ACF 101 102 Introductory Financial Accounting Introductory Financial

is a report of all")

is the remainder after all expenses have been deducted")

is the time span during which")

are increases in owners' equity arising from increases in assets received in")

is the excess of revenues over expenses. If expenses exceed")

is additional owners' equity generated by income")

")

◦ Interpreting economic events/preparing financial reports requires judgment ◦")

Equity For the period Jan")

- Slides: 52

ACF 101 -102 Introductory Financial Accounting Introductory Financial Statement Analysis LECTURE 3

Learning Outcome Understand the basics underlying financial accounting and financial statements Preparing basic Financial Statements

Topics Components of the Income Statement Preparing the Income Statement

Prepare an income statement and show it is related to a balance sheet…. .

An income statement (statement of earnings or operating statement) is a report of all revenues and expenses pertaining to a specific time period that is not more than one year.

Net income (net earnings, profit) is the remainder after all expenses have been deducted from revenue, assuming revenue is greater than expenses. If expenses are greater than revenue, then a company has a net loss.

Net income is used by investors to evaluate the success of the period's operations for a particular business.

The income statement is the major link between two balance sheets and shows the activities of an entity over a span of time.

The Income Statement The income statement summarizes a firm's revenues and expenses for a period of time. ◦ The date on the income statement will be a phrase such as, "For the month ended July 31, " or "For the year ended December 31. "

The Income Statement If revenues exceed expenses, then the result is net income. If expenses exceed revenues, then the result is a net loss.

The Income Statement Only revenues and expenses appear on the income statement. ◦Students sometimes think that cash is a good thing and should appear on the income statement. ◦Cash is an asset and so will appear on the balance sheet.

Explain how accountants measure income….

The accounting measurement of income is the major means for evaluating a business entity's performance. Some agreed-upon rules have emerged for income measurement so that investors can compare one company with another.

The operating cycle (cash cycle or earnings cycle) is the time span during which cash is used to acquire goods and services, which in turn are sold to customers, who in turn pay for their purchases in cash.

Accounting time periods are imposed on a business to enable periodic reports of performance.

The calendar year is the most popular time period for measuring income or profits, although other fiscal periods can be used.

Interim periods are the time spans established for accounting purposes that are less than a year.

Revenues (sales) are increases in owners' equity arising from increases in assets received in exchange for the delivery of goods or services to customers

Expenses are decreases in owners' equity that arise because goods or services are delivered to customers.

Income (profit or earnings) is the excess of revenues over expenses. If expenses exceed revenues, the excess is called a loss.

Retained earnings (retained income or reinvested earnings) is additional owners' equity generated by income or profits less payments (dividends) to owners

Cost of goods sold expense (also called cost of sales or cost of revenue) is the original acquisition cost of the inventory that a company sells to customers during the reporting period.

Measuring Income 1. The accrual basis recognizes the impact of transactions on the financial statements in the time period when revenues and expenses occur, whereas the cash basis recognizes the impact of transactions on financial statements only when cash is received or disbursed.

Determine when a company should record revenue from a sale…. .

To measure income on an accrual basis, a set of revenue recognition criteria is used to determine whether revenues should be recorded in the financial statements of a given period. Both U. S. GAAP and IFRS use these criteria, although they differ slightly in how they implement them. To be recognized, revenues must meet two criteria:

They must be earned. Goods or services are fully rendered, usually delivered to the customer.

They must be realized or realizable. Revenues are realized when cash or claims to cash are received, usually upon a market transaction. Revenues are realizable when the company receives assets that are easily converted into cash or claims to cash. (If cash is not received directly, the eventual collectability of cash must be reasonably assured. )

Use the concept of matching to record the expenses for a period…. .

Expenses of any period are linked to one of two types: Revenues earned that period—product costs (e. g. , cost of goods sold and sales commissions). Cost of goods sold pertains to the cost of inventory that was sold. Period of time itself—period costs (e. g. , rent expense).

Matching is the recording of expenses in the same time period as the related revenues are recognized. There are two types of expenses in every accounting period: (1) those linked with the revenues earned that period (product costs), and (2) those linked with the time period itself (period costs).

Measuring Income – increase in wealth over time ◦ Calendar year – Jan 1 to Dec 31 ◦ Fiscal year – Start anytime; end 365 days later (busy) ◦ Annual financial reports ◦ Interim periods – weekly, monthly, quarterly ◦ Quarterly (3 months) financial reports ◦ Operating cycle – time lapse between

Measuring Income – increase in wealth over time Basic accounting equation + specific accounts ASSETS = Cash Accounts Receivable Prepaid items Equipment Building Land LIABILITIES Accounts Payable Notes Payable + OWNERS’ EQUITY Paid in Capital Retained (Income = $60, 000) Revenue $160, 000 Expenses $100, 000 Gains (later) Losses (later) Distributions to owners Dividends

Measuring Income Revenues - net assets received from customers in exchange for delivery of goods or services Expenses – net assets given up or consumed when delivering goods or services to customers Income (profit, earnings) – revenues less expenses during some reporting period ◦ Revenues/Expenses – usual and frequent ◦ Gains/Losses (later) – unusual and/or infrequent Retained Earnings – income less dividends since the inception of the business

Measuring Income When to measure in and out flows? ◦Cash-only in and out flows ◦Used by many small businesses due to its objectivity and simplicity ◦Unrealistic - many events are initially on credit

Measuring Income ◦Accrual ◦ Measures in and outflows of all transactions, events, circumstances, when they occur regardless of whether cash flows are involved ◦ Used by most companies to prepare their financial statements

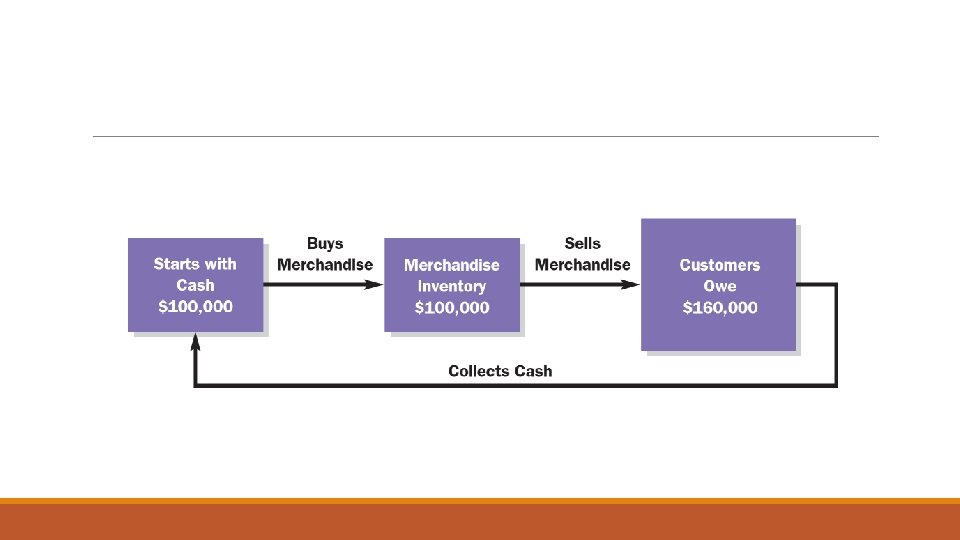

Measuring Income • Accrual Accounting Example - Sales on open account for the entire month of January amount to $160, 000. The cost of the inventory sold is $100, 000 Assets = Liabilities + Owners’ Equity Accounts Merchandise Receivable Inventory Cost of inventory sold Sales on credit – 100, 000 +160, 000 Retained Earnings – 100, 000 (cost of goods sold) +160, 000 (sales revenues)

Measuring Income Accounts receivable - amounts owed by customers to the business as a result of a usual and frequent transaction not involving cash Cost of goods sold (an expense) - the cost of the products the business sold to the customer that generated the revenue

Revenues Recognition Revenues are recognized when they are ◦ Earned - All (or substantially all) of the goods or services the customer wants have been delivered to and accepted by customers ◦ Realized - Cash has been received from the customer for those goods or services ◦ Realizable - If anything else besides cash (e. g. accounts receivable) are received, it (they) should be readily convertible into cash Revenues increase Retained Earnings and Stockholders’ Equity

Matching Expenses ◦ Usual and frequent assets sacrificed or liabilities assumed for goods or services that contributed to revenue earned in this reporting period ◦ Deductions from stockholders’ equity ◦ Matching ◦ List as expenses only those things that directly or indirectly contributed to this period’s revenue Product costs – more closely tied to product Period costs – more closely tied to the period

Matching Acquisition Assets Unexpired costs such as Inventory, Prepaid Rent, Equipment Expiration Expenses Instantaneously Or Eventually Become Expired costs, such as Cost of Goods Sold, Rent, Depreciation, Other Expenses)

Matching Acquire before it contributes to revenue ◦ Acquire 3 month’s rent in advance of usage ◦ Consume one month’s rent ◦ Assets (Prepaid Rent) decreases $2, 000 ◦ Equity (Rent Expense) decreases $2, 000 ◦ Probably listed as period cost (expense) ◦ If it was merchandise inventory – product cost Acquire/use same time – Rent Expense - $2, 000

Matching Depreciation is the systematic allocation of the acquisition cost of long-lived assets to the periods that benefit from the use of the assets Land is not subject to depreciation because it does not deteriorate over time Assets Cash Equipment 14, 000 + 14, 000 = Liabilities + Paid in Capital – 100 * * $14, 000 / 140 months expected life = $100 per month + Retained Earnings – 100 Depreciation Expense

Income Statement Income – increase in wealth over time Basic accounting equation + specific accounts ASSETS = Cash Accounts Receivable Prepaid items Equipment Building Land LIABILITIES Accounts Payable Notes Payable + OWNERS’ EQUITY Paid in Capital Retained Earnings Revenue Expenses Gains (later) Losses (later) Distributions to owners Dividends

Income Statement Balance sheet - financial position/condition at discrete points in time, e. g. fiscal year end Income statement (Statement of Earnings, Operations, Profit and Loss) - changes that took place between those points in time attributable to operating the business Revenues Expenses Gains/Loses (later) Net income (loss)

Income Statement Balance Sheet December 31 20 X 1 Balance Sheet February 28 20 X 2 Balance Sheet January 31 20 X 2 Income Statement For January Income Statement For February Balance Sheet March 31 20 X 2 Income Statement For March Time Income Statement for Quarter Ended March 31, 20 X 2

Income Statement Dynamics (ethical dilemmas) ◦ Interpreting economic events/preparing financial reports requires judgment ◦ Management ◦ Exercises that judgment ◦ Is rewarded on the reports’ content ◦ Circumstances have, do, and will occur where ◦ Honest disagreements occur ◦ Window dressing opportunities will tempt some ◦ A few will go too far and commit illegal acts

Dividends/Stockholders’ Equity Name of Company Statement of Stockholders’ (Shareholders’) Equity For the period Jan 1, 20 X 1 to 20 X 3 Paid-in Retained Comprehensive Capital Earnings Income (Chap 11) 1/1/20 X 1 Beginning Balance New issues (Buy backs/retirements) 12/31/20 X 1 Ending balance Beginning Balance Net Income (Dividends) Ending balance * Beginning Balance Various increases Various decreases Ending balance * (Repeat for two more years) * Could be a negative number

Dividends/Stockholders’ Equity • Combined Statement of Retained Earnings and Income Statement Sales Deduct expenses: Cost of goods sold $110, 000 Rent 2, 000 Depreciation 100 Net income Retained earnings, January 31, 20 X 2 Total Less: Dividends declared Retained earnings, February 28, 20 X 2 $176, 000 112, 100 $ 63, 900 57, 900 $ 121, 800 50, 000 $ 71, 800

Dividends/Stockholders’ Equity Assets = Liabilities + Paid-in Capital + Retained earnings [Beginning balance + Revenues - Expenses - Dividends] [57, 900 + 176, 000 - 112, 100 - $50, 000] Net income from the Income Statement Ending Retained Earnings Balance = $71, 800 Retained earnings is one type of claim against the net assets (assets less liabilities); it is not cash

Dividends/Stockholders’ Equity Cash dividends ◦ Board of directors decides whether to issue dividends ◦ If such a decision is made, three important dates ◦ Declaration – when publically announced ◦ Liabilities (Dividends Payable) increase ◦ Retained Earnings decrease ◦ Does not affect income statement (expenses) ◦ Record – owners, as of that day, get the dividend ◦ Payment – check is “in the mail” ◦ Assets (cash) and liabilities (Div. Pay. ) decrease