ACCOUNTING SERVICES COMPANY CHARACTERISTICS OF SERVICE COMPANY There

Date Information (1) Ref.")

Page 1 Date Information Ref. Debit Credit 2002")

is the removal of records from the")

Date Information Ref. Debit")

Reduction Debit")

Account Number")

is the adjustment of the records")

Aktiva Current")

Aktiva Currente assets :")

Page Date 2002 31")

- Slides: 73

ACCOUNTING SERVICES COMPANY

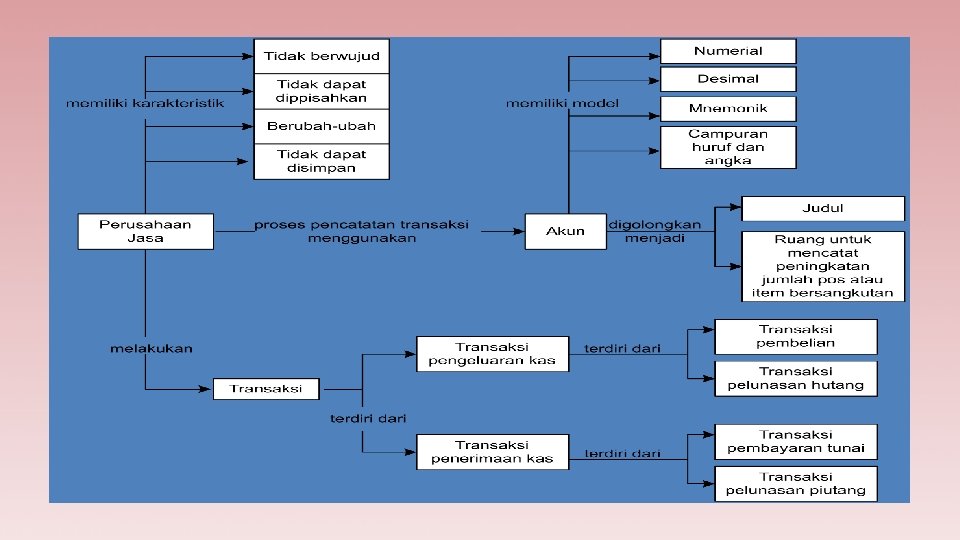

CHARACTERISTICS OF SERVICE COMPANY There are four characteristics that distinguish between services and goods, among others: 1. Intangible. The nature of the services does not have a physical form that can be seen and touched. 2. Inseparability. There is no separation between the production and sale of services. 3. Variability. Services properties can not be standardized because it depends on the tastes, time, place, and consumer characteristics. 4. Perishability. Services properties can not be stored for resale at a different time. This is why services company has no inventory services.

CLASSIFICATION AND RELATED TRANSACTIONS BETWEEN THE COMPANY Transaction Services Company consists of Administration transactions (Receive / pay / record) support Sales Transaction Services

grouping accounts Riil Account Assets Liabilities Equity Nominal Account Revenue Expense

CYCLE OF ACCOUNTING SERVICES COMPANY Make the final verse and closing the ledger accounts. Make a trial balance after closing the books. Records the transaction in a diary / journal. Prepare financial statements (balance sheet, income statement, statement of changes in equity, cash flow statement and notes to the financial statements). Make reversing entries. Move the transaction from the journal to the ledger accounts (posting). Creating a working paper (worksheet). Make a trial balance. Preparing the adjustment data. Prepare and gather evidence of the transaction.

LISTING STAGE COMPANY ACCOUNTING SERVICES

LISTING STAGE COMPANY ACCOUNTING SERVICES

Definition of journal Journaling is a process of recording a transaction into a journal. Prior to journal, we must first analyze the effect of each transaction to the accounts, among other assets, liabilities, capital, income, and expenses.

TRANSACTIONS RECORDED TO JOURNAL Debit and Credit Mechanism Increase (Normal Balance? Decrease Debit Credit Liabilities Credit Debit Equity Credit Debit Credit Revenue Credit Debit Expense Debit Credit Balance Account: Assets Accumulated Depreciation Prive Income Statement Account

Forms Journals Company’s Name General Journal (In Thousands of Rupiah) Date Information (1) Ref. (2) Debit (3) Credit (4) (5) (1) record the date of the transaction (2) record the names of the accounts relating to the transaction (3) record the number and the account code (4) record the number that should be on the debit (5) record the amount that must be in credit Information : Colomn

Example 1. On March 1, 2006, the company borrowed money from the bank amounting to Rp. 10, 000. Analysis: corporate debt increases with the addition of cash companies. 2006 30 Mar Cash Loans 10. 000 2. Pada tanggal 7 Maret 2006 perusahaan menerima uang atas pekerjaan yang belum dilaksanakan sebesar Rp. 1. 000. . Analisis: uang sebesar Rp. 1. 000 tidak boleh diakui sebagai pendapatan, perusahaan harus mengakuinya sebagai hutang. 2006 7 Cash Mar Prepaid Revenue 1. 000

Example 3. On March 8, 2006 the owners of capital in the form of a cash deposit of Rp. 40, 000. Analysis: as a first step or the development of enterprises, owners may deposit assets in the form of cash, equipment, supplies, and other assets to the company. 2006 8 Cash Mar Owner’s Equity 40. 000 4. On March 10, 2006, the owners took the company money for personal use amounted to Rp. 2, 000. Analysis: This transaction is considered as a capital withdrawal so that the owner of the company owner's equity is reduced. 2006 Mar 10 Owner’s Equity Cash 2. 000

Example 5. On March 10, 2006, the liquidation of the crisis resulted in the company can not pay for electricity, telephone and water for the month of February 2006 amounted to Rp. 6, 000. Analysis: although the company has not paid such expenses, the company has benefited from the use of electricity, telephone and water. 2006 10 Utilities Expenses Mar utilities Payable 6. 000 6. On March 12, 2006, the company has completed the work that had previously been paid by the customer Rp. 1, 000. Analysis: unearned income accounts are grouped into debt. 2006 12 Mar Prepaid Revenue 1. 000

Example 7. On March 22, 2006, the company bought a new engine in cash amounting to Rp. 10, 000. Analysis: machines purchased in cash would reduce the company's cash, but the machine account increases. 2006 12 Machine Mar Cash 10. 000 8. On March 25, 2006, the company received payment of customer receivables amounting to Rp. 2, 000. Analysis: accounts receivable (assets) will be reduced when the customer has to pay (credit), and will increase the company's cash (debit). 2006 25 Mar Cash Account Receivable 2. 000

Example 7. On March 27, 2006, the company received an income of Rp. 1, 000 on work completed. Analysis: income can raise capital, and recording done by crediting revenue (increases). 2006 27 Mar Cash 1. 000 Revenue 1. 000 8. On 30 March 2006, the company paid salaries amounting to Rp. 3, 000. Analysis: can reduce the burden of capital, and the company will debit the respective load. 2006 Mar 30 Salaries Expense Cash 3. 000

The following table summarizes the previously discussed journal Numb. Transaction Analysis Debit Credit 1 Borrowing money from bank assets increased debt increases Cash Account Payable 2 Receive money for work not yet done assets increased debt increases Cash Prepaid Revenue 3 Own capital in the form of cash deposits assets increased capital increase Cash Equity 4 The owner took the company money for personal purposes reduced capital assets decreased Equity Cash 5 Acknowledging the load electricity, telephone, and water that has not been paid. Expenses increased assets decreased Utilites Expense Utilities Payable 6 Recognize revenue for which payment is received in advance debt reduced revenue increases Prepaid Revenue 7 Cash purchase the company's assets increased assets decreased Machine Cash 8 Receiving payments receivable assets increased assets decreased Cash Account Payable 9 Receiving revenue assets increased revenue increases Cash Revenue 10 Noting salaries expense assets decreased expenses increased Salaries Expense Cash

Work on these transactions into the general ledger: During the month of December 2002, Salon Susi had the following transactions. Des. 5 Purchased salon equipment in cash from miscellaneous Store for Rp. 6, 000. 8 Paid employee salary of Rp. 2, 000. 9 To borrow money from the bank amounting to Rp. 10, 000. 15 The owners of capital to deposit money Rp. 30, 000. Keep a journal of transactions over the top!

Answer JOURNAL (IN THOUSANDS OF RUPIAH) Page 1 Date Information Ref. Debit Credit 2002 5 Equipment (Increase) 111 (+) 6. 000 Dec. Kas (Decrease) 101 (-) 6. 000 Purchase of screen printing equipment 8 Salaries Expense (Increase) 501 (+) 2. 000 Cash (Decrease) 101 (+) 2. 000 Payment of salaries 9 Cash (Increase) 101 (+) 10. 000 Account Payable (Increase) 201 (-) 10. 000 Borrowing money from bank 15 Cash (Increase) 101 (+) 30. 000 Equity (Increase) 301 (+) 30. 000 Equity expenditures

JOURNAL transfer the TO LEDGER Overbooking (post) is the removal of records from the journal to the accounts in the general ledger on a periodic basis. The ledger is a book containing a collection of accounts that are interconnected and constitute a whole separate. The books of the transfer procedure: 1. Move the date of the journal to date column on the accounts in question. 2. Move a brief description of the journal column to column remarks on that account. 3. Move the column to the journal page Ref. on that account. 4. Move the amount of discharge from the journal to the relevant account debit column and the amount of credit from the journal into account the credit column in question.

FORM LEDGER Account Name : Nomor akun : Date Information Ref. Debit Balance Credit Debit Credit Information : colomn (1) note the date of the transaction (2) record the type of transaction (3) record the number of pages of the journal (4) record the account debited (5) noted an account credited (6) noted the final balance

Example Account Number 101 CASH ACCOUNT (IN THOUSANDS OF RUPIAH) Date Information Ref. Debit Balance Credit Debit Credit 2002 5 Purchase of Office Equipment GJ 1 6. 000 Dec 8 Salaries Expense GJ 1 2. 000 4. 000 9 Loans GJ 1 10. 000 6. 000 15 Paid-up equity GJ 1 30. 000 36. 000 PERALATAN KANTOR (DALAM RIBUAN RUPIAH) Tanggal Account Number 102 Keterangan Ref. Debit GJ 1 Saldo Kredit Debit 6. 000 Kredit 2002 5 Cash 6. 000 Dec

Creating balance sheet • A trial balance is a list containing summaries of all the account and the balance of each account. • At the end of the fiscal year, the balance Salso made to summarize or recapitulate registries on the ledger in order to prepare the financial statements. Nevertheless, the trial balance can be made at the end of a certain period (eg, month-end, quarter end, or the end of the semester) in order to check the balance of account balances. • A trial balance is also called a trial balance (trial balance). • The trial balance putting each account according to the rules or specific order. Assets Account Payable Equity Revenue Expense

Normal Balance Accounts Type of Account Balance Account : Increase (Normal Balance) Reduction Debit Credit Debit Liabilities Credit Debit Equity Credit Debit Credit Revenue Credit Debit Expense Debit Assets Accumulated Depreciation Prive Income Statement Account :

EXAMPLE LIA’’S Salon Balance Sheet September 30, 2004 (In Thousands of Rupiah) Account Number Account Name Debit Credit 101 Cash XXX 102 Account Receivable XXX 103 Office Supplies XXX 111 Office Equipment XXX 106 Accumulated Depreciation Office Equipment XXX 201 Account Payable 301 Equity 302 Prive XXX 401 Revenue 501 Rent Expense XXX 502 Advertising Expense XXX 503 Insurance Expense XXX XXX XXX AMOUNT

SUMMARIZE STAGE COMPANY ACCOUNTING SERVICES

Summarize saget

ADJUSTING ENTRY • Journal of adjustment (adjustment journal) is the adjustment of the records or the actual facts at the end of the period. Journal of adjustment is based on data from the trial balance and the adjustment data at end of period. Aim 1. For any real estimates, particularly the estimated assets and liabilities at the end of the period shows the actual amount. 2. For each nominal estimate, ie estimates of revenues and expenses at the end of the period indicates the amount of revenues and expenses should be recognized

JOURNAL ARTICLE LISTING OF ADJUSTMENT • Assets • Prepaid Expense

USE OF supplies o The use of equipment that is part of the purchase price of equipment that have been consumed or used during the accounting period. Total adjusted for the amount used. 2006 Dec. 31 Supplies Expense 501 Supplies 104 xxxxxxx

Revenue receivable o Receivables revenue or accrued income means income that is rightfully companies but not recorded or not received. Total adjusted for amounts that have become income not yet received. 2006 Dec. 31 Account Receivable. . . . 104 Revenue. . . 401 xxxx

Expense Payable or Accrued Expenses o Debt load means that the load that it is the duty of the company but have not been recorded or unpaid. Total adjusted for amounts that have become a burden unpaid. 2006 Dec. 31 Expense. . . 501 Account Payable. . . 201 xxxx

Revenue debt or Prepaid revenue o Unearned income is recorded as a liability or debt. Total adjusted for the amount that has been exceeded or has expired. Journal of adjustment are: 2006 31 Dec. . . . Prepaid 201 Revenue. . . . 401 xxxx o Unearned income is recorded as income. Total adjusted for the amount that has not been exceeded or not yet expired. 2006 Dec. 31 Revenue. . . 201 . . . . Prepaid 401 xxxx

Advance fee or Prepaid Expenses Prepaid expenses means the expenses already paid, but the weight is a burden for the future. Preparation of adjusting entry to a prepaid expense can be done through two methods. That is : o Prepaid expenses are recorded as property or assets. the amount to be adjusted for the amount that has been exceeded or has expired /'ve become an expense 2006 31 Des. o Expense. . . . 501 . . . . Prepaid 104 Xxxx xxxx Prepaid expenses are recorded as expenses. Total adjusted for the amount that has not been exceeded or has not expired / not be a expense 2006 Des. 31 . . . Prepaid 201 Expense. . . . 401 xxxx

losses Receivables o Accounts receivable losses means the estimated losses arising from all or part of the amount receivable may not be collectible. 2006 Des. 31 Account receivable losses expense The loss receive account 502 xxxx

Depreciation of Fixed Assets o At the end of the period, fixed assets owned by a company must be depreciated, because the real value of fixed assets in the current year compared with the value of fixed assets in the year of purchase is not the same (except land). Method of Calculating Depreciation: Straight-line method. Fixed rate method over the book value. Method total number of years.

Continuation Adjusting Steps: • • • Prior to determining the value of depreciation each year, companies must estimate the residual values and useful lives of fixed assets. The residual value is the estimated remaining value when the useful life of such assets have been exhausted. The useful life is estimated term of such assets may provide benefits to the company. Residual value and benefits are determined by management. Great calculation of depreciation expense each period using the straight line as follows: Depreciation Expense=

Continuation Recognition of depreciation expense may be recorded using two methods: Direct Method • The method is accomplished by reducing direct fixed assets. • Example: • Car Depreciation Expense Rp. XXX • Car Rp. XXX Indirect Method • The method does not reduce directly the assets in question, but make accounter (contra account) by the name of accumulated depreciation. • Example: • Car Depreciation Expense Rp. XXX • Accumulated Depreciation Car Rp. XXX

Continuation Problems example : On January 1, 2006, the company bought a car worth Rp. 30, 000 with an estimated useful life of 3 years. After 3 years of use, the car is estimated to have a residual value of Rp. 15, 000. Answer : Indirect Method Direct Method 2006 Dec. 31 Car Depreciation Expense 507 Carl 108 5. 000 2006 5. 000 Dec. 31 Car Depreciation Expense 507 Accumulated Depreciation Car 108 5. 000

EXERCISES BALANCE SHEET 31, JAY’S SALON JANUARY 2013 ACC. NUMB ESTIMATE CASH TENT LEASE RECEIVABLE SUPPLIES OFFICE INVENTORY EQUIPMENT TENT EQUIPMENT PREPAID RENT ACCOUNT PAYABLE EQUITY MAKE UP REVENUE TENT LEASE REVENUE SALARIES EXPENSE ELECTRICITY EXPENSE WATER EXPENSE SALON MAINTENANCE EQUIPMENT EXPENSE TENT MAINTENANCE EQUIPMENT EXPENSE BUILDING MAINTENANCE EXPENSE TENT PAYLOAD EXPENSE OTHER EXPENSE Balance DEBIT BALANCE 169, 880, 000 10, 000 13, 500, 000 7, 500, 000 40, 000 50, 000 24, 000 7, 500, 000 1, 520, 000 650, 000 300, 000 500, 000 1, 500, 000 5, 000 332, 350, 000 CREDIT Prepare the adjusting entries from the following data: 24, 000 200, 000 79, 850, 000 28, 500, 000 332, 350, 000 • • • Supplies used Rp. 3, 500, 000 Rent paid on 1 August 2013 for one year Equipment is depreciated 10% annually Unpaid salaries amounting to Rp. 5, 000 Revenue that has not been paid by the customer Rp. 2. 000

Answer ADJUSTMENT JOURNAL ENTRIES J A Y’ S S A L O N JANUARI 31, 2013 in Rp, (000) DATE 2006 ACCOUNT 31 Dec. Supplies Expense Ref Debit 3. 500 Supplies 31 3. 500 Rent Expense 10. 000 Prepaid Rent 31 10. 000 Depreciation Equipment Expense 4. 000 Accumulated Depreciation Equipment 31 Salaries Expense 4. 000 5. 000 Salaries Payable 31 Credit Revenue Receivable 5. 000 2. 000 Service Revenue AMOUNT 2. 000 24. 500 24. . 500

ADJUSTED AFTER BALANCE SHEETS § As already noted, one purpose of making a trial balance is to facilitate the preparation of financial statements. This objective applies when the trial balance that is not yet require adjustment. If there any adjustments to the data in the trial balance, then we need a so-called trial balance adjusted trial balance. § Seetalah adjusted trial balance can be done directly from the ledger after adjusting entries posted to it. Another way is to create a trial balance before adjustment column, the column adjusting entries and trial balance columns after adjusting.

REPORTING STAGE COMPANY ACCOUNTING SERVICES

Worksheet 1. 2. 3. 4. Enter balances the ledger accounts into the columns of the trial balance. Incorporating adjustments into columns adjustments. Filling columns adjusted trial balance. Moving the amounts in the adjusted trial balance columns after columns into L / R (which is a nominal account) and the columns of the balance sheet (which is a real account)

The procedure makes Worksheets The purpose of the working paper: 1. Facilitate the preparation of financial statements. 2. Classify and summarize information-informasu of the trial balance and the adjustment data so that it becomes drafted preparation before the formal financial statements. 3. Easier to find errors that might do when making adjusting entries.

Forms and How to Resolve Working Paper WORK SHEET JAY’S S A L O N JANUARI 31, 2013 Numb Worksheet Account Name Acc. AJE Adjt. Worksheet Income Balance D C D C D C Rp. X Rp. V Rp. X Assets Liabilities Rp. X V V Rp. X Ekuity X V V X X Prive X V V X X Revenue X V V X X Expense X V V X X Accumulated Depreciation X V V X X X X V V X X Adjustment Account X X AJE X X Profit Balance

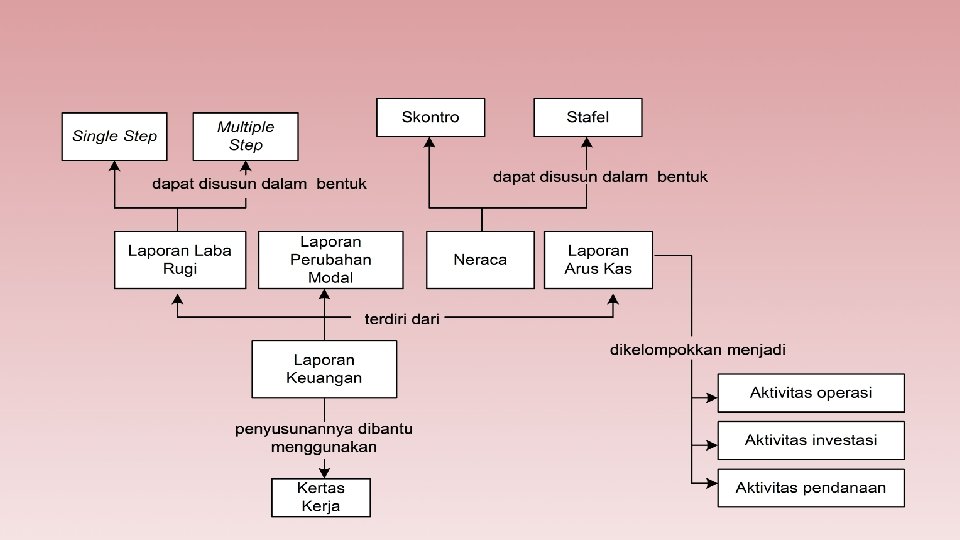

SERVICES COMPANY FINANCIAL STATEMENTS Income statement Statement of changes in capital balance Cash flow statement

Income statement An income statement is useful for: An income statement is a summary of income (revenue) and expenses (expense) for a period of time or a certain period, such as a month or a year. Determine the amount of income tax (the tax office). Assessing a company's success by counting profitablilitas company. Assessing the company's profit by comparing the last report period. Assessing the efficiency of the company by looking at the size of the load and compositing type of load.

Continuation Income Statement Single Step All types of revenues (revenues, non-trade income, and other income) compiled and summed up in one group, then diselisihkan the sum of all weights. The difference between the amount of revenues and expenses is the remainder of the profit or loss leftovers. Multiple Step Multiple step is the preparation of the income statement in stages starting from the group revenue and operating expenses, revenue load outside the business, up to group revenue and other expenses.

Continuation Form of Income Statment Single Step PT SEDAP Income Statment PER 31 DESEMBER 2004 (DALAM RIBUAN RUPIAH) Revenue : Services revenue xxxx Interest revenue xxxx total revenues xxxx Expenses : Rent Expenses xxxx salary expense xxxx Insurance Expense xxxx Expenses Electricity, Water. and Phone xxxx Total Expenses (xxxx) Net profit xxxx Information : C = A + B H = D + E + F + G I = C - H

Continuation Form of Income statment. Multiple Step PT SEDAP Income Statment PER 31 DESEMBER 2004 (DALAM RIBUAN RUPIAH) Service Revenues Expenses : Salary Expenses Electricity, Water. and Phone Total Expenses Operating profit Revenue outside the business: Interest Revenues Expenses outside the business: Interest Expenses Profit outside the business: Net Profit Information : E = B + C + D F = A - E J = F + I xxxx (xxxx) xxxx

Statement of changes in capital Statements of changes in capital presenting matters concerning: Statements of changes in capital is an overview of changes in equity or capital that occurred over a period of time or a certain period. This report was prepared only for the individual, and has nothing to do with the balance sheet and income statement. The amount of initial capital. Additions to capital, (investment) during the period. The rest of the profit or loss. Making money (prive) for personal gain.

Continuation Statement of changes in capital SALON LIA LAPORAN PERUBAHAN MODAL UNTUK PERIODE YANG BERAKHIR PER 31 DESEMBER 20 XX (DALAM RIBUAN RUPIAH) Rp. A Capital, January 1, 20 XX Net profit Prive Rp. B -C Additions (Deductions) Capital -D Capital, December 31, 20 XX Rp. E

balance Balance can be organized into two forms: Neraca merupakan suatu daftar berkaitan dengan posisi keuangan (aktiva, kewajiban, dan modal) pada tanggal tertentu, biasanya penutupan hari terakhir dari satu bulan atau tahun tertentu. Skontro shape is arranged side by side form of the balance between the left side (assets) to record the assets and the right side (liabilities) to record the liability (debt) and the capital. Number of the left side (assets) and the number of right-hand side (liabilities) must be balanced. Stafel shape is arranged in descending order from top to bottom. Top to record the treasures and the bottom to record debt plus capital. Total assets equal to the amount of capital plus debt. Stafel shape widely used for comparative balance sheet, which is to compare the balance sheet with the last period.

Continuation Bentuk neraca skontro COMPANY …………… NERACA PER ……………. (DALAM RIBUAN RUPIAH) Aktiva Current asset Liabilities Current liabilities ……………. . Rp. XXX ……………. . Rp. XXX …………………………. . XXX Total Current Assets Rp. XXX Total Current liabilities Fixed assets Rp. XXX Long-term liabilities …………………………. . Rp. XXX …………………………. . XXX Total Fixed assets XXX Total Long-Term Liabilities Total Liabilities Capital Total Aktiva Rp. XXX Capital XXX Total liabilities & capital Rp. XXX

Continuation Bentuk neraca stafel NERACA PER ……………. (DALAM RIBUAN RUPIAH) Aktiva Currente assets : ……………………. . Total Currente assets Fix assets : ……………………. . Total Fix Assets Total Aktiva Liabilities Current Liablities ……………………. . Total Current Liabilities Long term liablities ……………………. . Total Long term liablities Total Liabilities Capital…………………. . Total capital & Liabilities Rp. XXX XXX Rp. XXX

Cash flow statement Classification of cash flows consist of: The cash flow statement is a summary of cash receipts and disbursements for the period of time or a certain period, such as a month or a year. Operating activities: Direct Method Indirect Method Investment Activities Financing Activities

Definition of Cash Flow • Enterprises are encouraged to report cash flows from operating activities using the direct method. The reason, the direct methods generate information useful in estimating future cash flows, while today can not be produced by indirect methods.

Continuation Form of Direct Method Cash Flow Statement

Continuation Form of Statement of Cash Flows Indirect Method

Continuation Bentuk Laporan Arus Kas Masuk dan Keluar Aktivitas Operasi cash In Sales of merchandise Commission income, fees, etc. Interest income Cash out Payments to suppliers Employee salaries Payment of taxes Payments of interest and other expenses The profit and loss Investment Activities cash In Sales of fixed assets Cash out Purchase of fixed assets Posts Fix assets Financial. Activities cash In Acceptance Capital Acceptance of long-term loans Cash out Payment of long-term debt The posts are long-term liabilities and capital

PROCEDURE END CORPORATE SERVICES

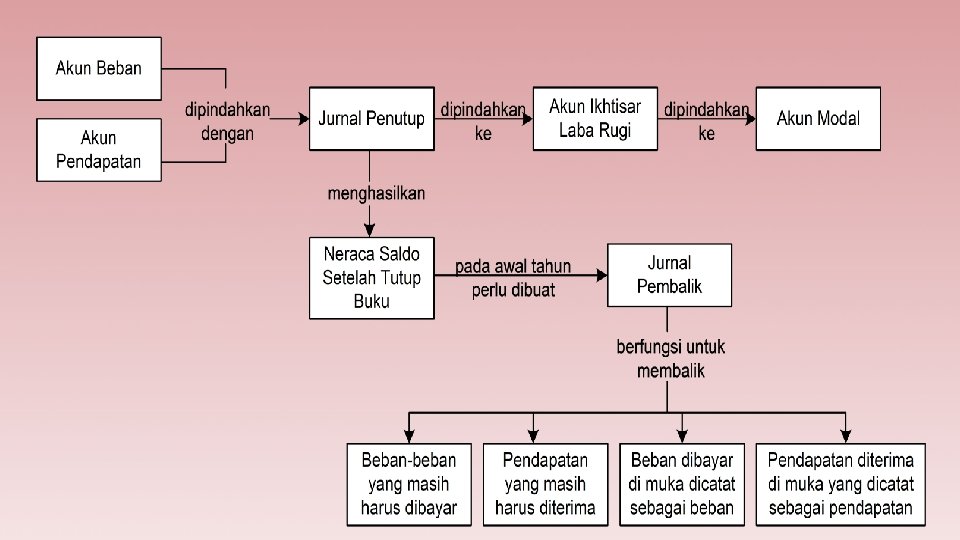

closure Bookkeeping • Journal Cover. Journal cover is a journal to move the accounts balance income and accounts of the load to the profit and loss account and then transferring the balance of the income summary account to the capital account. So we use a temporary account that is also new, the income summary account. This account is only used at the time of closing of books at the end of the period. Through the income summary account, all accounts balance income and accounts compiled load in order to obtain a figure which represents net income or net loss. And then this figure will be transferred to the capital account inverting.

Objective Closure 1. To cover the outstanding balance on the account temporarily. Said closing means reduce your account balance to be zero. All temporary accounts will thus start with a zero balance at the beginning of the next period. 2. In order for the capital account balance shows the amount in accordance with the circumstances at the end of the period. This journal covers makes capital account balance is equal to the final amount as reported on the balance sheet.

Steps to make journal covers 1. Close all account Revenues. All the Revenues account was closed by moving the balance of each account income to the income summary account. Consider the following closing entries : Revenues A Rp. XXX Revenues B XXX Income Summary Rp. XXX 2. Close All account Expenses. All expense accounts are closed by moving the balance of each account burden to the income summary account. Consider the following closing entries : Income Summary Rp. XXX Expenses A Expenses B Expenses C Rp. XXX

continuation 3. Close All acount Income Summary

continuation FORM OF CLOSSING JOURNAL Clossing Journal (IN THOUSANDS RUPIAHS) Page Date 2002 31 Des Closing Journal Income Summary Sallary Expenses Ref. 303 501 Electry Expenses etc. The closure of the account balance Expenses Service Revenues Income summary Closing of reveues account balance Income Summary Equity Nn. Lia The closure of the account balance overview profit and loss Equit of Nn. Lia Prive account closure 502 503 401 303 301 31 31 Account Debit Kredit 5. 750 1. 100 500 3. 000 9. 900 9. 000 4. 150 500

clossing Trial balance after • Closing trial balance is a list containing the real accounts along with the balance of each account are real, because nominal account has been closed. • The balance on each of the real account represents the balance for the next period.

Form Of Clossing Trial Balance SALON LIA Clossing Trial Balance PER 31 DESEMBER 2004 (DALAM RIBUAN RUPIAH) Halaman No. Akun Acoount Debit Kredit 101 Cash 102 Account receivable 103 Supplies 1. 000 104 Prepaid Rent 1. 250 105 Prepaid Insurance 111 Car 112 Equipment 113 Accumulated Depreciation Equipment 100 201 Account Payable 2. 000 202 Fees received in advance 4. 500 203 Accrued salaries 100 301 Equit Nn. Lia 21. 650 Total 11. 900 750 11. 000 2. 400 28. 350

Reversing entries • After the financial statements prepared journals and journal covers be established or maintained, the company at the beginning of next year feel the need to make adjustments back on some of the accounts that have been adjusted at the end of last year. Journal for this purpose called reversing entries. • Reversing entry not a necessity, but only to simplify the creation of the journal in question in the following year. In addition, the manufacture of reversing entries daat used to reduce the possibility of a mistake or recording at the time to journal the following year. • 1. 2. 3. 4. Here are the accounts that require reversing entries. These expenses are accrued. Revenues accrued. Prepaid expenses are recorded as expenses. Unearned income is recorded as income.

Dapat Juga Diakses : Play. Store : econosmart Web : www. e-conosmart. com