Productivity and Quality Management Tenth Lecture Summary Productivity

• Integrated audit approach • Includes diagnosis and monitoring")

• Qualitative assessment • Industry Performance Appraisal")

• Involves analyzing specific profitability and productivity ratios derived from")

for the past periods (a")

• • o If ROA trend is decreasing or constant:")

Total assets turnover = o (b)")

of return")

How to conduct CPA?")

o (b) o (c) o (d) o (e)")

By type of")

is decreasing which means that profitability ratios should")

• Usually done by an external firm or consultant. • Is")

are not sure where")

- Slides: 52

Productivity and Quality Management Tenth Lecture

Summary • Productivity indices help us to evaluate economic performance and the quality of social and economic policies. • Productivity Analysis helps identify factors affecting income and investment distribution within different economic sectors, and helps to determine priorities in decision making. • In enterprise, productivity is measured to help analyse effectiveness and efficiency. • Its measurement can stimulate operational improvement

Summary • • Performance and Productivity Public and Private Organizations Some reasons for Performance Major Performance Challenges – Stakeholders – Organizations – Projects – People

QUICK PRODUCTIVITY APPRAISAL

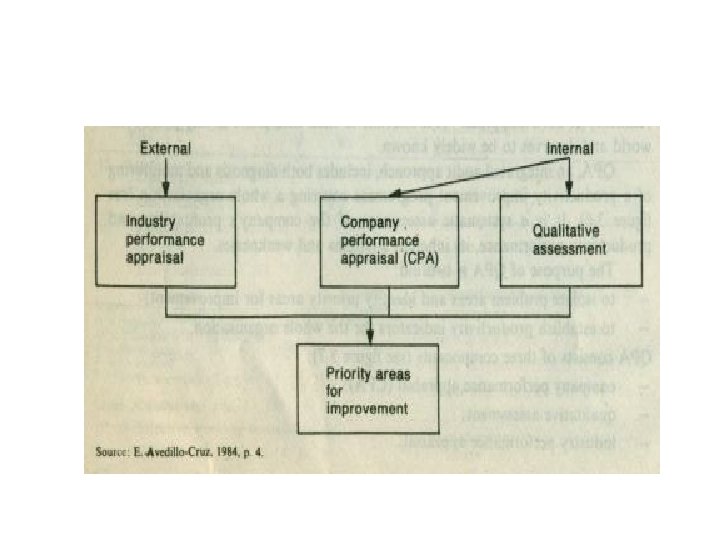

Quick Productivity Appraisal approach (QPA) • Integrated audit approach • Includes diagnosis and monitoring of a productivity improvement program covering a whole organization.

Purpose of QPA • To isolate problem areas and identify priority areas for improvement • To establish productivity indicators for the whole organization

Components • Company Performance Appraisal (CPA) • Qualitative assessment • Industry Performance Appraisal

Company Performance Appraisal (CPA) • Involves analyzing specific profitability and productivity ratios derived from financial statements. • In conducting CPA, two main comparisons have to be made: o between current performance and a previous base performance o between actual and desired performance (target)

Profitability • Profitability is defined as the change in output value compared with change in input value

Productivity • Productivity is the change between o quantity of output and / or quantity in unit price oand change in unit cost.

Performance ratios • Performance ratios classified as: o change in profitability, o change in productivity, o change in price recovery.

Steps • Step 1: Compute return on assets (ROA) for the past periods (a year, a quarter, a month) as net profit over total assets. • Step 2: Determine the trend of return on assets

Step 3: (Branch A) • • o If ROA trend is decreasing or constant: Compute primary profitability ratios (a) o (b) o (c) o (d) • Determine trends (increasing, decreasing or constant)

Cont… • Compute secondary profitability ratios: o (a) Total assets turnover = o (b) Accounts receivable turnover = o (c) Fixed assets turnover = o (d) Inventory turnover = • Determine trends • Perform step 6

Step 4 o If ROA trend is increasing, compute growth rate (GR) of return on assets (ROA) o GR = x 100%

Step 6 • Compute primary productivity ratios: • Total productivity = • Labour productivity o (a) o (b) o (c)

Steps in Company Performance Appraisal (CPA) How to conduct CPA?

Cont… • Capital Productivity o (a) o (b) o (c) o (d) o (e) • Determine trends

Cont… • Compute secondary productivity ratios: • Labour productivity o (a) By type of worker: o (b) By shift: o (c) By functional area :

Qualitative assessment ROA GR 1 2 3 4 5 0. 018 0. 026 0. 028 0. 035 0. 043 44% 8% 25% 23% TREND

Cont… • The example represents financial data for the past five years. Return on assets has increased. • It is necessary to compute the growth rate in order to determine which type of ratios to calculate first – profitability or productivity.

Cont… • The growth rate (GR) is decreasing which means that profitability ratios should be considered first. • Whenever the basic ratio, ROA or its growth rate is decreasing or constant, profitability ratios must be computed prior to productivity analysis.

Break-down • For analysis, net profit to net sales is broken down into o cost of goods sold ratio, o operating expenses to sales, o interest expenses to sales. • Total assets turnover is broken down into o accounts receivable, o inventory, o fixed assets.

Cont… • If assets turnover is decreasing, it will lead to a drop in ROA. • If this happens, a breakdown must be made of different assets comprising total assets turnover: o accounts receivable o Inventory o fixed assets

Cont… • A decreasing trend in accounts receivable turnover maybe due to the credit and collection system of the organization. • From the analysis of profitability trends it can be inferred that a decline in ROA trend may be due to either costs or asset turnover or both

Industry Performance Appraisal • An external industry performance appraisal can be made by: o analyzing the same indices for an individual enterprise o or the sum of individual enterprise assessments can also be used for an industry performance appraisal.

Inter-firm Comparison (IFC) • Usually done by an external firm or consultant. • Is an exchange of information regarding: o Costs o Performance o Efficiency etc. • Organizations engage in IFC in order to improve their productivity and profitability.

Objectives of IFC • to show the management how its firm’s performance compares with that of similar firms • to draw management’s attention to areas of comparative weakness and strength within the business • to give management an objective basis for judging progress and effectiveness.

Cont… • It is a powerful tool for comparative performance analysis and usually uses the same statistics as conventional productivity measurement.

Problems of Productivity Analysis The problems and difficulties in productivity analysis falls into two main categories: • Techniques of productivity measurement – Concerned with the organization – No single universal measure of productivity – Diverse business, different goals and objectives

Technical productivity measurement problems The most common problems which the designers of particular productivity measurement systems should take into consideration are: • How to combine different type of input into one acceptable denominator • How to deal with qualitative changes in input or output over time • How to keep input and output measurements independent of each other

Examples • An example of incorrect measurement would be if hospital managers considered productivity to be bed-days used per patient-year; the incorrect measure should be the weighted number of patients treated, where the weighting represents the seriousness of the illness. • Some organizations focus all their attention on the productivity of one particular section. • Another mistake, especially in public offices, is when managers confuse activities, output and results. For example, in training programs an incorrect measure would be the number of people trained; the correct one who would be the number of trainees who were placed in jobs or who improved their performance.

Complications It should be remembered that some significant changes over time complicate measurement. Among these are: • Major changes in plant facilities, wage rates, material costs, product prices, or even in accounting practices; • Purchase of more fabricated components; • Addition of more automated equipment; • Increase in machine speeds without additional labour; • Expansion of capacity through technological innovation; • Change in output which cannot be quantified by the old measure.

Sound Productivity Measurement System Here are few important characteristics of a sound productivity measurement system which would help to avoid the above-mentioned problems and mistakes: • • Provide simple and unambiguous signals to improve performance (productivity, profit, quality); Break down change in profit to reflect the contribution from each resource used in production (labour, capital, materials, energy); Break down the contribution to profit change from each resource into productivity terms and a price recovery term. This will isolate the effect of disparate change in productivity vis-à-vis resource price; Resources as a percentage of costs: amount of costs associated with each of the component resources as a proportion of total cost. In selecting a method of productivity measurement, feasibility and costs are major concerns.

Cont… • Use the price recovery term to evaluate whether productivity loss or gain for a given resource is appropriate; • Transform the above measures of change in profit into corresponding measures of change in profitability, change in cost per unit of output, and change in performance index number (e. g. productivity index numbers); • Provide consistent signals for profit improvement regardless of the units in which the measure is expressed.

Implementing Measurement Technique The implementation of a productivity measurement technique involves several steps: • Making the decision to measure productivity • Defining the target organizational system and the required level for intervention • Defining the measurement time period • Selecting the measurement technique • Using the measurement technique

Cont… To choose a specific measurement technique a number of variables should be considered: • Purpose and audience: what the measure is supposed to do and who will use it • Commitment to measurement: the extent to which an organization sees productivity measurement as a critical part of its effort to remain competitive • Awareness/understanding of management: the extent of management understanding/awareness of productivity measurement systems • Centralization/decentralization: the extent to which measurement control systems are part of the organizational culture

Cont… • Management style: measurement techniques should complement and extend the existing management style • Output variability: the extent to which the physical characteristics of the output change over time • Type of technology: ranges in manufacturing technology where input and output may vary considerably over time

Cont… • Process cycle time: length of time for one unit of output to be produced • Controllability: the extent to which management can “manage” or control input levels • Resources as a percentage of costs: amount of costs associated with each of the component resources as a proportion of total cost. In selecting a method of productivity measurement, feasibility and costs are major concerns.

Organizational Productivity Measurement Problems • There a number of potential sources of concern about and sometimes even fear of productivity measurement both for managers and for workers

Potential misunderstanding and misuse of measurement • The fear of many workers that managers who are not intimately involved with the work process will exaggerate or otherwise misinterpret the changes or trends in measurement data.

Exposure of inadequate performance • Since many workers (especially white-collar) are not sure where they stand with their boss, a measurement system that would clarify the situation may pose a threat.

Additional time and reporting demands • A frequently stated fear of productivity measurement is that it will increase the paperwork and take too much time.

Reduction in staff • There are obvious relationships between productivity and the staffing level, since one of the important benefits of productivity measurement is to maintain more rational staffing. Therefore, fears will be raised that the productivity data will be used as an excuse to cut staff. In this case there will be little co-operation form workers in productivity measurement.

Reduction of autonomy • Individuals staff members differ in terms of their desire for autonomy. Introduction of tighter management controls as a result of productivity measurement may be seen as a constraint.

Conclusion • Many of the perceived threats are result of problems in the organization that need to be understood and resolved. • Managing the introduction of a productivity measurement process involves managing resistance to change.

Summary • Quick Productivity Appraisal – Integrated audit approach – Includes diagnosis and monitoring of a productivity improvement program covering a whole organization • • Steps in Company Performance Appraisal (CPA) Problems of Productivity Analysis Misunderstanding of Productivity measurement Sound Productivity measurement system

Improving Productivity