From Crash to Recession Reinhart and Rogoff n

Systemic (severe) Financial distress")

n n Monetary easing: Federal Open")

n n Support the functioning of")

the Fed collaborated with the Treasury,")

2001 1. 1 2006 2. 7 2002 1. 8")

nothing to fear but fear itself” Economics focus,")

- Slides: 67

From Crash to Recession

Reinhart and Rogoff n n n “This time is different” is the common first impression with many financial crises, but this is wrong. There are common elements among many incidents. The subprime mortgage crisis of the late 2000’s is categorized as a “banking crisis”.

Banking crisis: Reinhart and Rogoff definition: 1. Bank runs that lead to the closure, merging, or takeover by the public sector of one or more financial institutions.

Banking crisis: 2. If there are no runs, the closure, merging, or takeover, or large scale government assistance of an important financial institution (or group of institutions) that marks the start of a string of similar outcomes for other financial institutions.

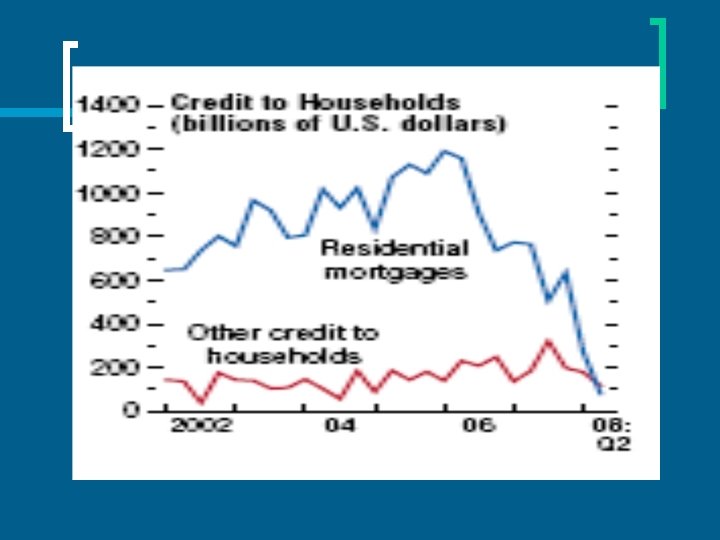

Banking crisis: n n In the case of banking panics and bank runs, the problem is in the liability (deposits) side. But more often, problems arise from the deteriotation in asset quality: collapse in real estate prices or increased bankruptcies in the nonfinancial sector.

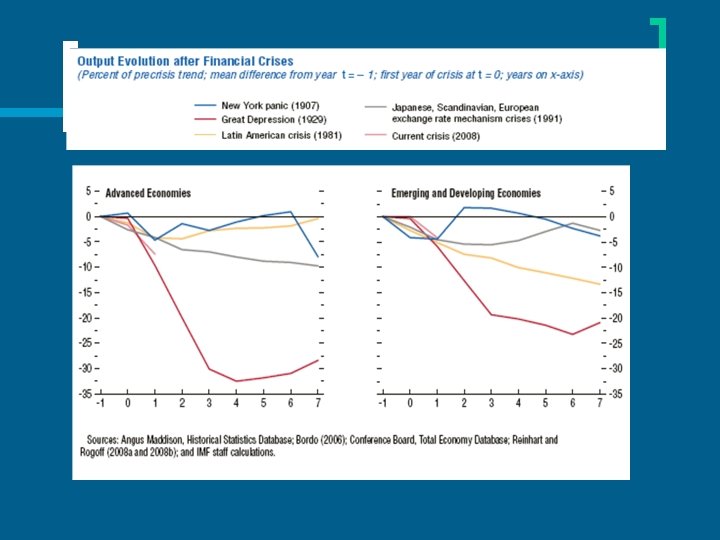

Banking crises 1. 2. n n n (Reinhart and Rogoff) Systemic (severe) Financial distress (milder) 18 banking crises in the developed world after World War II. 5 are big (severe). The largest is the current one. The second largest is Japan (1992).

Various comments on the current crisis n n This is a severe financial crisis A crisis of the Anglo-Saxon financial system (Martin Wolf) First crisis of financial globalization and securitization (Roubini) Due to financial innovation, the nature of systemic risk is changed

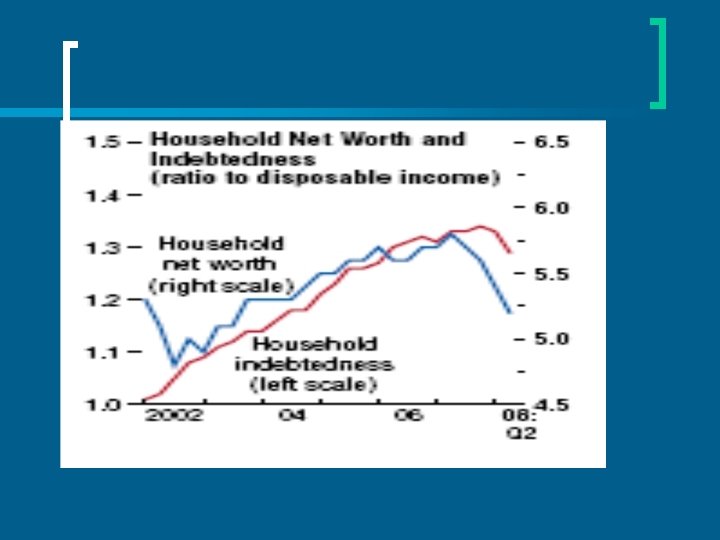

Indicators of risk of banking crises Before the crisis: n Rising asset prices n Slowing down of real economic activity n Large current account deficits n Sustained debt buildups

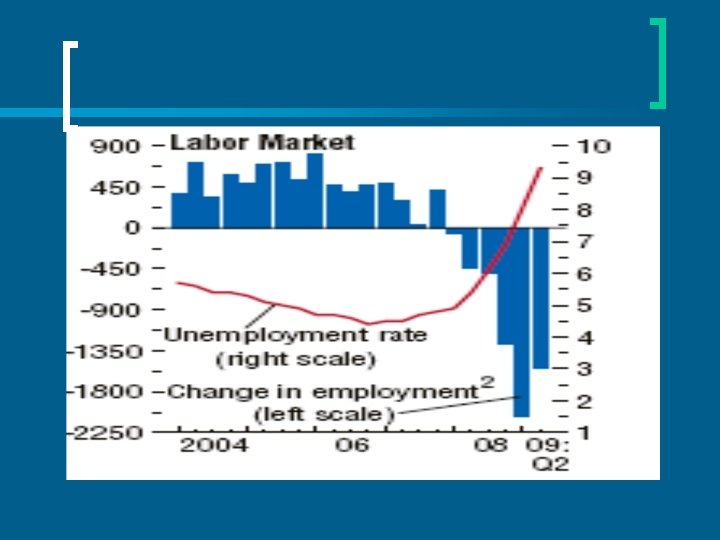

Aftermath of banking crises Indicators after the crisis: n Asset market collapses are deep and prolonged. n Profound declines in output and employment. n The value of government debt tends to explode.

Changing nature of systemic risk with financial innovation n n In the old times (1960 s-1980 s): banks held the credit risk of their lending on balance sheet. “Originate and hold” model When many bad loans/mortgage were made defaults would rise, a credit crunch would follow and then a recession

Changing nature of systemic risk with financial innovation n New model since 1980 s: securitization “originate and distribute” model. Banks not holding the credit risk but transferring to others. Look in “Originate-to-distribute: The origin of it all, ” MODELS & AGENTS January 26, 2008.

Changing nature of systemic risk with financial innovation The logic of this system: n Systemic risk should become lower as you slice and dice the risk because: n credit risk is spread out of the banks to capital markets and investors, domestic and abroad,

Changing nature of systemic risk with financial innovation Problem: systemic risk turned out to be now as high as in the past: 1. massive domestic financial contagion 2. massive global financial contagion 3. hard landing of the economy (recession or depression).

The Federal Reserve's strategy in the crisis (1) n n Monetary easing: Federal Open Market Committee (FOMC) has aggressively eased monetary policy to offset the effects of the crisis on credit conditions and the broader economy

The Federal Reserve's strategy in the crisis (2) n n Support the functioning of credit markets and to reduce financial strains by providing liquidity to the private sector--that is, by lending cash or its equivalent secured with relatively illiquid assets. (Look up the Financial Times interactive feature on Quantitative Easing)

The Federal Reserve's strategy in the crisis (3) the Fed collaborated with the Treasury, and sometimes with FDIC n for the acquisition of Bear Stearns by JPMorgan Chase n to stabilize the large insurer, American International Group (AIG). n put together a package of guarantees, liquidity access, and capital for Citigroup. n to support the government-sponsored enterprises (GSEs) Fannie Mae and Freddie Mac n assist in the resolution of troubled depositories, such as Wachovia. n the failure of such institutions would risk the whole financial system

Monetary policy ineffectiveness Monetary injections by central banks to solve the liquidity/credit crunch are ineffective because there is: n Shadow banking system n Insolvency rather than illiquidity n Uncertainty rather than risk

Shadow banking system n n The shadow banking system –unlike banks -does not have direct (or even indirect) access to the lender of last resort (LOLR) support of central banks Non-bank players are subject to severe liquidity/rollover risk as they borrow short/liquid and invest/lend long/illiquid

Insolvency rather than just illiquidity n n Millions of defaulting households 200 mortgage lenders gone bankrupt Many homebuilders gone bankrupt Many highly leveraged institutions have gone bankrupt

Risk vs uncertainty n n “Risk”is priceable while “Uncertainty”cannot be measured or priced lack of transparency lack of information/disclosure

Two types of unmeasurable uncertainty: n n Size of the losses is unknown. Uncertainty on who is holding the toxic waste

Unmeasurable uncertainty Uncertainty leads to : n lack of trust, confidence, and n large counterparty risk; Everyone hoards liquidity and is unwilling to lend n Liquidity injections by central banks have been hoarded

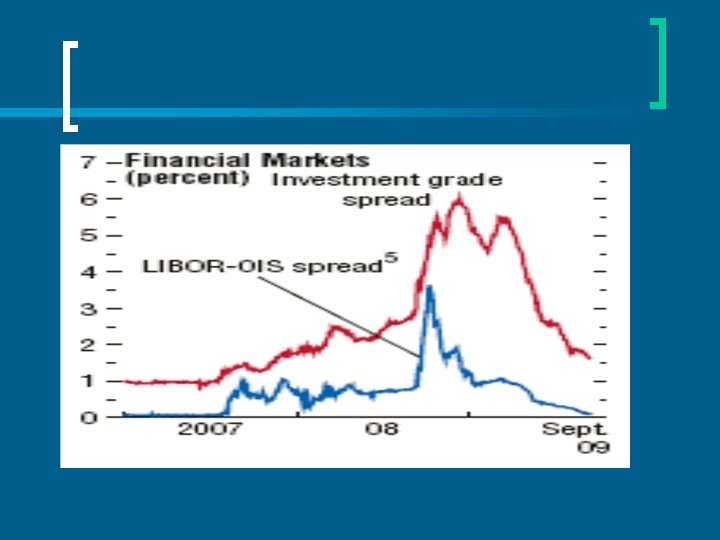

Uncertainty affects portfolio decisions n n n Shift away from risky assets to riskless assets eg American Treasury bills. Realisation that many new complex assets were much riskier General worry about all risky assets, and about the balance-sheets of the institutions that hold them. “Better safe than sorry” is the motto. The motto is having catastrophic macroeconomic consequences for the world. enormous spreads on risky assets, a credit crunch in advanced economies, and major capital outflows from emerging countries.

Tightness of credit

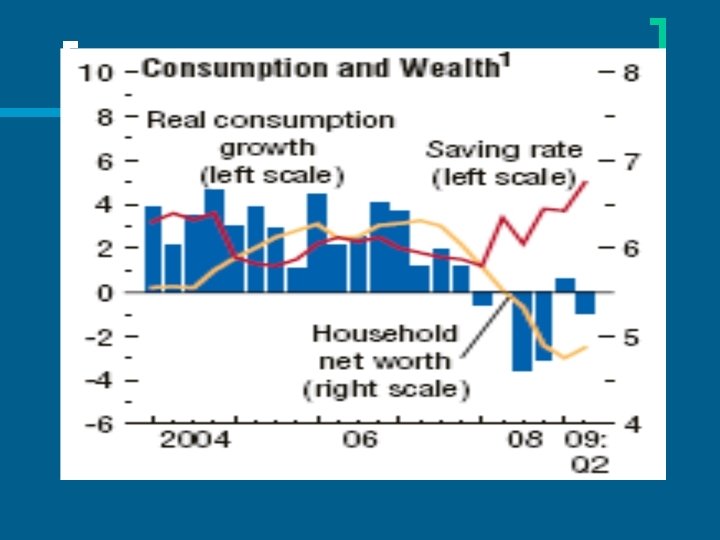

Uncertainty affects consumption and investment decisions n n Fears of depression forces consumers to be careful and save and to wait and see how things turn out. Buying a new house, a new car or a new laptop can be delayed a few months. Firms: given the uncertainty, why build a new plant or introduce a new product now? This is rational behaviour on the part of consumers and firms, but it has led to a collapse of demand, a collapse of output and to the current deep recession.

Lack of confidence Prevents n real investment spending by companies that are solvent n and spending by households that are sound

Viscious circle n n Small, medium and large-sized solvent firms may fail because of the lack of credit, The liquidity and credit crunch hurts even sound enterprises unable to roll over their debts.

Viscious circle Firms react to the falling demand by n investing less and n reducing production and employment n their goal is to survive the crisis by saving cash

Viscious circle n n But the loss of jobs or the risk of becoming unemployed restrains the consumption of households Banks that are under-capitalized are forced to reduce their risks and thus provide even less credit.

Aftermath of the US subprime crisis: Unlike emerging market economies in crisis, US did not face: 1. An exchange rate crash 2. A “sudden stop” in capital inflows

The crisis hit the US hard: Crises have deep and lasting effects on n Output and Employment (second great contraction) n Asset prices n Value of government debt increases

“Hard landing” n n There was discussion whethere would be “soft landing” or “hard landing”. NBER: The recession started in December 2007.

US GDP growth rates (%) 2001 1. 1 2006 2. 7 2002 1. 8 2007 2. 1 2003 2. 5 2008 0. 4 2004 3. 6 2009 -2. 7 2005 3. 1 2010 1. 5

Slowdown in 2007 n n n The U. S. economy slowed markedly to grow 2. 2 percent in 2007, down from almost 3 percent in 2006. Contraction of residential investment reduced growth in 2007. Consumption and business investment also decresed toward the end of the year, consumer confidence decreased and lending conditions tightened significantly after the outbreak of financial turbulence in August, despite the Federal Reserve’s aggressive turn to monetary easing.

Recession and depression n The popular definition for a recession : two consecutive quarters of falling GDP. Before the 1930 s all economic downturns were commonly called depressions. The term “recession” was coined later to avoid stirring up nasty memories. Look in: “Diagnosing Depression, ”The Economist , Dec 30 th 2008

Depression n n a decline in real GDP that exceeds 10%, or one that lasts more than three years. America’s Great Depression qualifies on both counts, with GDP falling by around 30% between 1929 and 1933. Output also fell by 13% during 1937 and 1938.

Difference between a recession and a depression The cause of the downturn matters: n A standard recession usually follows a period of tight monetary policy, n A depression is the result of a bursting asset and credit bubble, a contraction in credit, and a decline in the general price level.

Policy action n n A recession triggered by tight monetary policy can be cured by lower interest rates, but fiscal policy tends to be less effective because of the lags involved. By contrast, in a depression caused by falling asset prices, a credit crunch and deflation, conventional monetary policy is much less potent than fiscal policy.

Recession There is dicussion about the duration of the recession: n V or U or L shaped. n going on indefinitely: L-Shaped n long and protracted: U-shaped n short and shallow V-shaped

Index 2002=100

Policy Options: Brad De. Long n Nouriel Roubini n Olivier Blanchard n Paul Krugman Have suggestions regarding the use of monetary and fiscal policy n

Non depression economics n n n Short-run economic policy should be left in the hands of the central bank, with the legislature and the executive focusing on the long run and keeping their noses out of year-to-year fluctuations in employment and prices; Look in Depression Economics by J. Bradford De. Long Project Syndicate, December 2008

Non depression economics n n n Central banks’ highest priority should be to maintain their credibility as guardians of price stability, and only then turn their attention to keeping the economy near full employment, which they should do by influencing asset prices – upward when unemployment threatens to rise, and downward when an inflationary spiral looms;

Non depression economics n n n Central banks should influence asset prices through normal open-market operations by buying and selling short-term government securities for cash, thus changing the “safe” interest rate and the price of longer-duration assets;

Non depression economics n n While the central bank should stand ready to intervene to prevent bank runs, it should let the financial sector run itself with a light regulatory hand, viewing itself not as a chaperone but rather as the designated driver in the case of speculative excess.

Depression economics n n n Today, short-run economic policy cannot just be left to the central bank alone. its balance sheet is not big enough. the central bank now needs the assistance of that part of the government that taxes and borrows.

Depression economics n n n the highest priority for central banks can no longer be to maintain their credibility as guardians of price stability, but rather their credibility as guardians of the financial system’s stability and soundness. Once that highest goal has been achieved, central banks can turn their attention to trying to keep the economy near full employment.

Policy options: Roubini n n Governments and central banks are the only agents who take actions to prevent a worse recession. Partially socializing the losses of banks, firms and households, transferring to the public sector the losses of the private sector will be very expensive public debt-wise; but it is the policy medicine that can help an Lshaped near depression

Policy options: Roubini n n n The objective of central banks should be to ease the credit crunch with unconventional monetary policy actions and new tools. The risk of inflation from such aggressive easing is minimal: in spite of aggressive base money increases the money and credit multiplier has sharply fallen and the quantitative easing has not – so far – increased credit significantly

Policy options: Roubini n n n Today there is a glut of housing, consumer durables, autos and motorvehicles When you have a glut, capital spending becomes interest rateinsensitive. Easing money takes time to work out a glut and the related insolvencies

Policy options: Roubini n There are limits to how much the Fed can ease rates : inflation concerns, risk of free fall of the dollar, risk that foreigners will pull the plug on the external financing of the huge US current account deficit

Policy options: De. Long n n n Fiscal stimulus is needed as well. Non-depression economics overlooks fiscal policy, on the grounds that central banks’ tools are powerful enough and their decision -making more effective and technocratic than that by legislatures. But in today’s prevailing conditions, we cannot afford this perspective.

Policy options: Blanchard n n n Reduce uncertainty. On the portfolio side, establish a price, or at least a floor on the price, of the troubled assets. Ring-fence them or take them off bank balance-sheets. On the consumption side, commit to do whatever it will take to avoid a Depression, from fiscal stimulus to quantitative easing. Commit to do more in the future if necessary.

Policy options: Blanchard n n Above all, adopt clear policies and act decisively. Do too much rather than too little. Delays in financial packages have cost a lot already. Further rounds of debate will stoke uncertainty and make things worse.

Policy options: Blanchard n n return the private financial sector to health through recapitalisation. To caricature: if the world loves American Treasury bills but the funds would be more useful elsewhere, then the government should issue the bills, and use the proceeds to channel the funds where they are needed.

Policy options: Blanchard n n Undo the effects of the wait-and-see attitudes of consumers and firms on the demand side. Get them to spend more, and have the state do some of the spending itself. Offer incentives to buy now rather than later; for example, temporary subsidies to consumers who turn in a clunker and buy a new car, a measure adopted in France.

Policy options: Blanchard n n n Increase spending on public infrastructure, a central component of President Obama’s programme. Both types of measures are indeed present in the fiscal programmes more and more countries are putting in place. If tailored and communicated well, these programmes cannot only stimulate and replace private demand, but also convince consumers and firms that they are not in for another Depression. This will ensure that they stop waiting and start spending again.

Policy options: Blanchard n Coherent financial, fiscal and monetary measures are all needed. All three will have direct effects on demand. But, as importantly, they will help reduce uncertainty, lower risk spreads, and get consumers and firms spending again. If policymakers act decisively, private demand will recover sooner rather than later. And, within a year or less, we can be on the path to recovery.

Sources n Carmen Reinhart and Kenneth Rogoff, This Time is Different Eight Centuries of Financial Folly. Princeton University Press, 2009.

Sources n n Olivier Blanchard, “(Nearly) nothing to fear but fear itself” Economics focus, from The Economist print edition Jan 29 th 2009. Depression Economics J. Bradford De. Long, Project Syndicate December 2008.

Sources n n Nouriel Roubini, 2008 US and Global Economic Outlook and Implications for Financial Markets. RGE Monitor, January 2008. IMF World Economic Outlook, October 2009.