Reporting Financial results on Financial statements Chapter 3

: � Transaction � The types of events for")

Accounts Receivable Supplies")

Revenues ……………………………… xxx Total Revenues")

: � BUSINESS ACTIVITIES � Classifying AND Cash")

")

- Slides: 41

Reporting Financial results on Financial statements Chapter 3 T. Haya Alajaji

Financial statement : � Balance sheet � Income statement � Statement of cash flows � Statement of retrained earning

Financial Statement Preparing income statement Classified income statement Balance Sheet Ch 3 Transaction Classified Balance Sheet Income Statment Preparing Balance Sheet

Objectives ( Balance Sheet ) : � Transaction � The types of events for transactions � Balance � sheet Classified Balance Sheet � Preparing a balance sheet

Transactions and other actives : � Business activities that effect the basic accounting equation � Are A = L + SE called Transactions

Transactions include two types of events : � External exchanges : There are exchanges involving assets, liabilities and stockholder equity that you can see between the company and someone. � Internal exchanges : these events do not involve exchanges with others outside the business but rather occur within the company itself.

Preparing a balance sheet

Preparing a balance sheet � Using the ending amount from each T-account you could now prepare a balance sheet � Before do this , it’s good idea to check that the accounting records are in balance by determining whether debits = credit

Balance sheet : Reports the amounts of assets , liabilities and stockholders equity of a business at a point in time. Classified Balance Sheet : A balance sheet that shows a subtotal for currents assets and current liabilities.

Classified Balance Sheet 1. Current Assets Cash and other assets that are expected to be converted into cash, sold, or used up usually within a year or less, through the normal operations of the business, are called current assets. � Cash � Accounts Receivable � Notes Receivable are written promises by the customer to pay the amount of the note and possibly interest at an agreed rate. � Supplies. � Prepaid expenses. � Accrued revenues.

Classified Balance Sheet 2 - Fixed Assets Property, plant, and equipment (also called fixed assets or plant assets) include assets that depreciate over a period of time. Land is an exception, as it is not subject to depreciation. � Equipment � Buildings � Land

Classified Balance Sheet 3 - Current Liabilities that will be due within a short time (usually one year or less) and that are to be paid out of current assets are called current liabilities. � Accounts � Wages payable � Interest payable � Unearned fees

Classified Balance Sheet 4 - Long-Term Liabilities not due for a long time (usually more than one year) are called long-term liabilities. � Short-term � Mortgages � Bonds notes payable

Classified Balance Sheet 5 - Owner’s Equity Owner’s equity is the owner’s right to the assets of the business. Owner’s equity is added to the total liabilities, and this total must be equal to the total assets.

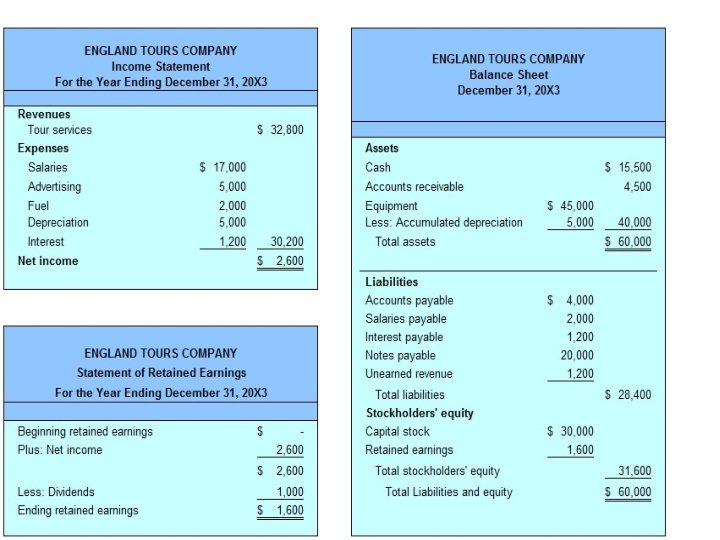

Company Name Balance Sheet Date Assets Current Assets Cash ……………………. . . Accounts Receivable …………… Notes Receivable ………………… Supplies ………………… Prepaid Expenses…………Total current Assets Fixed Assets Land …………………… Equipment ……………… Accum. Dep. – equipment …… Machinery ……………… Accum. Dep. – machinery …… Buildings ………………… Accum. Dep. – Buildings ……… Cars (automobile) ………………… Accum. Dep. – cars ……………… Total fixed assets ……………… Total assets ……………… Liabilities xx xx xx xx xx Current Liabilities Accounts payable ……………… Note payable ………………… Wages payable ………………… Interest payable ……………… Unearned fees ………………… Total current Liabilities ………………… xx xx xx Long-Term Liabilities Short-term notes payable …………… Mortgages payable …………… Bonds payable ………………… Loans ………………………… total. Long-Term Liabilities………… xx xx xx Owner’s Equity Owner’s capital ………………… xx Total Liabilities and Owner’s equity xx

Current Assets Cash Assets Accounts Receivable Supplies Prepaid insurance Total current assets Fixed Assets Land Equipment Accum. Dep. - equipment Total fixed assets Total assets Net. Solutions Balance Sheet December 31, 2011 2, 065 Liabilities Current Liabilities Accounts payable 900 2, 720 Wages payable 250 760 Unearned rent 240 2, 200 20, 000 1, 800 (50) 7, 745 Total current Liabilities Owner’s Equity Chris clark, capital 21, 750 29, 49 Total Liabilities 5 Owner’s equity and 1, 390 28, 105 29, 49 5

Exercise 1 : � complete the following table. � Indicate whether the account is classified as Current assets , noncurrent assets , current liabilities , noncurrent liabilities , or stockholder equity and whether the account usually has a debt or credit balance.

Account Land Retained Earning Notes payable (due in three years ) Accounts Receivable Supplies Equipment Accounts Payable Cash Taxes payable Balance sheet Classification Debit or Credit Balance

EXERCISE 2 : complete the following table Balance Sheet December 31, 2011 1000 Liabilities Current Liabilities Accounts payable 3000 500 Wages payable 1500 Supplies 2500 Unearned rent 1000 Prepaid insurance Total current assets Fixed Assets Land 3000 Total current Liabilities 5000 Owner’s Equity Chris clark, capital Equipment Accum. Dep. - equipment Total fixed assets Total assets 2000 (500) Current Assets Cash Assets Accounts Receivable Total Liabilities Owner’s equity and 8000

EXERCISE 3 : • From the following table prepare a classified Balance sheet at December 31 2013 Cash 3000 Accounts Receivable 5000 Supplies 5000 Inventory 4000 Accounts Payable 7000 2000 Note payable ( due 2013) 8000 Equipment 2500 Retained Earning 5000 Accum. Dep. – equipment 500 Loans 4000 Notes receivable ( due 2013) land 3000

Preparing a Income Statement

Objectives : � Income � The Statement. Three main sections statement. � Accounting � Preparing Methods Income Statement. of income

Income Statement � It called also the statement of operations. � It is reports the amount of revenues less expenses for a period of time. � The income Statement summarize the financial impact of operating actives under taken by the company during the accounting period. �A financial statement that measures a company's financial performance over a specific accounting period.

Income Statement include three main sections : 1 - Revenues. Amounts earned by selling goods or services. 2 - Expenses. Costs of business necessary to earn revenues 3 - Net income. The excess of revenues over expenses

Company Name Income Statement For The Period Ended (Date) Revenues ……………………………… xxx Total Revenues ………………………… Expenses ……………………………… xxx Total expenses ………………………… (xxx) Net income (or net loss) ……………… xxx

Expenses+Assets=Liabilities+Capital+Revenues Debit Accounts Credit Accounts If Debit, and if Credit If Credit, and if Debit Item Revenues Expenses Increase Decrease

Accounting Methods : 1 - Cash Basis Accounting : Reports revenues when cash is received and expenses when cash is paid. 2 - Accrual Basis Accounting : Reports revenues when they are earned and expenses are incurred regardless of the timing of cash receipts

Matching Principle : � The requirement under accrual basis accounting to record expenses in the same period as the revenues they generate not necessarily the period in which cash is paid for them. Expense Revenues

Netsolutions Income Statement For The Year Ended December 31, 2011 Fees earned …………………………… 16, 840 Rent revenue ………………………… 120 Total revenues …………………… 16, 960 Expenses: Wages expense ………………… 4, 525 Supplies expense ………………… 2, 040 Rent expense …………………… 1, 600 Utilities expense ………………… 985 Insurance expense ……………… 200 Depreciation expense ……………. . . 50 Miscellaneous expense …………… 455 Total expenses …………… Net income …………………………… 9, 855 7, 105

Exercise 1 : � Complete the following table by entering either debts or credit in each cell : Item Revenues Expenses Increase Decrease

EXERCISE 2 : � Complete the following : Company Name : Alaml Company Income Statement For The Period Ended (December 31 2013 ) Revenues ……………………………… 8000 Total Revenues ………………………… Expenses ……………………………… Total expenses ………………………… Net income (or net loss) ……………… 3000 ( )

Exercise 3 : From the following table prepare a Income statement at December 31 2013 Items Passenger ticket Revenues 10000 Onboard Revenues 8000 Ship expenses 1000 Selling expenses 1500 Wage expenses 4000 Income tax Expenses 1500

Objectives ( statement of cash flow) : � BUSINESS ACTIVITIES � Classifying AND Cash Flows CASH FLOWS

Business Activities and Cash Flows The Statement of Cash Flows focuses attention on: Operations Cash received and paid for day-to-day activities with customers, suppliers, and employees. Investing Cash paid and received from buying and selling long-term assets. 12 -35 Financing Cash received and paid for exchanges with lenders and stockholders.

Business Activities and Cash Flows Checking and Savings Accounts Cash Currency Cash Equivalents Highly liquid short-term investments within three months of maturity. 12 -36

Classifying Cash Flows 12 -37

Operating Activities Cash inflows and outflows that directly relate to revenues and expenses reported on the income statement. 12 -38

Investing Activities Under Armour’s 2008 Investing Activities 12 -39

Financing Activities Under Armour’s 2008 Financing Activities 12 -40

E 12 -7 Preparing and Evaluating a Simple Statement of Cash Flows (Indirect Method) Required: 2. Prepare a statement of cash flows using the indirect method. 12 -41