The CPA Profession Chapter 2 2008 Prentice Hall

")

and rules")

ﻣﻌﺎﻳﻴﺮ ﺍﻟﺘﺪﻗﻴﻖ ﺍﻟﻤﺘﻌﺎﺭﻑ ﻋﻠﻴﻬﺎ 1. 2. 3. General standards")

are issued by the International Auditing Practice Committee of")

- Slides: 26

The CPA Profession ﻣﻬﻨﺔ ﺍﻟﺘﺪﻗﻴﻖ Chapter 2 © 2008 Prentice Hall Business Publishing, Auditing 12/e, Arens/Beasley/Elder 2 -1

Certified Public Accounting Firms The legal right to perform audits is granted to CPA firms by regulation of each state. CPA firms also provide many other services to their clients, such as tax and consulting services More than 45, 000 CPA firms exist in the USA ranging in size 1 person to 20, 000 partners and staff. © 2008 Prentice Hall Business Publishing, Auditing 12/e, Arens/Beasley/Elder 2 -2

Certified Public Accounting Firms Ø Big Four international firms. In 2005 , the big four size by revenue As follow: (1) Deloitte & Touche : $7, 814 millions , 2650 partner, 23841 professionals (2) Ernst & Young : $6, 330 millions, 2130 partner, 15 900 professionals (3) Pricewaterhouse. Coopers: 6, 167 millions, 2019 part , 20056 professional (4) KPMG: $4, 715 millions, 1607 partner, 13184 professionals Ø National firms Ø Regional and large local firms Ø Small local firms © 2008 Prentice Hall Business Publishing, Auditing 12/e, Arens/Beasley/Elder 2 -3

Certified Public Accounting Firms The four largest CPA firms in the United States are called the “Big Four” international CPA firms. These four firms have offices in most major cities in the United States and in many cities throughout the world. © 2008 Prentice Hall Business Publishing, Auditing 12/e, Arens/Beasley/Elder 2 -4

Activities of CPA Firms Ø Accounting and bookkeeping services Ø Tax services Ø Management consulting services © 2008 Prentice Hall Business Publishing, Auditing 12/e, Arens/Beasley/Elder 2 -5

Structure of CPA Firms Three main factors influence the organizational structure of all firms: 1. The need for independence from clients. 2. The importance of a structure to encourage competence. 3. The increased litigation risk faced by auditors. © 2008 Prentice Hall Business Publishing, Auditing 12/e, Arens/Beasley/Elder 2 -6

Organizational Structure ﺍﻟﻬﻴﻜﻞ ﺍﻟﺘﻨﻈﻴﻤﻲ Ø Proprietorship: one owner Ø Professional corporation: owned by one or more shareholders Ø General partnership: multiple owners Ø Limited liability company: its owners have limited personal liability Ø General corporation: Ø Limited liability partnership: owned by one or more partners © 2008 Prentice Hall Business Publishing, Auditing 12/e, Arens/Beasley/Elder 2 -7

Hierarchy of a Typical CPA Firm ﺍﻟﺘﺴﻠﺴﻞ ﺍﻟﻬﺮﻣﻲ ﻟﺸﺮﻛﺔ ﺍﻟﺘﺪﻗﻴﻖ Staff level Experience Typical responsibilities Staff assistant 0 -2 years Perform most of the detailed audit work Senior or in – charge auditor 2 -5 years Responsible for the audit work, supervising and reviewing audit work Manager 5 -10 years Helps the in-charge plan and manage the audit, review the in-charge work, and manage relations with the client. May be is responsible for more than one engagement at the same time. Partner 10+ years Review the overall audit work and involved in the significant audit decisions. © 2008 Prentice Hall Business Publishing, Auditing 12/e, Arens/Beasley/Elder 2 -8

E-Commerce and CPA Firm Operations CPA firms are using the Internet to market their services. Firm Web sites also feature online software tools and databases to subscribers. Firms take advantage of online resources and databases to help their staffs stay current on emerging business and standards-setting issues. © 2008 Prentice Hall Business Publishing, Auditing 12/e, Arens/Beasley/Elder 2 -9

Securities and Exchange Commission The overall purpose of the Securities and Exchange Commission (SEC) is to assist in providing investors with reliable information upon which to make investment decisions. © 2008 Prentice Hall Business Publishing, Auditing 12/e, Arens/Beasley/Elder 2 - 10

AICPA The AICPA sets professional requirements for CPAs, conducts research, and publishes materials on many different subjects related to accounting, auditing, attestation and assurance services, management consulting services, and taxes. © 2008 Prentice Hall Business Publishing, Auditing 12/e, Arens/Beasley/Elder 2 - 11

Establishing Standards and Rules The AICPA is empowered to set standards (guidelines) and rules that all members and other practicing CPAs must follow. © 2008 Prentice Hall Business Publishing, Auditing 12/e, Arens/Beasley/Elder 2 - 12

Establishing Standards and Rules ﺗﺄﺴﻴﺲ ﺍﻟﻤﻌﺎﻳﻴﺮ ﻭﺍﻟﻘﻮﺍﻋﺪ The AICPA is empowered to set standards (guidelines) and rules that all members and other practicing CPAs must follow. 1. Auditing standards: the auditing standard board (ASB) ﻣﻌﺎﻳﻴﺮ ﺍﻟﺘﺪﻗﻴﻖ 2. is responsible for pronouncements, which are called Statement on Auditing Standards SASs 2. Compilation and review standards ﺗﺠﻤﻴﻊ ﻭﻣﺮﺍﺟﻌﺔ ﺍﻟﻤﻌﺎﻳﻴﺮ 3. 4. Other attestation standards Consulting standards 5. Code of Professional Conduct: professional ethics ﻧﻈﺎﻡ ﺍﻻﺟﺮﺍﺀﺍﺕ ﺍﻟﻤﻬﻨﻴﺔ © 2008 Prentice Hall Business Publishing, Auditing 12/e, Arens/Beasley/Elder 2 - 13

Other AICPA Functions Writes and grades the CPA examination. Supports research by its own staff and provides grants to others. Publishes a variety of materials. Provides seminars and education in a variety of subject matters. © 2008 Prentice Hall Business Publishing, Auditing 12/e, Arens/Beasley/Elder 2 - 14

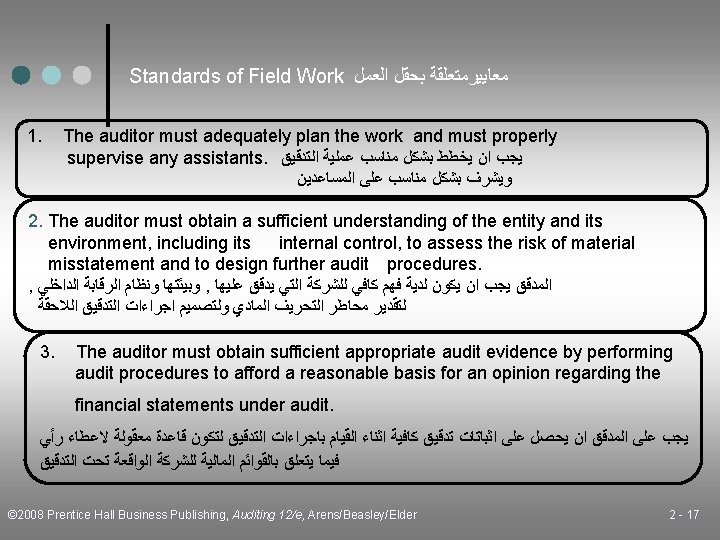

Generally accepted auditing standards (GAAS) ﻣﻌﺎﻳﻴﺮ ﺍﻟﺘﺪﻗﻴﻖ ﺍﻟﻤﺘﻌﺎﺭﻑ ﻋﻠﻴﻬﺎ 1. 2. 3. General standards Standards of field works Reporting standards © 2008 Prentice Hall Business Publishing, Auditing 12/e, Arens/Beasley/Elder 2 - 15

General Standards ﻣﻌﺎﻳﻴﺮ ﻋﺎﻣﺔ 1. The audit is to be performed by a person or persons having adequate technical training and proficiency as an auditor. ﺍﻟﺘﺪﻗﻴﻖ ﻳﺠﺐ ﺍﻥ ﻳﻨﺠﺰ ﻣﻦ ﻗﺒﻞ ﺷﺨﺺ ﻟﺪﻳﺔ ﺗﺪﺭﻳﺐ ﻭﻣﻬﺎﺭﺓ ﻣﻨﺎﺳﺒﺔ ﻛﻤﺪﻗﻖ 2. The auditor must maintain independence in mental attitude in all matters relating to the audit. ﻳﺠﺐ ﻋﻠﻰ ﺍﻟﻤﺪﻗﻖ ﺍﻥ ﻳﻜﻮﻥ ﻣﺴﺘﻘﻼ ﺫﻫﻨﻴﺎ ﻓﻲ ﻛﻞ ﺍﻻﻣﻮﺭ ﺍﻟﻤﺘﻌﻠﻘﺔ ﺑﺎﻟﺘﺪﻗﻴﻖ 3. The auditor must exercise due professional care in the performance 4. of the audit and the preparation of the report. ﺍﻟﻤﺪﻗﻖ ﻳﺠﺐ ﺍﻥ ﻳﻤﺎﺭﺱ ﺍﻟﺤﺬﺭ ﺍﻟﻤﻬﻨﻲ ﻓﻲ ﺍﺩﺍﺀ ﺍﻟﺘﺪﻗﻴﻖ ﻭﺍﻋﺪﺍﺩ ﺗﻘﺮﻳﺮ ﺍﻟﺘﺪﻗﻴﻖ © 2008 Prentice Hall Business Publishing, Auditing 12/e, Arens/Beasley/Elder 2 - 16

Standards of Reporting 1. The report shall state whether the financial statements are presented in accordance with generally accepted accounting principles. ﺍﻟﺘﻘﺮﻳﺮ ﻳﺠﺐ ﺍﻥ ﻳﻨﺺ ﻓﻴﻤﺎ ﺍﺫﺍ ﺗﻢ ﺍﻋﺪﺍﺩ ﺍﻟﻘﻮﺍﺋﻢ ﺍﻟﻤﺎﻟﻴﺔ ﺣﺴﺐ ﺍﻟﻤﻌﺎﻳﻴﺮﺍﻟﻤﺤﺎﺳﺒﻴﺔ ﺍﻟﻤﺘﻌﺎﺭﻑ ﻋﻠﻴﻬﺎ 2. The report shall identify those circumstances in which such principles have not been consistently observed in the current period in relation to the preceding period. © 2008 Prentice Hall Business Publishing, Auditing 12/e, Arens/Beasley/Elder 2 - 18

Standards of Reporting 3. Informative disclosures ﺍﻓﺼﺎﺡ ﻓﻴﺔ ﻣﻌﻠﻮﻣﺎﺕ ﻣﻔﻴﺪﺓ in the financial statements are to be regarded as reasonably adequate unless otherwise stated in the report. 4. The report shall contain an expression of opinion regarding the financial statements, taken as a whole. © 2008 Prentice Hall Business Publishing, Auditing 12/e, Arens/Beasley/Elder 2 - 19

Generally Accepted Auditing Standards General Standards 1. Adequate training and proficiency 2. Independence in mental attitude 3. Due professional care Standards of Field Work 1. Proper planning and supervision 2. Understanding of the entity 3. Sufficient appropriate evidence Standards of Reporting 1. Statements prepared in accordance with GAAP 2. Circumstances when GAAP not followed 3. Adequacy of disclosures 4. Expression of opinion on financial statements © 2008 Prentice Hall Business Publishing, Auditing 12/e, Arens/Beasley/Elder 2 - 20

Statements on Auditing Standards The 10 generally accepted auditing standards are too general to provide meaningful guidance. SASs interpret the 10 generally accepted auditing standards and are the most authoritative references available to auditors. © 2008 Prentice Hall Business Publishing, Auditing 12/e, Arens/Beasley/Elder 2 - 21

Statements on Auditing Standards Ø Classification of Statements on Auditing Standards Ø GAAS and Standards of Performance © 2008 Prentice Hall Business Publishing, Auditing 12/e, Arens/Beasley/Elder 2 - 22

International Standards on Auditing (ISAs) are issued by the International Auditing Practice Committee of the International Federation of Accountants (IFAC). © 2008 Prentice Hall Business Publishing, Auditing 12/e, Arens/Beasley/Elder 2 - 23

International Standards on Auditing IFAC is the worldwide organization for the accountancy profession. The IFAC works to improve the uniformity of auditing practices and related services throughout the world. © 2008 Prentice Hall Business Publishing, Auditing 12/e, Arens/Beasley/Elder 2 - 24

Elements of Quality Control Ø Independence, integrity, and objectivity Ø Personnel management Ø Acceptance and continuation of clients and engagements Ø Engagement performance Ø Monitoring © 2008 Prentice Hall Business Publishing, Auditing 12/e, Arens/Beasley/Elder 2 - 25

Relationships Quality control standards Generally accepted auditing standards AICPA practice sections Peer review © 2008 Prentice Hall Business Publishing, Auditing 12/e, Arens/Beasley/Elder 2 - 26