Hedging Strategies Using Futures 95320005 95320008 95320009 95320021

支持與反對避險的論點 Companies should focus on the")

S 2")

, S")

- 避險部位的多寡")

(profit of")

(profit of")

- Slides: 39

Hedging Strategies Using Futures 指導教授:吳銘政 95320005 蔡雅蘋 95320008 林佩儀 95320009 賴枚汮 95320021 陳佩絨 95320022 95320025 95320029 95320030 鐘于媜 林彥伶 羅婉瑜 蔡佳君

目錄 3. 1 3. 2 3. 3 3. 4 3. 5 3. 6 Basic principles Arguments for and against hedging Basis risk Cross hedging Stock index futures Rolling the hedge forward Summary

3. 2 Arguments for and against hedging (支持與反對避險的論點) 支持與反對避險的論點 Companies should focus on the main business they are in and take steps to minimize risks arising from interest rates, exchange rates, and other market variables

Arguments against Hedging Shareholders are usually well diversified and can make their own hedging decisions It may increase risk to hedge when competitors do not Explaining a situation where there is a loss on the hedge and a gain on the underlying can be difficult

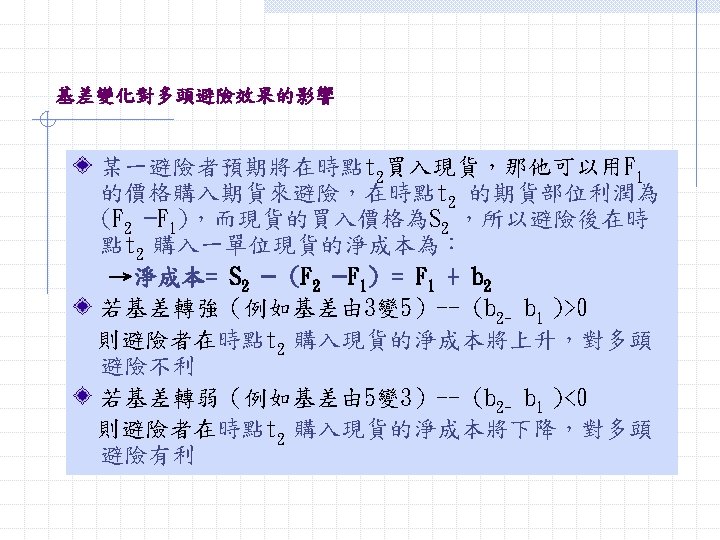

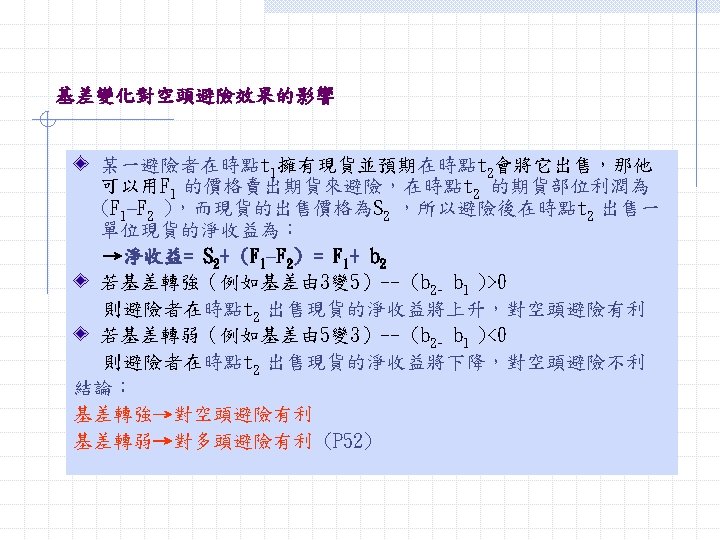

The Basis 基差 基差是期貨價格與現貨價格的差距 Bais=Spot price of asset to be hedged – Futures price of contract used →基差(B)=現貨價格(S)-期貨契約價格(F)

基差變化對多頭與空頭避險效果的影響 S 1 : spot price at time t 1 (在時點t 1的現貨價格) S 2 : spot price at time t 2 (在時點t 2的現貨價格) (Final Asset Price ) F 1 : futures price at time t 1 (在時點t 1的期貨價格) ( Initial Futures Price) F 2 : futures price at time t 2 (在時點t 2的期貨價格) (Final Futures Price) b 1 : basis at time t 1 (在時點t 1期貨之基差) →b 1= S 1 - F 1 b 2 : basis at time t 2 (在時點t 2期貨之基差) →b 2 =S 2 - F 2

Calculating the minimum variance hedge ratio ΔS : Change in spot price (現貨價格的改變), S , during a period of time equal to the life of the hedge ΔF : Change in futures price (期貨價格的改變), F , during a period of time equal to the life of the hedg σs : Standard deviation of ΔS (ΔS 的標準差) σF : Standard deviation of ΔF (ΔF的標準差) ρ : Coefficient of correlation between ΔS andΔF (ΔS 和ΔF的相關 係數) h* : Hedge ratio that minimizes the variance of the hedger‘s position (最小的變動避險比率) h*=ρσs/σF … (3. 1) 如果ρ=1和 ρ=1 σs=σF則避險比率h*=1,表示期貨價格完全反映了現貨價格

Optimal number of contracts QA : Size of position being hedged (units) - 避險部位的多寡 QF : Size of one futures contract (units) - 期貨合約的多寡 N* : Optimal number of futures contracts fot hedging (避險期貨合約的最適數量) N * = h * QA QF … (3. 2)

Tailing the hedge N *= h* VA VF

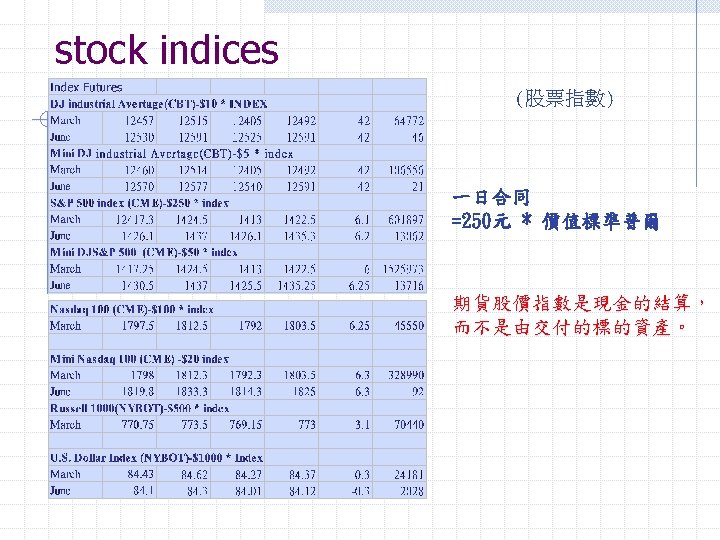

3. 5 Stock index futures we now move on to consider stock index futures and how they are used to hedge or manage exposures to equity prices. A stock index tracks changes in the value of a hypothetical portfolio of stocks. the weight of a stock in the portfolio equals the proportion of the portfolio invested in the stock. Dividends are usually not included in the calculation so that the index tracks the capital gain/loss from investing in the portfolio. Some indices are constructed from a hypothetical portfolio consisting of one of each of a number of stocks. Other indices are constructed so that weights are proportional to market capitalization

hedging an equity portfolio stock index futures can be used to hedge a welldiversified equity portfolio. P:current value of the portfolio F:current value of the stocks underlying one futures contract if the portfolio mirrors the index , the optimal hedge ratio, h*, equals 1. 0 and equation(3. 2) shows that the number of futures contracts that should be shorted is N*=P/A

when b=1, the return on the portfolio tends to mirror the return on the market; when b=2, the excess return on the portfolio tends to be twice as great as the excess return on the market; when b=0. 5, it tends to be half as great; and so on. in general, h* = β, so that equation(3. 2)gives N*=β (P/F)

Value of index in three months: 900 Futures price of index today: Futures price of index in three months: 1, 010 Gain on futures position: 810, 000 Return on market: -9. 750% Expected return on portfolio: Expected portfolio value in three months (including dividends): -15. 125% 4, 243, 750 Total expected value of position in three months: 5, 053, 750 902

Reasons for Hedging an Equity Portfolio Table 3. 4 shows that the hedging scheme results in a value for the hedger’s position at the end of the 3 -month period being about 1%higher than at the beginning of the 3 -month period. There is no surprise here. It’s natural to ask why the hedger should go to the trouble of using futures contracts.

Hedging can be justified if the hedger feels that the stocks in the portfolio have been chosen well. Another reason for hedging may be that the hedger is planning to hold a portfolio for a long period of time and requires short-term protection in an uncertain market situation.

Changing the Beta of a portfolio In the example in table 3. 4, the beta of the hedger's portfolio is reduced to zero. sometimes futures contracts are used to change the beta of a portfolio to some value other than zero.

In general, to change the beta of the portfolio from β to β *, where β > β *, a short position in (β - β *)P/F contracts is required. when β > β *, a long position in (β* - β)P/F contracts is required.

Exposure to the Price of an Indidvidual Stock hedging an exposure to the price of an individual stock using index futures contracts is similar to hedging a welldiversified stock portfolio. he hedge provides protection only against the risk arising from marked movements, and this risk is a relatively small proportion of the total risk in the price movements of individual stocks. it can also be used by an investment bank that has underwritten a new issue of the stock and wants protection against moves in the market as a whole.

3. 6 Rolling the hedge forward Sometimes the expiration date of the hedge is later than the delivery dates of all the futures contracts that can be used. The hedger must then roll the hedge forward by closed out one futures contract and taking the same position in a futures contract with a later delivery date. Hedges can be rolled forward many times.

Time t 1: Shore futures contract 1 Time t 2: Close out futures contract 1 Short futures contract 2 Time t 3: Close out futures contract 2 Short futures contract 3 ˙ ˙ ˙ Time tn: Close out futures contract n-1 Short futures contract n Time T: Close out futures contract n

Table 3. 5 Data for the example on rolling oil hedge forward. Date June 2008 Oct. 2007 futures price Apr. 2007 68. 20 Mar. 2008 futures price Feb. 2008 67. 40 67. 00 July 2008 futures price 65. 90 Spot price Sept. 2007 66. 50 66. 30 69. 00 66. 00

Suppose that in April 2007 a company realizes that it will have 100, 000 barrels of oil to sell in June 2008 and decides to hedge its risk with a hedge ratio of 1. 0. (In this example, we do not make the “tailing” adjustment described in Section 3. 4. ) The current spot price is $69.

The company therefore shorts 100 October 2007 contracts. In September 2007 it rolls the hedge forward into the March 2008 contracts. In February 2008 it rolls the hedge forward again into the July 2008 contract.

The October 2007 contract is $68. 20 $67. 40 ( per barrel) (profit of $0. 80) The March 2008 contract is $67. 00 $66. 50 ( per barrel) (profit of $0. 50)

The July 2008 contract is $66. 30 $65. 90 ( per barrel) (profit of $0. 40) The final spot price is $66.

The dollar gain per barrel of oil from the short futures contracts is (68. 20 -67. 40)+(67. 00 -66. 50)+(66. 3065. 90)=1. 70

The oil price declined from $69 to $66. Receiving only $1. 70 per barrel compensation for a price decline of $3. 00 may appear unsatisfactory. However, we cannot expect total compensation for a price decline when futures prices are below spot price. The best we can hope for is to lock in the futures price that would apply to a June 2008 contract if it were actively traded.

The daily settlement of futures contracts can cause a mismatch between the timing of the cash flows on hedge and the timing of the cash flows from the position being hedged. In situations where the hedge is rolled forward so that it lasts a long time this can lead to serious problems.

Summary

THE END THANK YOU~