Wall Street to Main Street ACCA CPD Event

- Slides: 47

Wall Street to Main Street ACCA CPD Event 2 December 2008 Hamid Hamirani hamid@investvis. com

. Recap Extracts from Nov 2007 Presentation .

So What is Causing All This – What are the Consequences ? ? Collection of Thoughts 2 - Toxic – Credit Problem - 22 August 2007 The problem facing the US economy is that toxic waste has infiltrated the credit markets. Financial institutions are afraid both to lend and to buy financial paper, for fear that the borrowing or issuing institution has ‘unknown' amounts of toxic credit in its portfolios and may default on a loan or paper obligation.

So What Created this Toxic Waste – the Credit Crisis ? ? ? Yen Carry Trade: Up until last year Yen-bore was at Zero % - Hedge Funds, seeing no end to the Asset Boom ( Brain Child of Alan Greenspan ), borrowed in Japan, converted into $ introduced new financial products : derivatives , commercial paper and provided commercial banks and mortgage lenders the opportunity to pass their risk to the hedge funds and credit was given to many insecure and known credit-risk borrowers thus: the Sub-prime crisis. The liquidity was poured into investments in China ( Manufacturing ) and India ( Soft Skill Outsourcing ) creating the demand which led to a commodity price inflation and broke the conventional relationship between a US $ rise and commodity price inflation. Thus the US $ lost its natural hedging characteristics: this is critical for the currencies which remain pegged to the US $ - and therefore we are seeing a number of countries considering pegging to a basket of currencies as Kuwait did and as China is currently contemplating, resulting in further misery for the $

What are the Consequences of the Credit Crisis ? ? ØFinancial Institutes suffering leading to job losses & economy slowdown Citigroup Inc. , the world's biggest bank, may have losses from assetbacked bonds of as much as $13. 7 billion. The shares have fallen 17% in a week, and reached a 4 year low. Bank of America Corp. , the second-biggest U. S. bank, is expected to announce losses of $5. 4 billion, and JPMorgan Chase & Co. , the third-biggest, is expected to have lost $4. 1 billion. Merrill Lynch & Co last month reported $8. 4 billion write-down's in the third quarter “Annual Audited Accounts may further open up the can of worms”

What are the Consequences of the Credit Crisis ? ? The losses are resulting in job losses and a reduction in wealth: this is likely to further dampen the consumption leading to the economy slowing down. . ØGood Business Starved of Essential Finances: With the Credit Squeeze and most leading financial institutions not really knowing either their own potential risk or the others have seriously curtailed their lending and they are lending at a risk premium which is likely to effect good business. ØMortgages are not now easily available and the cost has gone up This is causing house prices to fall bringing more pressure on the economy. The rise in cost is resulting in many foreclosures which is leading to a slow down in consumption.

. The Root Cause… Lending Disaster – Short Term Profit Motives .

US Financial Crises – Enormous Changes in Lending Standards Underlying EVERYTHING -- housing boom and bust, derivative explosion, credit crisis -- is the enormous change in lending standards. After the Greenspan Fed took rates down to ultra-low levels, home prices began to levitate. More and more mortgages were being securitized -- purchased by Wall Street, and repackaged in forms of bond-like paper. The low rates spurred demand for this higher yielding, triple AAA rated, asset-backed paper. In this ultra-low rate environment, where prices were appreciating, and most mortgages were being securitized, all that mattered to the mortgage originator was that a BORROWER NOT DEFAULT FOR 90 DAYS (some contracts were 6 Months).

US Financial Crises – Enormous Changes in Lending Standards The contracts between the firms that originated mortgages and the Wall Street firms that securitized them had explicit warranties. The mortgage seller guaranteed to the mortgage bundle buyer (underwriter) that payments were current, the mortgage holders were valid, and that the loan would not default for 90 or 180 days. So long as the mortgage holder did not default in that period of time, it could not be "put back" to the originator. A salesman or mortgage business would only lose their fee if the borrower defaulted within that 3 or 6 month contractually specified period. Indeed, a default gave the buyer the right to return the mortgage and charge back the lender the full purchase price.

US Financial Crises – Enormous Changes in Lending Standards What did the rational, profit-maximizers do? They put people in houses that would not default in 90 days -- and the easiest way to do that were the 2/28 ARM mortgages. Cheap teaser rates for 24 months, then the big reset. Once the reset occurred 24 months later, it was long off the books of the mortgage originators -- by then, it was Wall Street's problem. This was a monumental change in lending standards. .

US Financial Crises – Enormous Changes in Lending Standards. It created millions of new potential home buyers. Why? Instead of making sure that borrowers could pay back a loan, and not default over the course of a 30 YEAR FIXED MORTGAGE, originators only had to find people who could afford the teaser rate for a few months. Greenspan believed the free market could self-regulate. (After all, people are rational, right? ). This would not have been possible without the Greenspan ultra-low rates, which made the teaser portion (the "2" of the 2/28) of these mortgages so attractive. One of the many odd lessons of this era is that, under certain circumstances, companies and salespeople will pursue short term profits to the point where it literally destroys the firm and possibly the country;

Asset / Liabilities Total US commercial mortgages $ 14 trillion so would $ 700 billion be enough? Total CDS US 55 trillion what happens if there are corporate defaults?

Another Way of Understanding Wall Street Failure Once upon a time in a village in India , a man announced to the villagers that he would buy monkeys for $10. The villagers seeing there were many monkeys around, went out to the forest and started catching them. The man bought thousands at $10, but, as the supply started to diminish, the villagers stopped their efforts. The man further announced that he would now buy at $20. This renewed the efforts of the villagers and they started catching monkeys again.

Another Way of Understanding Wall Street Failure Soon the supply diminished even further and people started going back to their farms. The offer rate increased to $25 and the supply of monkeys became so little that it was an effort to even see a monkey, let alone catch it! The man now announced that he would buy monkeys at $50! However, since he had to go to the city on some business, his assistant would now act as buyer, on his behalf. In the absence of the man, the assistant told the villagers: ' Look at all these monkeys in the big cage that the man has collected. I will sell them to you at $35 and when he returns from the city, you can sell them back to him for $50. ' The villagers squeezed together their savings and bought all the monkeys. Then they never saw the man or his assistant again, only monkeys everywhere! Welcome to WALL STREET.

Why the Global Equity Market Shall Remain Under Stress? Recession - Are equities really cheap? • 75% of the World GDP ( Advance economies ) are already in recession. • A dozen emerging countries are in a stage of seeking IMF assistance. IMF has only $ 100 billion. • Even China’s and Brazil’s economies are in stress. China’s growth is now 9%, considerably lower than what was expected; next year’s growth will drop to between 8 & 9%.

Why the Global Equity Market Shall Remain Under Stress? Deleveraging – Have the equities really bottomed out ? • Hedge Funds ( see separate slide ) • Recession creates risk for corporate failures which in turn risk CDS write off - Sony sales are the worst in 13 years. Fall in House Values – Reducing credit worthiness which is a lubricant to economy Securitization – Potential for more bad news – write offs Securitization was supposed to mitigate risk but all it did was earn a considerable amount of fees for all the intermediaries and only ended in transferring the risk to the final victim.

Why Global Equity Market Shall Remain Under Stress? Seizure of Liquidity – starving good business of credit & ST finances • Increase in counter party risk, uncertainty on CDS write offs, potential private equity LBO write off and hedge fund failures and seized inter bank lending - this is effecting good business access to credit and working capital finances, risking more economic down turn. • Unemployment Growing unemployment - 6. 1% in the US, expected to be 8% by the middle of 2009.

Why Global Equity Market Shall Remain Under Stress? Regulation - Reducing potential returns as leverage is regulated. Increase in regulation as shadow banking system cease to exist or comes under more regulation with higher capital adequacy ratios and increase in transparency in securitized instruments. Bottom Line – Lost Consumers US annual consumption $ 9. 5 trillion. Chin-india annual consumption $ 1. 6 trillion

Hedge Fund Risk – More Worse Time to Come of Equities Some 8, 000 hedge funds with more than $1. 7 trn (£ 1. 1 trn) in assets are “being caught in a vicious cycle” say Business Week’s Matthew Goldstein. Over the three months to September, another $179 bn was wiped off the value of hedge fund assets by falling asset prices, according to Hedge Fund Research. Spooked by the market falls, and keen to have ready cash at hand, investors have been pulling their money out at a rapid rate, with almost $31 bn being withdrawn over the quarter – which means hedgies need to sell more assets to repay clients. .

Hedge Fund Risk – More Worse Time to Come of Equities As the markets fall, lenders are also cutting credit lines to their hedge fund customers or are making ‘margin calls’, i. e. demanding that those funds come up with extra cash to back up their borrowings. As many as 30% of hedge funds will be shutting up shop “in a Darwinian process”, says Emmanuel Roman at GLF Partners, and the US authorities will force-feed regulation onto the rest: “there need to be scapegoats, and they are going to go hunt people”. That will make business even harder, and lead to even more forced selling. In London, out of 450 hedge funds, more than 100 could be at risk, says Miles Costello in The Times.

So how far can the S&P 500 possibly fall further ? The consensus estimates peg 2009 aggregate operating earnings for companies in the Standard & Poor's 500 -stock index at about $94 a share, according to Thomson Reuters. That figure assumes earnings growth both this year and next. If those estimates panned out, the S&P on Friday would have traded at what looks like a bargain multiple of about 9. 3 times forward earnings. Shift earnings to the lower end of the consensus range, about $75 a share, and the multiple rises to 11. 7 times.

So how far further can the S&P 500 can possibly fall further ? That still might seem cheap compared with multiples that often exceeded 20 times during the 1990 s. But it is well above trough valuations of about eight times seen during the depths of the 1970 s bear market, according to data from UBS. And the economic outlook, along with the unwinding of the credit bubble, means it is unlikely that earnings will increase this year or next. . Bears are well below the consensus in their answer. Barry Ritholtz, director of research at Fusion IQ, for example, says he reckons that 2009 earnings could drop to about $50 a share. In that case, even a multiple of 14 times would bring the S&P to about 750 -- nearly 15% below current levels. "

USA Macro Analysis Will the Stimulus Work Consumption remains down Q 3 to -3. 7% from the original estimate of -3. 1 Home prices (S&P Case Chiller ) down 23% from its peak – negative wealth effect can amount to a whopping $ 500 bn. Consider adding stock market losses to it? ? . Retail Sales were down by 15% during July – October. Commercial real estate can be the next shoe to drop the default can be around $ 800 bn CMBS usually follow the fate of residential mortgages with a 2 years time lag. Unemployment spooked in November with the 8 month continuous rise in unemployment expected to rise to between 8% and 9%. This would represent a drag in the economy.

USA Macro Analysis Will the Stimulus Work Declining orders for durable and capital goods indicating industrial production will decline significantly in 2009. This will result in a cut in corporate expenditure representing a further drag on consumption. Fall in energy prices will help to strengthen the dollar. Lack of capital outflow to Asian & developing markets and global demand destruction is likely to result in slow down of exports to destinations like Japan, Europe, Asia and Latin America • Can fiscal stimulus be implemented fast enough in an increasing political environment. • Cost of debt is rising at the same time of global slow down • How will it all be financed.

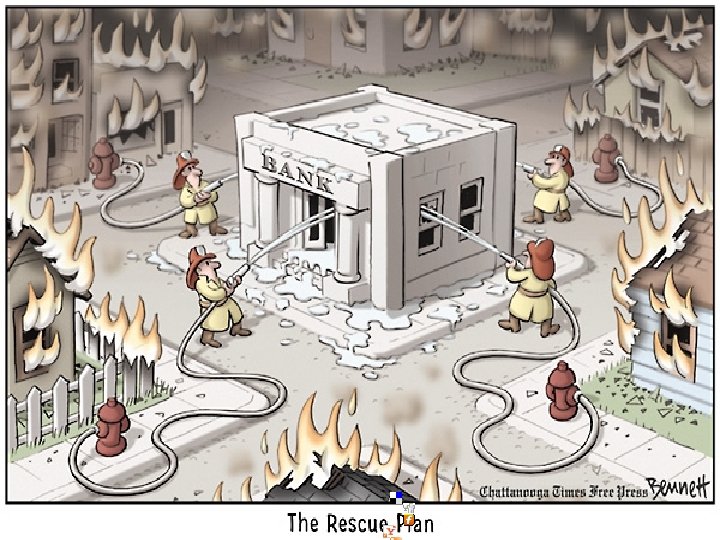

But All is not Gloom & Doom Stock / Sector selection is likely to be key for wealth management

So What is Next ?

Much of the Rest of the World May Follow America & Europe’s Footsteps Economists are lowering global growth estimates: 2009 E 2008 E 2007 A Euroland 0. 5% 1. 1% 2. 6% United Kingdom 0. 4% 1. 0% 3. 0% Japan 0. 5% 0. 7% 2. 1% China 8. 7% 9. 8% 11. 9% Brazil 3. 3% 5. 6% 5. 4% Key Factors Likely to suppress growths: • Decreased global liquidity. • Lower Capital Flows to emerging market • Reduced G-7 demand for imports • Lower demand for commodities

So What Lies Ahead for 2009 ? • Global Slow Down – growth estimates shall be further revised. Stagflation • Reduction in interest rates however spread would remain higher LIBOR loosing its benchmarking status • Regulations more for the buy side rather then sales side. • Fiscal stimulus and return of Keynesian Economy where Govt spending rises. • Rising Unemployment – More research and regulatory jobs – career prospects • Exchange Rate Volatility – Hedging demand is like to increase. • Consolidation Mergers & Acquisition – Bargain Valuations

So What Lies Ahead for 2009 ? • Change in Accounting Standards – Marked to Market Rules will be challenged • Social unrest– Geopolitical issues – Russia, Iran and Latin America – War generates growth potential • Commodity prices will act as a cushion • US deficit how it will be financed additional pressure: - Health care and ageing population • No more vendor finance so what would be financing based on geopolitical demand or higher interest rates • Strong Emerging Market Countries and the GCC will play an important role in stabilizing the world economy – China stimulus plan.

GCC Impact

How the GCC is likely to Fare… • No Recession fears for the GCC: growth expected to be around 4. 5% which is reasonable for the 33 million or so population. FIA may return for good returns. • 3 rd quarter results of Saudi & Omani Banks do not show any sign of stress. • The dollar liquidity squeeze will ensure projects are prioritized: it should result in projects of extreme national importance being given priority rather than investment hysteria into bricks and mortar Nakheel's decision to scale back work on Palm Deira • Cash surplus combined with low commodity prices provides an excellent opportunity for GCC to complete projects with relatively less cost.

How the GCC is likely to Fare… • Inflation will be checked, slow down will provide opportunities to align structural imbalances. • Loss of revenue in oil is to a larger extent compensated by a reduction in construction cost, deflationary pressures on wages and the strengthening of the $ and consequent increase in buying power • The oil price fall is likely to arrest or certainly delay capacity extension and alternative energy projects which were a real threat to the long term stability of oil prices. • The reduction in oil consumption will ensure that the life of the vital and finite asset will be extended for the future generation.

So Why Are The GCC Markets Are Falling? In general the GCC suffered from the triple whammy: 1. Liquidity dried up due to changes in reserve requirement for inflationary fears in Oman around US $ 500 million went out of the system. 2. FII withdrawals due to redemptions in their own backyards and due to unrealized expectations on currency revaluation. 3. Freezing of Inter-bank lending which prompted local banks to offer high fixed deposit rate to local depositor thus generating a switch in asset class from equities to deposits.

So Why Are The GCC Markets Are Falling? More recently due to the fear of local financial institutions exposed to toxic assets, global slow down and fall oil prices. More Specifically: 1. the real estate debacle in Dubai; corruption and fall in prices causing local banks to tighten the credit and increase in spread in Dubai around 700 basis points and lenders raising mortgage lending criteria's which puts further pressure on the real estate demand. 2. Oil prices fall in global slow down affecting the petrochemical industry basis of Saudi. So far the GCC has addressed the financial risk, but fiscal measures are required to address the economical risk. The market needs visibility of earning projections.

So Can China Make the Difference? Massive stimulus packaged of around $ 600 billion. Main spending includes public works, social welfare and tax reforms. • Public work spending areas are: public housing for poor households, infrastructure projects such as railways, roads, airports, power grid and earthquake repairs. • Tax reforms includes VAT reforms with estimated savings of 120 billion yuan. This will encourage capital spending by corporate businesses. • Social reforms include setting up minimum grain prices, increase in subsidies for farmers, social security benefits for low income groups, and increase spending on health and education. This should increase consumer spending as the above measures are likely to result in an increase in consumer disposal income.

So Can China Make the Difference? Factory closures are oversold. Most closures have been in the shoe and toy sectors which represent only 5% of China’s total exports. Factory closures are also due to relocation to inner china where cost are relatively still low. Export of machinery and transport equipment representing almost half of the total exports are up by 20% in volume in annual terms. The China housing bust is not as bad as the US. Total household debts are only 13% of GDP compared to the US 100%. Chinese buyers have had to put down a minimum deposit of 30%. Over the past year real income have risen to 10% in urban areas and 14% in the countryside. Retail sales rose by 17% in real terms in the year to October. Public sector debts represents only 20% of the GDP, surplus stands at 12% of GDP.

Final Words… No doubt we can be certain on the global slow down and financial crisis ( Wall Street ) turning into economic crises ( Main Street ). The US focus will shift from toxic assets to addressing the housing and lending crises which are the main drivers for all the gloom and doom. This is an “ Independence Day “ scenario where the whole world stands together from Mumbai to Shanghai ready with massive fiscal and monetary measures. The greatest fear is do we have enough time for all the measures to work before the social unrest further deteriorates and manifest into change in political uncertainties.

Final Words… Exchange rates and interest rates are likely to remain volatile. We can begin to see pressure building on dollar as the US bailout plan is financed and the interest rate option is not available at least in short to medium term. Commodity prices and energy prices should provide some cushion and inflationary pressure are likely to reside. Average growth of developing countries is likely to revert to the 1980 – 2002 pace of 3. 5 to 4%. For the GCC IMF forecasts 4. 5% growth for 2009. This is not too bad at a time when the US and much of the developed world faces an extended period of sub-par growth. This should increase the relative appeal of investing in the GCC and emerging markets in contrast to the 1980 s and 90 s when the US was growing at 3% and looked much less risky.

Final Words The views expressed in this presentation are purely of the presenter and does not represent the views of either the ACCA or Vision Investment Services. Disclaimer : This is an informative Seminar and needs to be used as such. The topic is dynamic and the Presenter shall not be held liable for any business decision taken based on this session. Each Business & individual makes their decision on specific circumstances and the business environment at the time of decision making.

Mr. Hamid Hamirani, FCCA +968 99359852 hamirani@accamail. com