Financial reporting financial accounting Financial reporting financial accounting

Фінансова звітність")

is the collection and presentation of data for use in")

- Slides: 16

Financial reporting (=financial accounting) Фінансова звітність

Financial reporting (=financial accounting) is the collection and presentation of data for use in financial management and accounting

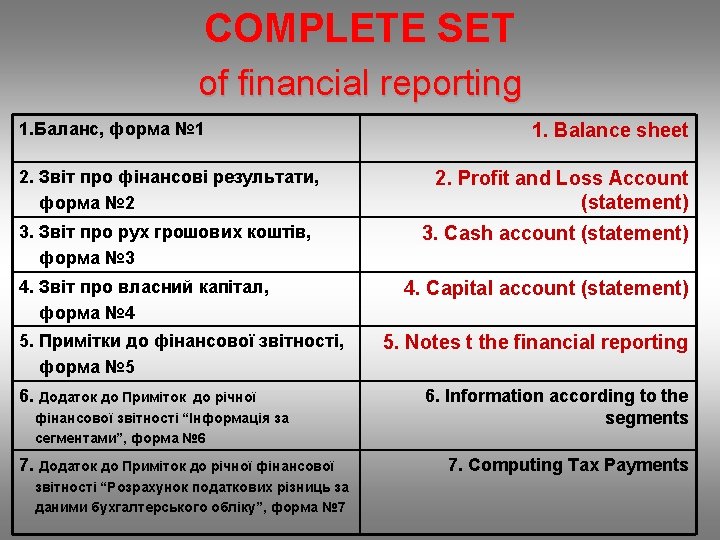

Financial reporting is dependent on the type of the enterprise 1. Small legal entity 2. Other enterprises 3. Holding company (middle and large) (суб’єкт малого підпртиємства) (інші підприємства) (материнські компанії) is required to present SIMPLE financial reporting COMPLETE SET of financial reporting CONSOLIDATED financial reporting

SIMPLE financial reporting 1. Баланс, форма № 1 2. Звіт про фінансові результати, форма № 2 1. Balance sheet 2. Profit and Loss Account (statement)

Balance sheet is in two parts: Assets Liabilities What are assets? What are liabilities? I. Fixed assets: Building Plant & equipment Transport Assets leasing to third parties I. Capital: Share capital II. Current assets: Stock Debtors Bank balance Cash Investments Total: II. Current liabilities: Creditors Loans Overdrafts Taxation Total:

Profit & loss account INCOME n Sales EXPENDITURE n Raw material purchases n Depreciation n Salaries and wages n Transport expenses n Distribution n Administrative expenses n Tax n Dividend on ordinary shares Total

The following institutions are interested in financial information of individual business: 1. Managers • 2. The State l. To 3. Investors 4. Employees 5. Trade unions 6. Creditors To plan, organize and control resources levy taxes on businesses W l. For the purpose of economic planning and h forecasting a l. To make informed judgments about future t investments and existing investments f l. For a profit sharing o l. For the company itself to involve its employees in r the running of the enterprise l. For wage negotiations l. To assess the risk in offering credit l. To safeguard against fraud

What is Financial reporting? Financial reporting is the collection and presentation of data for use in financial management and accounting What are the forms of financial statement? 2 major forms of financial statement are The balance sheet the profit and loss account (= income statement)

What is the balance sheet? What does the balance sheet show? The balance sheet is a summary of a firm‘s financial position at the end of an accounting period (one year). The balance sheet shows the state of a company‘s finance at a certain date.

What are the parts of the balance sheet? Balance sheet is in two parts: Assets What are assets? I. Fixed assets: • Building • Plant & equipment • Transport • Assets leasing to third parties II. Current assets: • Stock • Debtors • Bank balance • Cash • Investments Total: Liabilities What are liabilities? I. Capital: • Share capital II. Current liabilities: • Creditors • Loans • Overdrafts • Taxation Total:

Balance Sheet at 31 Dec 2003 ASSETS LIABILITIES Fixed assets Buildings Plant and equipment Transport Assets leased to third parties Current assets Stock Debtors Bank balance Cash Investments Total Capital Share capital 50 Current liabilities Creditors Loans Overdrafts Taxation 45 10 86 27 Total 218 550 253 102 12 43 116 34 25 20 1155

What is the double-entry book-keeping? Double-entry book-keeping is the accounting system in which every business transaction is recorded in 2 entries, a debit and a corresponding credit. Since every debit entry has an equal and corresponding credit entry, if follows that if the debit and credit entries are added up they will come to the same figure, i. e. BALANCE.

What is the profit & loss account? What does the P&L account show? The profit & loss account (= income statement (Am)) is a statement of a company‘s expenditure and income over an accounting period of time (usually 1 year), showing whether the company has made a profit or loss. The profit & loss account shows the movement which have taken place since the last balance sheet.

Profit & loss account at 31 Dec 2003 INCOME Sales EXPENDITURE 837 Raw material purchases Depreciation Salaries and wages Transport expenses Distribution Administrative expenses Tax Dividend on ordinary shares 255 28 37 43 15 58 127 20 Total 583

What institutions are interested in financial information of individual businesses? The following institutions are interested in financial information of individual business: 1. Management • To plan, organize and control resources; 2. The state 3. Investors 4. Employees 5. Creditors (banks & suppliers) W H A T F O R ? • The state requires public companies to be • accountable and present their accounting information (a balance sheet, a profit and loss account, a directors‘ report, and on the account where necessary) • To levy taxes on businesses • For the purpose of economic planning and forecasting • To make informed judgments about future investments and existing investments • For those involved in a profit sharing or share ownership scheme • For trade unions in planning wage negotiations • For the company itself to involve its employees in the running of the enterprise • To assess the risk in offering credit • To safeguard against fraud