ACF 101 102 Introductory Financial Accounting Introductory Financial

passes laws and funding for")

◦ Independent nonprofit organization ◦")

◦ Does not have investigatory or enforcement authority")

◦ Not a U. S.")

◦ Established the Public")

◦ National voluntary")

◦ Sets knowledge, integrity, and")

earns this designation by a combination of education, qualifying")

is the principal professional association in")

regulates disclosures for nonfederal governmental organizations (states")

applies to all broad concepts and detailed practices to")

is responsible for establishing GAAP in the United")

was established to develop, in the public interest,")

. IFRS is used in more than")

Entity - an organization that stands apart from other organizations and")

◦ Reporting entity will continue to exist indefinitely, i.")

and internally (previous")

- Slides: 43

ACF 101 -102 Introductory Financial Accounting Introductory Financial Statement Analysis LECTURE 5

Learning Outcome Understand the accounting concepts and conventions present in accepted accounting principles Demonstrate knowledge and understanding of ethical issues in this area Appraise financial performance and the position of an organisation through the calculation and review of a number of basic ratios.

Topics Regulation of Financial Reporting Ethics Basic accounting concepts

Explain the purpose of accounting systems, accounting classifications and understanding accounting conventions within the context of professional regulatory requirements.

Regulation of Financial Reporting Federal Government ◦ Legislative (Congress) passes laws and funding for federal agencies ◦ Judicial – enforces laws ◦ Executive – Proposes, signs, administers budgets and laws (see SEC below) SEC – Has statutory authority to ◦ regulate investment management activities ◦ regulate stock market activities ◦ investigate violations of security laws ◦ control financial reports and their preparers

Regulation of Financial Reporting Financial Accounting Standards Board (FASB) ◦ Independent nonprofit organization ◦ Writes accounting/reporting standards for not-for-profit organizations ◦ Has delegated authority from SEC to create and amend financial accounting/reporting standards for-profit organizations subject to control by the SEC ◦ Authority may be rescinded at any time

Regulation of Financial Reporting FASB (continued) ◦ Does not have investigatory or enforcement authority ◦ Published over 160 separate opinions that include Generally Accepted Accounting Principals (GAAP) ◦ Selected recent/current projects ◦ Codification (now only one set of guidance) ◦ Convergence with the IFRS

Regulation of Financial Reporting International Accounting Standards Board (IASB) ◦ Not a U. S. governmental agency ◦ United States is represented on the board ◦ Creates and amends financial accounting and reporting standards for European Union and many other countries ◦ Selected current projects: ◦ Convergence with U. S. GAAP

Regulation of Financial Reporting Sarbanes Oxley Act – 2002 ◦ Board of directors must have an audit committee composed only of “independent” directors ◦ Management must examine and certify the adequacy of internal controls used by its company ◦ Prohibits public accounting firms from providing audit clients with certain non-audit services ◦ Requires rotation every 5 years of the lead audit or coordinating partner and the reviewing partner

Regulation of Financial Reporting Sarbanes Oxley Act – 2002 (continued) ◦ Established the Public Company Accounting Oversight Board (PCAOB) ◦ Subordinate to the SEC ◦ Writes Generally Accepted Auditing Standards (GAAS) that external auditors must follow when conducting an audit ◦ Writes policies directed toward management regarding internal controls of the companies ◦ Investigates audit and management compliance ◦ SEC approves recommended disciplinary actions

In 2002, the U. S. Congress passed the Sarbanes-Oxley Act, which gave the government a larger role in regulating the audit profession.

Sarbanes-Oxley Act regulations Establishment of the Public Company Accounting Oversight Board with powers to regulate many aspects of public accounting and to set standards for audit procedures, Prohibiting public accounting firms from providing to audit clients certain nonaudit services,

Sarbanes-Oxley Act regulations Rotation every five years of the lead audit or coordinating partner and the reviewing partner on an audit, Boards of directors of publicly held companies to appoint an audit committee composed only of “independent” directors,

Sarbanes-Oxley Act regulations CEOs and CFOs personally sign a statement certifying the appropriateness and fairness of their companies’ financial statements, and Increasing the criminal penalties for knowingly misreporting financial information.

Regulation of Financial Reporting American Institute of Certified Public Accountants (AICPA) ◦ National voluntary membership association of CPAs ◦ Sets strategic direction for the profession ◦ Members must abide by a code of conduct ◦ Writes/grades/updates the Uniform CPA Examination XXX Society of CPAs ◦ Each state has its own society ◦ Advocate for the profession within the state ◦ Provides multiple goods and services to members

Regulation of Financial Reporting State Boards of Accountancy (SBA) ◦ Sets knowledge, integrity, and ethics policies ◦ Uses the Uniform CPA Exam, written and graded by the AICPA, as part of the licensing process ◦ Licenses and disciplines CPAs ◦ Requires certain number of professional-subject courses (continuing professional education [CPE]) to be taken within a period of time to maintain license ◦ Works with other SBA on reciprocity of CPA licenses between states

Describe auditing and how it enhances the value of financial information.

The credibility of financial statements is the ultimate responsibility of the managers who are entrusted with the resources of the entity under their command.

Third-party assurance about the credibility of financial statements gave rise to the CPA profession. An auditor examines the information that managers use to prepare the financial statements and provides assurances about the credibility of those statements.

A certified public accountant (CPA) earns this designation by a combination of education, qualifying experience, and the passing of a two-day written national examination, administered and graded by the American Institute of Certified Public Accountants (AICPA). ACCA ACA CIMA

An audit is an in-depth examination of transactions and financial statements made in accordance with generally accepted auditing standards developed by the AICPA.

The audit is conducted by an independent CPA to lend credibility to management's financial statements and is described in the auditor's opinion. An auditor’s opinion (also called an independent opinion) describes the scope and results of the audit, and companies include the opinion with the financial statements in their annual reports.

The American Institute of Certified Public Accountants (AICPA) is the principal professional association in the private sector that regulates the quality of the accounting profession.

Auditing 1929 Stock Market Crash – Senior managers ◦ Rewarded in part by content of financial statements ◦ Prepare financial statements ◦ Potential for bias SEC Act of 1934 required public companies to ◦ have their financial statements audited by independent outside auditors who are CPAs ◦ File results with the SEC Shareholders – audit report adds credibility to the financial statements they use when making decisions

Auditing The four largest international public accounting firms are ◦ Deloitte Touche Tohmatsu ◦ Ernst & Young ◦ KPMG International ◦ Pricewaterhouse. Coopers ◦ 97% of the firms listed on the NYSE are clients of these four firms • National, regional and local firms also exist • Offer fee-based tax, consulting, auditing services

Auditing Audit – examination of a company’s transactions and the resulting financial statements Standard report includes the following topics: ◦ Introduction – what was audited? ◦ Scope – how was the audit conducted? ◦ Opinion as to ◦ fairness of financial statements ◦ degree to which GAAP was followed ◦ Other topics (e. g. , changes in principals, adequacy of management’s review of internal controls)

Evaluate the role of ethics in the accounting process. Members of the AICPA, as well as members of the Institute of Management Accountants, must abide by a code of professional conduct, which is especially concerned with integrity and independence. Professional accounting organizations have procedures for reviewing behavior alleged as not being consistent with the codes of professional conduct

Ethics – doing what is right for all stakeholders Ethics are an integral part of the accounting profession and are stressed in guidance from the following: ◦ Professional societies (AICPA, IMA, state societies) ◦ Regulatory bodies (SEC, PCAOB, SBA) ◦ Accounting firms (international, regional, local) ◦ Publically traded firms (set the “tone at the top”) Nevertheless – greed often trumps ethics

Miscellaneous The Governmental Accounting Standards Board (GASB) regulates disclosures for nonfederal governmental organizations (states and below, organizations, etc. ) More CEOs started out in finance or accounting than any other area, i. e. , Accounting provides an excellent training ground for future managers and executives

Explain the regulation of financial reporting, including differences between U. S. GAAP and IFRS.

Generally accepted accounting principles (GAAP) applies to all broad concepts and detailed practices to be followed in preparing and distributing financial statements

The Financial Accounting Standards Board (FASB) is responsible for establishing GAAP in the United States. The U. S. Congress has charged the Securities and Exchange Commission (SEC) with the ultimate responsibility for authorizing GAAP for companies whose stock is held by the general investing public.

However, the SEC has informally delegated much rule-making power to the FASB. Congress can, however, overrule both the SEC and the FASB.

The International Accounting Standards Board (IASB) was established to develop, in the public interest, a single set of high quality, understandable, and enforceable global accounting standards.

The IASB sets International Financial Reporting Standards (IFRS). IFRS is used in more than 100 countries around the world, including all European Union countries. The IASB has 16 members who represent a diversity of geographic and professional backgrounds.

BASIC CONCEPTS (Economic) Entity - an organization that stands apart from other organizations and individuals as a separate economic unit ◦ The first line in the statements’ headings ◦ Personal transactions are not recorded by a business entity Stable Monetary Unit ◦ Currency is used to measure events ◦ Its purchasing power is assumed to be stable (low inflation) over time

BASIC CONCEPTS Going concern (continuity) ◦ Reporting entity will continue to exist indefinitely, i. e. can use historical costs to measure long-lived assets ◦ If liquidation is in sight, assets should be revalued to their current market value Materiality ◦ If it makes a difference to a decision maker, information should be separately identifiable ◦ Immaterial – combine with other information

BASIC CONCEPTS Cost-benefit ◦ Apply established criteria, i. e. U. S. GAAP or IFRS ◦ If the costs to comply with that criteria exceed the benefits of doing so, deviations are permissible ◦ Difficult to measure benefits – judgment which can easily lead to disagreements ◦ U. S. GAAP contains verbiage permitting deviations justified by cost-benefit considerations

BASIC CONCEPTS Reliability ◦ Management prepares and is rewarded by the content of financial statements (possible bias) ◦ Independent auditors, in theory, add quality to those statements by offering three opinions ◦ “Fair” presentation (unqualified) ◦ Prepared according to the relevant accounting standards ◦ Adequacy of internal controls ◦ Higher quality statements makes them more reliable (useful) in decision making

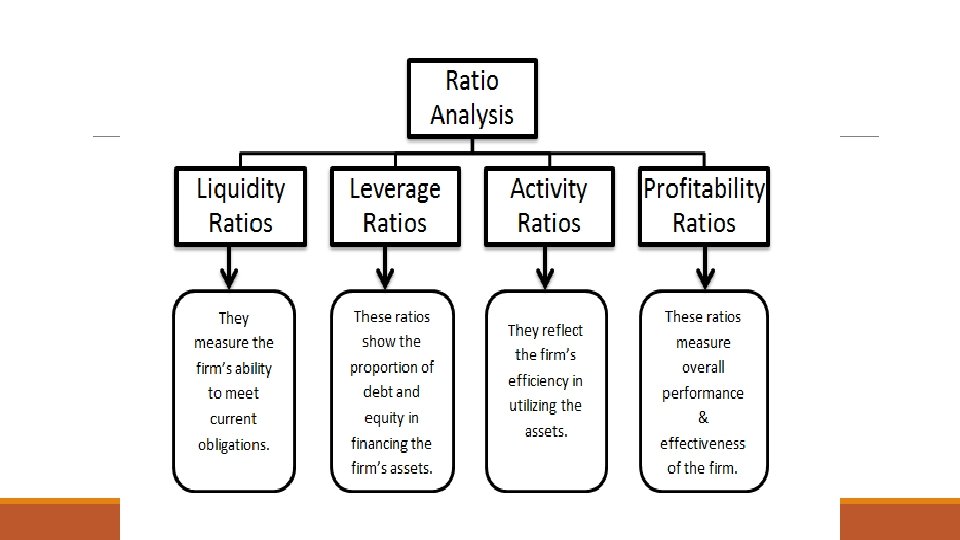

Ratios: Calculate ratios to reflect: profitability, liquidity, efficiency, gearing, investment;

Ratios: Comparison of these ratios both externally (other companies, industry standards) and internally (previous periods); interpretation of results