Chapter 3 Part 3 A pricetaking firm firm

")

perfectly inelastic demand. b) downward-sloping marginal revenue curve.")

is the responsiveness of a product’s quantity demanded to")

is the responsiveness of the quantity demanded")

")

4 Inelastic Supply Curve For Tomatoes S 1 3")

S 1 0")

- Slides: 38

Chapter 3 Part 3

A price-taking firm (firm that cannot influence market price with the quantity it produces) faces a a) perfectly inelastic demand. b) downward-sloping marginal revenue curve. c) downward-sloping supply curve. d) perfectly elastic demand. e) downward-sloping demand curve.

A price-taking firm faces a a) perfectly inelastic demand. b) downward-sloping marginal revenue curve. c) downward-sloping supply curve. d) perfectly elastic demand. e) downward-sloping demand curve. any increase in the price, no matter how small, will cause demand for a good to drop to zero.

Learning Objectives Be able to calculate supply elasticity and comprehend what the numbers mean Understand the differences between constant-cost and increasing-cost industry Apply immediate, short and long-run in scenarios

Price Elasticity of Demand Price elasticity of demand shows how responsive consumers are to price changes. “How does change in price impact quantity demanded? ” ed = ΔQd ÷ average Qd Δprice ÷ average price

Total Revenue and the Price Elasticity of Demand Elasticity and Changes in Total Revenue Price Change in Total Revenue Elastic Demand up down up Inelastic Demand up down Unit-Elastic Demand up down unchanged

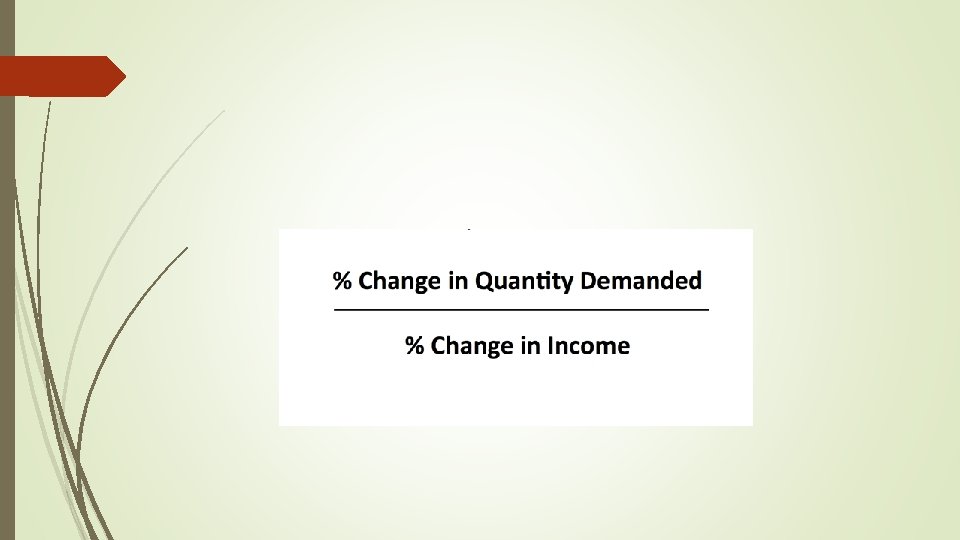

Income Elasticity Income elasticity (ei) is the responsiveness of a product’s quantity demanded to changes in consumer income. In mathematical terms: eincome = ei = ΔQd ÷ average Qd ΔI ÷ average I = ΔQd ΔI x I Q

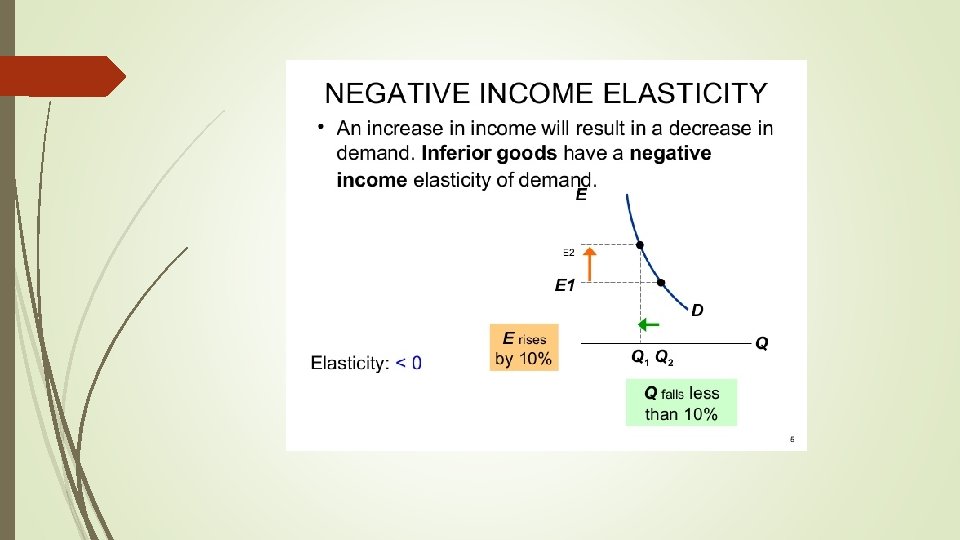

Income Elasticity Ei>1 then the good is a Luxury Good and is Income Elastic If 0<Ei<1 then the good is a Normal Good and Income Inelastic If Ei<0 then the good is an Inferior Good and Negative Income Inelastic The higher the income elasticity, the more sensitive demand for good to income changes A very high Ei suggests that when consumer income goes up, consumers will buy MORE of that good A very high Ei also suggests that when consumers income goes down, consumers will buy LESS of that good

Cross-Price Elasticity of Demand Cross-price elasticity (ei) is the responsiveness of the quantity demanded of one product (a) to a change in price of another (b). Measures the change in demand for one good in response to a change in price of another good In mathematical terms: e. AB= ΔQa ÷ average Qa ΔPb ÷ average Pb e. AB = % Change in Quantity Demanded for Good A % Change in Price of Good B

Cross-Price Elasticity of Demand If EAB>0, a higher price for good A increases the quantity of good B demanded => Demand Substitutes Example: apples and peaches are demand substitutes: As the price of peaches increases, the quantity of apples demanded increases If EAB<0, a higher price for good A decreases the quantity of good B demanded => Demand Complements Example: apples and bananas are demand complements: As the price of bananas increases, the quantity of apples demanded decreases

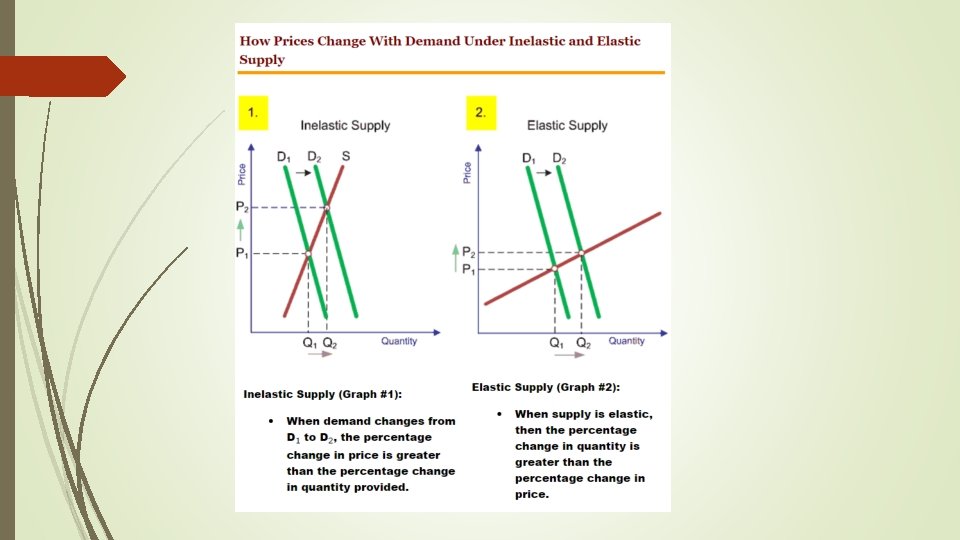

Elastic and Inelastic Supply Price elasticity of supply measures the responsiveness of quantity supplied to price changes. Elastic supply means % change in quantity supplied is more than % change in price. Inelastic supply means % change in quantity supplied is less than % change in price. Copyright © 2009 by Mc. Graw-Hill Ryerson Limited. All rights reserved.

Calculating Price Elasticity of Supply A numerical value for price elasticity of supply (es) is found by taking the ratio of the changes in quantity supplied and in price, each divided by its average value. In mathematical terms: es = ΔQs ÷ average Qs Δprice ÷ average price Copyright © 2009 by Mc. Graw-Hill Ryerson Limited. All rights reserved.

Elastic and Inelastic Supply (graph) 4 Inelastic Supply Curve For Tomatoes S 1 3 50% 2 100% 1 0 100 000 120000 Quantity Supplied (kilograms per year) Copyright © 2009 by Mc. Graw-Hill Ryerson Limited. All rights reserved. Price ($ per kilogram) Elastic Supply Curve for Tomatoes 4 S 2 3 50% 2 1 0 20% 100 000 120 000 Quantity Supplied (kilograms per year)

Perfectly Elastic and Perfectly Inelastic Supply Perfectly elastic supply means a constant price and a horizontal supply curve. Perfectly inelastic supply means a constant quantity supplied and a vertical supply curve. Copyright © 2009 by Mc. Graw-Hill Ryerson Limited. All rights reserved.

Example A rare book merchant who holds three copies of original Shakespeare manuscripts and needs to sell them before her shop goes out of business. Because Shakespeare is no longer alive, there can be no more new original Shakespeare manuscripts, and the merchant has no ability to change the supply of manuscripts in the shop. In this scenario, the merchant is compelled to sell these manuscripts, regardless of demand or price considerations, because failing to do so would only lead to larger losses. What is this? perfectly inelastic supply A market situation in which any increase or decrease in the price of a good or service does not result in a corresponding increase or decrease in its supply.

Es and its Determinants 1. Flexibility of sellers: goods that are somewhat fixed in supply (ie: beachfront property) have inelastic supplies 2. Time Horizon: supply is usually more inelastic in the short run than in the long run

Question The price of milk increases from $2. 85 per L to $3. 15 per L and the quantity supplied rises from 9000 to 11, 000 L per month % change in price = (3. 15 -2. 85)/3. 00 x 100% = 10% % change in Q supplied = (11, 000 – 9000)/ 10, 000 x 100% = 20% Es = 20%/ 10% = 2

Why do we care about Elasticity of Supply? Elasticity of supply tells us how fast supply responds to quantity demand price increase. When there is a popular product that is in short supply for instance, the price may rise as a result. The manufacturers of that product will increase output (the supply) to keep up with the demand. The higher the elasticity of supply, the faster the supply will increase when demand price increase. Some goods/services are more supply inelastic however, whenever there is a supply shortage. Limited tickets to a concert may have a very inelastic supply. The price of the concert tickets can be raised to any amount, but because there is a fixed number of seats and tickets, the supply (of tickets sold) may not be increased by much if at all.

Es Es<1 Inelastic Es=1 Unit Elastic Es > 1 Elastic

Main Factor that affect Es : Time Price elasticity of supply changes over three production periods: Supply is perfectly inelastic in the immediate run. Certain industries can make no changes in the quantities of resources they use Ie: Price of strawberries jumps up due to increase in demand, you would want to produce more strawberries so that you can sell more and increase revenue but because quantity supplied is constant, you are unable to Supply is either elastic or inelastic in the short run. Quantity of at least one of the resources used by business in an industry cannot be varied Ie: Price of strawberries from $2 to $2. 50, the farmers can increase their production by using more labour and maximizing the crop with fertilizers thus the price rises causes an increase in quantity supplied from 9 to 11 Supply is perfectly elastic for a constant-cost industry and very elastic for an increasing-cost industry in the long run.

Time and the Price Elasticity of Supply Price ($ per kilogram) S 1 0 750 000 Quantity Supplied (kilograms per month) Perfectly Inelastic Copyright © 2009 by Mc. Graw-Hill Ryerson Limited. All rights reserved. Short-Run Supply Elasticity For Strawberries Price ($ per kilograms) Immediate-Run Supply Elasticity for Strawberries S 2 2. 50 2. 00 0 9 11 Quantity Supplied (millions of kilograms per year)

Long Run vs Short Run Elasticities are often lower in the short run than in the long run Short Run Size of plant and machinery is fixe and the increased demand for the good/commodity is met only by increasing variable factors (ie: more workers) If the price of good is higher than the marginal cost (the cost added by producing one extra unit of good), the firm will expand its output If price of good is less than the marginal cost, it is incurring a loss and will reduce its output

Example if a farmer brings a truckload of watermelons to the farmers market, then he will try to sell all the watermelons, regardless of the price; otherwise, the watermelons will perish. On the other hand, even if the price is very high, the farmer has no way of supplying more watermelons right away. Short Run Supply tends to be inelastic Limited options available to increase supply Long Run Supply becomes more elastic Suppliers can take actions to increase supply (ie: build new factories, grow more crops)

Supply is perfectly elastic for a constant-cost industry and very elastic for an increasing-cost industry in the long run. Constant-cost industry An industry that is not a major user of any single resource Ie: the increase in quantity supplied following a short-run rise in the price of strawberries has NO EFFECT on resource price. The extra profits helps production to expand this will then cause the price of strawberries to fall until the price is back to its original level The price of strawberries always return to the original level in the long run which is why it exhibits a horizontal long run supply curve Long-Run Supply Elasticity Price ($ per kilograms) An industry in which the increase or decrease of industry output does not affect the prices of inputs S 4 S 3 2. 00 Increasingcost Industry 0 Quantity Supplied (millions of kilograms per decade) Constantcost Industry

In short… In a constant cost industry, an increase of firms entering an industry does not affect the price of resources needed for that industry. That is, as more and more firms enter an industry, the costs of production remain constant, or the same. This is caused by an abundance of this firm's resources. Normally, when more firms enter an industry, the amount of resources decreases, and so, the costs of production industry increase (this is called an increasing cost industry). This means that the entry or exit of firms does not shift the long run average total cost curve (average total cost does not change with the entrance or exit of firms). This happens because the demand for the resources of a constant-cost industry is relatively small compared to the total demand for these resources. One example of a constant-cost industry is the cucumber industry. As more farmers begin growing cucumbers (or many farmers stop), costs of production (land, fertilizer, labor, etc. ) stay relatively the same.

Increasing-Cost Industry An industry that is a major user of at least one resource Ie: a greater Q supplied of strawberries leads to an increase in the price of a single resource (land/machinery) which increase the bottom-line A short-run rise in the price of strawberries causes production to grow as farmers take advantage of extra profits. As long as there is increased profits, price is driven down in the long run to its lowest possible level BUT is now about its initial level since farmers face higher per-unit costs thus quantities supplied are highly sensitive to price changes => Elastic Long-Run Supply Elasticity Price ($ per kilograms) An industry in which increases in industry output increases the prices of inputs S 4 S 3 2. 00 Increasingcost Industry 0 Quantity Supplied (millions of kilograms per decade) Constantcost Industry

In short…. Increasing cost industries result from an increase in firms in that industry. When there are less firms in an industry, the costs for production are relatively low, but as there are more firms added, the demand for resources goes up, so as a result so do costs for those resources, which creates an increasing-cost industry The increased demand = require to produce larger output = higher cost of production In short, an increasing cost industry results from an increase in producers which results in an increase in supply which causes a greater demand for the resources, which causes prices for resources to go up, which is why the costs for the industry as a whole are increasing.

What industry do you think Farms are? Increasing cost industry. As the industry size increases, costs for supplies like plows, tractors, etc. increases dramatically because the firms that are producing those products are trying to maximize their own profits as well.

Quick Check The long run supply curve of an increasing-cost industry is A. Vertical Line B. Horizontal Line C. Upward Sloping D. Downward Sloping

The long run supply curve of an increasing-cost industry is A. Vertical Line B. Horizontal Line C. Upward Sloping D. Downward Sloping

Summary Short-run supply curve of industry always slopes upward to the right Long-run curve my be a horizontal straight line, sloping upwards or sloping downwards Depends whether industry is a constant cost industry or an increasing cost industry In the long run, price elasticity of supply depends on the industry’s use of resources. In a constant-cost industry (not a major user of any one resource), supply in the long run is perfectly elastic, with a constant price at all possible quantities supplied. In an increasing-cost industry (a major user of at least one resource), the long-run supply is very elastic, with price rising gradually at higher quantities supplied

When the demand for electricity peaks during the hottest days of summer, Hydro One can generate more electricity by using more fuel and increasing the working hours of many of its employees. The company cannot, however, increase electric power production by building additional generating capacity. This means that the company is operating in the a) market run. b) Immediate run. c) long run. d) short run.

When the demand for electricity peaks during the hottest days of summer, Hydro One can generate more electricity by using more fuel and increasing the working hours of many of its employees. The company cannot, however, increase electric power production by building additional generating capacity. This means that the company is operating in the a) market run. b) Immediate run. c) long run. d) short run.

Why did OPEC Fail to Keep the Price of Oil High? In the 1970 s and 1980 s, OPEC reduced the amount of oil it was willing to supply to world markets. The decrease in supply led to an increase in the price of oil and a decrease in quantity demanded. The increase in price was much larger in the short run than the long run. Why?

The demand supply of oil are much more inelastic in the short run than the long run. The demand is more elastic in the long run because consumers can adjust to the higher price of oil by carpooling or buying a vehicle that gets better mileage. The supply is more elastic in the long run because non. OPEC producers will respond to the higher price of oil by producing more.