming, and part owned by one or more Chinese investors. Kooroora Commodities will be valued at A$ 14 million. Roberts Farming will maintain a 48% stake in Kooroora Commodities. We need an investment of A$ 7. 4 million for a 52% stake in Kooroora Commodities. This could come from one investor with A$ 7. 4 million, or two investors, each taking a 26% stake for A$ 3. 7 million. An individual who invested A$ 3. 7 million, and invested A$ 1. 3 million in New South Wales government bonds, may qualify for a Significant Investor Visa. These figures are negotiable.

What is the investment? (2) Kooroora Commodities will be involved in the following businesses: Selling Roberts Farming’s wheat and other grain directly to China. Selling neighbouring farms’ wheat and other grain directly to China. Storing, containerising and transporting wheat and other grain. Growing carob trees, harvestings carob, and selling carob directly to China. The company will also own 2, 000 acres of farmland.

What is the opportunity? The area around Dubbo is one of the most productive wheatgrowing areas in Australia. Much of the wheat grown around Dubbo is eaten in China. Dubbo is just under 400 km from the nearest major port (Newcastle), and just over 400 km from the nearest container port (Port Botany in Sydney).

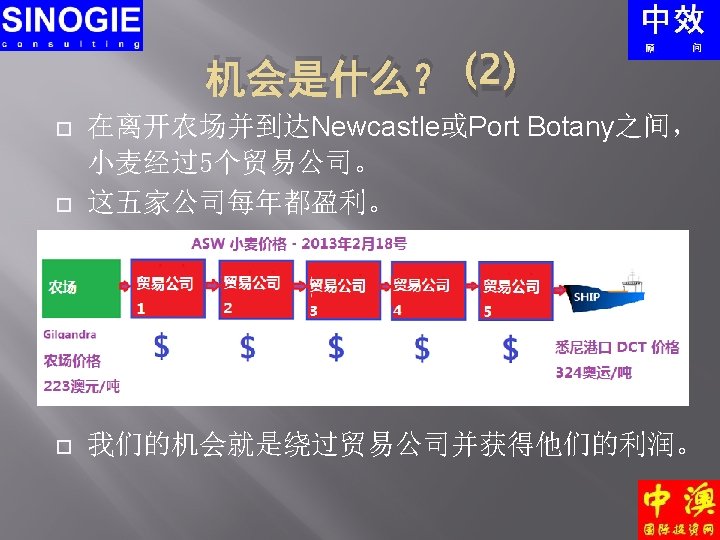

What is the opportunity? (2) Between leaving the farm and arriving at Newcastle or Port Botany, the wheat goes through up to five trading companies. Each of these five companies makes a profit. Our opportunity is to bypass the trading companies and take their profit.

What is the opportunity? (3) As worldwide demand for food grows, grain prices will continue to increase. As Chinese demand for meat grows, demand for animal-feed grains will continue to increase. As grain prices rise, agricultural land prices will rise. Kooroora Commodities can offer the investor a stable supply of grain at predictable prices. Kooroora Commodities carob crop gives the investor access to a high-quality animal-food additive which is growing in value. Kooroora Commodities’ land ownership gives the investor an additional return on investment as land prices rise.

资产总结 Kooroora Commodities 将有以下资产:

Summary of assets Kooroora Commodities will have the following assets:

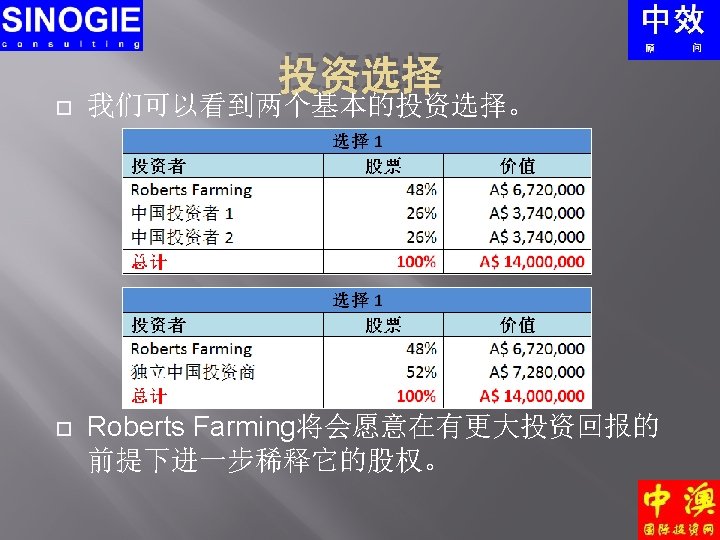

Investment options We see two basic investment options. Roberts Farming would be willing to dilute its equity stake in return for a larger investment.

About Roberts Farming has been involved in largescale wheat farming near Dubbo for 60 years. Roberts Farming currently owns 10, 000 acres of farmland, and produces approximately 8, 000 tonnes of grain per year. Roberts Farming is, as a standalone unit, a viable farming operation. However, it seeks to improve its profitability through the direct sale of wheat to China through Kooroora Commodities.

About Roberts Farming (2) Roberts Farming has many decades of experience in large-scale grain farming in New South Wales. Its management team is familiar with climate and harvest trend, transportation issues, input costs, and all of the other issues relevant to farming in the region. It has its own trucks, and a great deal of experience in grain transportation. Its management team has strong, well-established links with other local farms, transportation companies, equipment providers and containerisation companies.

The opportunity – grain trading Roberts Farming will create a new entity, Kooroora Commodities (“KC”). KC will build a 6, 000 tonne grain-storage facility on its own land. KC will buy Roberts Farming’s grain at a competitive price. KC will also buy grain from neighbouring farms at a competitive price. KC will work with a partner to containerise grain in Dubbo. The containerised grain will be sent by rail directly to Port Botany, and then shipped to China. KC will sell grain directly to trading companies and/or end-users in China.

The opportunity – grain trading (2) We believe there is significant scope for profit. (The figures below are based on Australian Standard White (“ASW”), a medium-grade wheat. Prices are as at February 18, 2013. ) The farm-gate price for ASW in Gilgandra, near Dubbo, was A$ 223 per tonne. The DCT price for fully-documented sealed, containerised wheat on the dock at Port Botany was US$ 334 (A$ 327) per tonne. This gives a total margin of A$ 104 per tonne.

The opportunity – grain trading (3) The difference between the farm-gate price at Gilgandra and the DCT price at Port Botany is A$ 104 per tonne. Transportation from any farm within a 70 km radius of Dubbo to a containerisation facility will cost A$ 15 per tonne. This transportation will be carried out by Roberts Farming and outside contractors: discounts should be available. KC’s containerisation partner will containerise the wheat and send it by train to Port Botany for A$ 65 per tonne. (We believe that it will be possible to reduce this to A$ 60 per tonne or lower, but we will use the A$ 65 price for planning. ) Documentation costs are A$ 3 per tonne. The maximum cost to KC of transporting wheat from farms, containerising them, documenting them, and taking them to port is therefore A$ 83 per tonne. This gives KC a projected minimum margin of A$ 21 per tonne. We expect that higher margins can be achieved. With projected discounts, we believe a minimum margin of A$ 2931 per tonne can be achieved

Grain trading – gross margins We have targeted initial shipments of 1, 000 tonnes per month: more than half of this will be accounted for by Roberts Farming. By Year 4, we expect shipments to rise to 1, 000 tonnes per week, and by Year 5, this should rise to 1, 250 tonnes per week.

Grain trading – securing grain KC will have 2, 000 acres of land. Around 1, 000 acres of this will be farmed for grain by RF. This will produce around 1, 000 tonnes of wheat per year. RF will continue to farm its own land, and will produce 6, 000 to 8, 000 tonnes of wheat per year. The remaining wheat will be purchased from neighbouring farms, within a 100 km radius (more to the Northwest) of the RF and KC site.

Grain trading – Securing grain (2) The A$ 21 -41 margin that we believe we can secure means that KC will be in a position to pay farmers several dollars per tonne more than Dubbo-based traders. Paying a slightly higher price will enable us to secure supply while maintaining strong profit margins. Paying a higher price will probably not even be necessary. Most traders pay farmers 30 -60 days or more after the grain is delivered. Most farmers are short of cash. They would prefer to be paid immediately. The A$ 2 million in operating capital will mean KC can offer farmers cash on delivery. If we offer the same grain prices as other traders, but offer immediate payment, most farmers will choose to deal with us. This means that, in a worst-case scenario, we may sometimes have to drop our margin by A$ 3 to A$ 5 per tonne. But in most situations, we will be able to maintain our margins.

Grain trading – Storage and transportation KC will set up its own 6, 000 -tonne grain storage facility. The equipment, installation, and groundwork will cost A$ 2, 000. The site will be installed on KC’s land. It will be close to Collie Road (a paved road with roadtrain access). Roadtrains can carry 50 tonnes of grain at a time.

Grain trading – Storage and transportation (2) RF’s roadtrains will be used to transport grain to and from the storage facility. With initial throughput of 12, 000 tonnes per year, this will require one 50 -tonne roadtrain per day, five days per week. Up to 6, 000 tonnes of grain can be stored at KC’s storage facility at any one time. The storage facility will keep the grain fresh and free of parasites. Grain will be stored at KC’s facility until it needs to be transported to the containerisation facility.

Grain trading – Storage and transportation (3) RF will transport grain as required from KC’s storage facility to our partner firm’s containerisation facility. Our partner firm will containerise the wheat on site, and load the containers onto a train. At present, our partner leases whole trains, but our partner plans to buy its own trains. Our partner has excess capacity on its trains, and is keen to partner with us to use this excess capacity. Our partner will charge KC a maximum of A$ 65 per tonne to inspect wheat, containerise it, send it by rail to Port Botany, and offload it at the port, ready to be loaded onto a ship. We believe that our partner will be willing to reduce this price further if we commit to shipping large volumes.

Carob farming KC will take possession of 3, 000 carob trees from RF. These trees were planted in 2008, and will reach commercial maturity in 2018. The trees will have a productive life of at least 100 years. The trees are fed by a computerised drip-irrigation system. Carob is used in the Middle East as an ingredient for sweet food. Carob is increasingly used as a food additive for animals. It enhances animals’ appetite and speeds weight gain, and prevents diarrhoea and intestinal infections without the use of antibiotics. As Chinese consumers and the Chinese government become more concerned about food safety and the use of drugs in animals – especially after the recent KFC scandal – demand for carob will increase.

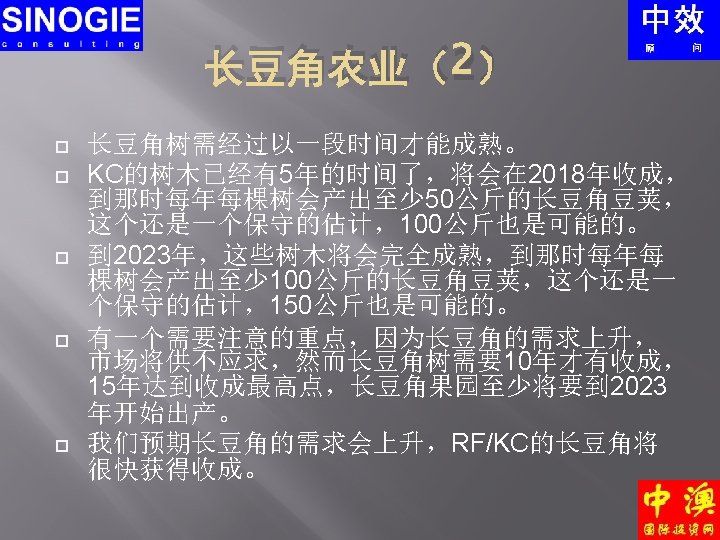

Carob farming (2) Carob trees take some time to reach full maturity. KC’s trees are already five years old. They will reach a commercial production level of maturity in 2018, and by then, will produce at least 50 kg of carob pods per tree per year (this is a very conservative estimate: 100 kg per tree per year is possible). By 2023, they will reach full maturity, and will produce at least 100 kg of carob pods per tree per year (this is a very conservative estimate: 150 kg per tree per year is possible). It is important to note that, as carob demand grows, the market will be unable to meet demand, as carob trees take ten years to reach commercial production and 15 years to reach peak production. New carob orchards which are planted now will not begin production until at least 2023. RF/KC’s carob crop will reach commercial maturity soon after we expect carob demand to increase.

Carob farming (3) At current prices, the farm-gate price of carob pods is A$ 10 per kilogramme. However, it is important to note that much of last year’s crop was sold to a company which uses carob in health foods for human consumption. This company paid RF A$ 35 per kilogramme. We have based our projections on a market price of A$ 10 per kilogramme, but we believe that far higher prices are achievable. It is worth noting that this projection only covers the market value of the carob crop. It would also be possible to earn carbon credits for maintaining the trees.

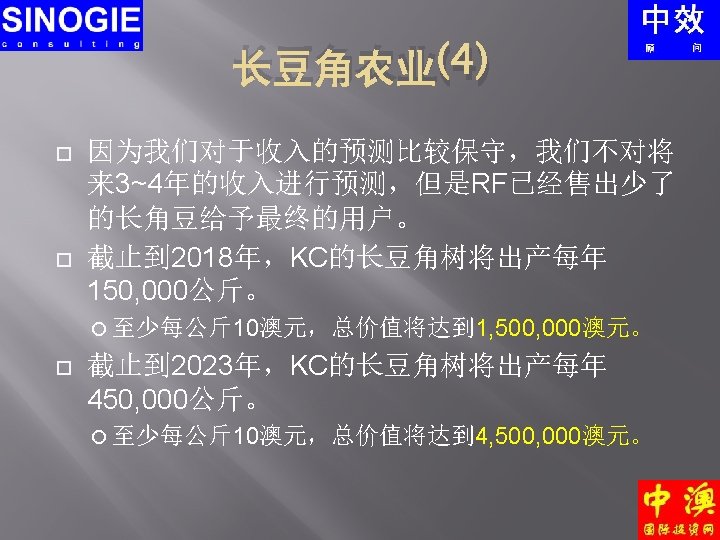

Carob farming (4) As we are making a conservative income projection, we are not going to project any income from the carob crop over the next four years. However, it should be noted that RF has already sold small amounts of carob to end-users. By 2018, KC’s carob trees should produce at least 3, 000 x 50 kg = 150, 000 kg of carob pods per year. At a minimum of A$ 10 per kg, these will be worth at least A$ 1, 500, 000. By 2023, KC’s carob trees should produce at least 3, 000 x 100 kg = 450, 000 kg of carob pods per year. At a minimum of A$ 10 per kg, these will be worth at least A$ 4, 500, 000.

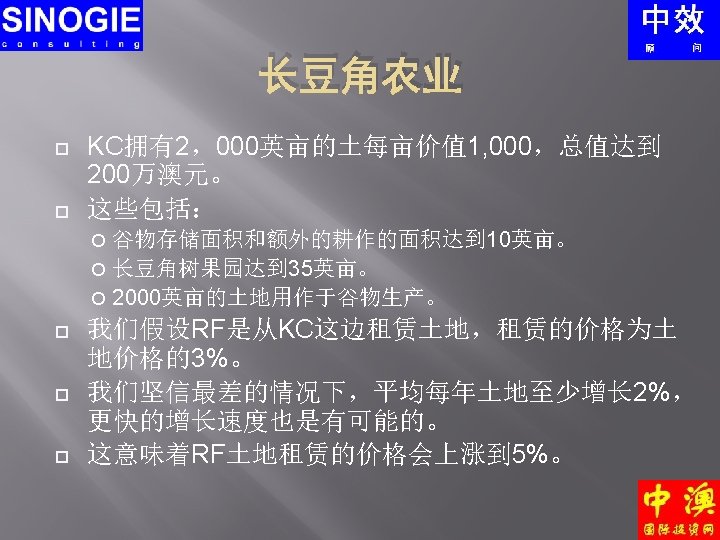

Land ownership and grain farming KC will own just over 2, 000 acres of land, valued at A$ 1, 000 per acre, for a total of A$ 2 million. This will include: The grain storage site and additional land works: 10 acres. The carob tree orchard: 35 acres. 2, 000 acres of farmland for grain production. We envisage RF renting the farmland from KC. Land will be rented for 3% of its value. We believe that, in a worst-case scenario, the value of the farmland will rise by an average of at least 2% per year. We believe that a more rapid rise is more likely. This means that the projected rate of return on farmland rented to RF will be at least 5%.

Land ownership and grain farming (2) Australian wheat-farming land is very undervalued: high-quality farmland near Dubbo costs around A$ 1, 000 per acre, compared to US$ 10, 000 per acre for similar land in Ohio. Several units in the Chinese government have said that Chinese investment in Australian agriculture will increase significantly over the next 18 months. Based on this, and on increasing global demand for grain, it is reasonable to assume that the value of the land will increase by far more than 2% per year. The return on KC’s farmland is therefore likely to be more than 5% per year.

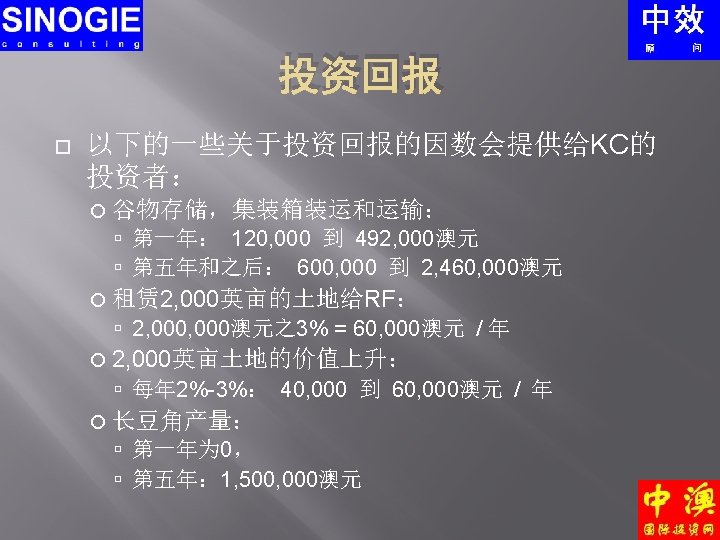

Return on investment The following factors will provide KC’s investors with a return on investment. Grain storage, containerisation and trading. A$ 120, 000 to A$ 492, 000 in Year 1. A$ 600, 000 to A$ 2, 460, 000 in Year 5 and subsequent years. (Note – these figures are calculated after all transportation costs. ) Rental of 2000 acres of land to RF. 3% of A$ 2, 000 = A$ 60, 000. Land-value appreciation on 2, 000 acres. 2% – 3% of A$ 2, 000 = A$ 40, 000 – A$ 60, 000. Carob crop. Zero in Year 1 A$ 1, 500, 000 in Year 5.

Projected return on equity We have provided three sets of projected return on equity. The first is based on a margin on grain trading after costs of A$ 10 per tonne; this is far less than we expect. The second is based on our projected minimum margin after costs on grain trading, of A$ 21 per tonne. The third is based on a median margin after costs on grain trading of A$ 31 per tonne. These projections do not include additional revenue which the investor may be able to earn by selling grain directly to end-users in China.

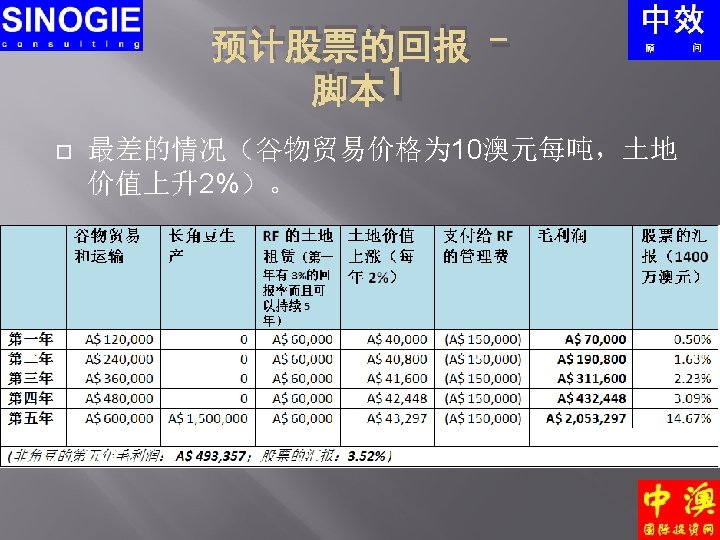

Projected return on equity – scenario 1 Worst-case prediction (grain trading margin of A$ 10 per tonne; 2% land-value appreciation).

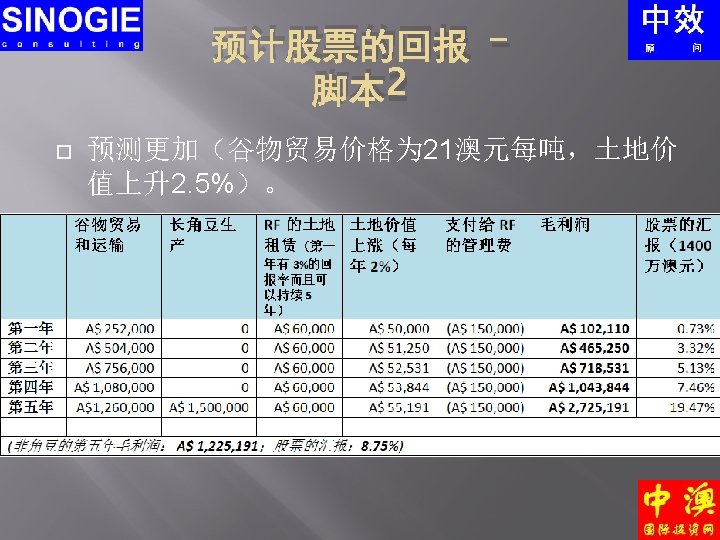

Projected return on equity – scenario 2 Base prediction (grain trading margin of A$ 21 per tonne; 2. 5% land-value appreciation).

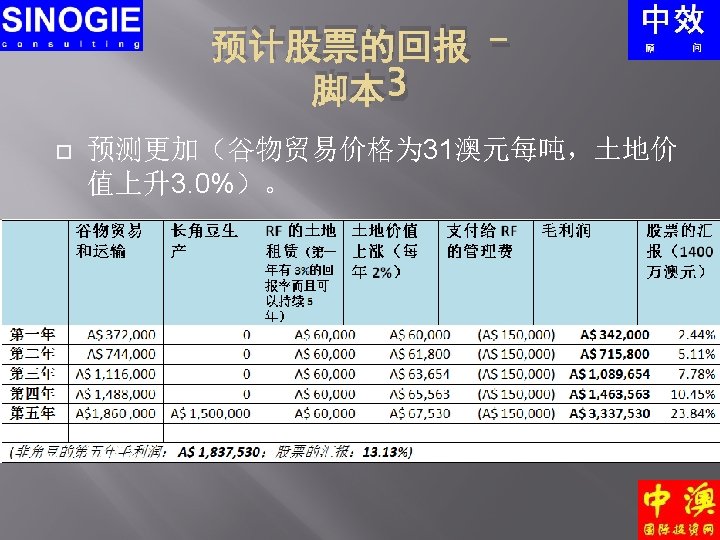

Projected return on equity – scenario 3 Optimistic prediction (grain trading margin of A$ 31 per tonne; 3. 0% land-value appreciation).

Additional revenue stream – fertiliser distribution We believe that the entire project would suit two investors seeking Significant Investor Visas, or a single investor seeking a strong return on equity and a steady supply of high-quality, low-cost grain. However, we believe that one type of investor would be able to use KC to create an additional income stream. KC is so far focused on getting grain out of rural New South Wales, and into China. An additional revenue stream would involve moving farming inputs – such as fertiliser – out of China and into rural NSW.

Additional revenue stream – fertiliser distribution (2) There is currently a severe shortage of fertiliser in North-West NSW. Fertiliser prices have risen significantly over the past few years. Price rises are unpredictable because of supply-chain problems – in some years, fertiliser prices have more than doubled, and even trebled, from year to year. Much of this is because it is difficult to transport fertiliser to North-West NSW from bases in Sydney and Newcastle. Some fertiliser is being imported from China by NSW-based trading companies. Much of this fertiliser is fake or sub-standard: the NSW trading companies are buying from dishonest Chinese trading companies. This is causing long-term damage to the reputation of Chinese fertiliser manufacturers. At present, most fertiliser is being imported and distributed from coastal cities. This is inefficient, as these cities are a long way from the best farmland. It can also lead to supplies suddenly being cut off. We know that many Chinese fertiliser companies are only able to export fertiliser four months per year. This creates problems for farmers needing a steady supply.

Additional revenue stream – fertiliser distribution (3) The ideal solution would be for a Chinese company to sell fertiliser directly to Australian farmers. This would allow the fertiliser company to ensure that only genuine, high-quality fertiliser goes to Australian farmers. It would also allow the fertiliser company to bypass traders and maximise profit. Selling to Australia would allow the fertiliser company to even out demand, as Australian demand is counter-cyclical to Chinese demand. The distribution centre should be in the middle of prime farming land. Creating an inland distribution hub would minimise transportation costs and allow direct contact with farmers. It would be good to have a storage centre. Fertiliser could then be exported during export periods and stored in Australia for sale throughout the year.

Additional revenue stream – fertiliser distribution (4) KC’s primary business plan is to store and export grain. This means KC has storage facilities. Through RF, it has access to road-trains for short-haul transportation. Through its containerisation partner, it has access to container trains. At present, containers are travelling from Port Botany to Dubbo empty. They are filled with grain or other farm products, and sent back to Port Botany. This means it would be possible to use these empty containers for very low-cost transportation to a distribution hub at KC’s facility. RF’s trucks will be travelling empty to farms to collect grain. This capacity can be used to transport fertiliser at low cost to farms.

联系我们 Bruce Mc. Laughlin Sinogie Consulting Australia Pty Ltd 16 -18 Grosvenor Street Sydney, 新州 2000 Australia / 澳大利亚 电话: +61 2 8705 5435 传真: +61 2 9241 5477 手机: +61 432 020920 电邮: bruce@sinogie. com 网站: www. sinogie. com www. zhongao. com. au

Contact us Bruce Mc. Laughlin Sinogie Consulting Australia Pty Ltd 16 -18 Grosvenor Street Sydney, NSW 2000 Australia Tel: +61 2 8705 5435 Fax : +61 2 9241 5477 Mobile: +61 432 020920 e-mail: bruce@sinogie. com Websites: www. sinogie. com www. zhongao. com. au