IPOs IPO Anomalies and Stylized Facts Underpricing On

- Slides: 32

IPOs

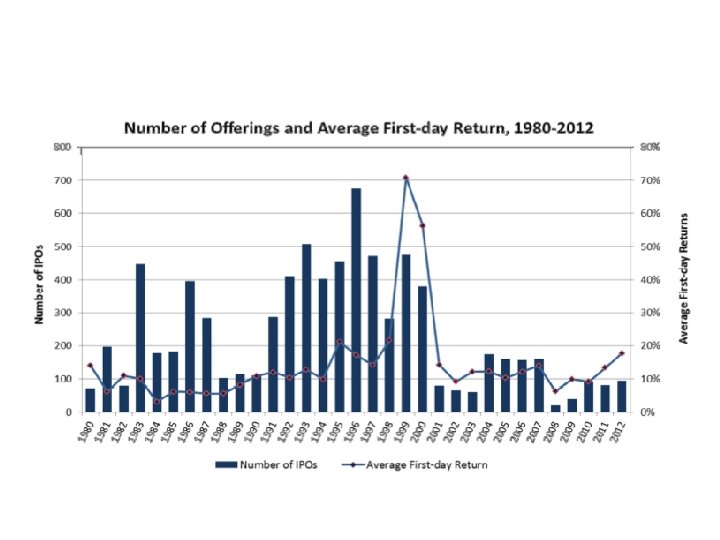

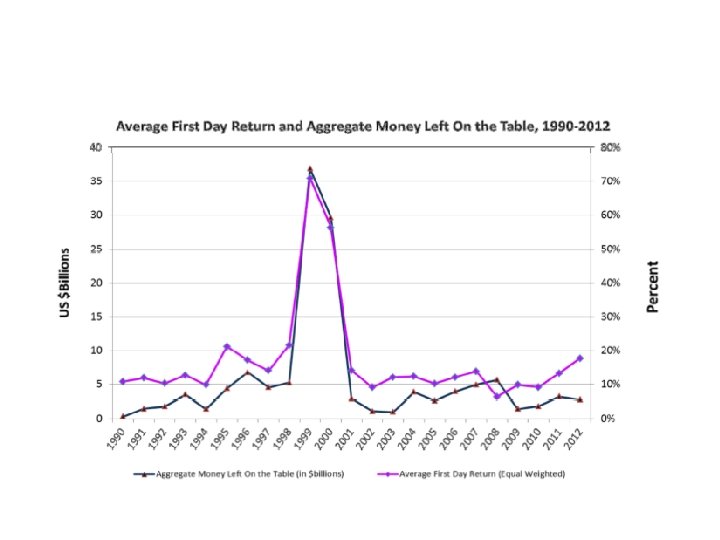

IPO Anomalies and Stylized Facts • Underpricing – On average IPO shares are underpriced in the market (18%). • Aftermarket Price Stabilization – Underwriter sells more shares than they buy (Aggarwal 2000). • Strong demand? Cover short position via overallotment option. • Weak demand? Cover short position via open market purchases. • IPO Lockups – Information Asymmetry? – Moral Hazard? • Waves (Lowery and Schwert 2003, Loughran and Ritter 2002) • Long-run (under)performance – Ritter (1991), Barber and Lyon (1997), Gompers and Lerner (2001)

Benveniste and Spindt • Point out that there are two types of asymmetric information of concern in the IPO process – Between the firm and the market • Certification role • Underwriter reputation backs this role – Between different types of investors • Bookbuilding process • Investors have little incentive to reveal positive information • Underwriter being a repeated player in the market is important here as well

Benveniste and Spindt • Underpricing combined with differential allocation is used to provide informed investors with the incentive to truthfully reveal positive information. – Underpricing provides a benefit to receiving an allocation. Payment for truthful disclosure. – Skewing the allocations to investors in the “premarket” who reveal positive information and away from those who reveal negative information makes truthful revelation incentive compatible and can help minimize underpricing. – This is how Benveniste and Spindt model the roadshow and the bookbuilding process that characterize the actual IPO procedures in the US.

Benveniste and Spindt • Empirically: – Underpricing is directly related to the ex ante marginal value of private information. – Underpricing is directly related to the level of interest in the premarket. – Underpricing is directly related to the level of presales. – Underpricing is minimized if priority is given to orders from investors who indicate good information.

Litigation • Litigation risk: – Underpricing has been conjectured by Ibbotson 1975, Tinic 1988, Hughes and Thakor (1992) to be a form of insurance against future litigation. – Section 11 of the securities act of 1933 gives investors the right to sue issuers and underwriters for declines in value below the offer price if there are material omissions in the prospectus. – The inherent uncertainty of IPO pricing and the potential reputational losses associated with litigation suggest that issuers and underwriters may attempt to hedge litigation risk by underpricing.

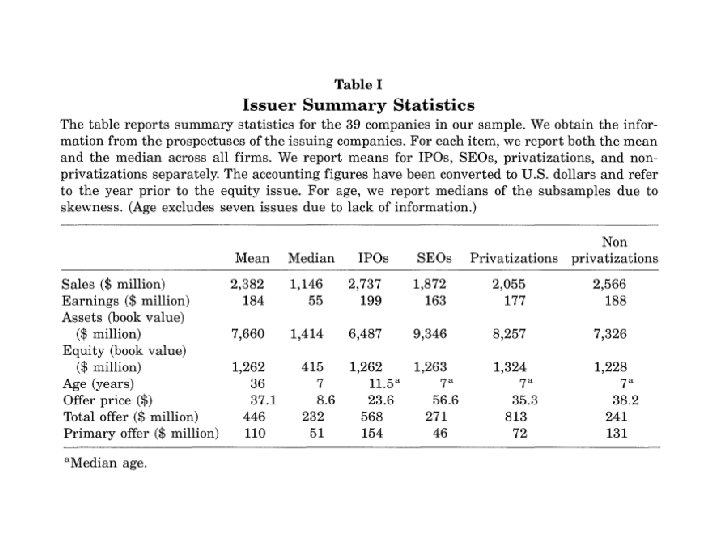

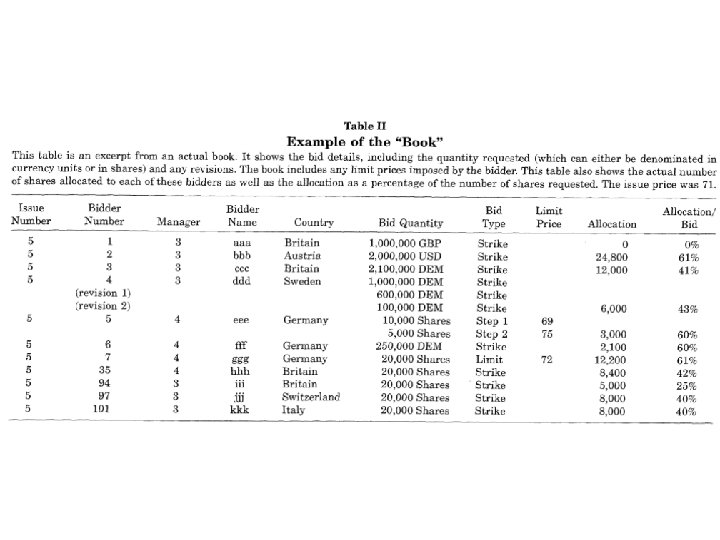

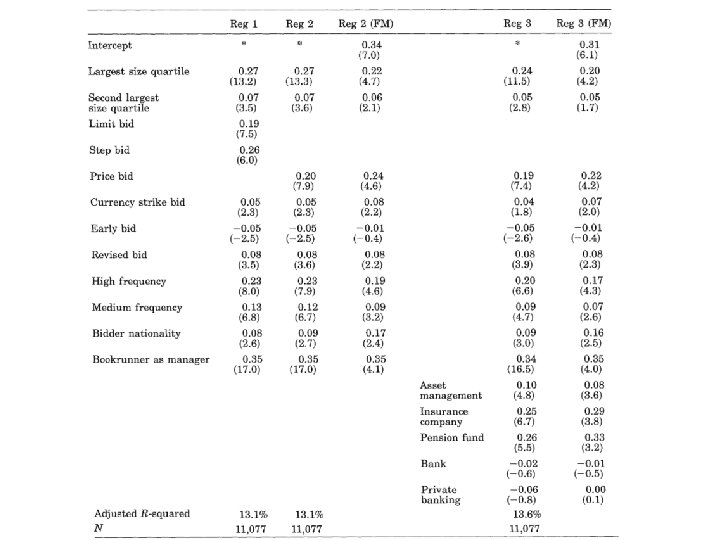

Cornelli and Goldreich 2001 • Data on “books” and allocations for 39 international equity offerings (23 IPOs and 16 SEOs) from 1995 - 1997. – They can study how information is provided by investors in the indications of interest. – They can also study who gets what and why.

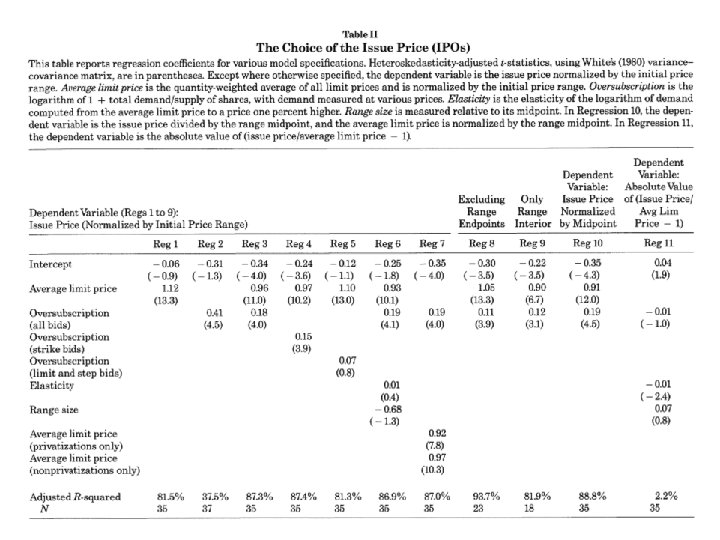

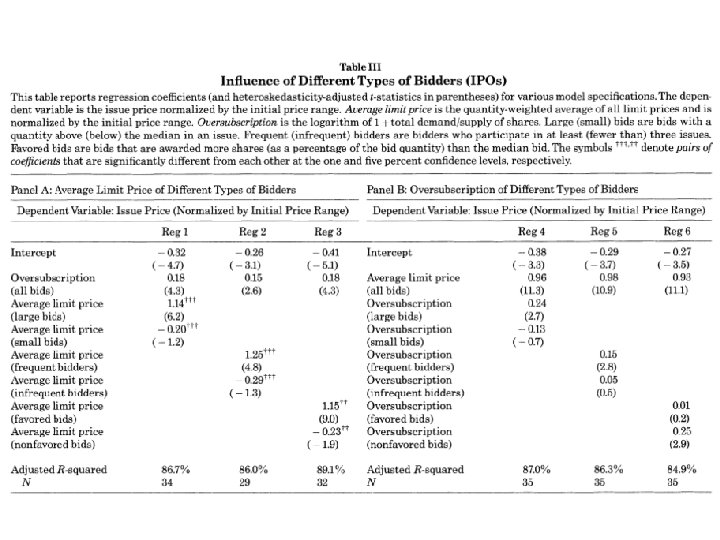

Cornelli and Goldreich 2001 • Bids – A strike bid is a request for shares regardless of the issue price – A limit bid specifies the maximum price that the bidder is willing to pay for the shares – A step bid is a demand schedule submitted as a step function

Allocations • Strike bids for fixed quantities of shares reveal no information on pricing the issue. – If all bids were strike bids for a fixed quantity of shares the demand curve would be perfectly inelastic. • Limit bids revel information – Limit bids provide specific information on the elasticity of demand. – They also put the bidder at risk: • If the limit price is too low, the issuer may set the price higher and the bidder receives no allocation. • If the limit price is too high, the issuer may raise the offer price and the bidder receives an over-priced issue. • A testable implication of the information extraction theories is therefore that limit bids should see favorable allocations.

Allocations • Beatty and Ritter 1986: riskier issues are more underpriced. – Pooling offerings allows the underwriter to reduce average underpricing. – Underwriter uses his discretion over allocations to enable him to pool offerings (Benveniste and Spindt). – Underwriter should discriminate in allocations based on past participation in offerings. – Frequent investors should not receive higher returns on average as they are simply being compensated for buying less successful offerings.

Allocations • Welch 1992: informational cascades – Underwriter may attempt to encourage early demand for shares by informed investors as this may encourage other investors to follow. – Requires that the underwriter “hint” at the early demand to investors. – Underwriter may give larger allocations to early bids as the “encouragement. ”

Allocations • Other predictions: – Ownership distribution – spread ownership to increase liquidity and so favor investors who demand a smaller number of shares (Brennan and Franks 1997) or look to build blockholders. – Issuer or the investment bank may prefer investors from the issuing firm’s country or it may prefer a widely dispersed set of equityholders. – Lead underwriter may favor investors who place bids directly with them.

Results

Profits

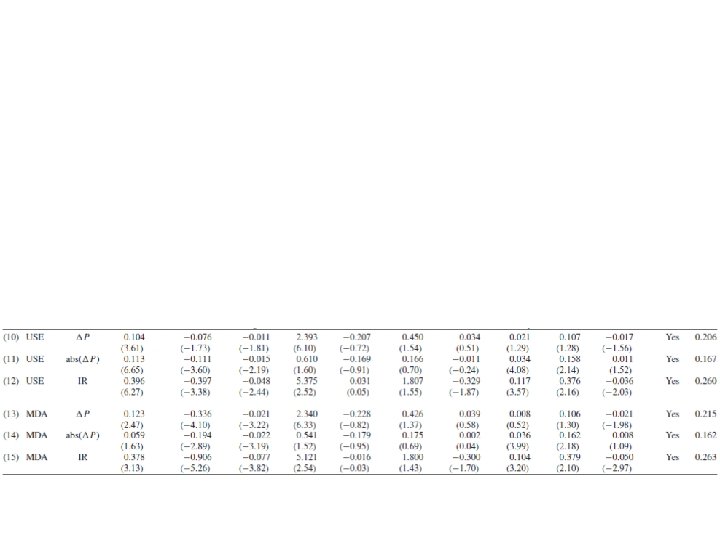

Hanley and Hoberg 2010 • The underwriter may expend resources prior to filing the prospectus with the SEC to collect information about the offer and use this to set the initial price range. • However, the information will be believed only to the extent it supported by informative disclosure in the prospectus and during the road show. • This disclosure may itself have a cost for some firms as it may reveal strategic or proprietary information to rivals.

Hanley and Hoberg 2010 • Alternatively, the underwriter and the issuing firm may rely on the information produced by investors during the bookbuilding period. • Investors must be compensated for gathering and revealing valuable information. • There is then a tradeoff between the cost of gathering and revealing information in the prospectus and gathering information during the bookbuilding period. • They examine whethere is evidence of this tradeoff and evaluate its impact on IPO pricing.

Hanley and Hoberg 2010 • Cannot measure the amount of premarket information gathering. Instead they consider disclosure in the prospectus. • Decompose the initial IPO prospectus into standard content and informative content. – Standard content is exposure to information that is already contained in recent and past industry IPOs. – Informative content is the residual. • Greater information gathering and revelation should result in more content that is unique to a particular IPO.

Hanley and Hoberg 2010 • To the extent it is efficient, greater information gathering in the premarket period should result in more accurate initial offer prices relative to the final offer price before bookbuilding begins and so reduce the need for information gathering during bookbuilding. – Offers with greater informative content will have smaller absolute changes in offer prices relative to the initial price range. – Offers with greater informative content will have lower underpricing.

Hanley and Hoberg 2010 • Use algorithms to gather prospectuses and to sort the texts into “normalized word vectors” that can be compared across IPOs. • Consider the total prospectus as well as the four main sections: Prospectus Summary, Risk Factors, Use of Proceeds, Management’s Analysis and Discussion. • Use a measure of “document similarity” to decompose “standard” content (similar to recent prospectuses from the same underwriter and similar to past prospectuses in the same industry) and content that is not similar (informative content).

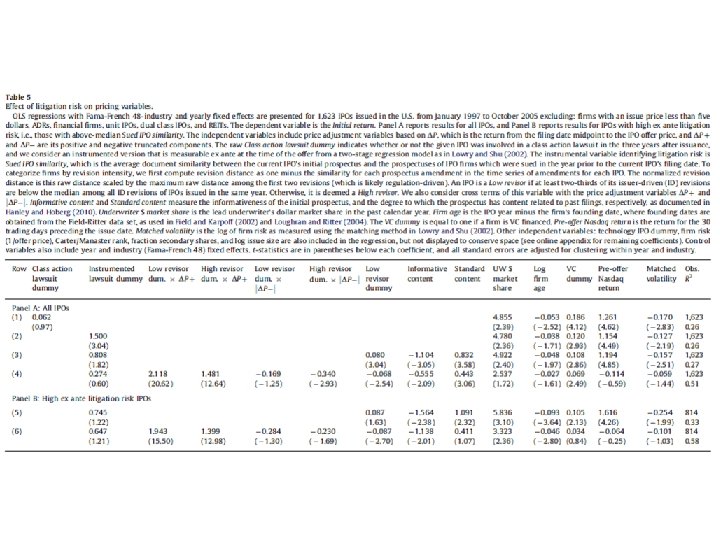

Hanley and Hoberg 2012 • Litigation Risk – Section 11 of the Securities Act requires a loss and material omissions in the prospectus. – Disclosure and underpricing are substitute hedges against liability risk. – They use a similar methodology as in the last paper to study this tradeoff and its impact on IPO pricing. – Cannot measure a “material omission” but they can examine the extent to which the disclosure strategy of the issuing firm adjusts to the arrival of information during the bookbuilding period. • Consider 1) the extent to which the initial price range is adjusted and 2) whether the initial prospectus is not substantially revised during the offering period.

Hanley and Hoberg 2012 • Litigation Risk Hedging – If an issuer receives bad news during the bookbuilding period, its price is set too high. The issuer will be able to reduce the price but its ability to use underpricing as a hedge may be limited by a minimum proceeds constraint or the threat of a pulled offer. Increased disclosure becomes paramount. – If the issuer receives good news during the bookbuilding period, its price is set too low. The issuer will raise the price and in this case both underpricing and disclosure can be freely used as hedges against litigation risk. Underpricing protects the underwriter from section 11 lawsuits. • Underwriter is named in over 70% of all section 11 lawsuits but only in 3% of 10 b-5 suits. • Underwriter suffers significant reputational and market share losses when named in a suit.