Chapter 9 Financial Statements Preparing Financial Statements Seventh

- Slides: 16

Chapter 9 Financial Statements

Preparing Financial Statements Seventh Step in the Accounting Cycle: provide information for business decisions owners managers investors prepared in ink or on computer

financial statements sole proprietorship 1. 2. income statement shows net income or net loss for period statement of changes in owner’s equity summarizes changes in owner’s capital as result of business transactions during period 3. 4. balance sheet reports on assets and financial claims to those assets (A=L+OE) statement of cash flows

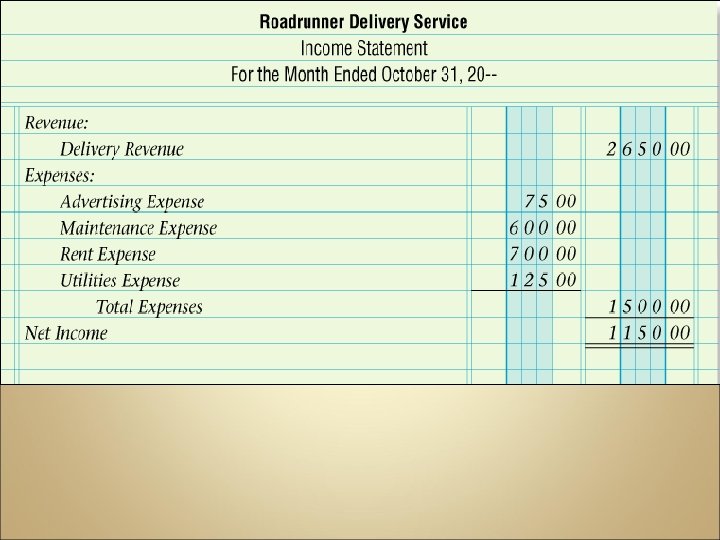

The Income Statement shows details about profitability income made or loss incurred in period Timeframe: for a specific period of time Source of Information: Income Statement Section of the Work Sheet

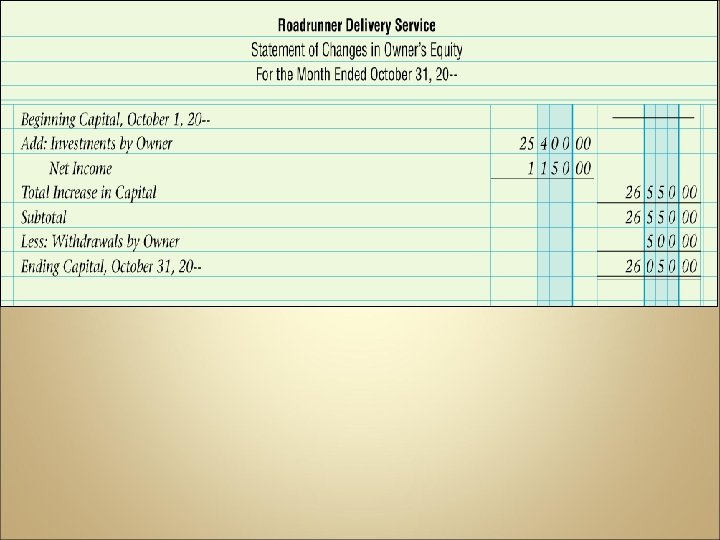

Statement of Changes in Owner’s Equity tracks increase/decrease in owner’s equity financial claims to assets of business

Stmt of Chng in OE Timeframe: for a specific period Sources of Information: Capital Account in General Ledger beginning capital and investments during period Income Statement net income of net loss Work Sheet withdrawals by owner

Trial Balance Capital – Investments During the Period -----------------------Beginning Capital Need to know ending capital in order to complete the next financial statement: the Balance Sheet.

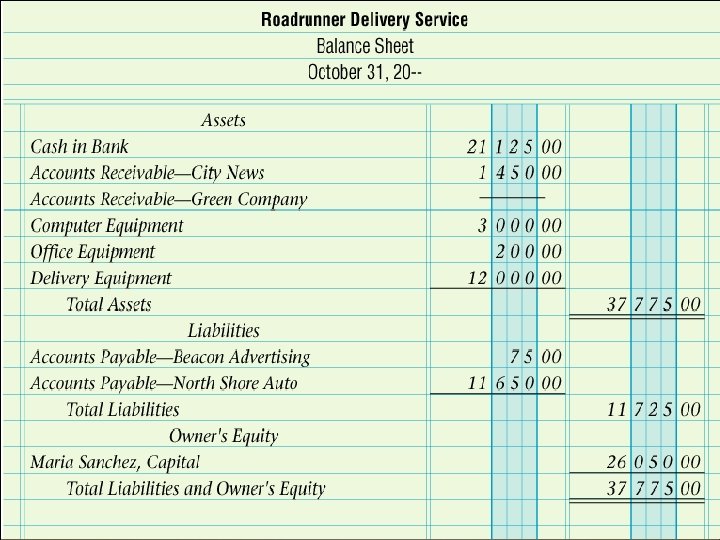

Balance Sheet report of balances in all permanent accounts assets, liabilities, and capital represents basic accounting equation; A=L+OE

Timeframe: as of a specific date Sources of Information: Balance Sheet Section of the Work Sheet Statement of Changes in OE. Report Form: Account classifications are shown one under the other with section titles centered

Ratio Analysis comparison of two amounts on financial statement evaluation of relationship between these amounts Used to determine financial strength activity debt-paying ability

Return on Sales: Determine the portion of each sales dollar that represents profit. Net Income / Sales = Return on Sales

Current Ratio: Relationship between current assets and current liabilities. Current Assets / Current Liabilities = Current Ratio

Quick Ratio: The relationship between short term assets and current liabilities. Cash and Receivables / Current Liabilities = Quick Ratio